BOOT - Foot Locker: Inventories Are Preventing This From Being An Attractive Fit

2023-05-21 06:40:25 ET

Summary

- Foot Locker shares plunged 27.3% after management announced financial results for Q1 of the 2023 fiscal year, missing analysts' expectations on both top and bottom lines.

- The company revised lower its guidance for the 2023 fiscal year, with sales expected to be down between 6.5% and 8%, and comparable store sales potentially down as much as 9%.

- Foot Locker is currently rated as a 'hold' due to concerns over bloated inventory levels and weak demand, which may persist for the next few quarters.

May 19th ended up being a very dark day for shareholders of footwear and apparel retailer Foot Locker ( FL ). After management announced financial results covering the first quarter of the 2023 fiscal year, shares of the business plunged, closing down 27.3%. It was already bad enough that management missed analysts' expectations on both its top and bottom lines. But then when you factor in that the company revised lower its guidance for the 2023 fiscal year as a whole, the picture looked downright awful. In the event that financial performance for the company eventually reverts back to what it was in prior years, shares could offer a tremendous amount of upside for investors. But as they are priced now on a forward basis, the stock looks more or less fairly valued compared to similar firms.

Typically, in a situation like this, I would find myself drawn to the opportunity to buy some of your units on the cheap. After all, the value investor in me likes buying discounted stocks. But given the significant inventory excess that the firm is contending with, I do believe that some additional pain could be around in the near term. Those who have a very long term investment horizon might want to look at this as a viable prospect. But given the uncertainty in the space, and the aforementioned inventory issue, I am taking a more neutral stance on the company and rating it a ‘hold’.

A painful quarter

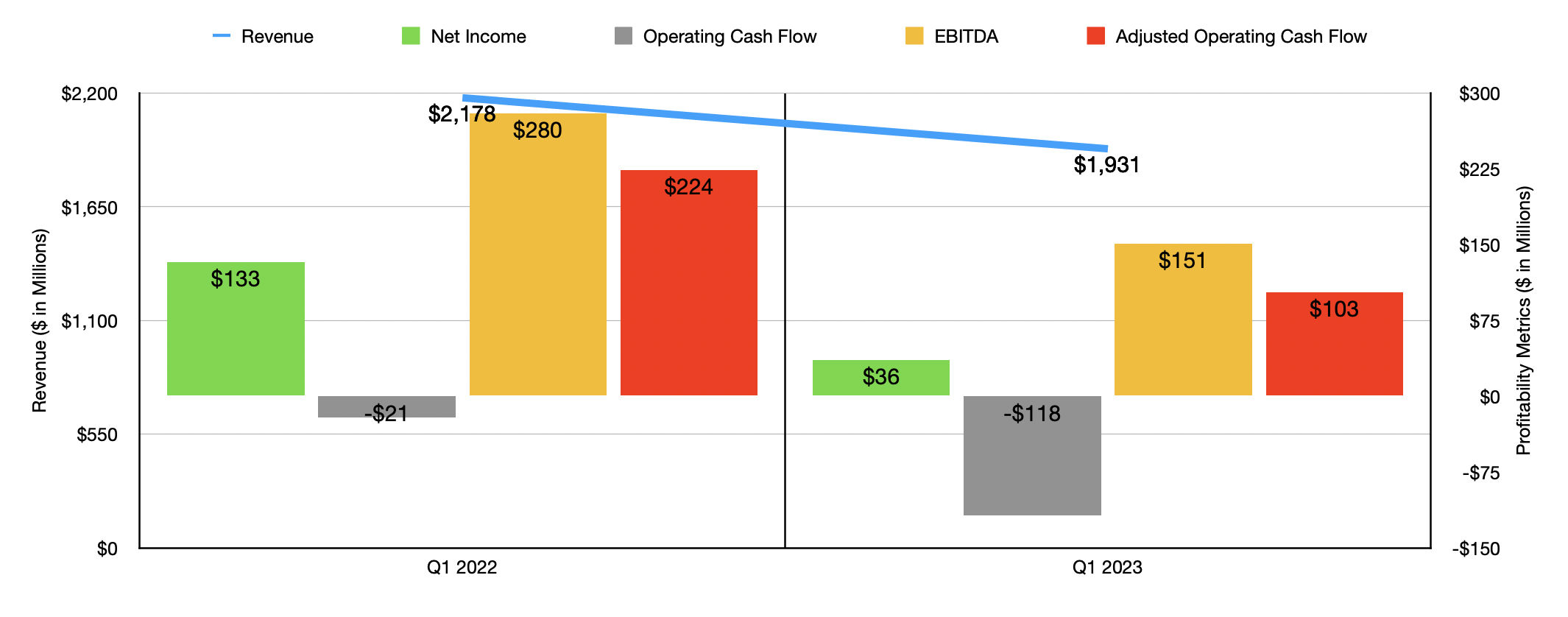

Before the market opened on May 19th, the management team at Foot Locker announced financial results covering the first quarter of the company's 2023 fiscal year. By pretty much every measure imaginable, the picture for shareholders was awfully painful. Consider revenue. During the quarter, sales came in at $1.93 billion. That's 11.3% lower than the $2.18 billion the company reported the same quarter one year earlier. The largest driver behind this drop was a 9.1% plunge in comparable store sales, driven by weak economic conditions causing a reduction in demand. Management believes that some of the pain was attributable to lower income tax refunds in the us that resulted in less spending on shoes and apparel. Other factors were also at play, such as the changing vendor mix that the company has seen and its repositioning of Champs Sports. It is worth noting that not only did sales weaken year-over-year, they also came in $64.8 million lower than what analysts had forecasted .

{kind=link}

Author - SEC EDGAR Data

The weakness that Foot Locker experienced impacted its bottom line as well. During the quarter, the company generated profits per share of only $0.38. That's down significantly from the $1.37 per share that the business reported one year earlier. That translates to a decline in net income from $133 million to $36 million. The earnings reported by management were also $0.36 per share lower than what analysts thought they would be. On an adjusted basis, the profits per share for the company totaled $0.70. This represented a significant haircut from the $1.60 per share reported the same time last year. And even it missed analysts’ expectations, with the miss amounting to $0.08 per share.

As you can imagine, the decline in profitability brought with it a decline in cash flows. Operating cash flow, for instance, went from negative $21 million to negative $118 million. If we adjust for changes in working capital, we would see that this metric had fallen from $224 million to $103 million. And finally, EBITDA for the company plummeted from $280 million to $151 million. If these declines seem disproportional relative to the drop in sales, keep in mind that this kind of drop is typical in the retail space. In order to operate, retailers almost always have a significant amount of capital invested in fixed assets. As sales drop, especially if that drop is related to a decline in comparable store sales, you see less revenue spread across these significant assets. That results in meaningful margin contraction. You can see this materialize in the company's margins. For instance, its gross profit margin declined by 4%, while selling, general, and administrative costs, grew by 1.1%. These changes may not seem significant. But when applied to the amount of revenue the company generated in the first quarter of 2023, it translates to an extra $98.5 million in pre-tax profits being wiped out for shareholders.

{kind=link}

Author - SEC EDGAR Data

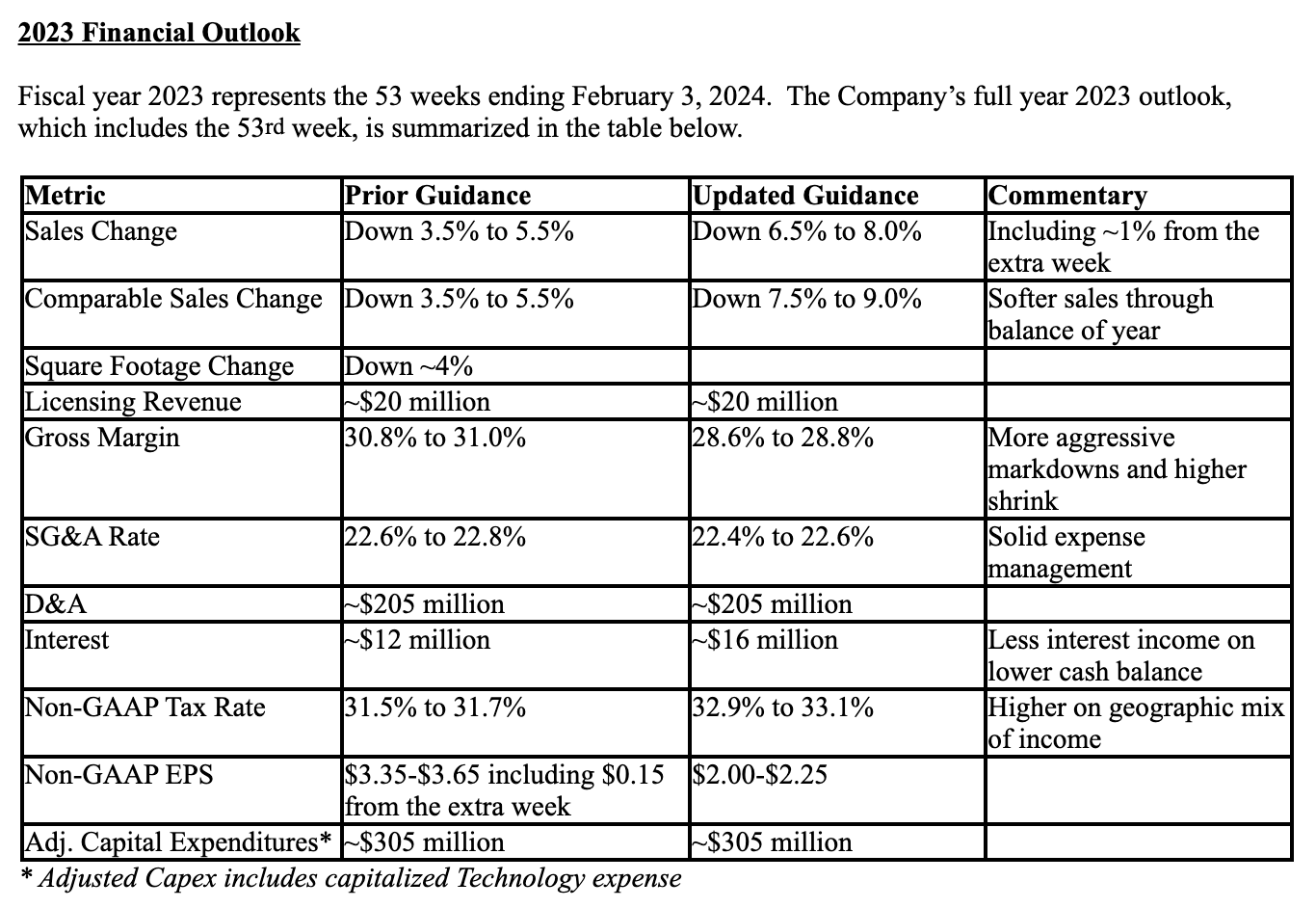

If this were just a one time blip on the radar, the market might have been more forgiving. But management also came out with some rather painful news. They now expect 2023 as a whole to be much worse than they previously thought it would be. Sales, for instance, should be down by between 6.5% and 8%. Prior expected guidance called for a decline of between 3.5% and 5.5%. Comparable store sales could be down as much as 9%. Management is also forecasting a decrease in the company's overall gross profit margin, and a modest worsening in the company's tax rate. As a result of these factors, the company is now forecasting earnings per share of between $2 and $2.25. This is a significant drop compared to the prior expected guidance of between $3.35 and $3.65.

{kind=link}

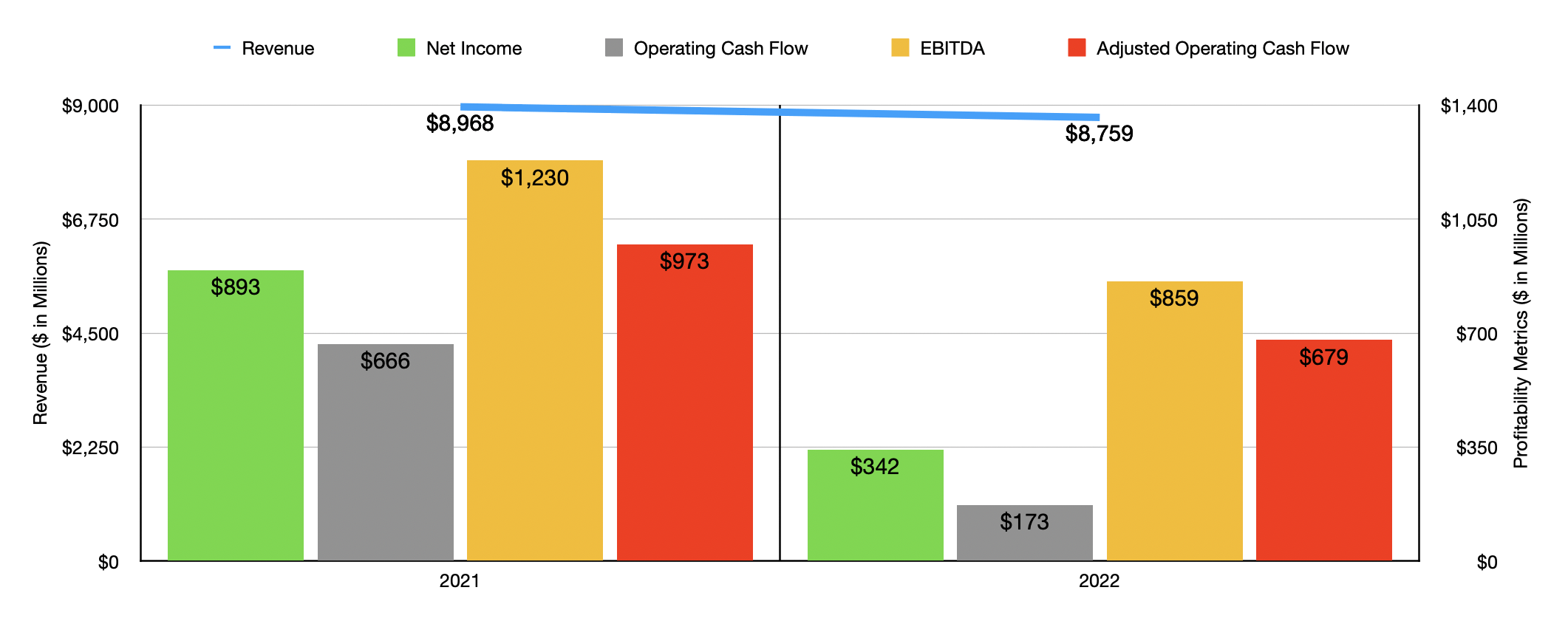

At the midpoint, we are looking at overall earnings for the company of $202.1 million. That would be down almost half compared to the $342 million reported for 2022. Based on the estimates provided by management, I figured that operating cash flow for the year should be around $407.1 million, while EBITDA should total somewhere around $522.6 million.

{kind=link}

Author - SEC EDGAR Data

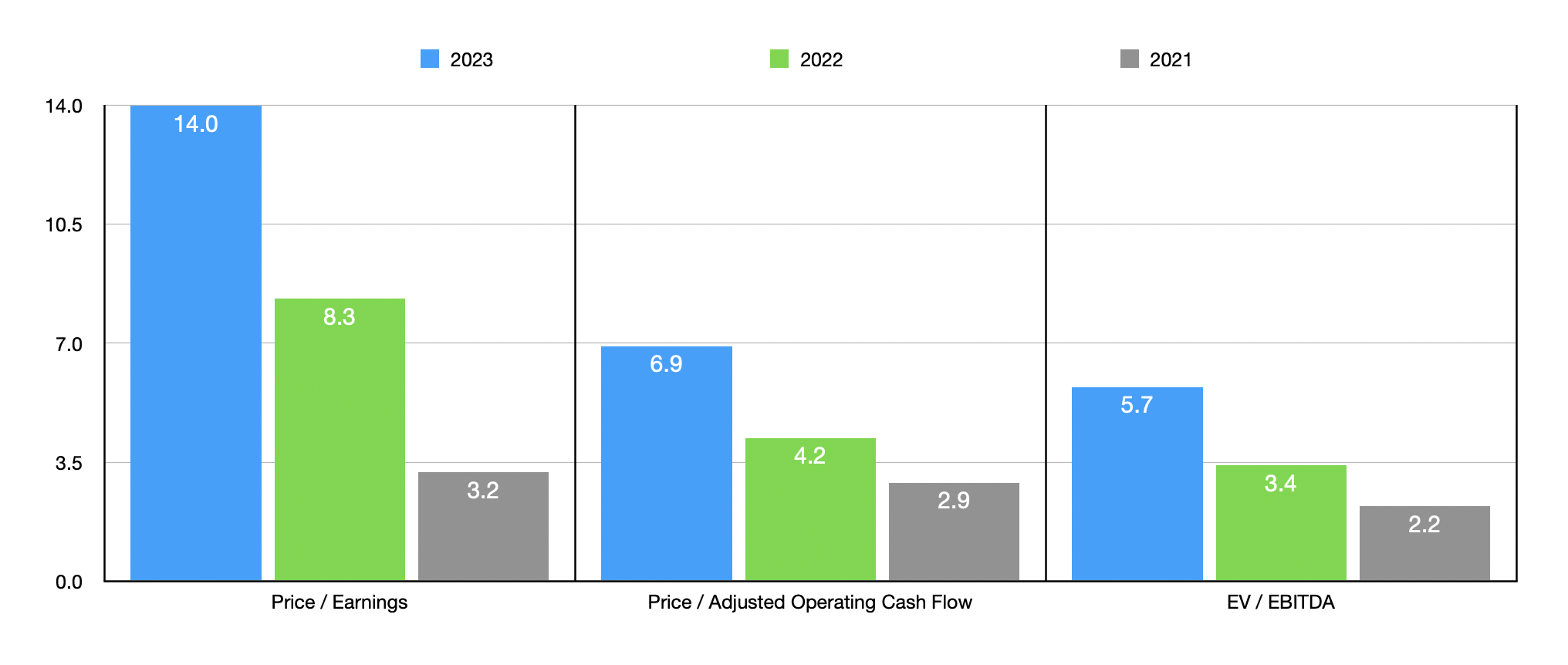

Based on these estimates, I was able to easily value the company. As you can see in the chart above, the company is trading at a forward price to earnings multiple of 14. While this might be lofty for a slow growing retailer, the price to operating cash flow multiple is considerably lower at 6.9. Meanwhile, the EV to EBITDA multiple should be about 5.7. As you can see in the aforementioned chart, this pricing is more expensive than if we were to rely on data from 2021 or 2022. Market conditions do change and the past couple years have been truly odd. But the same could be said of existing conditions now. I also, as part of my analysis, like to compare the companies I analyze to similar firms. In the table below, you can see how Foot Locker is priced compared to five similar enterprises. On both a price to earnings basis and EV to EBITDA basis, I found that three of the five companies were cheaper than Foot Locker. Meanwhile, when it comes to the price to operating cash flow approach, two of the five ended up being cheaper.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Foot Locker |

| 14.0 |

| 6.9 |

| 5.7 |

| Boot Barn Holdings ( BOOT ) |

| 11.7 |

| 108.2 |

| 7.6 |

| Buckle ( BKE ) |

| 6.3 |

| 6.6 |

| 4.1 |

| Guess' ( GES ) |

| 8.1 |

| 7.5 |

| 4.4 |

| Abercrombie & Fitch ( ANF ) |

| 380.7 |

| 5.5 |

| 4.3 |

| Skechers U.S.A. ( SKX ) |

| 19.8 |

| 13.4 |

| 10.9 |

The value investor in me would love to swoop in and pick up some shares. With 2,692 stores spread across 29 different countries, and another 163 locations franchised and operating in the Middle East and Asia, the company has at large physical footprint that it can rely on as industry conditions improve. However, I am worried about the inventory levels that are on the company's books. At the end of the most recent quarter, Foot Locker had $1.76 billion worth of inventories on its books. This was up materially from the $1.40 billion reported one year earlier. In addition to this, the company also saw inventories rise quarter over quarter, jumping 7% from $1.64 billion at the end of 2022 to the inventory levels that the company has today. Surging inventories during times like what we have today and at a time when revenue is dropping, suggests that the company may need to take a more sizable haircut on inventories in order to get them off its books. This could, in turn, translate to even more pain on the bottom line in the quarters to come.

Takeaway

Operationally speaking, things are not going particularly well for Foot Locker. The company seems to be suffering on both its top and bottom lines. Inventory levels are bloated and weak demand will probably persist for at least the next couple of quarters. The downward revision in guidance is particularly painful. Given all of these factors, and even in spite of the fact that shares look cheap in a scenario where financial performance recovers to what it was in 2021 or 2022, I do think a more cautious approach to the company is warranted. And as such, I have decided that a ‘hold’ rating makes sense for now.

For further details see:

Foot Locker: Inventories Are Preventing This From Being An Attractive Fit