FMX - Fomento Economico Mexicano: Refocusing On Its Core Business Seems Promising

2023-11-01 05:22:04 ET

Summary

- FEMSA operates highly stable businesses throughout Mexico and Latin America, such as convenience stores, pharmacies and a bottling company.

- The company had diversified into segments such as Logistics, investments in Heineken and other segments that had little to do with its core business.

- They have recently decided to focus only on their retail consumer business, which seems positive because it will mark a clear direction in which to head.

- A sum-of-the-parts valuation shows us that the company could be undervalued.

Investment Thesis

Fomento Económico Mexicano, or FEMSA ( FMX ), has established an empire in Mexico and Latin America, with its various businesses integrated into the country's economy, covering a range of essential consumer segments.

As a substantial business conglomerate, they had been diversifying extensively, potentially losing a clear sense of direction. However, they have recently been announcing divestments to refocus on their core retail consumption business.

In this article, we will explore the businesses that constitute FEMSA, assess their value, and provide justification for why I believe the strategic shift, in conjunction with the valuation, presents an entry point.

Price Return vs S&P500 (Seeking Alpha)

{kind=link}

Business Overview

FEMSA is a leading Mexican multinational company with operations in various sectors, including beverage production and convenience stores.

FEMSA is well-known for its significant involvement in the beverage industry. It owns a majority stake in Coca-Cola FEMSA, one of the world's largest franchise bottlers of Coca-Cola products. In addition to its beverage operations, FEMSA also operates its flagship, OXXO, a chain of convenience stores widespread throughout Mexico and other Latin American countries, boasting enormous brand power.

The company has a diverse range of interests and investments and has been involved in various industries, including logistics and real estate. Below, we will explore in-depth all the businesses that this conglomerate encompasses.

{kind=link}

Coca-Cola FEMSA

Coca-Cola FEMSA is responsible for producing, distributing, and selling Coca-Cola products in various countries in Latin America. It operates independently but under a franchise agreement with The Coca-Cola Company (NYSE: KO ). This partnership allows KO to access local expertise and resources, reduce costs, and expand its market presence while focusing on its core strengths in marketing and brand management.

This business relationship started in 1991, and it appears unlikely to end soon. However, it's evident that the greatest risk for this segment of FEMSA is its dependency on The Coca-Cola Company. The Coca-Cola Company provides the recipes and products, and losing this relationship would leave FEMSA without any products to offer and a large number of unused bottling plants.

Coca-Cola FEMSA Footprint (FEMSA)

{kind=link}

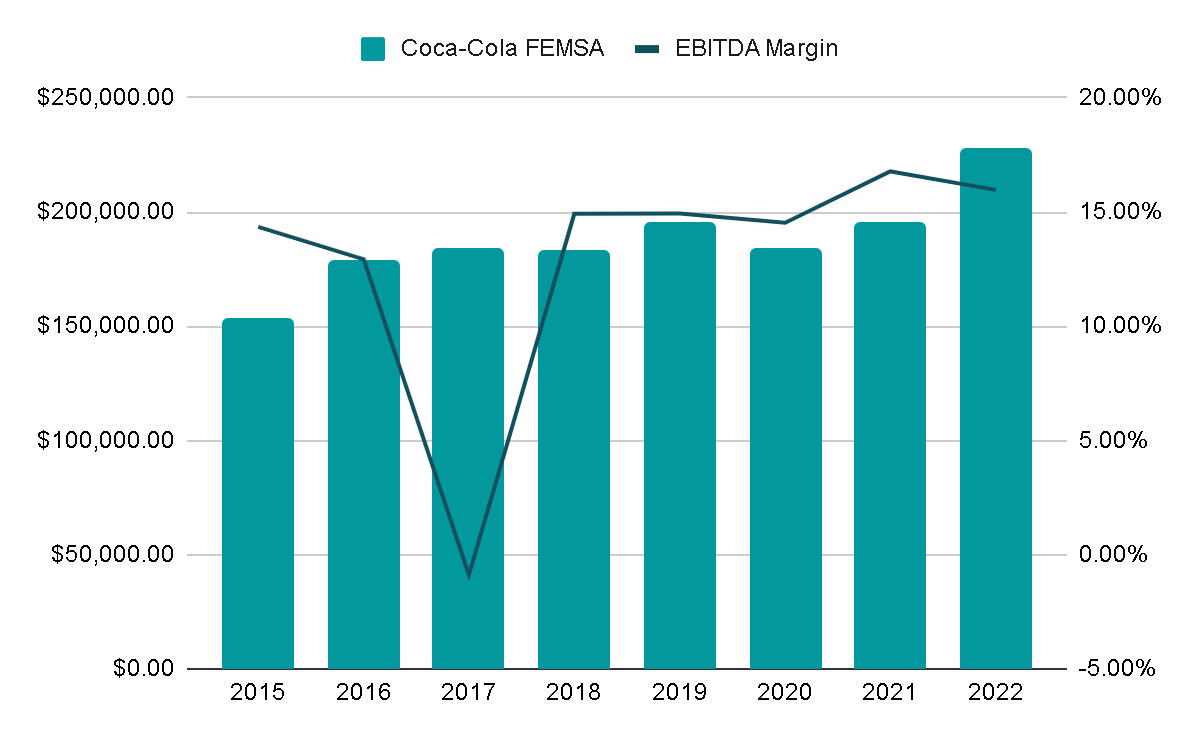

A few years ago, this segment used to have the greatest weight in sales, but as the company has generated new sources of revenue, this segment now represents 33% of total revenues. It has also experienced the slowest growth between 2015 and 2022, with a slight annual growth rate of 5.8%. Nevertheless, this segment serves as a 'cash cow' with stable income, enabling FEMSA to invest in other lines of business.

Another positive aspect is that the EBITDA margins of this segment are the highest in the entire conglomerate, currently at 16%. Therefore, even though it represents only a third of the revenues, it contributes half of the total EBITDA.

Coca-Cola FEMSA Revenue and Margin (Author's Representation)

{kind=link}

Proximity Stores

This is where the convenience stores called ' OXXO ' are located, which follow a concept similar to businesses like Circle K in Canada or 7-Eleven in the US. On average, an OXXO store covers around 106 square meters of retail space, not including areas designated for refrigeration, storage, or parking. These stores typically stock an average of 3,275 different products across 29 main product categories. Additionally, OXXO stores provide electronic and individual payment services, such as account deposits and cash withdrawals, remittances, and money transfers between stores. They also offer bill payment services, including payments for household electricity bills and cable television, among others.

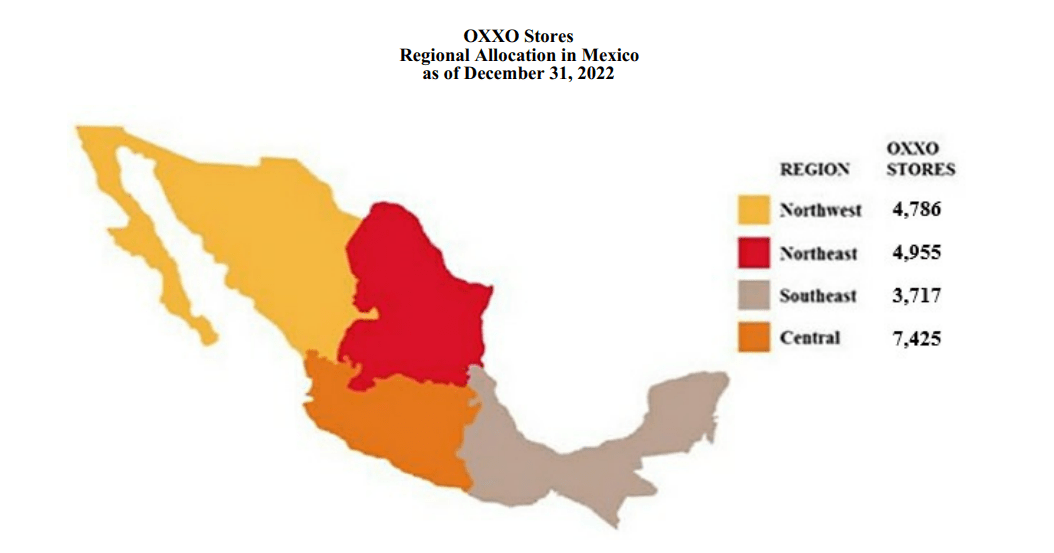

As of July 2023, the company reported that there are 21,000 OXXO stores in Mexico alone . To provide a comparison, in the United States, there are 19,400 Dollar General stores, 16,200 Starbucks locations, and 13,600 McDonald's restaurants. The footprint of these convenience stores is gigantic and their brand is well known throughout the country.

While there is still room for growth in Mexico, the company has already begun its geographical expansion . In 2009, they expanded to Colombia where there are currently 231 stores. In 2016, they entered the Chilean market (270 stores). In 2018, they expanded to Peru (75 stores). In 2020, they entered the Brazilian market (217 stores). Additionally, in 2022, they initiated their expansion into Europe through the acquisition of Valora, a convenience store chain with nearly 2,700 points of sale in countries such as Switzerland, Germany, Austria, Luxembourg, and the Netherlands.

{kind=link}

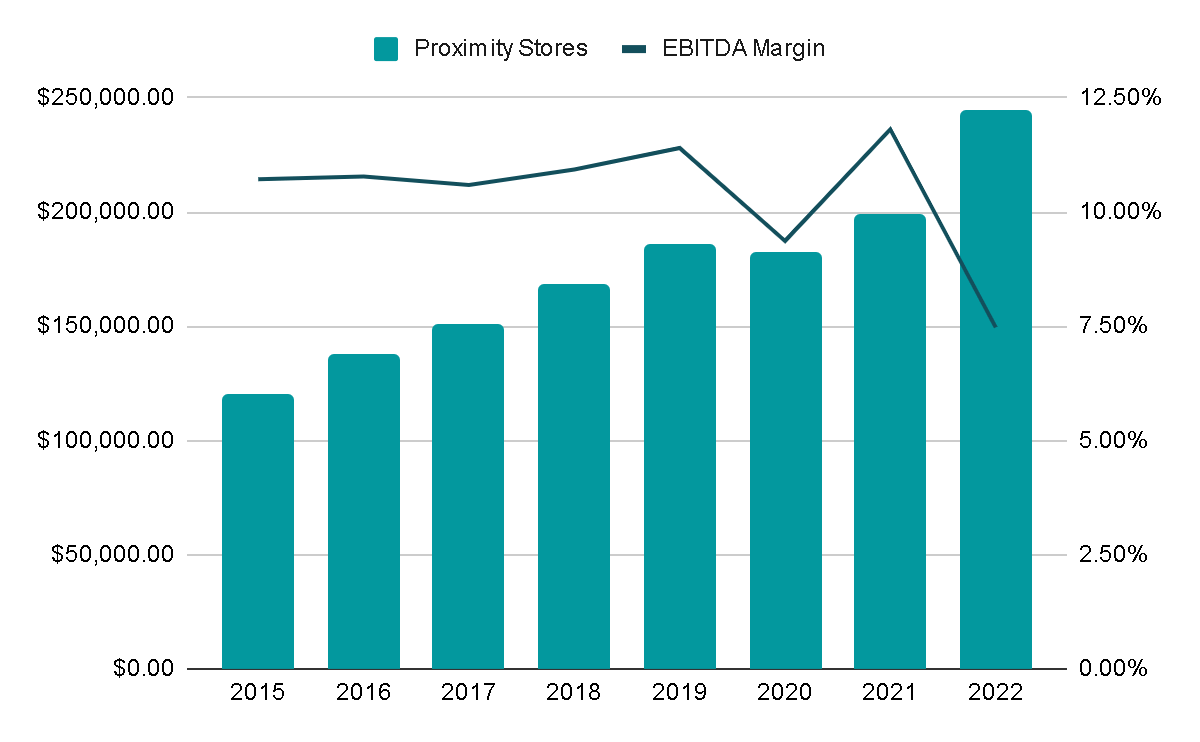

The revenues of this segment have been growing at an annual rate of 10% since 2015. In FY2022, growth accelerated, primarily due to the acquisition of Valora, and year-to-date (YTD), the growth rate for this segment has reached 20%. EBITDA margins typically hover around 11%, making it one of the company's strongest segments in terms of both growth and profitability.

Proximity Stores Revenue and Margin (Author's Representation)

{kind=link}

Health Stores

The Health Division operates pharmacy services locations with a concept similar to that of CVS or Walgreens in the US. Currently there are about 4,100 points of sale in Mexico, Chile, Ecuador and Colombia.

This segment was born with the idea of ??consolidating the fragmented health market in Mexico. To give an idea of ??the fragmentation of the market , FEMSA competes through its brands Farmacias YZA, Moderna and Farmacon, however, there are other strong competitors in the country such as Farmacias Similares, Farmacias Guadalajara, Farmacias del Ahorro, Farmacias Benavides or Farmacias San Pablo. And these are only the ones that I know as a Mexican who lives in the country.

While businesses of this nature typically enjoy steady and recession-resistant revenues , I believe that FEMSA might encounter significant challenges in establishing a prominent presence within this sector. A 2022 survey revealed that no FEMSA brands made it into the Top 5 of preferred pharmacies among Mexicans. Farmacias del Ahorro, of which Walgreens maintains a stake in, secured the second spot, while Farmacias Guadalajara, owned by Corporativo Fragua and listed on the Mexican stock exchange, claimed the number one position.

{kind=link}

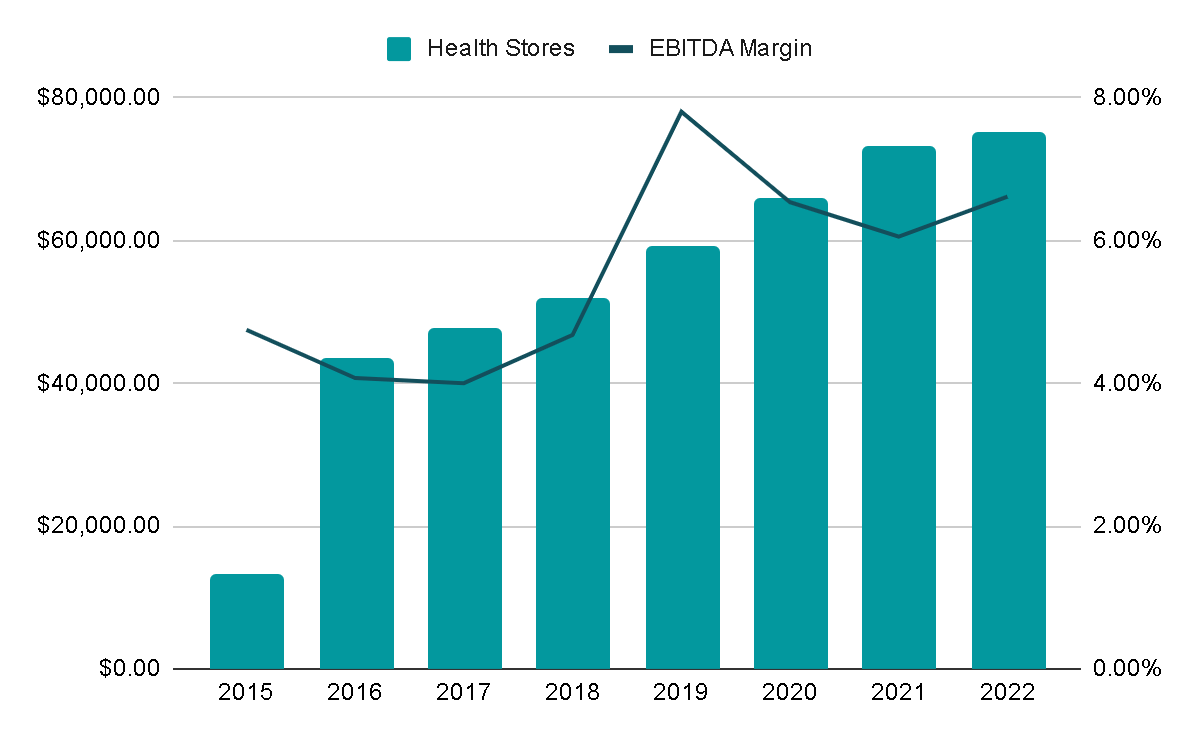

Revenues from this segment have been growing at a rate of 9% since 2016, and EBITDA margins have expanded from 4% to the current 6.6%. For comparison, similar businesses such as CVS and WBA have historically maintained EBITDA margins between 6% and 7%, while FRAGUA, a competitor in Mexico, currently boasts margins of 7.9%.

In general, we can conclude that growth is positive, the business model yields stable revenue, and the profitability margins are in line with those of its competitors.

Health Stores Revenue and Margin (Author's Representation)

{kind=link}

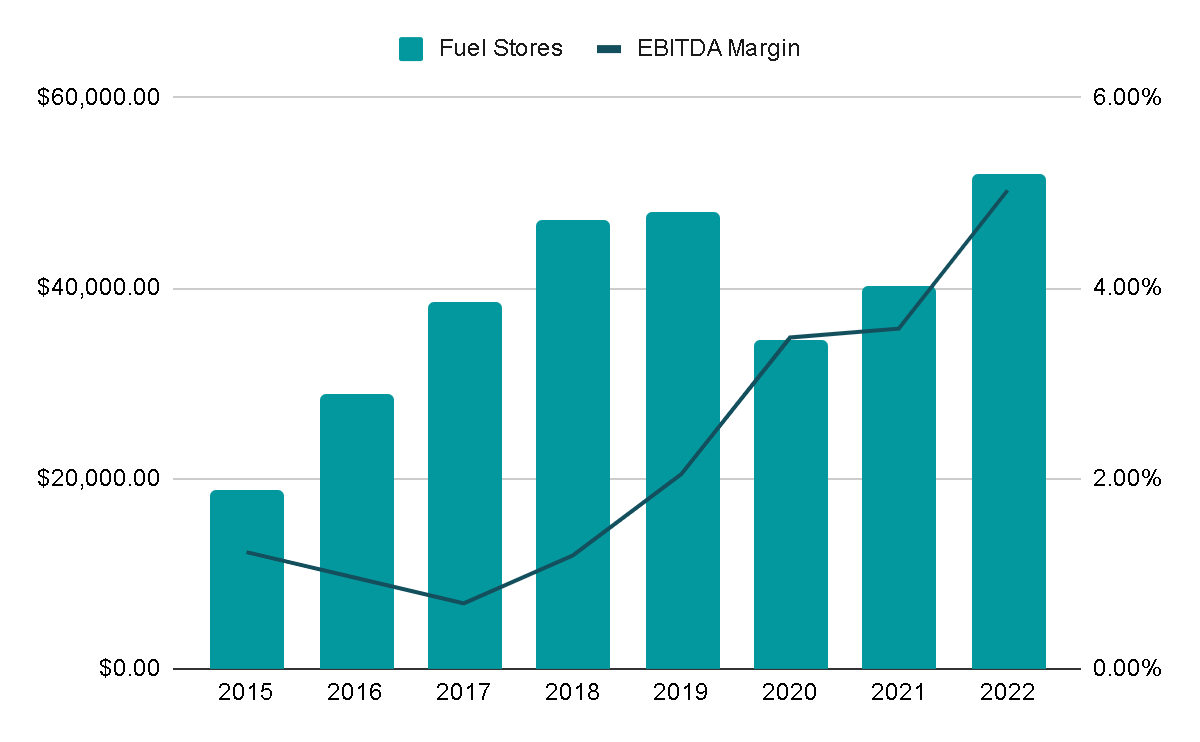

Fuel Stores

This division operates retail gas stations for fuels, motor oils, and other car care products, following a business model similar to that of Alimentation Couche-Tard, where the key focus is not the sale of fuel but rather the purchases made within the convenience stores located at the gas stations.

While it's clear that this provides an additional source of income, it appears to be a challenging market to compete in. This is not only due to competition from companies like Petro Seven (associated with 7-Eleven), G500, or BP but also because the gas stations with the largest presence in the country are operated by Petroleos Mexicanos, the state-owned company overseen by the Mexican government.

Although the government allows competitors to enter the country, fuel prices typically move at rates established by the government . Therefore, even in environments with high inflation in fuel prices, these businesses must maintain competitive prices compared to those set by the government, which is more interested in maintaining affordable prices for consumers than in generating profits from its gas stations.

OXXO Gas Stations (FEMSA)

This segment represented 7.5% of total revenues during FY2022 and has been growing at a rate of 15% annually since 2015. EBITDA margins are relatively low, ranging between 3% and 4%, but they are consistent with those of gas station businesses like Parkland Corporation or Murphy USA.

Fuel Stores Revenue and Margin (Author's Representation)

{kind=link}

Focusing on Core Business

All of these business lines exemplify the company's visionary approach to cultivating diverse revenue streams as it continues to expand. This not only propels its growth but also encourages vertical integration . For example, in the past, OXXO stores were located within PEMEX gas stations. Now, FEMSA is capitalizing on the strong reputation of its brand to own both gas stations and convenience stores, ensuring it captures 100% of the revenues generated at those gas stations.

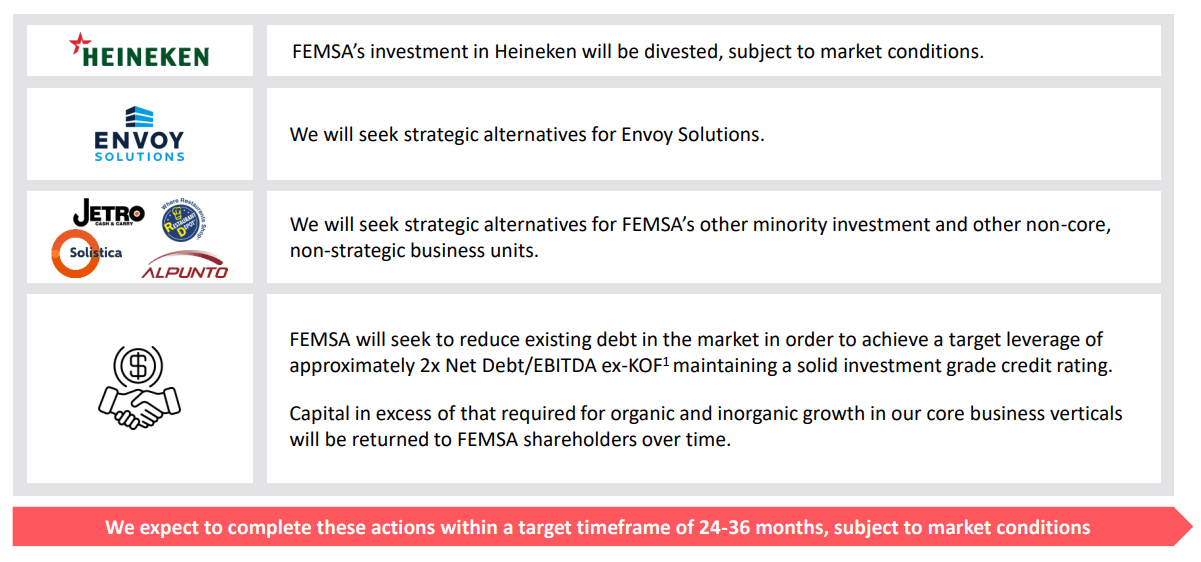

Nevertheless, this strategy also brings risks associated with " diworsification ", a term popularized by Peter Lynch to describe diversification that is not beneficial, as it might lead to a loss of focus on the core business. It appears that the company has recognized this concern , and during the current year, they announced plans to restructure the company. This entails divesting their 14.7% stake in Heineken shares, selling 63% of their Logistics and Distribution segment, and exploring potential sales for the business lines categorized as 'Other,' which contributed to 3% of total revenue in FY2022.

{kind=link}

This appears to be a highly positive move as it would enable them to unlock the value of the Logistics business, which, while promising, seems somewhat unrelated to the rest of their business lines. More importantly, it will allow them to allocate resources to their core segments related to traditional retail sales.

For instance, the introduction of Spin, a digital wallet and debit card that offers consumers cashback every time they make a purchase at OXXO. This cashback can only be used at OXXO, enhancing customer loyalty and improving the overall retail business ecosystem. Initiatives like these are the ones truly worth investing resources in and have a positive impact on the core business.

{kind=link}

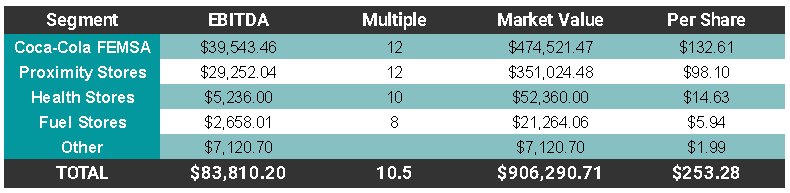

Valuation

For the valuation, I will perform a sum-of-the-parts analysis, estimating the growth and profitability of each segment in FY2023. We already have good indications of what these metrics will be, as the company has already reported results for three quarters of the fiscal year.

The growth rates and margins I will apply to each segment, based on year-to-date data, are as follows:

- Coca-Cola FEMSA: Revenue growth of 9% and EBITDA Margins of 16%.

- Proximity Stores: Revenue growth of 10% and EBITDA Margins of 10%, assuming margins in a normalized environment.

- Health Stores: Revenue growth of 0% and EBITDA Margins of 7%.

- Fuel Stores: Revenue growth of 14% and EBITDA Margins of 4.5%.

- Other: In the case of "Other" I will assume that the Revenue and EBITDA remain exactly the same as last year and later I will add the remaining 37% of Revenue and EBITDA of Envoy Solutions during FY2022, remembering that FEMSA sold 63% of the company and now does not report income from this segment.

Below, I will outline the EBITDA multiples I assigned to each segment. These multiples have been selected based on the quality and competitive position of each business segment, with reference to comparable businesses and their respective multiples. I will not assign a multiple to the EBITDA of the 'Other' segment because it appears that the company is seeking to divest the businesses within it. So we could say that this segment comes "for free" when we buy FEMSA.

{kind=link}

The total of the segments results in a Market Cap of $900 billion Mexican pesos or $253 pesos per share, which is 45% higher than the current Market Cap of $630 billion Mexican pesos.

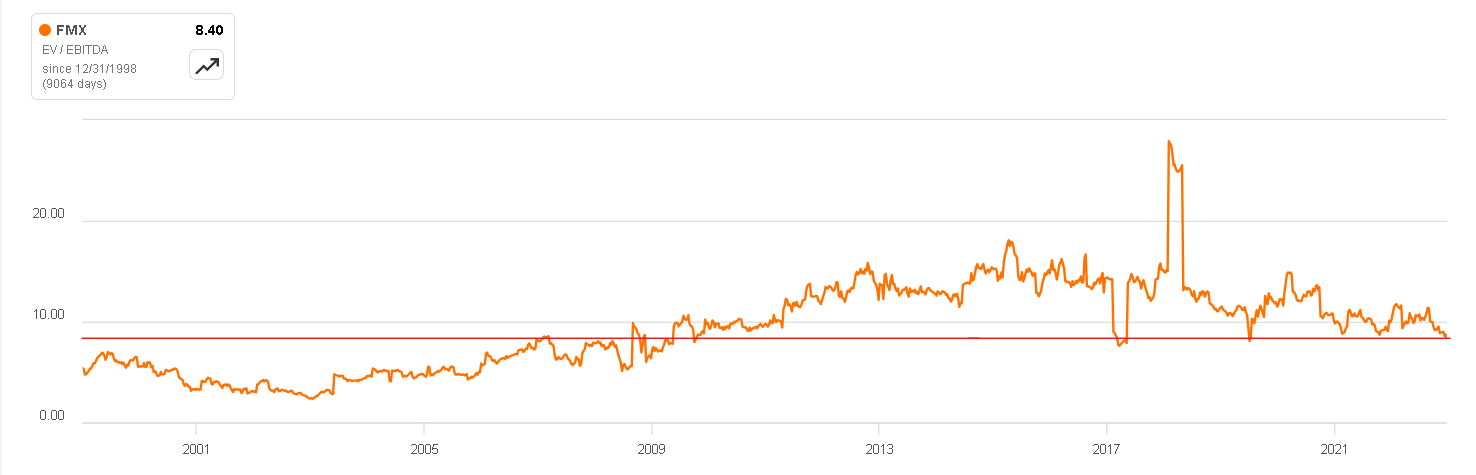

It's important to note that holding companies typically trade at a discount compared to the sum of their parts. However, it appears that the current discount is quite substantial . Additionally, if we consider that the company is trading at 8x LTM EV/EBITDA, the undervaluation becomes even more apparent. A company like FEMSA could potentially trade at 10 or 12x without any issues.

{kind=link}

Final Thoughts

The company is undergoing an exceptionally interesting strategic shift. It seemed that it was venturing beyond its circle of competence and facing the risk of 'diworsification'. However, by refocusing on its core business, which is also quite robust, they can optimize their investments and establish a clear direction.

In addition to the previously mentioned risk concerning Coca-Cola FEMSA, it's worth noting that operating in Latin America presents significant challenges. This is due to the fluctuation of its currencies and the prevalence of corrupt politics. While these factors pose risks, they could also serve as entry barriers for American or European competitors attempting to penetrate these markets.

Taking into account the risks, the quality of the business, and the valuation, I have decided to assign it a ' buy ' rating.

For further details see:

Fomento Economico Mexicano: Refocusing On Its Core Business Seems Promising