FLR - Fluor: The 'Hold' Stance Paid Off - A Better Valuation

Summary

- I wrote on Fluor almost 5 months back when the war in Ukraine was still a relatively new thing. At the time, I considered it a "HOLD".

- The company is theoretically appealing - but the valuation is the variable that needs to work in order for this to actually be attractive.

- For now, this is the problem with this investment. I see the industry as attractive, and this is my update on it.

Dear readers,

In this article, we're going to revisit Fluor Corp ( FLR ), a business I wrote about some months back. While the Oil & Gas sector has seen some attractive valuations and trends, it does not mean that every company here is an automatic "BUY". Indeed, since my last article, the company has actually underperformed the broader indexes and trends here.

Seeking Alpha Fluor Article (Seeking Alpha Fluor Article)

In this article, we update on the company and see what the upside based on the current valuation is. We also look at whether recent results have changed the thesis in any significant way.

Fluor - An Update

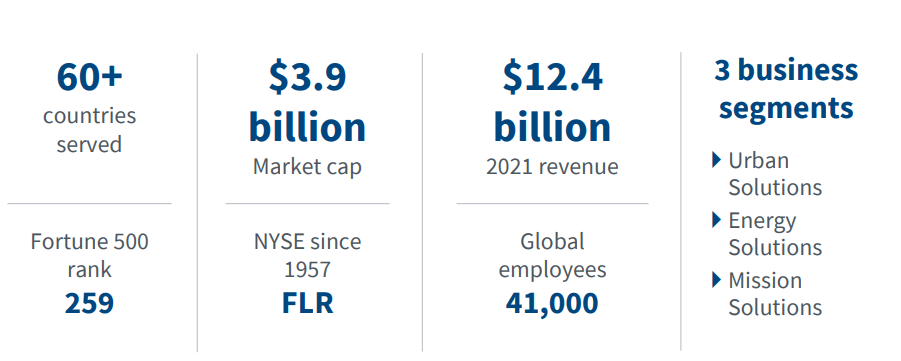

So, as I mentioned in my last piece on Fluor, the company is at its heart a holding company that owns subsidiaries as well as JVs, and through these, it's one of the larger professional service firms around, providing EPC, fabrication, and modularization services as well as project management on a global basis.

The end markets the company is active in are primarily found in fuels, LNG and various chemicals - but also nuclear, infrastructure, mining, metals and sciences.

Part of the pro-Fluor argument is the company's proximity to the US government - a partner for the business.

However, it lacks any dividend yield, is barely BBB anymore, and saw its earnings collapse during COVID-19. As I see it, it has little business trading at the level it did during the last article, and even during this article.

The company also has Fluor Constructors International, which is organized and operates separately from the rest of the businesses, and provides unionized management and construction services across North America for Fluor-specific projects. The construction business has refocused from volume of contracts to quality of contracts, which is a similar development to what we've seen in Europe during the past few years.

Recent results for the company have been good enough, considering the sort of macro we're currently in.

{kind=link}

The company worked hard to accelerate its ESG goals, but also achieved some hard contract wins, including 73% reimbursable contracts, the total contract volume amounted to $3.6B for the quarter alone, and 40% of them related to energy transition work.

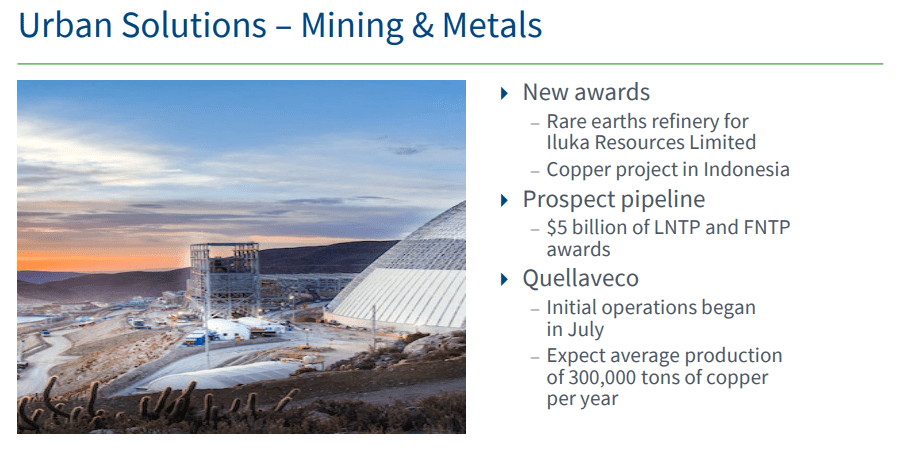

How good the company is working is fairly easy to put into mathematical terms. The company managed margins of 550 basis points above the new, planned ambition going forward, and despite overall slowdown continues to see strong demand for technical and construction services. All segments showed impressive trends, including new pipeline and refinery awards in the rare earth sector.

{kind=link}

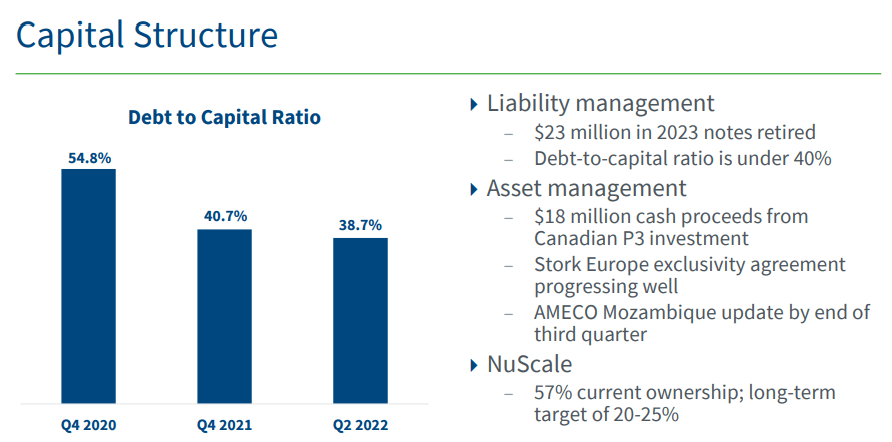

With good adjusted EBITDA, new massive awards, over $100M in segment profit and expected cash balances for the year to be around flat, the company is in decent shape. Fundamentals remain what I would consider "good enough" , with debt/capital down quickly from over 54% back down to under 39% in less than 2 years, essentially.

{kind=link}

In addition, the company's current updated outlook is positive. FLR expects an EPS at the maximum range of $1.35/share at this time, with an adjusted EBITDA of $380 to $430M, while maintaining segment margins of between 3.5-5%.

The company's expertise and world-class experience across multiple fields see it having massive advantages. The overall global post-pandemic recovery is not unlikely to have the company reverse its negative earnings trend. This is a necessity following the trends during 2020-2021, which saw EPS drop to actual negative levels.

I wrote in my last piece that governments are expected to shift to sustainable infrastructure and the energy transition as well as commodities, which directly ties into the company's operations and ambitions. There are strong pricing trends and signals throughout the commodities space, indicating massive upside for chemicals, mining, and other areas. This is currently materializing, with the company's share of sustainable investments increasing significantly.

The company is also delivering significant progress on its strategies and new goals.

{kind=link}

And the company has multiple levers to pull in order to both position itself and to be an attractive partner for the clean energy transition that seems to be clearly ongoing here.

{kind=link}

Worries for the quarter, and risks? Inflation and trends are giving rise to project uncertainties and confidence levels for clients, translated through notices. The potential recession generally speaking gives rise to some of these uncertainties - but it's equally important to remember that generally speaking, Fluor has stayed very profitable even in a recessionary sort of environment.

It's also about hedging inflation and costs, which the company handles by locking in commitments with suppliers. This brings risks to contracts where things aren't locked in, but where the company has commitments that might have to be met at a loss. Aside from this legacy risk, the company is now extremely picky with the sort of infrastructure projects it works on. It also works by having the client take quantity responsibility, like with a recent project the company is delivering.

For example, the recent I-35, East South Austin award on that project, the client takes all quantity responsibility.

(Source: David Constable, Fluor Earnings Call 2Q22)

Like with any construction company, there are ways in which revenue flows through the company when we're talking about multi-billion dollar infrastructure projects. This is an entire article in itself for an important quality that needs to be understood if you're serious about investing in the sector. However, none of these are things that the company isn't somehow experiencing anyway or in other cases.

In the end, Fluor is a play on various infrastructure markets. These markets are generally positive, but they can come at a bit of a risk when things go up and down - and especially when pricing for raw materials and components starts to fluctuate. It pays off to follow the company when this is the case to make sure that your investment is properly safeguarded.

That's what we're going to do here.

Fluor - The Updated Valuation

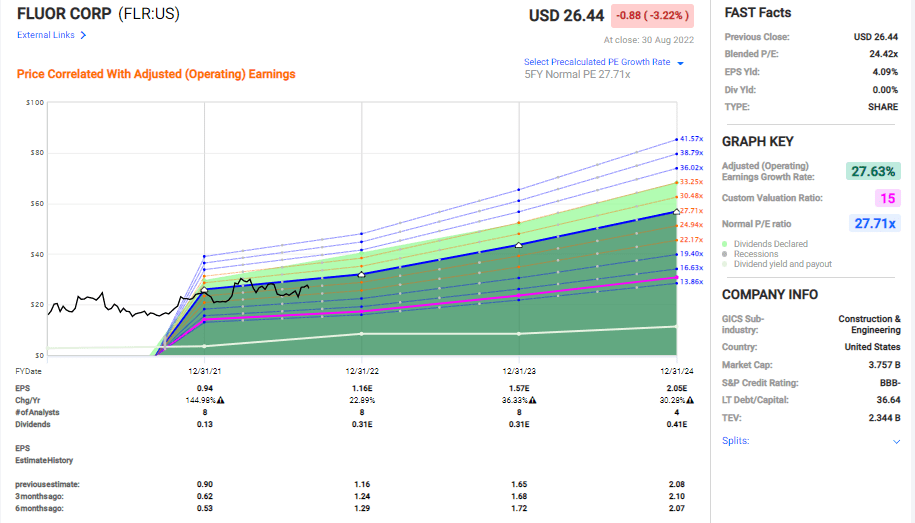

So, the company's earnings cratered during the COVID-19 crisis. Since that time, we've seen an impressive recovery, and the company is on track to deliver some decent EPS growth for the foreseeable future - the next 3 years are expected to see around 27% average annual EPS growth, with 22% during this year.

Fluor Valuation (F.A.S.T grpahs)

{kind=link}

Fluor is, without a doubt, a bit of a high-risk investment. Not because the company is in a threatened position in terms of survival, but because of the relative historical volatility this business sees. Even these forecasts aren't exactly certain, and it wouldn't be unfair or wrong to say that this company has already recovered to a level where, on a 2021-2022E EPS level, it has reached the valuation that it should be, based on historical multiples.

Still, an upside can exist - even for Fluor, and even at this valuation. If we consider the premium likely and consider EPS growth likely, then even a 20-22x P/E multiple on a forward basis gives us no less than a 20.15% annual RoR - and that is based on a 19.4x P/E. Well below the 5-year average of 27x.

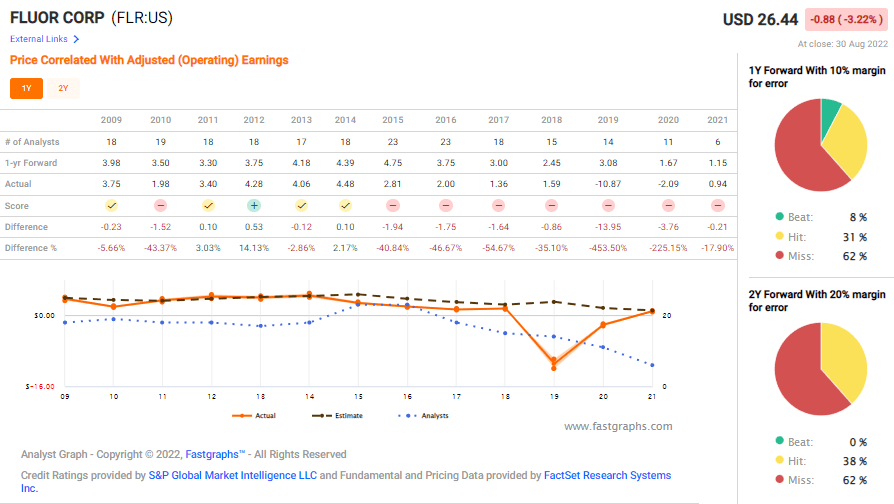

However, at the same time, the yield is currently zero. While the company is expected to restore the payout at a low level, this isn't anything to write home about just yet. Also, the forecast accuracy for this company for the past 7 years has been absolutely abysmal.

F.A.S.T graphs Forecast accuracy (F.A.S.T graphs/FactSet)

{kind=link}

There's a massive amount of forecast uncertainty to the company when you look at the forecast success ratio - meaning it's more than a 50% negative miss ratio for forecasting the company's EPS.

Investing in a business like this takes a very strong stomach and high conviction. I know these sorts of businesses as I've been investing in them for years. They're businesses like Skanska ( SKSBF ) and NCC AB, both construction companies with very similar trends.

In my last article, I said it was not the best time to invest in Fluor based on valuation. I would say that today, we're at a better, but still not at a good valuation to do so.

Why?

Because there are many better investment options out there, based on the qualities of:

- Fundamentals, including but not limited to credit rating.

- Dividend Yield, coverage, and dividend tradition.

- Overall conservative upside and forecast accuracy.

So, why on earth should I, with my hard-earned capital on hand, invest in Fluor, when there are companies that without a doubt have these far better qualities?

The upside is between 20-30% here based on a forward P/E ratio of 20x. This is a definite improvement on the last thesis. However, given that the company already trades at 27x today, the upside is based primarily on earnings growth. And given how low the accuracy ratio is for this, I don't consider this a very strong case to make.

It's possible, but the low EPS visibility and the current zero dividends make this a weak case in my book. Investing in a 27x P/E stock at this time, with this volatility, isn't something I'd do.

S&P Global's targets for the company are interesting - because they agree with this assessment. Usually, S&P Global targets are exuberant. In this case, they're no higher than $26/share, meaning according to analyst targets, this company is slightly overvalued. At this valuation, only 1 out of 9 analysts have a "BUY" target - the rest are at "HOLD".

Fluor as a company is an interesting business - and potentially an appealing one. This is the case with most construction businesses because they provide very crucial overall services to societies, businesses, and governments as a whole.

But, as with all things, you need to buy them at the right price. A real estate investment at a 1-2% cap rate? That's not going to happen, almost regardless of the geography or specifics.

6-9% cap rate? Now we're talking - and I could even swallow sub-par geography provided that the other indicators line up.

It's all about valuation.

If the company drops below $25.90/share , then I would consider this company a "BUY" - but even then, it would only be a buy-in of what I would consider a "vacuum". And that's not really how the market works.

So with that said, I call this company a "HOLD" even now.

Thesis

Here is my thesis on Fluor:

- Fluor has a similar problem to most construction and engineering companies. They're great companies - and I do mean great companies to invest in during an upswing.

- However, when and if these companies go into the doldrums, they can stay there for several years, and once earnings crash, they can do so to negative levels and be there for several years as well. This is more or less what happened to some of those construction companies I invested in.

- For now, I remain tepid on this company - my PT is $25.9 and I'm at a "HOLD" here.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

If you're interested in significantly higher returns, then I'm probably not for you. If you're interested in 10% yields, I'm not for you either.

If you, however, want to grow your money conservatively, and safely, and harvest well-covered dividends while doing so, and your timeframe is 5-30 years, then I might be for you.

Fluor is a "HOLD" here due to poor valuation and some lacking qualities

Here are my criteria and how the company fulfills them (Bolded):

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

For further details see:

Fluor: The 'Hold' Stance Paid Off - A Better Valuation