FFIC - Flushing Financial: 'Buy' Based On Balance Sheet But Earnings Could Disappoint

2023-05-25 10:30:00 ET

Summary

- Flushing Financial Corporation's balance sheet and access to liquidity look great, but the net interest margin continues to decrease.

- This will put pressure on the net earnings.

- The dividend of $0.22/share will likely be covered in the next few quarters, but I'd personally prefer the bank to forego dividend payments.

- That's an unpopular opinion, and Flushing Financial will likely maintain its dividend.

- With Flushing Financial Corporation trading at about 0.5x tangible book value, the stock is not expensive, but expect a sub-$1 EPS this year.

Introduction

In December of last year, an investment in Flushing Financial Corporation ( FFIC ) seemed like a good idea . The New York focusing bank had a robust loan book with exposure to low-LTV residential mortgages in New York. Notwithstanding the issues in the region, I thought owning mortgages with an LTV ratio of less than 40% should be pretty safe. Everything changed in March, when the U.S. regional banking sector was shaken up, and Flushing Financial didn't escape the volatility.

Profitable, but let's keep an eye on the continuous net interest margin pressure

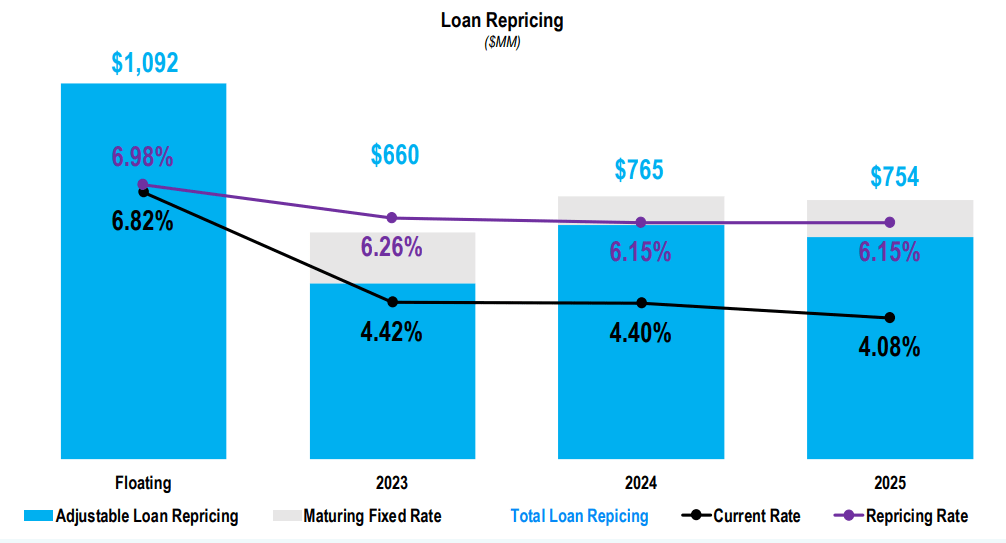

In my December article, I was expecting the increasing interest rates on the financial markets to boost Flushing's net interest income, but the market was warned this would likely go slower than expected. Only $1.03B of the loan book had a floating rate, while only $994M of loans was slated for repricing in 2023, followed by $785M in 2024. This means that while Flushing Financial would immediately feel the impact of the higher interest rates, it would have to start paying on deposits, and it would only gradually see its interest income increase as well. As fellow analyst Sheen Bay Research explained , the earnings were likely to decrease in 2023 due to the different pace in paying higher interest rates on the deposits and actually receiving higher rates on its outstanding loan book.

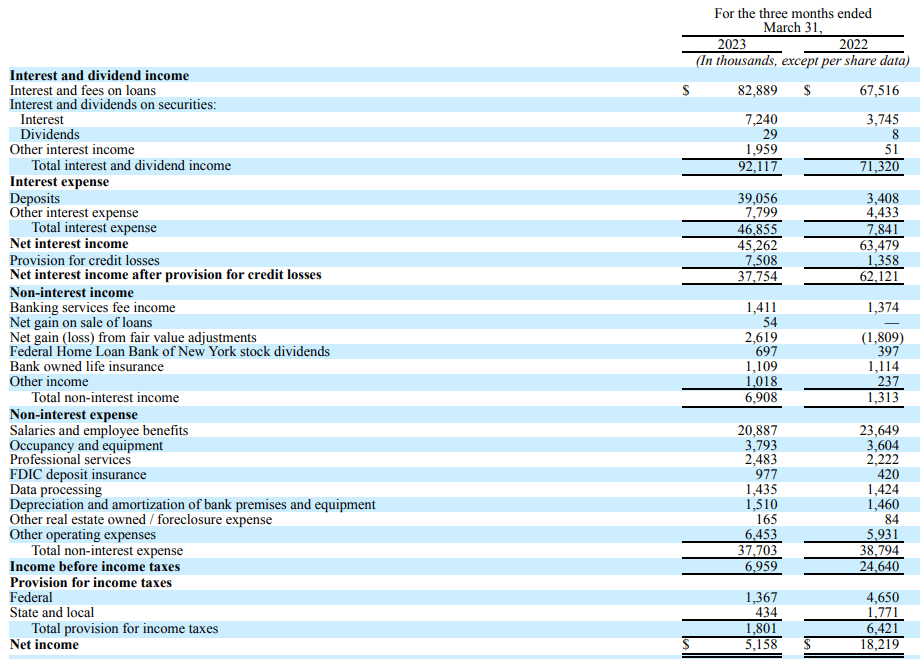

Unfortunately, the result in the first quarter of this year was even worse than I expected. Sure, the interest and dividend income increased by approximately $21M compared to the first quarter of last year, but the interest expenses on the deposits more than ten-folded to almost $40M. The total amount of interest expenses increased from less than $8M to almost $47M. And that's worse than I expected.

{kind=link}

This resulted in a rather substantial decrease in the net interest income, which fell from $63.5M to $46.9M. Fortunately, I do think the worst will soon be behind us, as it doesn't really look like interest rates on deposits will increase by too much from here on while every quarter more loans of the loan book will be repriced into higher-yielding loans. We already see a slow increase in the yields on the interest-earning assets. These increased from 4.11% in the loan portfolio in Q1 2022 to 4.83% in Q1 2023 . The total average of all interest-earning assets increased from 3.77% to 4.61% in the same time frame. Unfortunately, the average interest rate on the deposits and other interest-bearing liabilities increased from 0.5% in Q1 2022 to 2.80% in Q1 2023.

That being said, the evolution will be slow. Increasing the average interest by 200 basis points on the $660M that has to be repriced this year will only add about $13M in interest income. The 175 basis points in 2024 will add another $13M, which means Flushing will likely need all the way until the end of 2025 to get its net interest income back up to last year's levels.

{kind=link}

There is a silver lining, though. The current banking crisis is a liquidity-related crisis, and it looks like Flushing doesn't have too much to worry about as it actually saw an inflow in deposits. As of the end of March, the bank had about $5.78B in interest-bearing deposits, up from $5.52B as of the end of last year. While that's great, it also means there is a "lag" while Flushing is deploying the cash. The balance sheet does show there is an increase in cash and securities available for sale on the balance sheet, while the bank also reduced its FHLB advances from $815M to $652M.

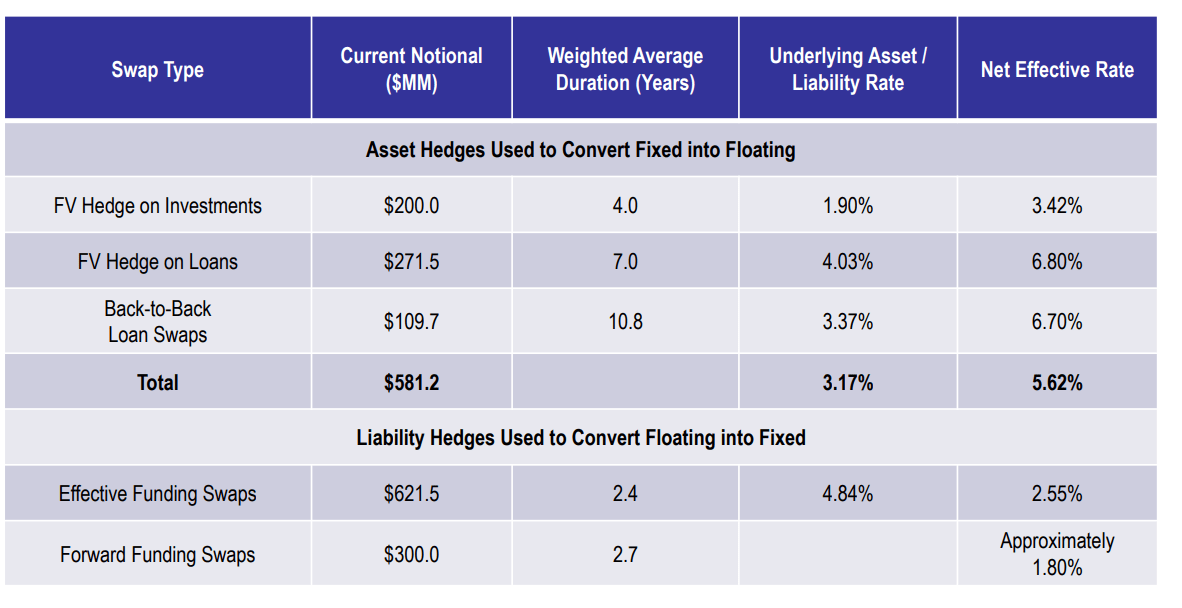

The bank has also taken steps to reduce its sensitivity to the interest rate levels. These swaps aren't the Holy Grail but will help to narrow down the duration gap between assets and liabilities and make the situation more manageable.

{kind=link}

Despite these measures, the results in 2023 will likely remain under pressure. The net income in the first quarter of the year was just $5.2M for an EPS of $0.17, but this was also due to higher loan loss provisions (which increased to $7.5M in Q1) which was related to one charge-off on a loan where the problems were identified about a year ago. Excluding this element, the net income would likely have been approximately 60-70% higher with an EPS of $0.27-0.30, which means the dividend of $0.22 per share would still be fully covered on an underlying basis. I expect the loan loss provisions to decrease in the subsequent quarters, but that's not a guarantee the EPS will increase as the net interest margin will likely see additional compression throughout the year.

That being said, the collapse of New York based Signature Bank could create some opportunities for Flushing. From the Q1 conference call :

We increased deposits by nearly $250 million during the quarter. Our liquidity is over three times the uninsured and uncollateralized deposits. Customer experience and our ties to the communities are also key to our success. Due to a major competitor, Signature Bank, leaving the market, additional opportunities are emerging, particularly with shared relationships.

Investment thesis

Flushing Financial is a double-edged sword. I think its real estate loan book with an LTV ratio of less than 40% is safe while the bank is flush with cash and liquidity (pardon the pun). The inflow of deposits means the bank should not be a victim of a liquidity crunch (it has access to $3.7B in liquidity), but the downside is obvious: There is a lag between repricing the loan book and having to pay higher interest rates means the net interest margin will likely continue to decrease.

During the first quarter, Flushing's average cost of deposits was still just 2.80%. This will likely continue to increase, and this will likely also happen at a faster pace than the loans are being repriced, so I am NOT expecting the net interest income to start to trend upwards in the current financial year. 2023 will be a year of damage control. In an ideal world, Flushing should cancel the dividend, but I realize that would not only be a very unpopular suggestion, it would also reduce the confidence of its depositors in Flushing Financial. This means Flushing is between a rock and a hard place.

From a balance sheet perspective, I don't see any major issues. Flushing has access to liquidity and perhaps even too much liquidity as there was a net inflow of deposits. Meanwhile, the stock is now trading at a discount of approximately 50% to its tangible book value (the TBVPS was $22.18 as of the end of Q1), which makes FFIC appealing from a fundamentals perspective. But the earnings this year will likely be abysmal, and I don't expect to see an EPS in excess of $0.80. 2024 could be more promising, as more loans will be up for repricing, but it will take years before we see the $2+ EPS from the past few years again.

I have a long position in Flushing Financial Corporation. I think the bank still is a buy from a fundamentals perspective (balance sheet strength), but I don't expect this year's earnings to come in above $0.85 while the 2024 EPS will likely remain below $1.25. I'm a moderate buyer of Flushing Financial Corporation stock at these prices, but I'm not a big fan of the cash dividend right now.

For further details see:

Flushing Financial: 'Buy' Based On Balance Sheet, But Earnings Could Disappoint