FORG - ForgeRock: Undervalued And Likely To Benefit From AI And Thoma Bravo Acquisition

2023-05-22 03:47:10 ET

Summary

- ForgeRock is a global leader in digital identity.

- The company may soon be acquired by Thoma Bravo.

- There are other investors that are interested in ForgeRock, Inc. In my view, if the DOJ blocks the transaction, other acquirers may show up.

- I do not know whether the valuation made in 2022 included the fact that artificial intelligence may bring economies of scale.

Editor's note: Seeking Alpha is proud to welcome Kesef Management as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis

ForgeRock, Inc. ( FORG ) is waiting for the approval of the DOJ to close the acquisition by Thoma Bravo for $23.25 per share in cash. Right now, even if the merger does not close, I believe that buying shares is interesting. The new developments using artificial intelligence could make the digital identity management solutions much more efficient, which may imply a valuation for FORG of more than $23.25 per share. It is also worth noting that according to the background of the merger, other sponsors were interested in ForgeRock, so we may see new bids if the transaction does not close. In sum, I see more upside potential than downside risks.

Target: ForgeRock

ForgeRock is a global leader in digital identity, delivering modern identity and access management solutions for clients, employees, and employers. In my view, we are talking about a growing giant because management, in the last quarterly report, noted that more than 1,300 clients manage identities. The company reports a market capitalization of less than $2 billion.

Buyer Is A Large Private Equity Firm

The buyer, Thoma Bravo, is a large global investment manager with a software portfolio that includes around 70 companies, which generate about $24 billion of annual revenue. With this in mind, I believe that the buyer is large enough and sophisticated with sufficient expertise in the M&A markets to acquire ForgeRock. For those readers who may not know about the buyer, the company has a lot of expertise in the acquisition of infrastructure and cybersecurity companies. I believe that Thoma Bravo will most likely use know-how from previous private equity deals to enhance the business model of ForgeRock.

M&A Analysis: There Is Only One Condition Remaining For The Transaction To Close

I revised the merger agreement , which did not include very difficult precedent conditions. The requisite stockholder approval is not a problem anymore because shareholders approved the acquisition. The conditions also included the approval from the FTC's Bureau of Competition and the expiration of the waiting period pursuant to the Hart-Scott-Rodino Act.

Antitrust Laws. The waiting period (and any extensions thereof) applicable to the Merger pursuant to the HSR Act, will have expired or otherwise been terminated, and no agreement with any Governmental Authority not to consummate the Merger shall be in effect. Source: Merger Agreement

The U.S. Department of Justice issued a second request that pushed the share price down. However, I would not expect a lot of trouble from the DOJ. It is also worth noting that ForgeRock and the DOJ signed an agreement noting that they would not certify compliance with the Second Request no earlier than May 1, 2023. With this in mind, I believe that the company could certify compliance soon.

As previously reported, the U.S. Department of Justice (the "DOJ") has issued a Second Request in connection with its review of the proposed acquisition of ForgeRock by Thoma Bravo pursuant to the Hart-Scott-Rodino Antitrust Improvements Act of 1976 (the "HSR Act"). In February 2023, ForgeRock and entities affiliated with Thoma Bravo entered into an agreement (the "Timing Agreement") with the DOJ in connection with the proposed acquisition and the Second Request. Under the Timing Agreement, ForgeRock and Thoma Bravo agreed that they will certify compliance with the Second Request no earlier than May 1, 2023, and will not consummate the proposed acquisition less than 75 days after compliance with the Second Request. Source: 8-K

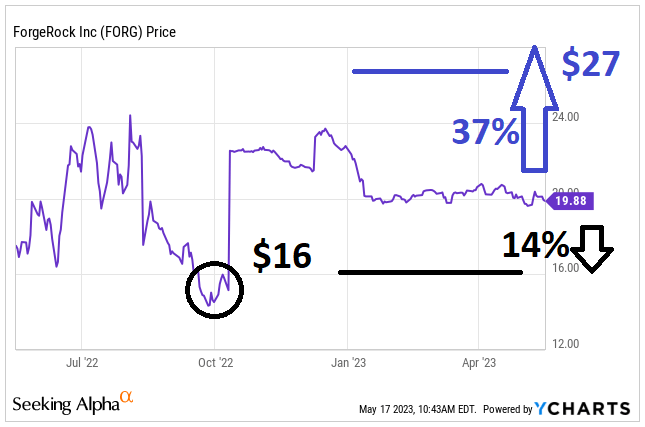

With that being said about the investigation of the DOJ, I would also note that the expiration or termination of the waiting period is the last condition. Hence, as soon as the companies deliver the termination, the stock price could push back up to more than $22-$23 per share.

The expiration or termination of the waiting period applicable to the proposed acquisition pursuant to the HSR Act is the only remaining approval or regulatory condition required to consummate the closing of the proposed acquisition. Source: 8-K

There Are Many Competitors, I Do Not Expect The DOJ To Stop The Transaction

Thoma Bravo acquired several competitors in the IAM market, however I believe that there is a sufficient number of actors in the market. Legacy providers, companies offering homegrown solutions, and cloud- only providers are among the competitors of ForgeRock.

The IAM market in which we operate is characterized by intense competition, constant change, and innovation. We face competition from (1) legacy providers such as CA Technologies, IBM and Oracle, (2) cloud- only providers such as Okta, (3) companies that provide only a subset of functionality across identity, access and governance and (4) homegrown solutions that are designed to solve a limited identity use case and are difficult to secure, maintain and scale, and quickly become obsolete. Microsoft and other companies that offer a broad array of IT solutions also compete in our market. Source: 10-k

In any case, even if the DOJ decides to block the transaction, I believe that other private equities may be interested in the business model, and may launch new bids for the company.

I Think That The Stock Is Worth More Than $27 Per Share, So I Am Not Worried About The Transaction

There are many reasons to believe that the stock is worth much more than $19-$20 per share. First, financial forecasters out there believe that the company will deliver significant FCF growth from 2025. Market estimates also expect 2025 sales growth close to 22% and positive 2025 net income. With this type of revenue growth and FCF growth, I believe that we could assume a rich EV/FCF multiple.

It is also worth considering that the company obtains revenue from the sale of subscriptions, which represents recurring revenue. With 95% of the total amount of revenue for the three months ended March 31, 2023 being recurrent, I believe that we could expect revenue stability in the coming years. With these conditions, running a DCF model appears ideal.

Our revenue includes recurring revenue from term licenses, SaaS, and maintenance and support (which we refer to collectively as our subscription revenue). We generate substantially all of our revenue from the sale of subscriptions (which excludes perpetual licenses), which accounted for 95% and 96% of our total revenue for the three months ended March 31, 2023 and 2022, respectively. Source: 10-Q

I also believe that we could expect that new AI capabilities to automate decision making could accelerate the efficiency and productivity. I do not know whether the valuation made in 2022 included the fact that artificial intelligence may bring economies of scale. Besides, in my view, if clients appreciate the new functionalities offered thanks to AI, the sale of subscriptions may increase. ForgeRock made a comment about its intentions to invest in AI capabilities in the last quarterly report.

Invest in AI capabilities to automate decision making and deepen the security of our platform. Source: 10-k

With regard to the previous remarks, I believe that investors may want to read the following commentaries from Forbes about how AI could identify and access management.

IAM systems that are backed by AI offer several benefits in three major aspects: authentication, identity management and secure access. Just imagine a world where passwords are no longer needed, behavioral patterns become the new standard for identity authentication and AI and ML algorithms can effectively detect and impede security breaches even before they occur. Source: Forbes

Taking into account my previous remarks, I designed a DCF model with more conservative assumptions than those reported by other analysts. I assumed sales growth going from 22% in 2023 to around 9% in 2031, positive net income in 2026, and net income growth in 2028, 2029, 2030, and 2031.

{kind=link}

The global digital identity solutions market is expected to grow at a CAGR of close to 16.8% from 2022 to 2030, so I believe that my sales growth assumptions are conservative.

The global digital identity solutions market was valued at USD 23.40 billion in 2021 and is expected to grow at a CAGR of 16.8%. Source: Digital Identity Solutions Market Size Global Report, 2022 - 2030

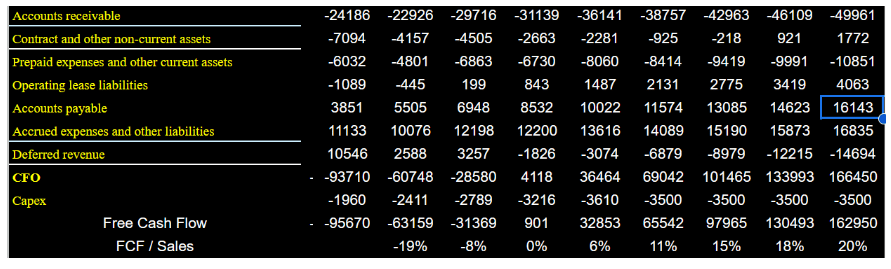

My cash flow model also included 2031 depreciation of $0.7 million, 2031 amortization of $23 million, and changes in accounts receivable of close to $49 million.

{kind=link}

Also, with changes in operating lease liabilities of $4 million, prepaid expenses of $10 million, changes in accounts payable of $16 million, and changes in deferred revenue of $14 million, I believe that 2031 CFO could be close to $166 million. Finally, with capital expenditures of $3.5 million, 2031 FCF would be close to $162 million.

{kind=link}

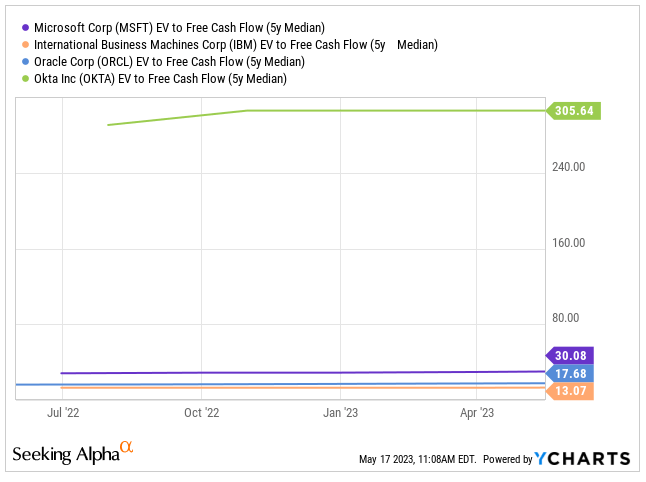

Competitors of ForgeRock, Inc. include Okta ( OKTA ), Oracle ( ORCL ), Microsoft ( MSFT ), and IBM ( IBM ). These companies trade at 13x-305x FCF, so I believe that assuming an EV/FCF ratio of close to 34x is very conservative.

{kind=link}

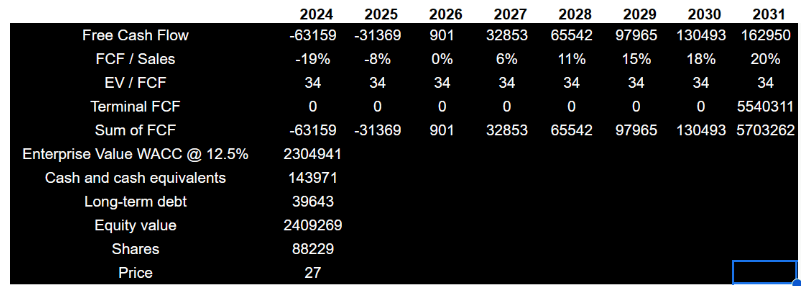

Also, with a conservative cost of capital of close to 12.5%, the sum of future free cash flow figures from 2023 to 2031 imply an enterprise value of $2.3 billion. If we add the current cash in hand, and subtract the current long term debt, the equity valuation would be close to $2.409 billion. Finally, the fair price would be close to $27 per share.

{kind=link}

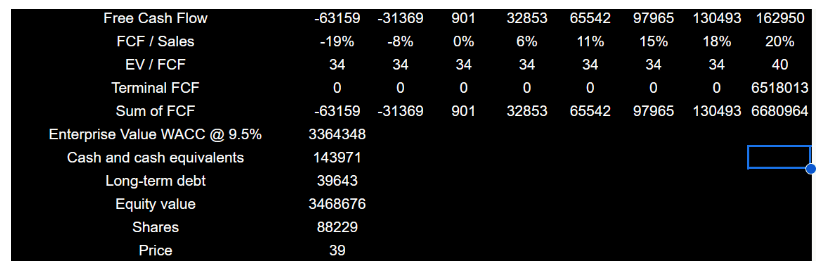

Considering the sensitivity of the financial model, I believe that the fair price could be even higher than $27 per share. With a cost of capital of 9.5%, which other financial advisors are currently using , and an EV/FCF ratio of 40x, the implied valuation could be close to $39 per share.

{kind=link}

I believe that the symmetry of the investment is quite interesting. If the merger closes, which is likely, we would obtain $23.25 per share in cash. If it does not close, which could occur, but I do not believe that it is likely, I believe that we may see a decline in the share price of close to 14%. Keep in mind that the stock price was around $16 per share, when the merger agreement announcement was made. However, in my view, in the long term, shareholders would enjoy a valuation of close to $27 per share or even more. In my view, as soon as market participants see the FCF expected for 2025, the stock price would most likely trend up.

{kind=link}

The Background Of The Merger Revealed That The Financial Advisors Expect 2032 Unlevered FCF Of Close To $260 Million, And Several Other Sponsors Were Interested

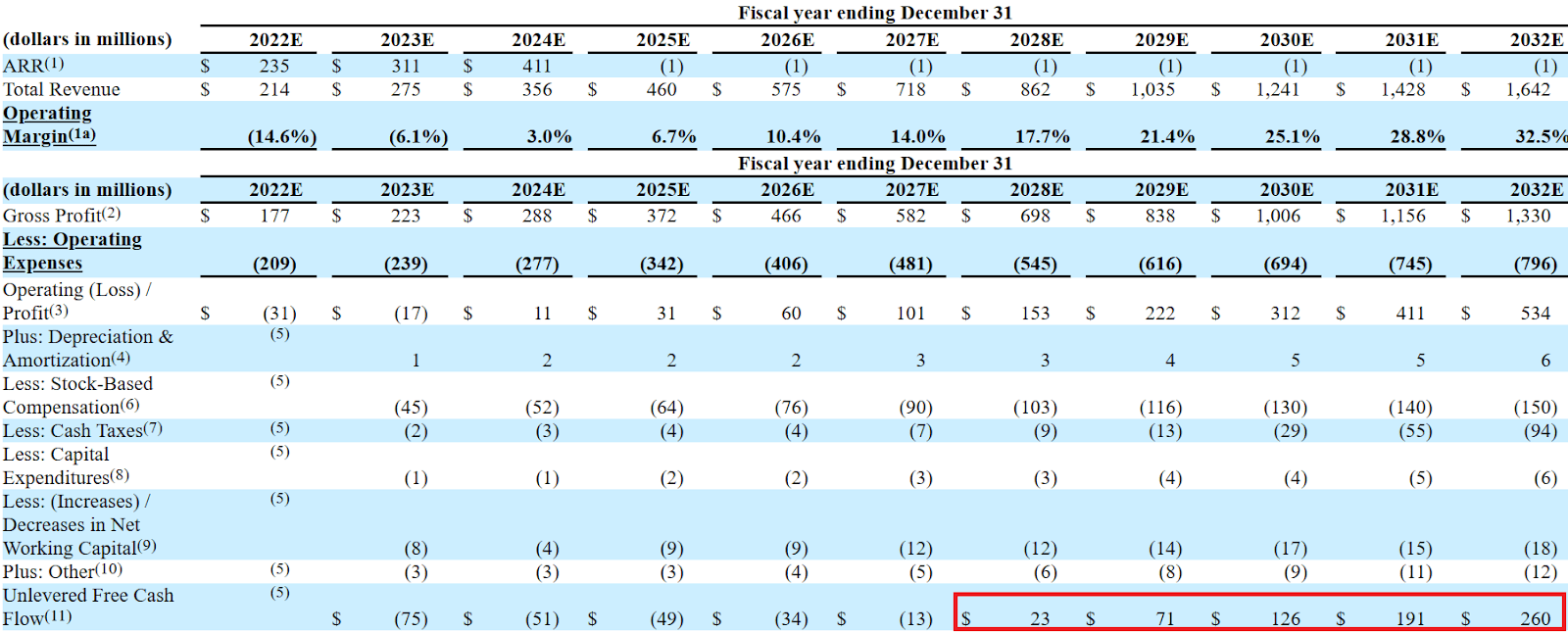

Considering that I gave my own financial model, I believe that investors may want to have a look at the expectations of the financial advisor. In the background of the merger , I could find that the advisor expects 2032 revenue of $1.6 billion and FCF close to $260 million. Considering these figures, I believe that a DCF valuation would imply a valuation of more than $27 per share.

Source: Background Of The Merger

{kind=link}

It is also worth noting that there are other investors that are interested in ForgeRock, Inc. If the DOJ blocks the transaction, other acquirers may show up.

The Strategic Committee updated the ForgeRock Board on the status of discussions with Thoma Bravo, Sponsor A, Sponsor B and Sponsor C. Source: Source: Background Of The Merger

Solid Balance Sheet With Not A Lot Of Debt, Cash In Hand, And A Small Amount Of Liabilities

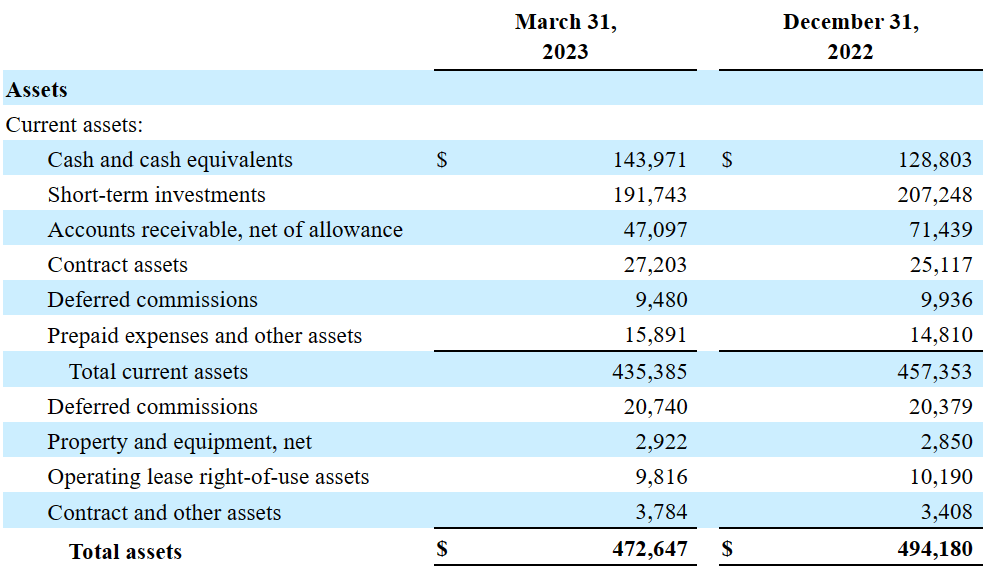

I also believe that the financial position reported by ForgeRock, Inc. is quite solid. The company does not really need to be acquired because it does not really have a lot of debt, and the asset/liability ratio stands at more than 2x. Besides, management also reports a considerable amount of cash. As of March 31, 2023, the cash in hand stood at $143 million with short-term investments worth $191 million.

{kind=link}

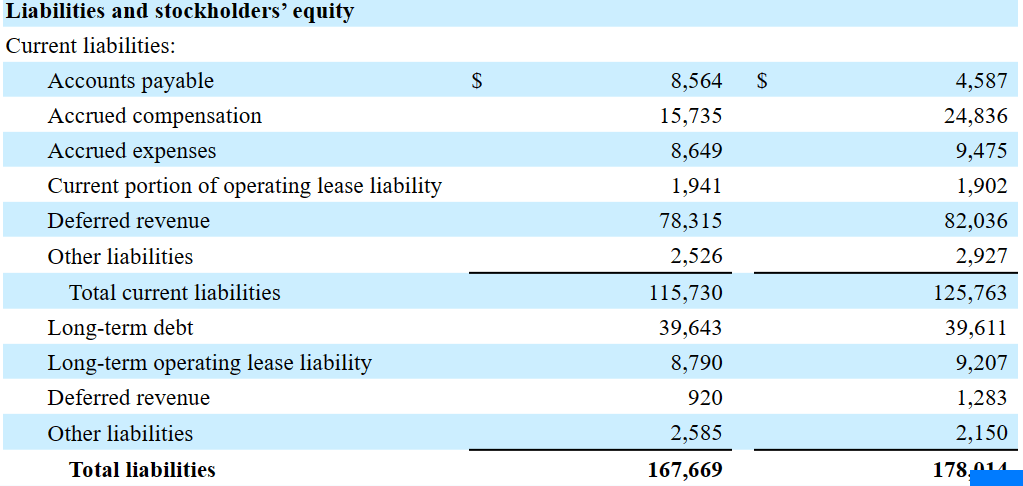

The list of liabilities does not seem worrying. Management reported deferred revenue worth $78 million, accrued compensation of $15 million, and long-term debt worth $39 million. Total liabilities were equal to $167 million.

{kind=link}

Risks

If the DOJ finally blocks the transaction, I believe that the investors may see the stock price decline to around $16 per share. I do not believe that this is a likely scenario because the agreement was signed a few months ago, and the DOJ may have blocked the deal a long time ago. Perhaps, the DOJ forces Thoma Bravo to sell certain parts of the business model, but I would not expect a complete failure of the merger.

If the merger does not close, I believe that the company could suffer a crisis of confidence for some time. Litigation could be expected, which affects the relationships the company has with investors, clients, and other service providers. Management made several comments in this regard in the last annual report.

Investor confidence in us could decline, stockholder litigation could be brought against us, relationships with existing and prospective customers, service providers, investors, lenders and other business partners may be adversely impacted, we may be unable to retain key personnel, and our operating results may be adversely impacted due to costs incurred in connection with the Merger. Source: 10-k

If the merger does not close, I believe that investors will do good by not selling the share. Under this case scenario, there are other risks that investors have to keep in mind. First, lower revenue growth than expected would most likely lead to lower FCF growth expectations, which may imply lower fair valuation. As a result, I believe that investors may sell their shares.

If we fail to manage our growth effectively, we may be unable to execute our business plan, maintain high levels of service and customer satisfaction or adequately address competitive challenges. Source: 10-k

I also think that lack of information or wrong information from third parties could bring a lot of issues for ForgeRock. The company uses this information to verify data about identities. Failed identification may bring reputation issues, and clients may leave the company.

Certain estimates and information that we refer to publicly are based on information from third-party sources and we do not independently verify the accuracy or completeness of the data contained in such sources or the methodologies for collecting such data, and any real or perceived inaccuracies in such estimates and information may harm our reputation and adversely affect our business. Source: 10-k

Finally, I believe that lack of new financing from investors or lack of liquidity could significantly complicate future operations. First, ForgeRock, Inc. may not be able to hire that many new employees as it did recently. As a result, development of new identification software may slow, which may bring lower revenue growth.

{kind=link}

My Conclusion

ForgeRock is still waiting for the approval from the DOJ, which is the last condition to approve its acquisition by Thoma Bravo. Considering that this is a new growing market with many actors, I do not think that the DOJ would block the transaction. I also think that the company is worth $27 per share or more. If the DOJ blocks the transaction, other acquirers may appear. I could also see that the financial advisor in the M&A agreement included a 2031 revenue forecast of $1.6 billion and 2031 FCF of $260 million, significantly larger than my estimate. Taking into account these figures, I believe that other advisors may offer more money for ForgeRock.

For further details see:

ForgeRock: Undervalued And Likely To Benefit From AI And Thoma Bravo Acquisition