VWO - FM: Why I Am Not A Buyer

2023-10-22 05:04:48 ET

Summary

- iShares Frontier and Select EM ETF is an actively managed ETF that provides exposure to frontier and select emerging market equities.

- FM has a high management fee of 0.80% and is highly concentrated in terms of geographic exposure with over 30% of assets invested in Vietnam.

- FM appears cheap when considering the trailing PE ratio of 9.1x but that does not tell the full story as FM is mostly invested in low valuation sectors.

- FM has significant exposure to countries which may be impacted by the ongoing geopolitical challenges in the world.

- I am initiating coverage of FM with a sell rating.

ETF Overview

The iShares Frontier and Select EM ETF ( FM ) seeks to provide investors with actively managed exposure to frontier market equities along with select emerging market equities. FM is managed by BlackRock ( BLK ) and currently has ~$574mm in net assets.

FM holds 159 stocks, trades at a trailing PE ratio of 9.1x, a price to book ratio of 1.59x and offers a current dividend yield of ~2%.

High Management Fee

FM has an expense ratio of 0.80% which I view as fairly high in the ETF space. Comparably, the Vanguard FTSE Emerging Markets ETF ( VWO ) has an expense ratio of just 0.08% while the MSCI Next Emerging & Frontier ETF ( EMFN ) has an expense ratio of 0.55%. As an investor I work diligently to avoid high active management fees given that active managers have struggled to outperform over long periods of time.

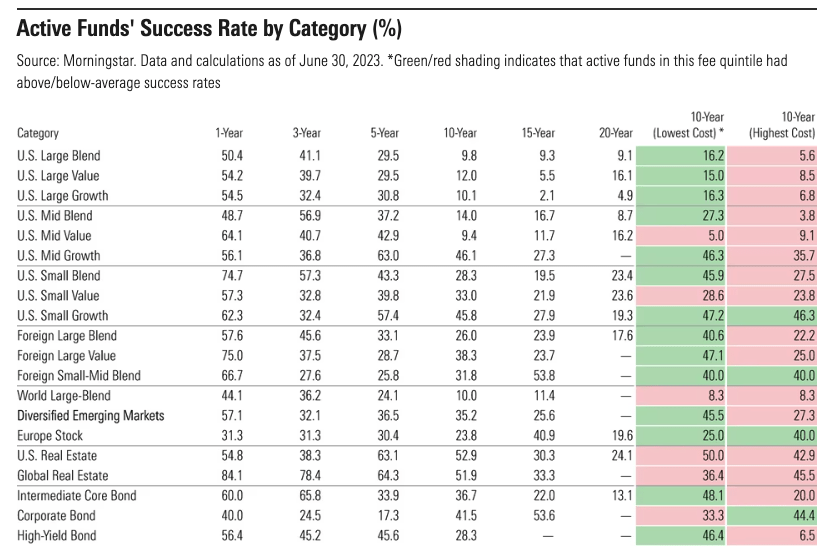

As shown by the chart below, just 25.6% of active managers in the diversified emerging markets category have outperformed over the past 15 years while 35.2% have outperformed over the past 10 years.

{kind=link}

Lack of Geographical Diversification

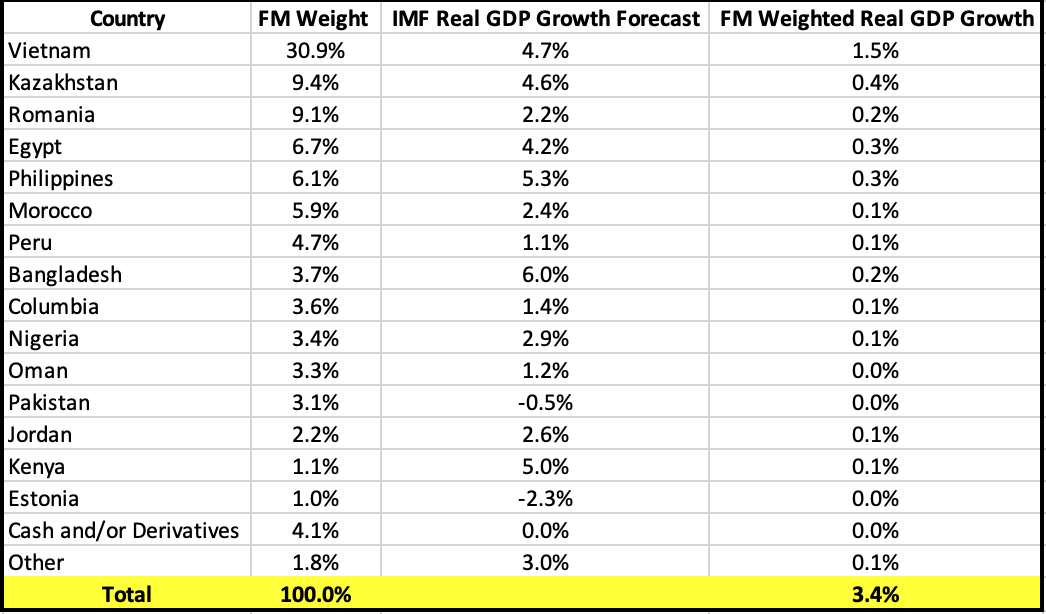

As shown by the geographic concentration table below, FM is highly concentrated with over 30% of fund assets invested in Vietnam and over 9% of fund assets invested in Kazakhstan and Romania each.

Given the relatively high risk nature of the countries in which FM is investing, I would prefer to see a more diversified exposure. High exposure to a single country heavily exposes investors to country specific political and environmental risks.

iShares

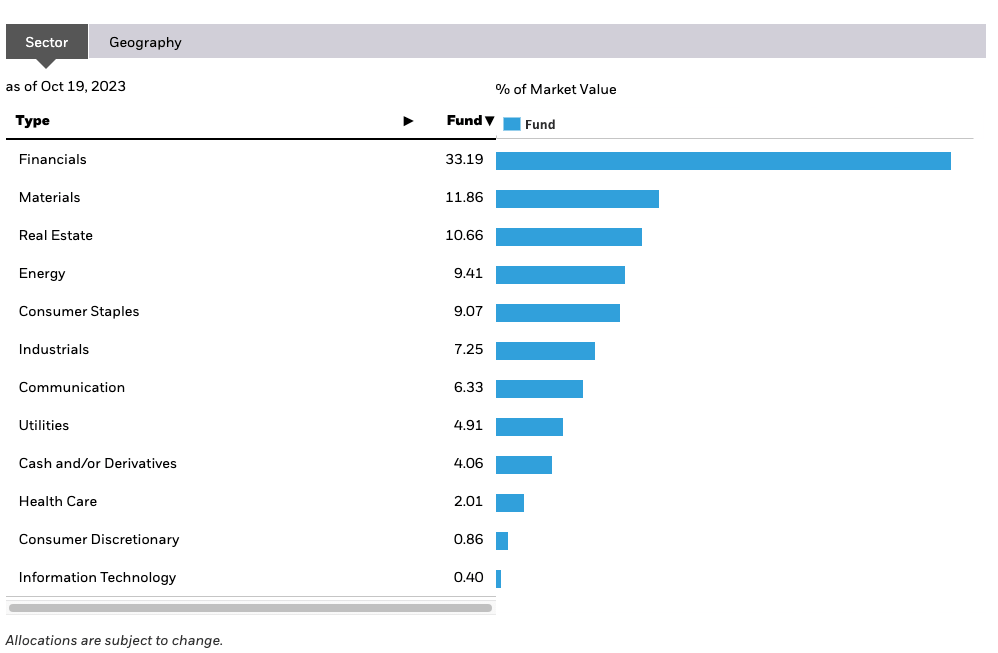

High Allocation to Financial Sector

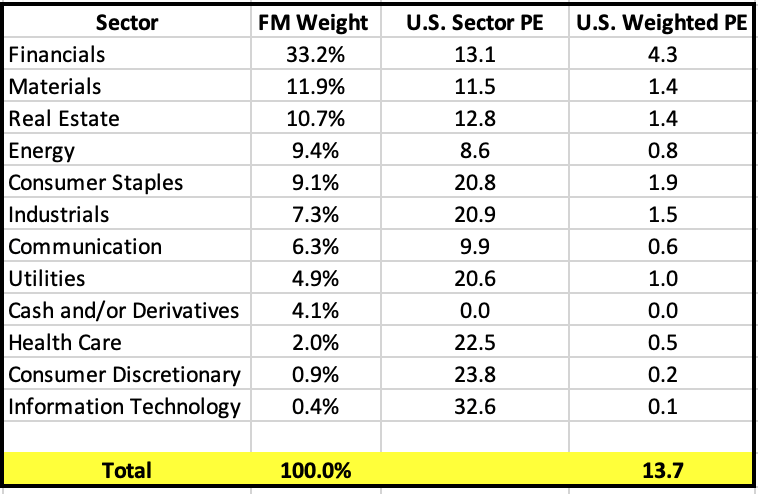

As shown below, FM has a 33% allocation to financials and a 11.8% allocation to the materials sector. While the on the surface the 9.1x PE ratio seems cheap compared to 21.8x for the S&P 500, on a sector adjusted basis the story is very different. When applying the FM sector allocations to the U.S. sector PE ratios, as is shown in the analysis below, the U.S. weighted PE comes to 13.7x. Thus, on a comparative basis FM is not nearly as cheap as it appears.

{kind=link}

{kind=link}

Economic Growth Prospects only Marginally Better than U.S. Economy

The IMF projects U.S. Real GDP growth for 2023 to come in at 2.1%. Below are the IMF Real GDP Growth rates for the countries in which FM is invested note that the world growth rate of 3% has been used for the "other" holdings.

The weighted Real GDP Growth rate for the FM portfolio is just 3.4% which is only marginally higher than the U.S. growth rate of 2.1%. For this reason, I believe it is hard to argue in favor of investing in highly risky countries that FM is current invested in as the growth differential is marginal at best.

{kind=link}

Weak Historical Performance

Since its inception in 2012, FM has significantly underperformed the S&P 500. FM has returned ~39% compared to 264% by the S&P 500 during the same period. FM has also significantly underperformed the S&P 500 over more recent time periods including the past 3 and 5 years.

One bright spot for FM is that is has managed to outperform emerging markets since inception. I believe part of that outperformance is due to the fact that FM has not been heavily in China as Chinese equity exposure has hurt broader emerging market indexes.

High Risk Global Geopolitical Environment

The global geopolitical outlook is very challenging right now. The war between Ukraine and Russia as well as the war between Israel and Hamas have threatened to destabilize the world order. FM has closed to 9% of its assets invested in Egypt and Jordan which could prove extremely risky in the event of further instability in the middle east. FM also has more than 9% of its assets invested in Kazakhstan which borders Russia and has already been impacted by the war in Ukraine. Moreover, strained relations between the U.S. and China has created additional risk. Given this, I believe now is a time to focus on more defensive investment opportunities and frontier markets do not fit that bill.

Conclusion

FM represents a relatively unique ETF as it is one of the few ETFs currently on the market that allows investors to access frontier markets. However, FM charges high management fees and is highly concentrated in terms of geographic exposure. While the trailing PE ratio of 9.1x seems cheap on the surface compared to the 21.8x PE of the S&P 500 the difference is much smaller once adjusting for differences in sector exposure. While the countries in which FM is invested in are forecast to grow faster than the U.S., this difference is relatively small. FM is currently invested in a number of countries that have a significant potential to be highly impacted by the ongoing wars in Ukraine and Gaza. For these reasons, I believe investors should avoid investing in FM.

For further details see:

FM: Why I Am Not A Buyer