NKE - Foot Locker: 4 Reasons To Consider Selling The Recent Bounce

2023-11-19 22:26:29 ET

Summary

- Foot Locker shares have rallied sharply and are now only slightly below levels seen prior to the company's disappointing Q2 earnings release.

- FL operates in a highly competitive industry and competes directly with its largest supplier which is Nike.

- The Company has a history of underperforming the S&P 500 over both recent periods and longer periods of time.

- Despite recent challenges, FL is trading at a premium to peers and its own historical average valuation.

- I am initiating FL with a sell rating and would consider upgrading the stock if operating performance improves or the valuation picture improves.

Shares of Foot Locker, Inc. ( FL ) have rallied by nearly 32% from a 52-week low of $14.84 per share which was reached on August 23, 2023.

On August 23, 2023, FL shares plunged 28% after the company delivered weak Q2 results, paused its dividend, and lowered guidance for the rest of 2023.

At current levels, FL shares are now just 5.2% lower than where they traded prior to the Q2 earnings release.

In my view, this recent rally represents nothing more than a dead cat bounce and has provided investors with an excellent selling opportunity.

1. Highly Competitive Business Resulting in a Thin Moat

FL is a leading footwear and apparel retailer with global operations. The footwear and apparel business is highly competitive. FL competes with sporting goods retailers such as DICK'S Sporting Goods ( DKS ), Big 5 Sporting Goods ( BGFV ), and other smaller players. FL also competes with larger retailers such as Walmart ( WMT ), Macy's ( M ), Target ( TGT ), and many others. In the online space, FL competes with Amazon ( AMZN ) and other smaller online players.

In addition to all those companies, FL also competes directly against its suppliers such as Nike ( NKE ) and Adidas which have substantial direct to consumer channel businesses. In 2022, ~65% of all merchandise purchased by FL was from Nike. Thus, Nike has very strong negotiating leverage with FL when it comes to pricing.

As a result of these dynamics FL has been able to generate only low to mid single digit profit margins historically. Historically, the company's average profit margin has been ~3%. In addition to a low average level of profitability, FL has experienced significant earnings volatility as the business is significantly driven by consumer spending and overall economic conditions.

Low and inconsistent profitability has led to weak historical performance for FL shares. As shown by the charts below, FL has underperformed the S&P 500 over the long term and more recent time periods.

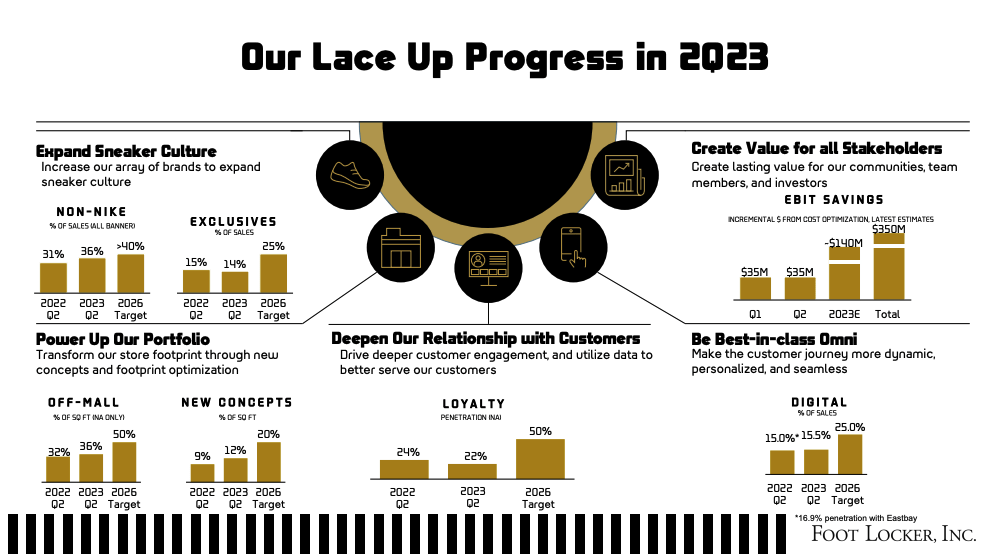

2. Lace Up Plan Has Failed To Deliver

In March 2023, FL announced its "Lace Up" plan to revitalize the company. The plan calls for the company to grow from ~$8.5 billion in annual revenue to more than $10 billion over the long-term. Additionally, the plan calls for EBIT margins to improve to >10% from historical levels <7%.

Key pillars of the plan include diversifying sales away from Nike, an increased focus on brands exclusive to FL, optimization of store footprint, an increased focus on building customer loyalty, and a focus on omni channel and growing the digital % of sales.

As shown below, FL has made progress on some of its key goals including reducing its reliance on Nike and increasing off-mall as a % of total store footprint. However, these changes have thus far failed to deliver the intended results.

FL's reduced reliance on Nike products was a forced decision in some ways as Nike announced changes in late 2022 to reduce FL's product allocations in a bid to focus more on its own direct to consumer business.

While reducing reliance on Nike over the longer term may be a positive, there are potential short-term consequences as Nike remains a very popular brand with consumers.

In addition to a lack of top-line and bottom line benefits from diversifying away from Nike, FL also has yet to experience any gains related to its shift away from mall-based locations.

Thus far, FL has failed to deliver on its goals to increase the % of exclusives as a percentage of total sales, drive deeper customer engagement, and material increase digital sales.

For these reasons, I am skeptical regarding FL's ability to deliver on its proposed plan going forward given the lack of progress in key areas.

{kind=link}

3. Recent Wall Street Downgrades

On October 19, Goldman Sachs lowered its rating on FL to Sell from Neutral. In its note, Goldman noted that its bearish stance on FL is partially based on the view that FL's market share position will be difficult to stabilize following Nike allocation changes. Goldman assigned a price target of $18 to FL.

On September 25, Jefferies lowered its rating on FL to Hold from Buy. In its note, Jefferies noted concerns related to slowing consumer spending and the potential impact related to the resumption of student loan repayments. Jefferies noted that a recent survey given to U.S. consumers with outstanding student loan debt for themselves or their children found that ~54% and ~46% of respondents plan to spend less on apparel/accessories and footwear due to the restart of loan repayments. Additionally, Jefferies slashed its 2024 EPS outlook to $1.20 from $1.40 and reduced its price target on the stock to $18 from $28.

The average Wall Street price target is currently $19.47 which implies ~11.5% of downside from current levels.

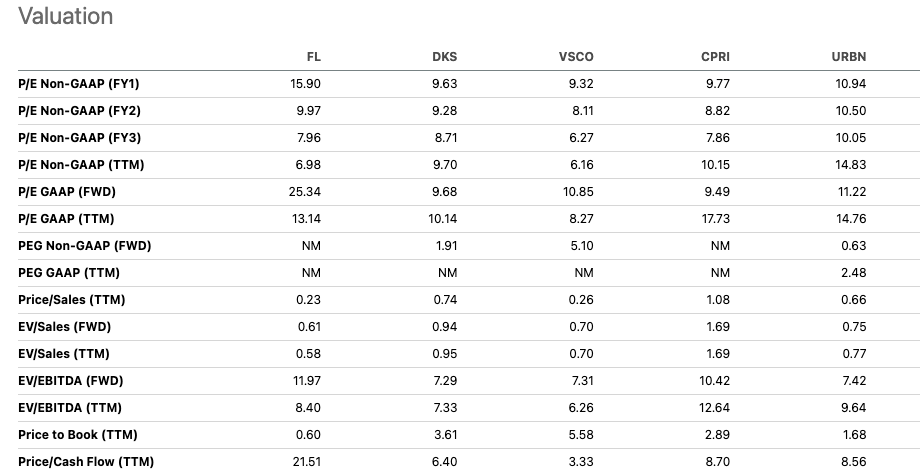

4. Valuation Is Not Highly Attractive

Given the very thin moat around FL's business due to high levels of competition and dependence on its single largest supplier, I do not believe the company should trade at a premium to other similar retail companies.

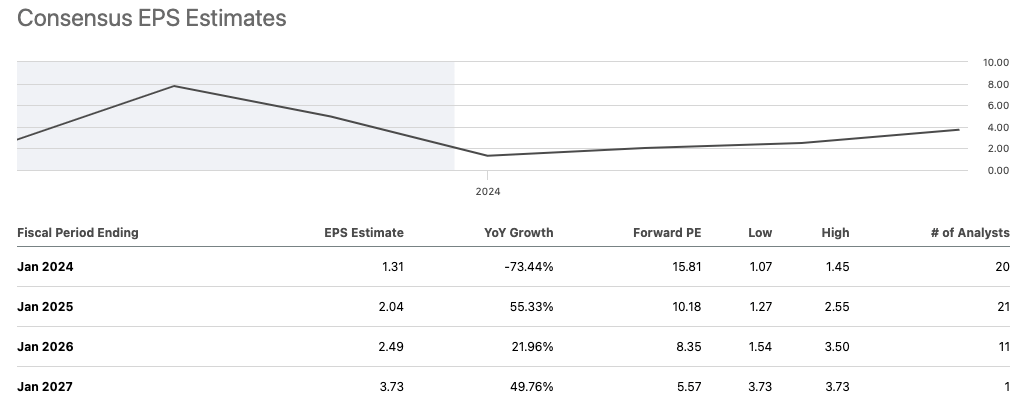

At first glance, FL appears to be trading in line with other retailers such as Dick's Sporting Goods, Victoria's Secret, Urban Outfitters, and Capri Holdings. However, 2024 consensus earnings estimates for FL are in my view overly optimistic and not fully reflective of recent weakness.

As shown below, consensus EPS estimates for FY 2024 for FL are currently $2.04 which represents a 55% increase compared to FY 2023 estimated EPS of $1.31.

My view is that the $1.40 2024 EPS target recently put out by Jefferies is a more reasonable estimate of 2024 earnings potential given recent business struggles.

Based on this level of earnings, FL is currently trading at a forward P/E ratio of ~15.7x which is well above peer companies and not far from the S&P 500's forward P/E ratio of ~18x.

Based on a forward P/E ratio of ~15.7, FL is trading at a premium relative to its historical valuation range. As such, I believe FL is overvalued relative to its historical norm.

Seeking Alpha Seeking Alpha

{kind=link}

{kind=link}

Q3 2023 Earnings Preview

FL is expected to report Q3 2023 earnings on November 29, 2023. Consensus analyst estimates call for FL to report EPS of $0.23 per share which represents a ~82% decline on a year-over-year basis. The company is expected to report revenue of $1.96 billion which represents a ~10% decrease on a year-over-year basis. During its Q2 2023 earnings release, FL cut its Q3 2023 earnings outlook due to a challenging operating environment. Given the recent rally over the past few months, I believe the downside in the event of an earnings miss is greater than the potential upside in the event of an earnings beat.

Potential Upside Catalysts

Despite all the headwinds I have noted, it should be noted that there are some possible upside catalysts that could drive FL shares higher that investors should be aware of.

The relatively high short interest (~13.3% of shares out currently sold short) has created a situation in which a short covering rally is possible in the event of any positive news. Positive news could include operational improvements going forward which lead to higher margins and thus higher earnings.

The company has an ambitious target of $350 million in EBIT savings over the long term related to its Lace Up plan which may be able to drive margin improvement and thus earnings growth. It should be noted that FL reported diluted EPS of $3.59 for FY 2022 and $8.61 for FY 2021. However, the changes in the Nike relationship and slowing consumer spending will make it difficult for FL to get back to that level of earnings in my view.

Another potential upside catalyst would be a potential approach takeover approach from another company. Nike could be a potential buyer given the fact that the companies already have a close relationship with Nike accounting for a very significant portion of FL sales. Nike has been focused on growing its direct to consumer business and acquiring FL would be an easy way to accelerate that strategy. However, there has not been any chatter in the market regarding this so I would say an acquisition is unlikely at this time.

Conclusion

FL shares have rallied recently and are now 32% higher than where they were just a few months ago. FL shares have recovered nearly all the losses that occurred following a very disappointing Q2 earnings release.

FL operates in a highly competitive industry and faces structural challenges due to its reliance on Nike which is the company's largest supplier. Nike has been focused on growing its direct to consumer offering which has resulted in lower product allocations to FL.

FL has thus far failed to realize significant gains from its Lace Up plan which calls into question the ability of the company to deliver on its plan going forward.

Despite recent challenges, FL is not trading at a cheap valuation relative to the S&P 500 and its peers based on my expectations for 2024 earnings.

For these reasons, I am initiating FL with a sell rating and would consider upgrading the stock if it is able to deliver on its Lace Up program. Moreover, I would also consider upgrading the stock if the valuation picture were to significantly improve from here.

For further details see:

Foot Locker: 4 Reasons To Consider Selling The Recent Bounce