CNY - Forex: Real Rate Convergence Still On The Cards

2023-09-01 04:49:00 ET

Summary

- Stubborn resilience in US activity data and risk-off waves from China have translated into a strengthening of the dollar over the summer.

- We still think this won’t last much longer and see Fed cuts from early 2024 paving the way for EUR:USD real rate convergence. Admittedly, downside risks to our EUR/USD bullish view have grown.

- A broad-based dollar decline should translate into a recovery in the currencies hit most during the period of Fed tightening.

By Francesco Pesole , FX Strategist; Chris Turner , Global Head of Markets and Regional Head of Research for UK & CEE

Still awaiting the turn in US activity data

The underlying factors driving FX markets became "crystallised" over the summer, as investors waited in vain for a negative turn in US economic activity that would justify a dovish shift in both the Federal Reserve's rhetoric and market pricing. However, since forward-looking indicators and evidence from the job market have not shown enough reason to cast doubt on the resilience of the US economy, US yields have faced limited resistance once again. This has made it increasingly discouraging, particularly in real terms, to play the long bearish game through dollar shorts.

At present, the US dollar index finds itself at a critical juncture, trading close to 104 (a multi-month high), and is about to face a month where decisions made by the central banks of both the US and the eurozone will determine whether it can break through to the March peaks (105.60) and beyond. Our economists expect no further interest rate hikes by the Federal Reserve, and while it is a close call, we anticipate the European Central Bank to deliver one final 25bp raise in September. In other words, we have reason to believe that the dollar may have reached its peak around current levels.

Another reason for the dollar's resilience has been the influx of negative news from China. The dollar typically benefits from a deterioration in Chinese sentiment through two channels: directly through yuan depreciation (to which USD is highly correlated) and indirectly through the risk environment channel. It is conceivable that there could be a further deterioration in investor sentiment regarding China in the coming months. However, the People's Bank of China's determined defence of the renminbi means that the dollar may only gain indirectly from these developments.

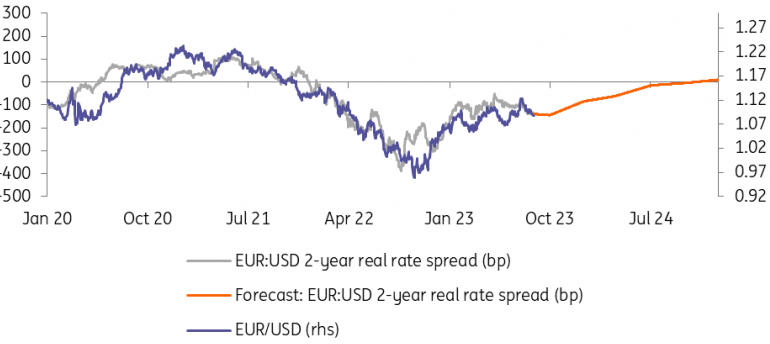

Looking beyond the near term, monetary policy divergence is expected to remain the overwhelmingly predominant factor driving currency trends into the next year. Another way to consider this is through short-term real rates. For example, EUR/USD has closely followed its short-term real rate spread since 2020. If nominal rate fluctuations have been the primary force behind these real rate changes thus far, the end of tightening cycles may result in a period where the inflation rates, on the right side of the subtraction, gain more significance.

Our EUR:USD real rate forecast

{kind=link}

ING, Refinitiv

EUR/USD upside potential remains sizable

Our economics team remains of the view that markets are underestimating the downside risks facing the US economy and that the Fed will need to implement significant rate cuts from the first quarter of 2024. Despite a deteriorating outlook for the eurozone economy, we only expect the ECB to begin to ease policy in the summer of 2024. Based on that, we anticipate the EUR/USD two-year real rate gap narrowing to zero by the end of 2024, allowing the pair to comfortably trade above 1.15.

A broad-based dollar decline should translate into a recovery in the currencies hit most during the period of Fed tightening. We expect Scandinavian currencies to rebound from next quarter, although the Swedish krona’s grim domestic outlook means the road should be bumpier compared to its Norwegian peer.

The Australian and New Zealand dollar need to wait for some recovery in Chinese sentiment before unlocking “recovery mode”, while the pound remains tied to market expectations for Bank of England tightening that we still deem too hawkish. USD/JPY should remain the barometer of market sentiment on US yields: a turn lower is long due on the overbought pair, but may need to wait later this year given the Bank of Japan’s lingering easing bias.

As for emerging market currencies, monetary stimulus will keep the renminbi soft and will also see Asian currencies lag in any rebound against the dollar later this year. Better positioned remain some currencies in the CEE space and Latam (eg Hungary, Brazil) where real rates remain deeply positive despite the start of easing cycles this year.

Content Disclaimer:

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more .

For further details see:

Forex: Real Rate Convergence Still On The Cards