PSFE - Flywire: Still Too Hot For Payments Sector

2023-03-06 07:18:01 ET

Summary

- Flywire reported another impressive quarter with revenues beating estimates and growing 42%.

- The company has traded at a premium valuation since completing a hot IPO back in 2021.

- FLYW stock valuation isn't too stretched, but Flywire isn't as appealing as other payment plays.

While the global economy struggled during 2022, Flywire ( FLYW ) reported a blockbuster year. The company operates in the global payments sector with a focus on the education and healthcare verticals that saw strong rebound in 2022. My investment thesis is still Neutral on the stock due to an elevated valuation from a traditional IPO.

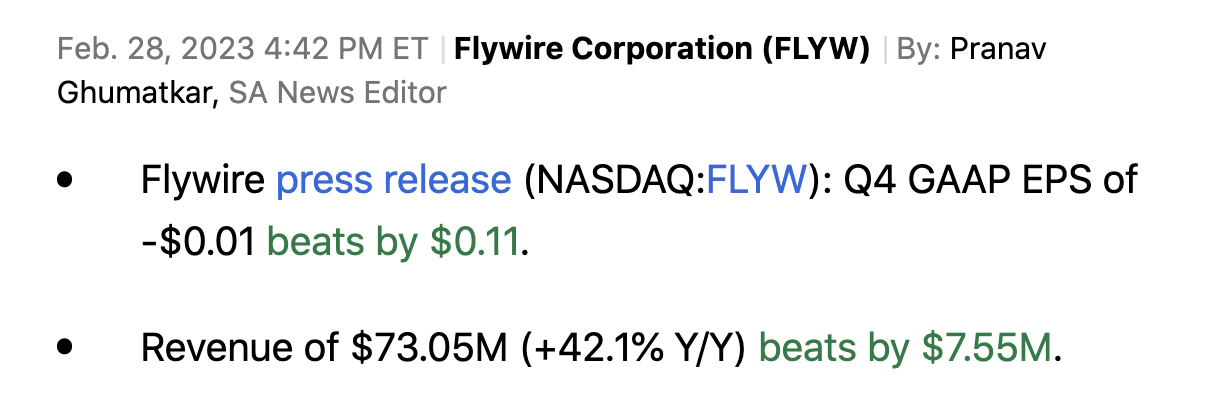

Source: Finviz

Smashing Estimates

Flywire went public back in 2021 and the payments company has done nothing but smash analyst estimates during that period. For Q4'22, the company beat revenue targets by $7.6 million:

{kind=link}

The education and travel verticals saw a huge rebound in demand, sending payment volumes to record levels. Not to mention, the acquisition of Cohort Go added strong revenues to the education vertical allowing international students to make cross-border tuition payments.

As with most payments firms, Flywire benefits from existing clients driving higher volumes while new clients build upon this existing expansion. In addition, the company expands the payments network into new countries, including Mexico and Nepal, while also building new products, such as a comprehensive receivable solution.

{kind=link}

In fact, the pre-2019 customer cohort grew NRR by 25% in 2022 alone. Flywire didn't even need to add new clients last year in order to produce growth far in excess of the market.

Strong Outlook

Flywire doesn't provide any indication growth is about to slow. The company guided to Q1'23 revenues of $88 million for not only a big beat from analyst estimates at $82 million, but the target is for ~40% growth.

{kind=link}

On the negative side, the company only guided to 2023 adjusted EBITDA of $31 million. The whole market has strayed away from limited profit companies, yet this stock still trades at a $3.0 billion market cap, or nearly 100x EBITDA targets.

Flywire is forecasting a doubling of adjusted EBITDA in 2023 after reporting $15 million last year. The company has a massive global payments opportunity and expansion into new verticals like travel and B2B A/R comes at a cost to current profits.

The global payments company went public back in 2021 at an IPO price of $24 . Unfortunately, investors learned another tough less about the difference between an IPO and SPAC.

While the market initially loved the IPO sending Flywire to a high above $50, the stock has gone nowhere but down during 2021 and the weak market of 2022. The problem all along was the stretched valuation considering the company reported another brilliant quarter with revenues surging 42%.

A lot of other payment companies went public via SPACs and the related stocks plunged and haven't rebounded. Stocks such as Payoneer Global ( PAYO ) and Paysafe ( PSFE ) trade around a forward EV/S multiple of 2x after completing SPAC deals versus up at 7x for Flywire. Even Paymentus Holdings ( PAY ) was a fellow IPO, but the stock trades similar to a SPAC unlike Flywire.

While Flywire isn't too bad of a deal with their reported growth rates, the payments firm isn't a bargain like the general payments group discussed above. In addition, the stock has massive downside risk on any scenario where growth rates fail to meet targets.

Paysafe has struggled since going public, but both Payoneer and Paymentus reported revenue growth topping 25% in the last few quarters. Clearly, Flywire has produced the fastest growth during the last couple of years, but the fintech doesn't have the excess growth to warrant the premium multiple.

Takeaway

The key investor takeaway is that Flywire offers investors an attractive business model. The business is slowly becoming adjusted EBITDA profitable making the stock appealing. Though, so many other payment stocks have underperformed in the last couple of years that the appeal of buying Flywire near the yearly highs has less interest with many other better deals around.

For further details see:

Flywire: Still Too Hot For Payments Sector