FWONK - Formula One Group: Adjusted OIBDA Should Grow At A Robust Rate

2023-12-11 17:40:03 ET

Summary

- Reiterating a buy rating for FWONK based on a positive outlook for adjusted OIBDA growth driven by top line growth and operating leverage.

- 3Q23 Adjusted OIBDA beat expectations, driven by healthy performance in main revenue drivers.

- I expect the Vegas Grand Prix to generate strong revenue and create new revenue streams, but higher year-one operating expenses have impacted valuation.

Summary

Readers may find my previous coverage via this link . My previous rating was a buy, as I believed Formula One Group ( FWONK ) would continue to grow its adjusted operating income before depreciation and amortization [OIBDA] at 20% over the next few years. I am reiterating my buy rating for FWONK as I remain positive about its adjusted OIBDA growth outlook, driven by top-line growth and operating leverage. I believe the compression in valuation multiples is due to the elevated year-one cost structure for the Vegas Grand Prix. Valuation should re-rate back to the historical average as FWONK continues to show that margins can expand.

Financials/Valuation

FWONK reported mixed 3Q23 headline results , where revenue was $887 million (below consensus of $901 million), but adjusted OIBDA beat by $1 million ($215 million vs. $214 million). However, on a deeper look, I think FWONK did well for 3Q23, and the outlook remains robust. On the revenue miss, it was driven by other F1 revenue that came in at $97 million. The main revenue drivers, which include Race Promotion, Media Rights & Sponsorship, continue to look healthy, coming in at $790 million, representing 27% y/y growth. On adjusted OIBDA, it grew 26% on a y/y basis, benefiting from the reduction in team payment expenses.

Based on author's own math

Based on my view of the business, I expect FWONK to continue growing positively by 26% in FY23 (continuing the momentum from 3Q23 and the Vegas event), followed by a normalized growth back to 10% (pre-COVID FY19 levels). I note that FY23 is going to be an extraordinary year because of the Vegas Grand Prix; as such, FY24 is not going to experience the same easy competition that FY23 is going to face (FY22 has no Vegas Grand Prix). On a like-for-like basis, growth in percentage terms should taper down. However, I expect the adjusted OIBDA margin to continue expanding as FWONK continues to see operating leverage from a reduction in team payments as a percentage of pre-teen share adjusted OIBDA. Relative to the last time I wrote about FWONK, valuation de-rated further to the current 20x forward EBITDA (a proxy for adjusted OIBDA). I believe the reason for this de-rate is the higher than expected year-one operating expenses for the Vegas Grand Prix, which led to investors becoming more careful about the following years' profitability. As such, when FWONK shows margin can continue to expand, as I discussed below, valuation should re-rate back to the historical average of 21x, leading to my price target of $78.

Comments

The focus of FWONK is the Vegas event . During the call, management practically confirmed that they are going to generate at least $500 million in revenue from the Vegas event and set the expectation that this is going to be a major growth driver for FWONK in the long term. Specifically, they highlighted the possibility of increased direct and indirect revenue streams.

But more importantly, we think the Vegas experience will create commercial opportunities beyond the race itself and accrue to the broader F1 ecosystem. The Amex partnership we recently announced is a great example, and there are more to come. Source: 3Q23 earnings

During the call, management explained that the higher cost structure was a result of the launch costs, which include a number of one-time items like an opening ceremony, the development of a multipurpose app, and additional provisions for traffic flow and safety. Hence, I am not too bothered by the increased cost structure for the year-one operation, as I think management is investing in the right places to ensure this event can operate without hiccups. As such, with year one done, I believe the following years' profitability will increase as these non-recurring expenses disappear and management knows how to operate the event more efficiently.

That said, as much as management had planned and prepared for the event, an accident occurred during one of the practice sessions. From the headline, it seems like FWONK failed to do all its checks, but I note that related incidents (drainage cover issues) are not uncommon, as this happened before back in 2019. The fact is that the covers were secured in advance. It was the systems that were securing the covers at fault (usually not tested with real F1 cars until practice sessions start). In hindsight, it is not exactly FWONK's fault, but they possibly could have done a better job. Nonetheless, I think this is going to be a great lesson for management so that such incidents do not happen again. The good news is that the official race ended nicely and has significantly lifted the brand's image globally, given the scale of this event.

{kind=link}

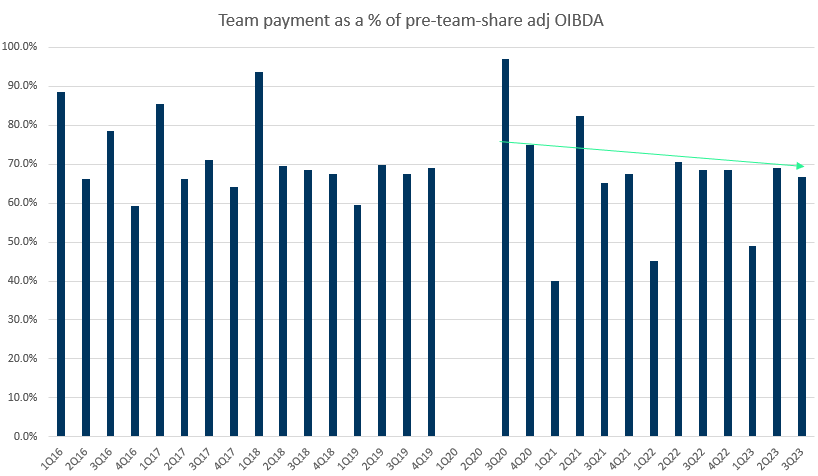

Importantly, FWONK continues to show signs of operating leverage, which is a key part of my OIBDA growth assumption. The major expense - team payments - as a percentage of pre-team-share [PTS] adjusted OIBDA continues to decline, now reaching 66.8% in 3Q23 vs. 68.5% in 3Q22. On a year-to-date basis, PTS team payment as a percentage of revenue has decreased to 64.6% (around 70bps lower than last year). This payout percentage is expected to decline in 4Q23, according to management, as a result of a higher mix of profitable flyaway races. Remember that there are several non-recurring expenses due to the launch of LVGP. If we were to remove those expenses, FWONK is going to see higher operating leverage for the year. Under the assumption that F1 PTS adjusted OIBDA increases its role as the LVGP's profitability grows, I think this data point is encouraging for additional operational leverage in 2024 and even beyond.

{kind=link}

Risk & conclusion

My buy rating is largely dependent on FWONK expanding its adjusted OIBDA margins as discussed above. A reduction in the number of races or sponsors could cause revenue growth to be slower than anticipated. Additionally, teams may receive a larger portion of EBITDA as a result of negotiations.

I reiterate my buy rating for FWONK as I remain positive about the company's ability to grow adjusted OIBDA at robust rates. FWONK's operational leverage, evidenced by declining team payments as a percentage of revenue remains a key factor in my optimistic adjusted OIBDA growth assumption. The current valuation is likely depressed due to elevated costs associated with the Vegas Grand Prix. However, I anticipate a re-rating as FWONK showcases margin expansion potential.

For further details see:

Formula One Group: Adjusted OIBDA Should Grow At A Robust Rate