TGT - Forget General Motors And Buy These High-Yield Dividend Aristocrats Instead

2023-10-11 07:15:00 ET

Summary

- General Motors is facing multiple challenges, including a potential recall of 20 million airbags and a strike by the UAW.

- The company's historical performance and dividend cuts make it an unattractive investment option. This industry isn't conducive to long-term dividend growth.

- GM's long-term consensus return potential of 4% is bond-like. GM's returns since it exited bankruptcy have been equal to those of bonds.

- I have never owned and will never own GM or any dividend paying automaker. It's one of 3 industries I avoid (shipping and coal are the others).

- Here are two high-yield aristocrats trading at 52-week lows whose fundamentals are intact. They are not value traps like GM which has lost investors money since its 2010 IPO. One yields a very safe 6.4% and the other offers over 400% return potential over the next decade.

It's always a market of stocks, not a stock market.

Stocks At 52-Week Lows

{kind=link}

Many wonderful companies are trading in the toilet, and many terrible companies deserve to be flushed away forever.

I've been inundated with requests from members via direct message asking me for updates about their favorite companies. So, I'll combine several requests to cover as many companies as possible while teaching some timeless and invaluable wisdom. Wisdom can hopefully teach you how to avoid value traps and specific industries that dividend investors should avoid, like the plague.

Why GM Is A Value Trap, I'll Never Buy

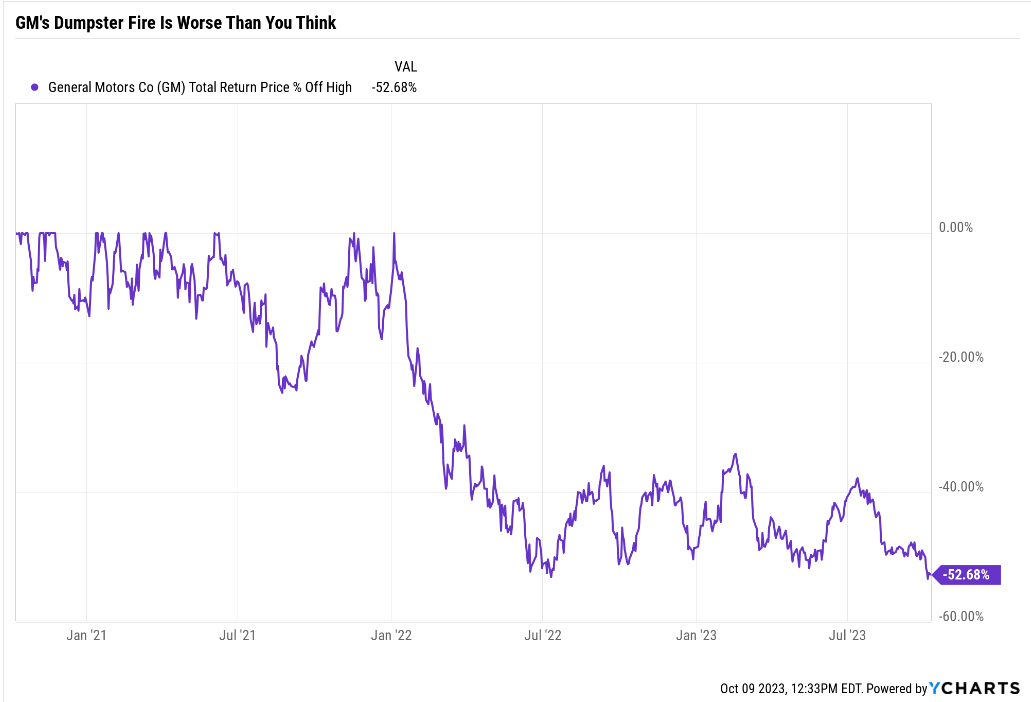

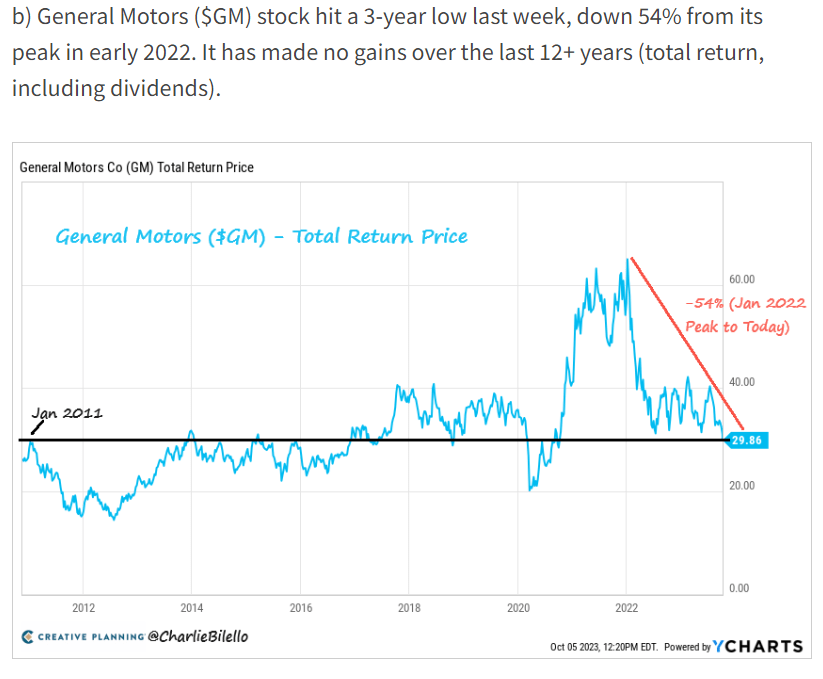

I've never owned General Motors ( GM ), and I never will. Is it because of this chart?

{kind=link}

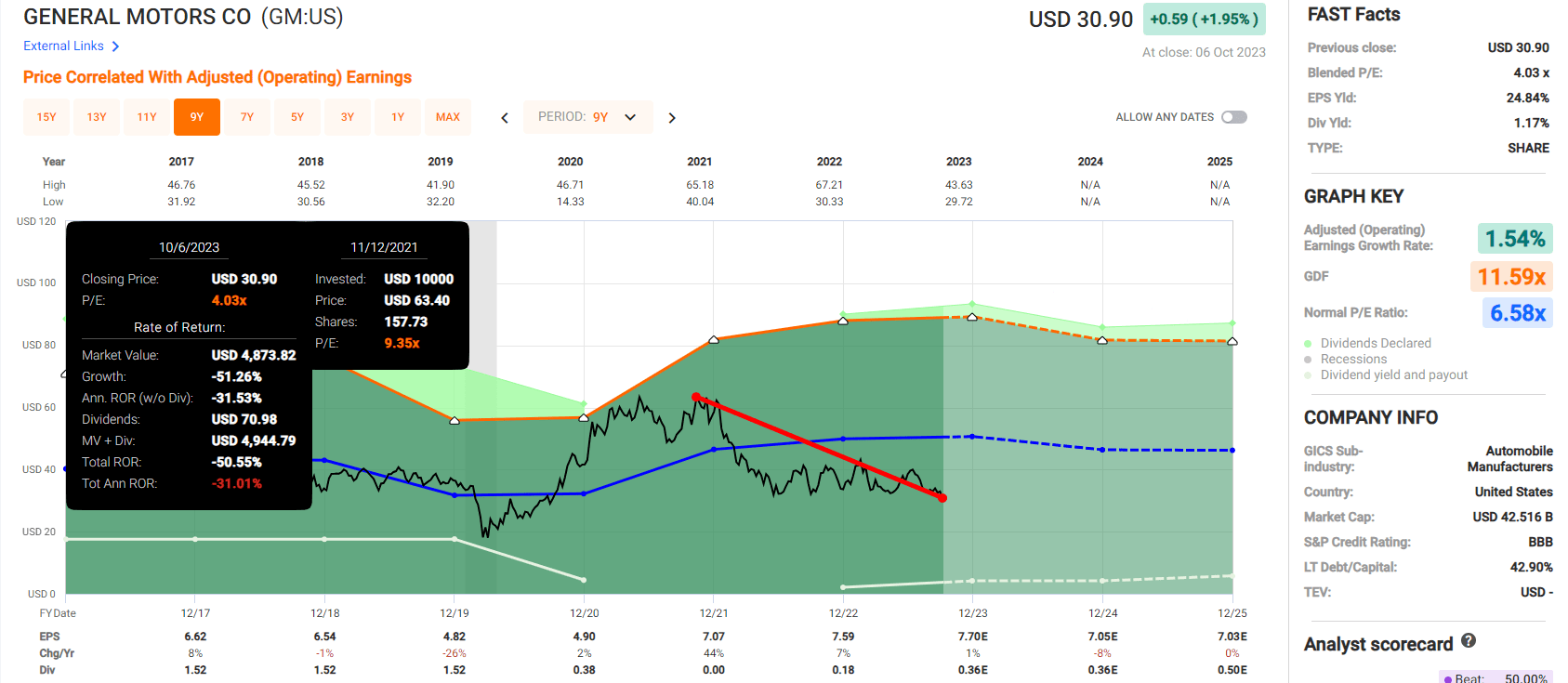

That's certainly an ugly chart. What caused GM to fall 53%? It wasn't valuation, because at its 2022 peak GM traded at less than 10X earnings.

{kind=link}

Maybe it's because GM went "woke" and drank the EV Kool-Aid?

{kind=link}

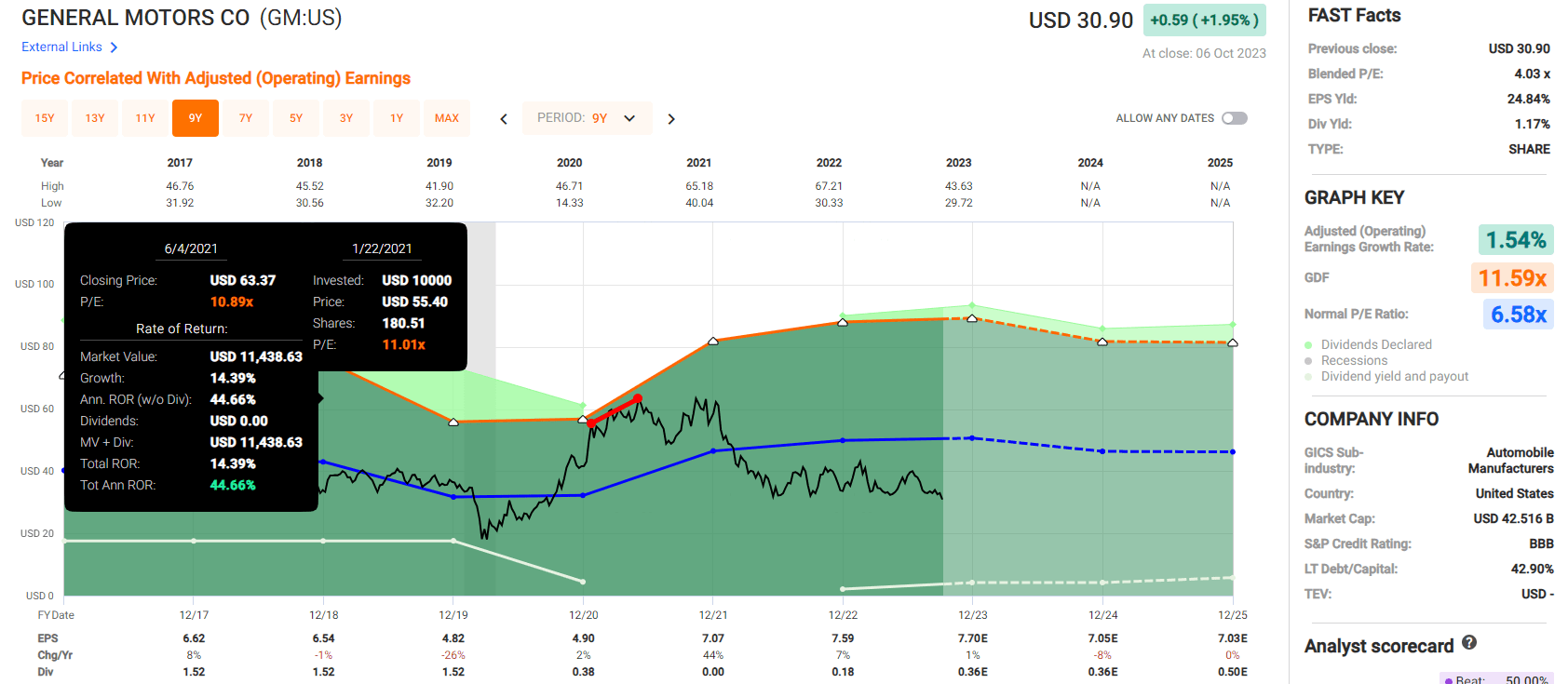

Nope, not really. In fact, GM's stock price hit its new highs after announcing the big EV initiative.

{kind=link}

The company announced today it's investing $918 million in four of its facilities for "V-8 engine production, EV components." The EV components part comprises of a mere $64 million, less than 10%, going toward two of its facilities." - Elektrek

GM is still all-in on trucks, including diesel trucks. And its EVs aren't exactly eco-conscious unless you think we're all going to save the earth by driving EV hummers.

- the Hummer EV weighs over 9,000 lbs, twice the weight of a Chevy Silverado 1500 full-size pickup.

- Its 3,000 lb battery weighs as much as a Honda Civic.

- 53 mpgE vs 140 mpgE for the most efficient EV, the Hyundai Ioniq 6

OK, but GM is slashing its dividend, right? To pour cash into the money-losing EV business? And you've said many times, "when the dividend is cut, it's time to sell".

My approach to companies that cut their dividends, even dividend aristocrats.

From Hell's heart I stab at thee . For Hate's sake, I spit my last breath at thee ." - Khan, Star Trek 2 The Wrath of Khan

Here's the dividend consensus for GM.

- 2023: $0.36

- 2024: $0.36

- 2025: $0.50

Nope, it's not because GM is expected to cut its dividend, at least not for the foreseeable future.

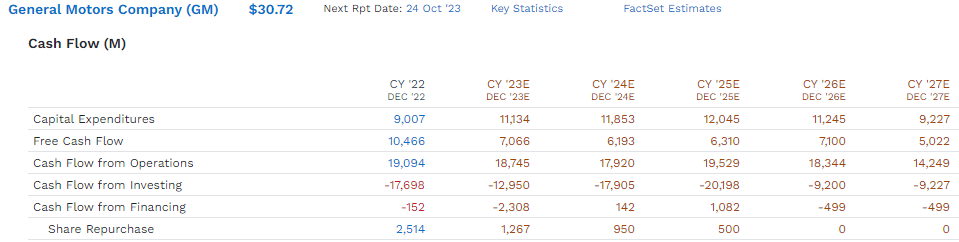

Okay, but the earnings must be about to go off a cliff, right? Because building all that EV infrastructure is going to cost a lot?

{kind=link}

Well, it is true that GM's capex is going to soar by about $3 billion per year in the next few years, and its free cash flow is expected to fall by 50%.

Is that why the stock price is down?

{kind=link}

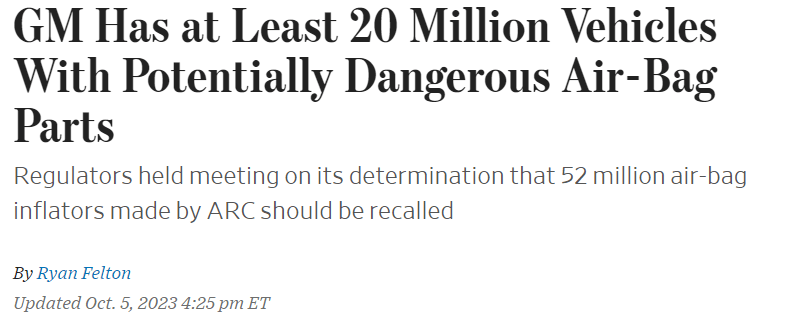

Or is it that GM might be on the hook for 20 million airbags being recalled?

Or is it that the UAW strike is in its 4th week, and the UAW is asking for a package that will cost an average of $270,000 per worker?

Actually, the UAW asks would cost approximately $900 million per year extra for GM, which is less than 20% of its 2027 consensus free cash flow.

So why don't I like GM? Why have I never been tempted to buy it? Why will you never see me recommend buying it even at a 52-week low and just 4.4X forward earnings?

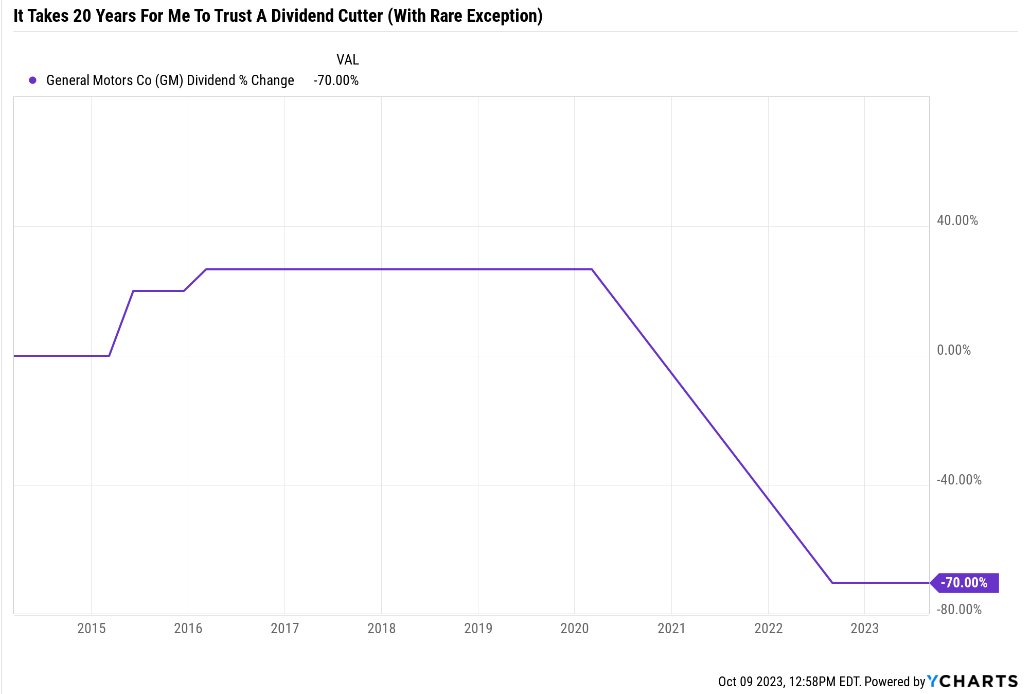

Never Trust A Dividend Cutter (With Rare Exception)

{kind=link}

GM did cut its dividend during the Pandemic. In fact, it was suspended and brought back at 30% the previous rate.

Ben Graham considered a 20-year streak without a dividend cut to be an important sign of quality. 20+ year dividend growth streaks are the Graham sign of excellence.

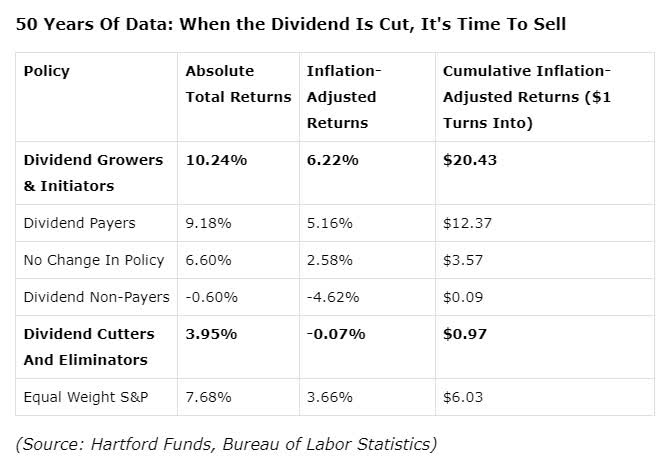

And what about dividend cutters?

{kind=link}

Dividend cutters almost always tend to be terrible companies. And in the case of GM?

90% Statistical Probability You Should Never Own GM

{kind=link}

GM has been flat over the last 12 years. Statistically speaking, 90% of companies that are flat for that long are just bad companies you should avoid.

Oh it gets worse though. Inflation in the last 12 years has been 39%, so GM is actually down 39% adjusted for inflation.

What about dividends?! That -39% inflation-adjusted return includes dividends!

- -4% inflation-adjusted total return (including dividends) for 12 years

That's a dumpster fire of an investment and it should be no surprise that GM has suffered this fate.

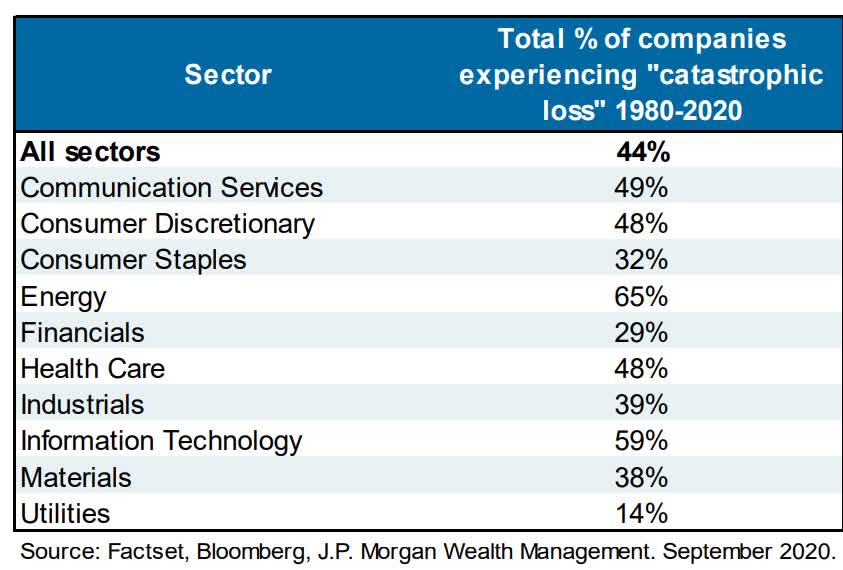

{kind=link}

44% of all US stocks end up in the toilet, suffering a "permanent catastrophic" 70+% decline from which they never recover.

Avoiding such companies is imperative for anyone buying individual companies.

Car makers are cyclical, and there is generally no moat with rare exceptions for the likes of Ferrari or Tesla where brand loyalty is strong.

That's why they tend not to make great dividend stocks. Even great car markets like Honda or Toyota still don't do well over time.

And in case you think I'm cherry-picking, let's remember two things.

- GM went bankrupt in the GFC and wiped out investors

- the shares trading today popped into existence in Dec 2010

How has GM performed since its brand-new IPO 13 years ago?

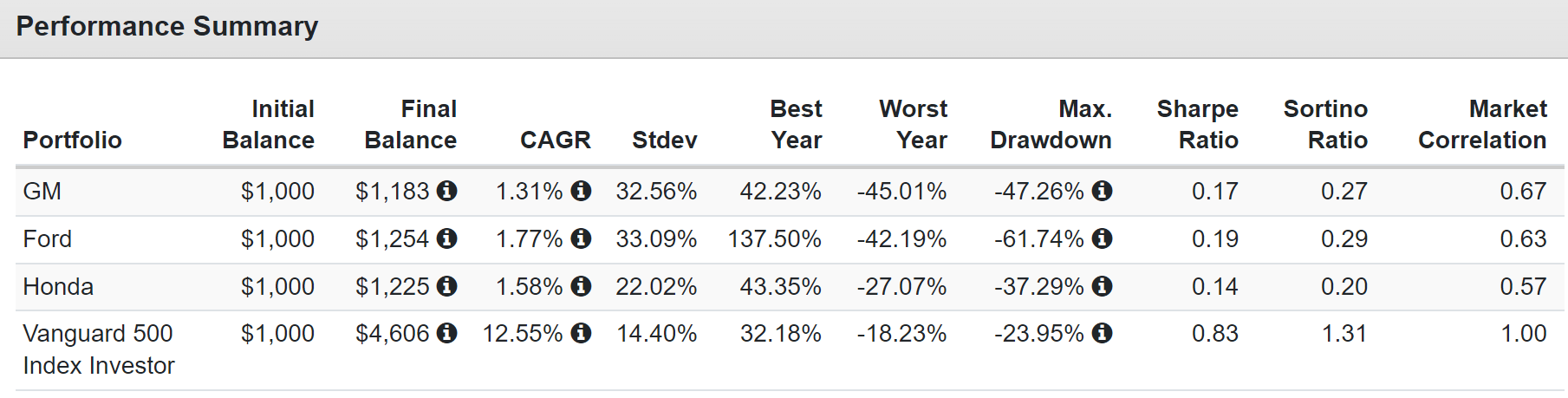

Historical Returns Since 2010

{kind=link}

How about other automakers?

- Toyota: 8.5% CAGR

- BMW: 6.8% CAGR

- Mercedes: 3.3% CAGR

- Tesla: 44% CAGR

If you buy a brand of car that people love or at least trust a lot (like Toyota #1 automaker on earth), you can do OK. BMW and Toyota investors have made out fine. Except for one thing.

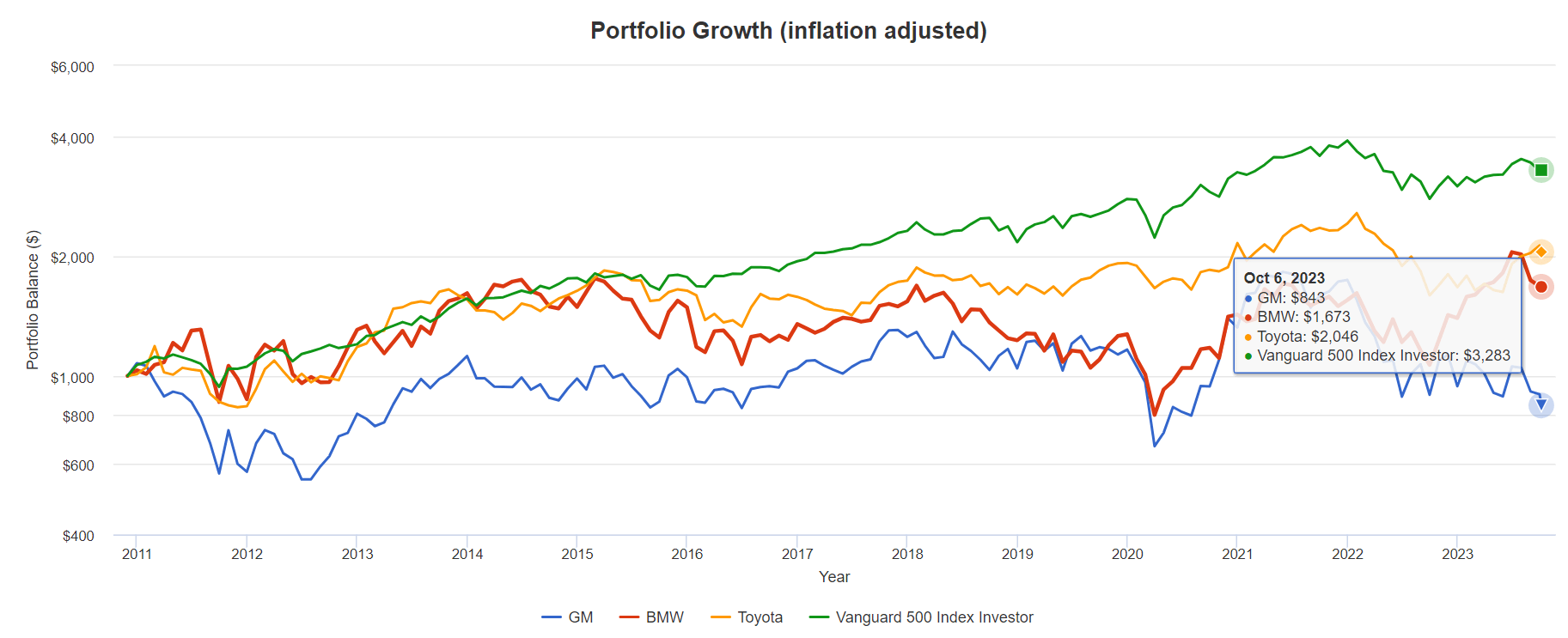

Inflation & Dividend Adjusted Returns Since Dec 2010

{kind=link}

- GM: -16% = -1.3% CAGR

- BMW: 67% = 4.0% CAGR

- Toyota: 105% = 5.7% CAGR

- S&P 500: 228% = 9.8% CAGR

Now, I'm not saying that everything has to beat the S&P in a tech-fueled bubble. But I would like to think that after 13 years you would have made money with a decently run company.

Ok, but isn't this being unfair to GM? Can't cyclical companies, if you cherry-pick the time frame, lose money for over a decade?

Let's compare GM to Exxon and Chevron, remembering that the last 13 years include the worst decade for energy stocks in human history.

- two historical oil crashes

- including this one

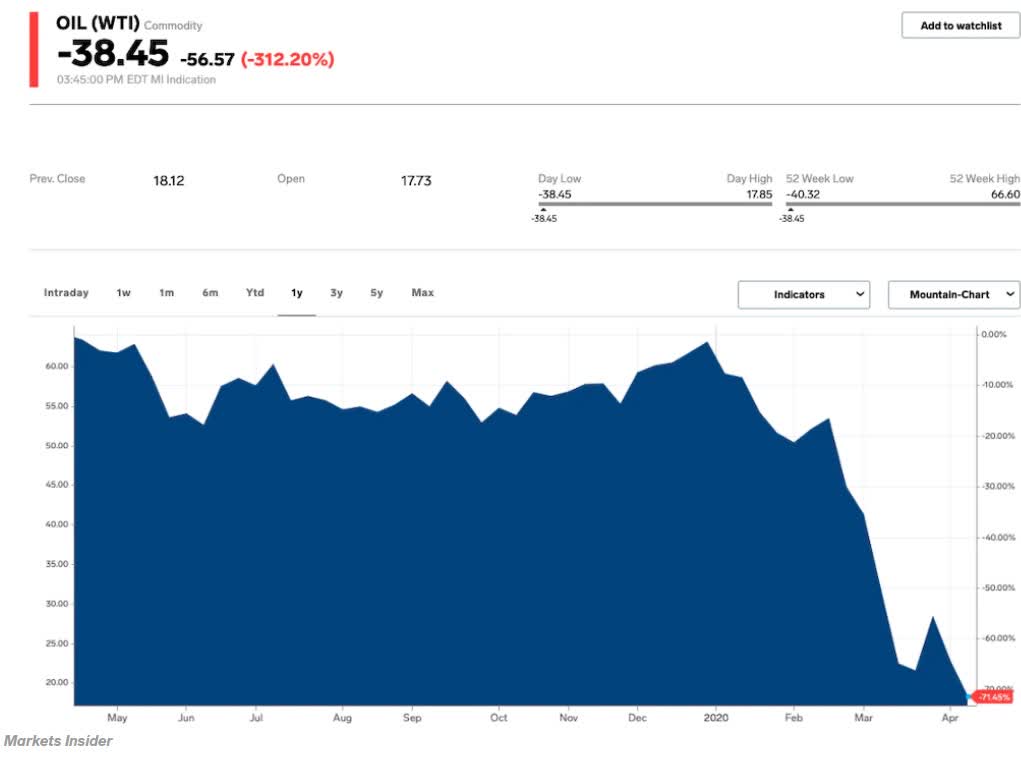

{kind=link}

April 20th, 2020, oil hit -$38. Oil spent a decade flat, and how about the last 13 years?

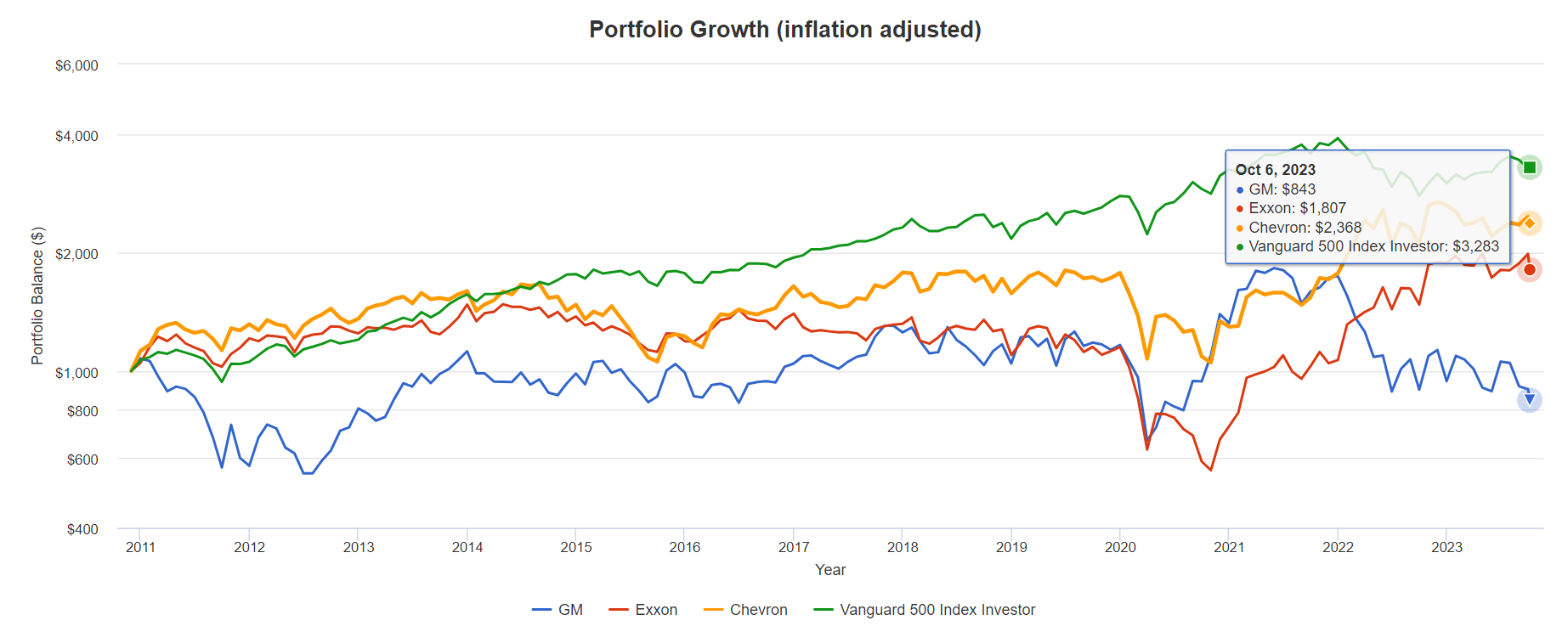

Inflation & Dividend Adjusted Total Returns Since 2010

{kind=link}

- GM: -1.3% CAGR

- AT&T: 0.5% CAGR

- BMW: 4.0% CAGR

- Exxon: 4.7% CAGR

- Toyota: 5.7% CAGR

- Chevron: 6.9% CAGR

Is BMW a bad company? No, it's just a bit of bad luck. Are Exxon and Chevron bad companies? They've beaten the S&P over the last 38 years.

- 97% statistical probability they are good companies

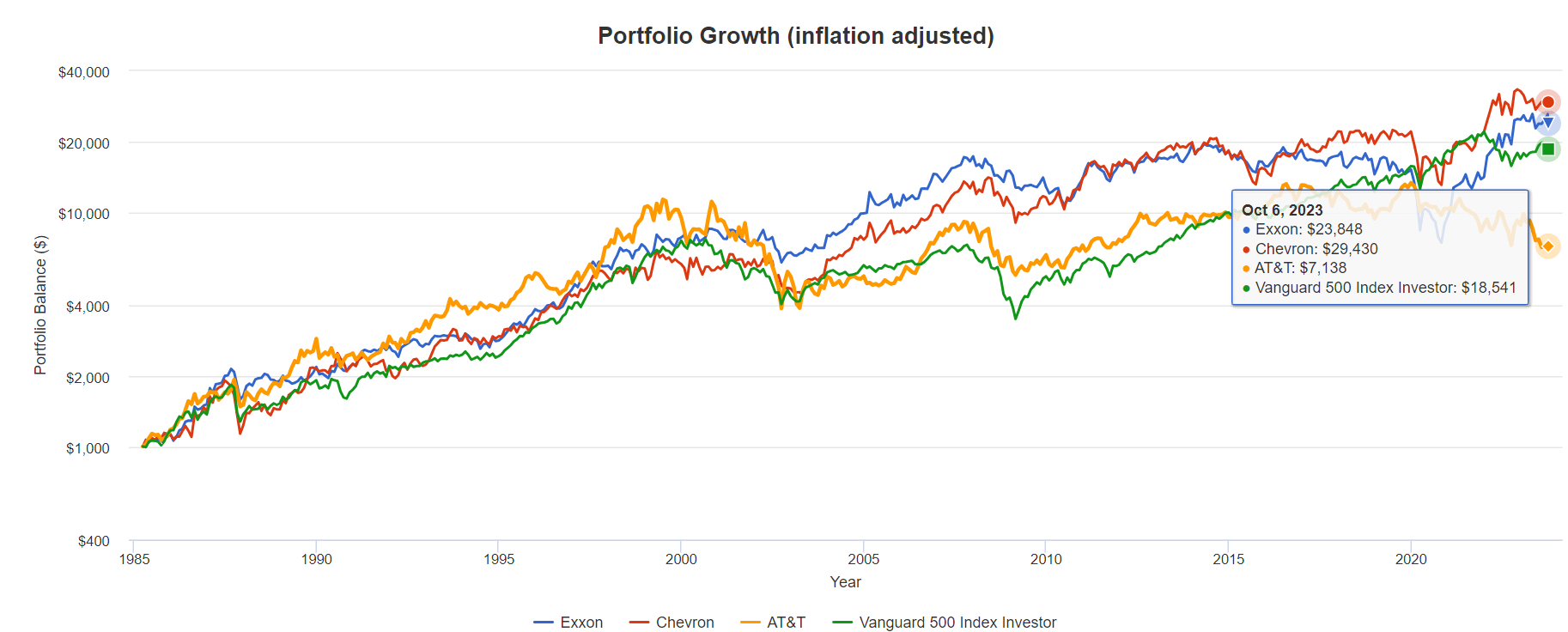

Inflation & Dividend Adjusted Returns Since 1984 (39 Years)

{kind=link}

- AT&T: 5.2% CAGR (flat for the last 26 years!)

- S&P 500: 7.8%

- Exxon: 8.5% CAGR

- Chevron: 9.1% CAGR

The probability of a good company being flat for 26 years is approximately 9%. So that's a 91% chance that AT&T is a low-quality company you want to avoid.

Exxon and Chevron? There is just a 3% chance that they got lucky and managed to beat the market over 39 years in a highly cyclical industry.

No, that's the power of relatively safe and steadily growing dividends being reinvested in the many energy crashes.

- the same reason tobacco blue-chips are so successful long-term

But without a secure dividend? That grows consistent? Well, you are far more likely to fall victim to decades of weak or even negative returns.

That's why you won't see me ever recommend GM or any automaker. As far as dividend growth stocks, it's just not a good industry.

The same is true for coal and shipping. The economics of these three industries are just not conducive to safe dividend growth and good, market-beating returns.

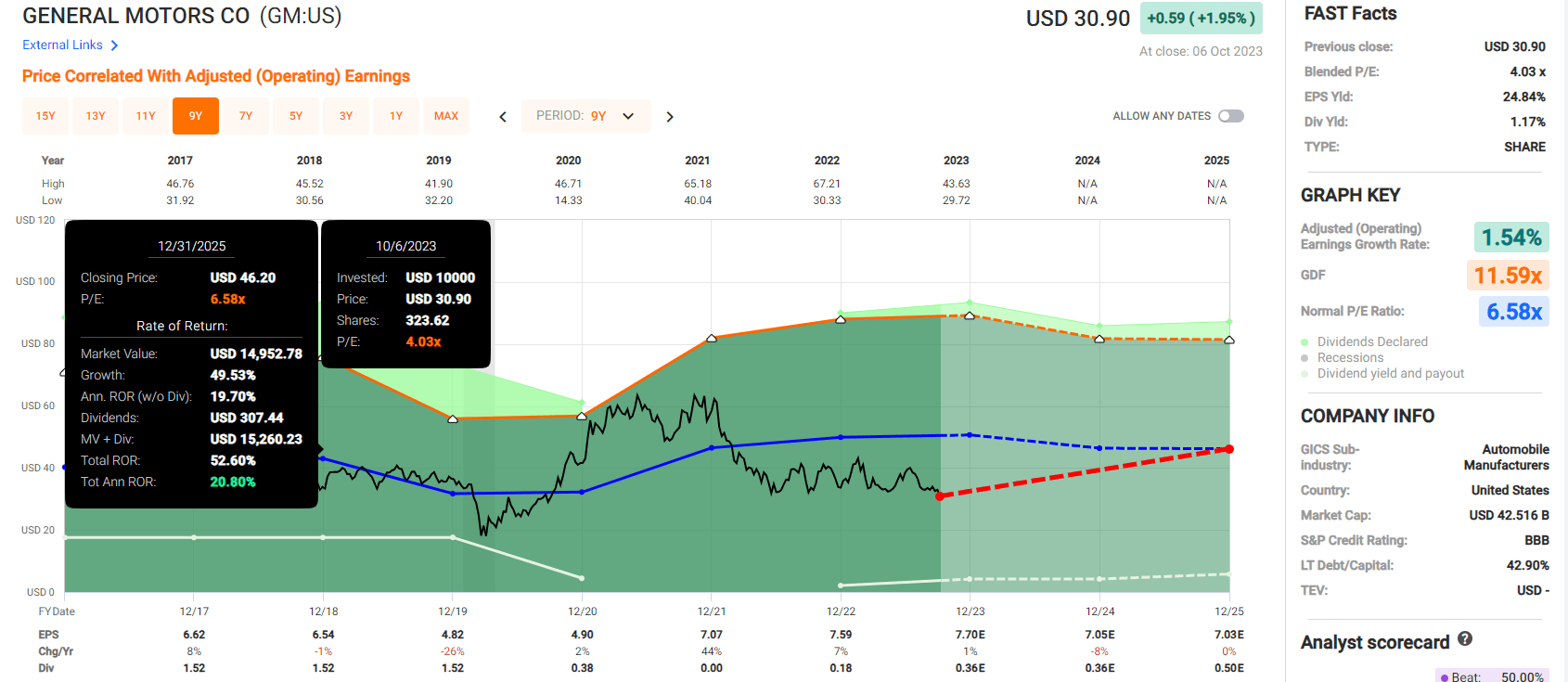

What About Valuation?! 4X Earnings!

{kind=link}

First, let's get this out of the way. GM is expected to grow 2% to 3% over time and yields 1.2%. That's a 3.8% long-term consensus total return potential.

- 30-year US Treasuries yield almost 5%

- and over the next 30 years are expected to outperform GM

When a stock isn't expected to outperform risk-free government bonds, I have no interest.

But what about that 4 PE! That's an earnings yield of 25%!

Surely Ben Graham would be pounding the table about GM at these valuations!

Don't get too excited. GM's cash-adjusted PE is 7.4X because of all its debt.

And let's not forget that the 15 PE rule of thumb doesn't apply to cyclical stocks like this.

{kind=link}

GM is undervalued without question. But it's not worth 15X earnings, not even close. Its bubble high was less than 10X earnings. No less than Ben Graham said that over long enough time periods, the market will "weigh the substance of a company" and tell you its fair value.

This is GM's historical market-determined fair value, 6 to 7X earnings.

If you pay 8X earnings for GM? Normally, an anti-bubble valuation pricing in -1% growth. You're overpaying for an inflation-adjusted no-growth company that will earn you about 1.2% real returns.

- 30-year US treasury real yield is 2.7%

GM offers about 60% worse real return potential, adjusting for inflation and dividends than US treasury bonds.

But what about the 53% upside potential through 2025? That's 21% annual return potential! Yes, it is.

So, if you want to buy GM, you're doing it as a deep-value play, not a long-term investment.

If you buy GM to buy and hold forever, you're not being prudent or rational; you're doing it for the love of the company and its cars.

Buying GM Stock Makes As Much Long-Term Financial Sense As My Single Share Of The Packers

{kind=link}

If you want to buy GM, understand that it is a trade, not a buy-and-hold forever investment. Use trailing stops once its overvalued (above a PE of 7) and then have the market sell you out at a profit.

Otherwise, you'll very likely regret it, especially when there are far superior options such as these two dividend aristocrats you can buy right now.

NNN REIT (Formerly National Retail Property Trust) ( NNN )

Further Reading

NNN is not suffering due to any fundamental issues. This 33-year dividend growth streak dividend champion would be an aristocrat if it were big enough to be in the S&P. In fact, NNN hasn't cut its dividend since it began paying one 35 years ago.

How do I know this 6.4% yielding unofficial aristocrat and future dividend king is rock solid?

Its occupancy rate is steady at 99.2%, and it is expected to remain at 99.1% next quarter.

Its interest coverage ratio is steady at 4.4X to 4.5X, and rating agencies consider 2+ safe for this industry.

The debt/EBITDA (leverage) ratio is 5.3, and 6X or lower is safe according to rating agencies that rate it BBB+ stable, tied for the 3rd highest credit rating in REITdom.

According to rating agencies, 90% payout ratios are safe for this industry, and NNN's is 69%.

If 31% of rent stopped immediately and forever, NNN could still easily pay its dividend.

In the Pandemic, despite unprecedented lockdowns for many of its tenants, NNN's AFFO fell just 10%.

In the Great Financial Crisis, when all but 17 REITs cut their dividends as credit markets slammed shut, NNN kept on growing its dividend and its AFFO only fell 21%.

For NNN's dividend to be threatened, its cash flow would have to be permanently reduced by at least 32%, something that would require a Great Recession + Pandemic and be permanent.

NNN is anti-GM. A rock steady recession-resistant ultra-yield Ultra SWAN dividend aristocrat and future dividend king you can trust.

Fundamental Summary

- Yield: 6.4%

- dividend safety: 96% very safe = 1.2% dividend cut risk

- overall quality: 96% Ultra SWAN

- growth consensus: 3.0% vs. 6% for the REIT sector

- total return potential: 94% CAGR vs 10.2% S&P 500 and 10% sector and 11% aristocrats

- current price: $35.20

- historical fair value: $53.72

- discount to fair value: 13%

- DK rating: potential good buy

- 10-year valuation boost: 1.4% per year

- 10-year consensus total return potential: 6.4% yield + 3.0% growth + 1.4% valuation boost = 10.6% per year

- 10-year consensus total return potential: = 174% vs 160% S&P

{kind=link}

NNN isn't a fast-growing REIT; it's a utility and a slow-growing but very safe one. Yet, thanks to the current interest rate freakout, it has almost 100% upside to fair value by 2025. In fact, in the next four years, your money will likely double if it grows as expected and returns to fair value.

That's about 2X the return potential of GM.

Target ( TGT )

Further Reading

{kind=link}

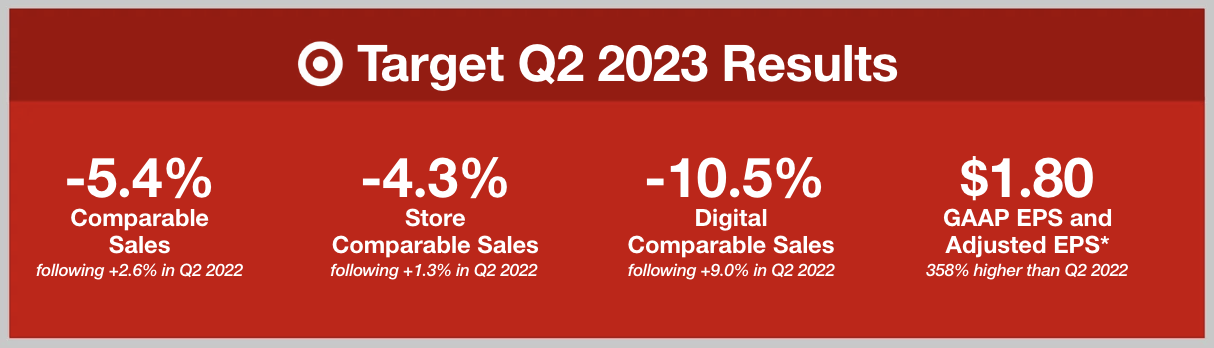

Yes, Target is facing some major fundamental issues in the short term. Largely, these are things outside its control, such as high inflation. The big negative comps are partially due to the company struggling to stock enough inventory in the early days of the Pandemic and over-ordering as most companies did.

{kind=link}

The company has a sensible plan for improving its stores and reversing the temporary decline in same-store sales.

Rating agencies are confident in TGT's plan, giving it an A-stable rating with a 0.66% 30-year default risk.

The Bond Market's Real-Time Bankruptcy Risk Estimates

FactSet Research Terminal

The bond market estimates TGT's fundamental risk at 2.43%, an A- credit rating.

That fundamental risk has been stable over the last six months.

{kind=link}

The dividend, earnings, and free cash flow are expected to grow at a nice clip.

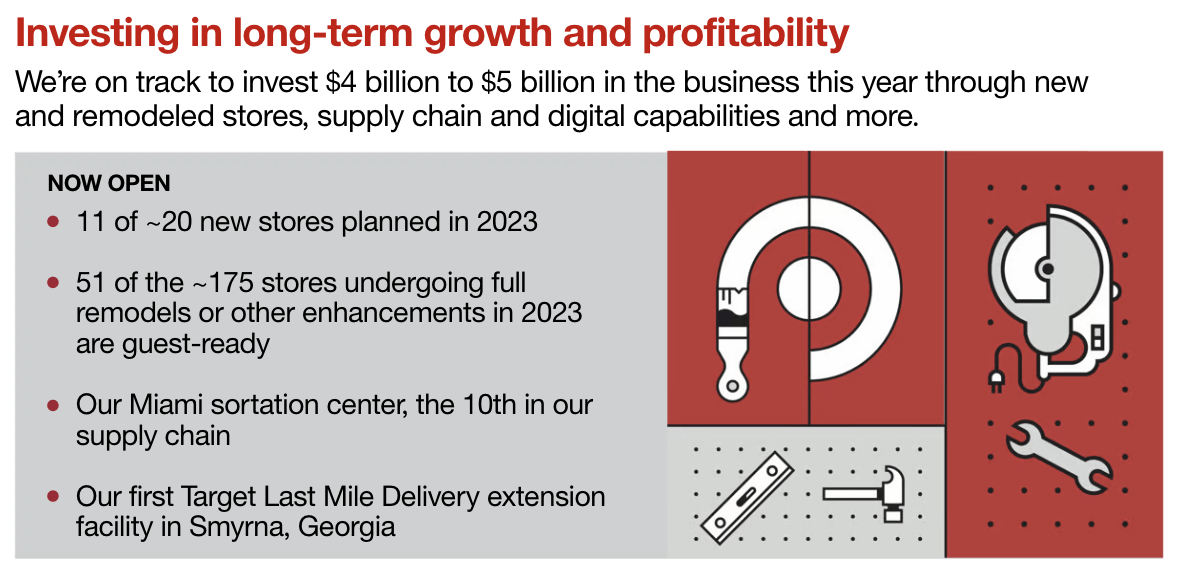

Long-term double-digit growth is expected to be powered by steady 3% to 4% same-store sales beginning in 2024 (next year is a recession), rising margins, and buybacks.

In other words, Target's thesis is not broken, and it's a potentially wonderful time to buy this dividend king with a 51-year dividend growth streak.

Fundamental Summary

- Yield: 4.2%

- dividend safety: 100% very safe = 1% dividend cut risk

- overall quality: 98% very low-risk Ultra SWAN

- growth consensus: 10.6% vs. 8.5% S&P 500

- total return potential: 14.8% CAGR vs 10.2% S&P 500 and 11% aristocrats

- current price: $105.76

- historical fair value: $149.63

- discount to fair value: 29%

- DK rating: potential very strong buy

- 10-year valuation boost: 3.5% per year

- 10-year consensus total return potential: 4.2% yield + 10.6% growth + 3.5% valuation boost = 18.3% per year vs 10.1% S&P

- 10-year consensus total return potential: = 437% vs 160% S&P

More than twice the yield of the S&P and 3X the return potential over the next decade.

{kind=link}

Note the big spike in post-pandemic earnings and a big decline as the one-time sugar rush ran off. TGT's long-term growth prospects appear solid, offering superior short-term return potential than GM and about 5X better long-term return potential.

Bottom Line: Forget GM And Buy These High-Yield Dividend Aristocrats Instead

GM is perhaps a good company but a bad business. Its volatile earnings, so the market pays less than 7X for its cyclical fundamentals.

It's not a wide-moat company, and its EV transition plan is 100% necessary and also something that will be costly and cut its free cash flow in half.

While it can deliver around 50% to 60% returns in the next two years, I would never hold GM long-term. History has shown that it is a 97% likely road to disappointment and, in many cases, tears.

In contrast, NNN is a recession-resistant dividend aristocrat REIT offering a mouthwatering potentially safe 6% yield and steady, if not inspiring, 3% long-term growth.

But right now, that's good enough for 80% returns in the next two years and potentially almost 200% in the next ten years.

Target is a solid growth investment that offers an attractive 4.2% yield and double-digit growth potential. TGT's short-term return potential is about 20% higher than GM's.

I can't think of any logical reason why a long-term income growth investor would buy GM over these two far higher-quality businesses.

For further details see:

Forget General Motors And Buy These High-Yield Dividend Aristocrats Instead