FWONK - Formula One Group: Racing Ahead

2023-11-10 12:33:16 ET

Summary

- Formula One Group is rated as a Buy due to its strong race economics, growth prospects, and increasing popularity.

- The Las Vegas Grand Prix is expected to boost Formula One's media rights and increase viewership, especially among American fans.

- Apple TV's potential bid for Formula One's broadcasting rights could further demonstrate its growing popularity and generate significant profits.

Investment Thesis

We rate Formula One Group ( FWONA ) ( FWONK ) ( FWONB ) a Buy driven by its strong race economics, growth prospects, and robust and increasing popularity and fan base. We believe the company will likely benefit from the Las Vegas Grand Prix in garnering better media rights driven by increased viewership, particularly amongst the American fans. Recent media reports suggesting Apple TV bidding for its broadcasting rights could further prove a testament to its increasing popularity amongst its fans.

Company Background

Formula One Group is a tracking stock within the Liberty media complex comprising of the Formula One operating business which holds the exclusive commercial rights to the FIA Formula One World Championship. The FIA Formula One World Championship is an annual motor racing competition that takes place across various circuits globally. It generates revenue primarily from the commercialization of TV and digital broadcasting rights, premium subscription through its F1 TV, sponsorships, freight, and logistical services provided to F1 teams, as well as through its Formula 1 Paddock Club hospitality program.

Historical Financials

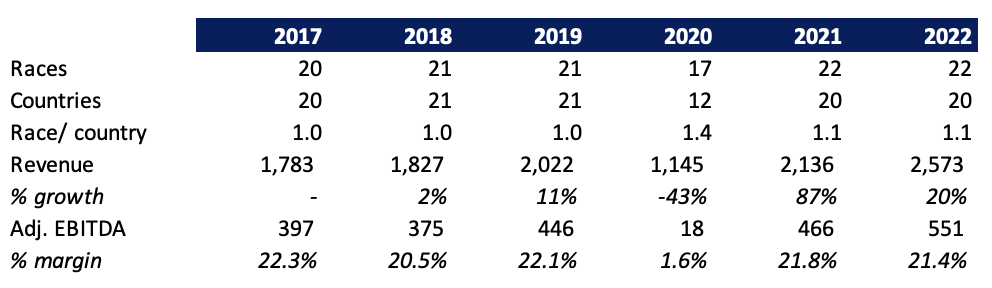

Formula One became massively popular through Netflix's ( NFLX ) Drive to Survive show which first aired in 2019. However, COVID dealt a severe blow which led to a delayed start and a significant reduction in the number of races as a result of widespread restrictions across countries to curb the spread of COVID-19. However, the popularity continues to surge which leads to a strong growth in a post-pandemic era with the F1 racing expanding to 22 races in 2021 and 2022. Revenues grew at a CAGR of 8% during the historical period as well as comparing it with the pre-COVID period (2019-2022) which reflects a complete recovery from COVID-19. The growth was also boosted by rising popularity of Max Verstappen and Redbull Racing who grabbed his first world championship in 2021 from the seven-time world champion Lewis Hamilton. It further added cost caps in 2021 of $140 mn , which was further reduced to $135 mn in 2023 until 2025 which provided a greater racing spectacle and a chance for the weaker teams to compete. Adj. EBITDA margin remained at 20%+, slightly down from pre-COVID levels as a result of higher marketing expenses.

{kind=link}

Stable Q3 Results

FWONA reported stable Q3 results on November 3rd with revenues growing 24% YoY to $887 mn, a tad below the consensus expectation. F1 revenue grew by 27% YoY across race promotion, media rights, and sponsorship driven by one more race in the current period as well as robust fan engagement. Other F1 revenue grew by 7% YoY at $97 mn which was primarily driven by two additional races held outside Europe along with higher hospitality revenue partially offset by lower licensing income. Adj. EBITDA including corporate overheads grew by 25% YoY with EBITDA margins improving by 10 bps driven by SG&A deleverage and higher cost of revenues due to wage pressures and general inflationary outlook. The company reported an Adj. Net Income attributable to FWONA shareholders of $118 mn compared to $108 mn in the year-ago period primarily as a result of higher interest expenses which grew by 37% YoY due to the significant increase in interest rates by the US Fed since last year.

All Eyes on Las Vegas Grand Prix

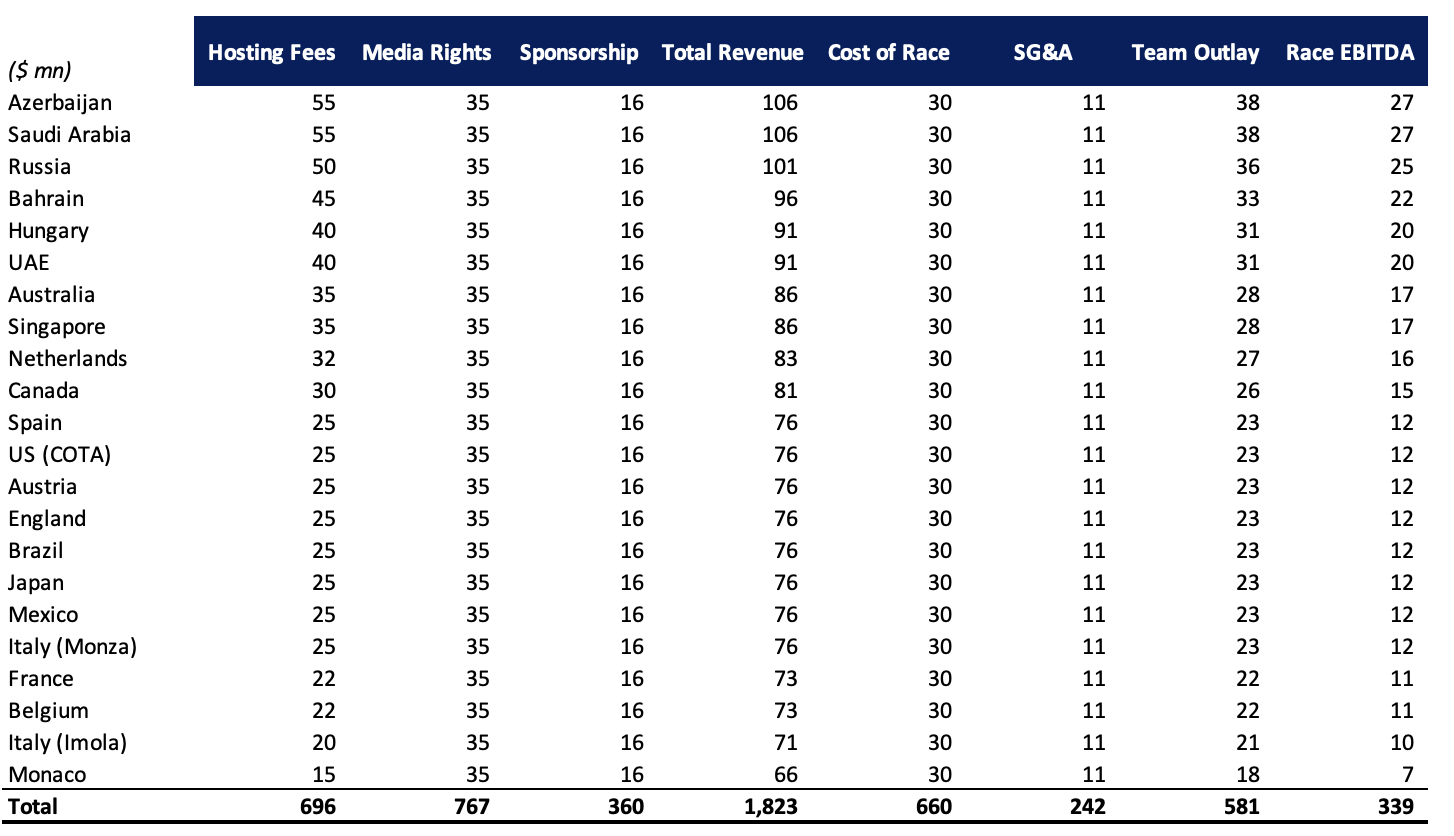

FWONA's management in its Q2 earnings mentioned that capex for Vegas has been somewhere around $400 mn. Las Vegas Grand Prix is the only grand prix that the F1 itself is promoting. According to our unit economics per race based on 2022 estimates, the most profitable F1 circuits generate a Race EBITDA of $20-$30 mn (or about 20-25% margins). We believe the Las Vegas Grand Prix is likely going to be the biggest of the circuits with eye-popping packages that the Grand Prix is commanding. FWONA expects to generate about $500 mn in revenue during the weekend which is significant from F1 comparison, but still pales in comparison to Super Bowl which generates about $500 mn in ad revenue only in one night alone. We believe the race EBITDA margin for Las Vegas strip is likely to be lower due to race promotions and higher costs as F1 itself is promoting. Basis our estimates, we believe F1 will likely be able to recoup its investment within ~6 years. Las Vegas Grand Prix will mark its re-entry into F1 calendar since 1980s and also makes it the third grand prix within the US generating significant interest amongst the American fans. The recent Austin and Miami Grand Prix had a strong following with packed stands and celebrities such as Adam Driver, Drew Barrymore, and Elon Musk. In addition, most importantly, it will help drive strong viewership in the US which can help F1 garner better media rights which is soon expiring. It also garnered Heineken as the title sponsor for its Las Vegas Grand Prix.

{kind=link}

Apple Deal

Investors were concerned and bearish on the US sports post the lukewarm media rights deal in WWE Smackdown worth just about $1.4 bn for 5 years to NBC Universal vs $1.0 bn spent in 2019 to Fox. This eventually saw the stock plummet by about 10% citing tepid media spends and bearish outlook on the US Sports. We believe the comparison is unwarranted as WWE has consistently seen a plateauing or decline in viewership since peaking a decade earlier, while F1 is just starting to expand its viewership in the US. Media rights for UFC and WWE contribute about 70% of the TKO's 9 Month revenues while it is only expected to contribute a significantly smaller amount to F1's overall revenues. In addition, there were press reports suggesting that Apple TV is looking to make a $2 bn offer for the broadcasting rights that could allow Apple TV to broadcast Formula One on its streaming platform, twice the current amount that F1 is generating. Assuming at least 70-80% of the incremental revenue generated flows through EBITDA, it would generate an incremental EBITDA of $700-$800 mn. Considering half of the incremental EBITDA is provided to the teams, FWONA can generate an incremental profits of about $350-$400 mn by 2028 which could provide an upside of $7-$10 per share.

Valuation

The company trades at EV/2023E EBITDA of 25x which is significantly below its long-term average of 34x. We believe the current valuation does not accurately capture the future growth prospects including the potential new media rights deal as well as incremental upside to the Vegas Grand Prix. We believe 2024E revenues are expected to grow by 20% ahead of the consensus to $3.9 bn as a result of 2 new additional races (which were cancelled in 2023) along with continued incremental revenues from the Las Vegas Grand Prix. We expect EBITDA margins to be stable at 22% in line with historicals and expect 2024 EBITDA to be ~$870 mn. This implies an EV/2024E EBITDA of ~18x which is significantly below its long-term average. FWONA does not have a direct comparable with WWE being an indirect comparable as a league operator although its core audience is substantially different. TKO Group Holdings ( TKO ) trades at just ~9x EV/2024E EBITDA which makes FWONA trade at a significant premium. However, we believe given its growth characteristics and at the beginning of its expansion compared to WWE's saturation phase, this growth is warranted. We ascribe a target multiple of ~25x EV/2024E EBITDA, at a discount to its historical averages to reflect the current overhang and depressed multiples as a result of market activity. Initiate at Buy with a target price of $75.

Risks to Rating

1) In case the popularity of F1 wanes, it can significantly impact the broadcasting and sponsorship rights

2) Las Vegas Grand Prix is touted to be the largest event for F1 in several years and lower-than-anticipated buzz could significantly hurt the growth prospects

3) Its inability to monetize media rights at favorable terms poses downside risks

Conclusion

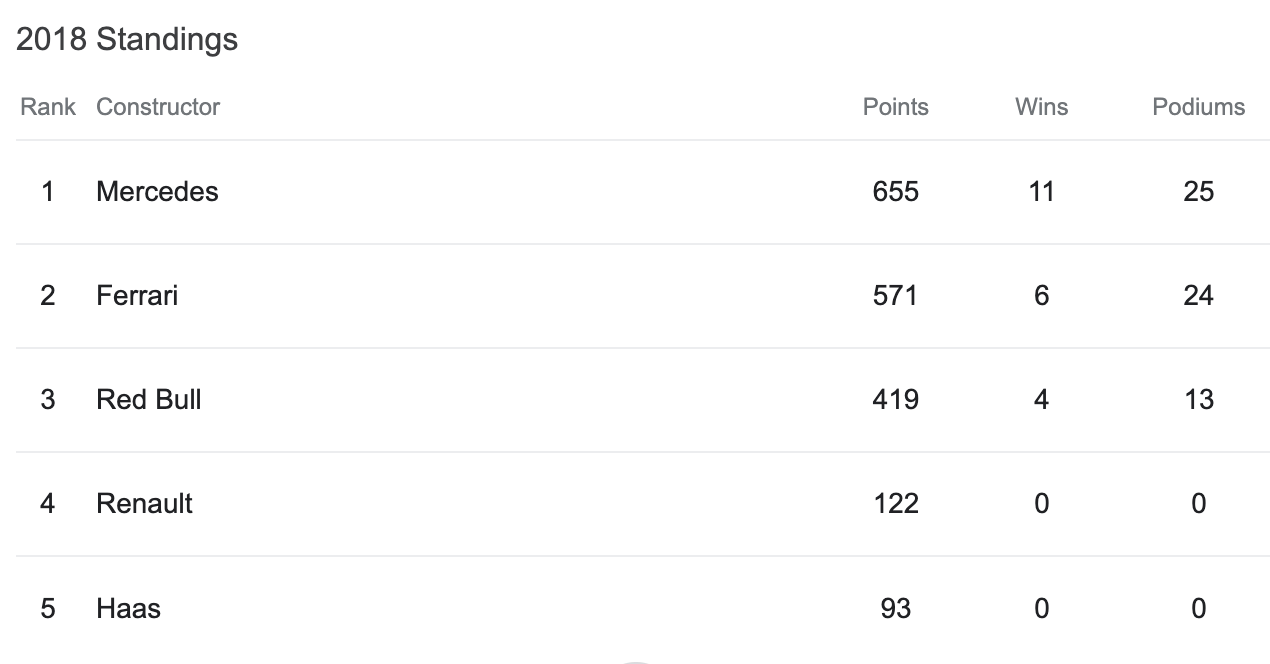

We believe Formula One Group has been benefited by the robust popularity it garnered since the Netflix series 'Drive to Survive' aired which coincided with Max Verstappen snatching its first world championship title from Lewis Hamilton in a dramatic finish at the end of 2021. The group has taken several steps including cost caps to make a level playing field and has been mildly successful with several of the top teams competing for price. For example, if we compare 2018, the top 3 teams were primarily the ones which scored the most points, most wins, and most podiums.

{kind=link}

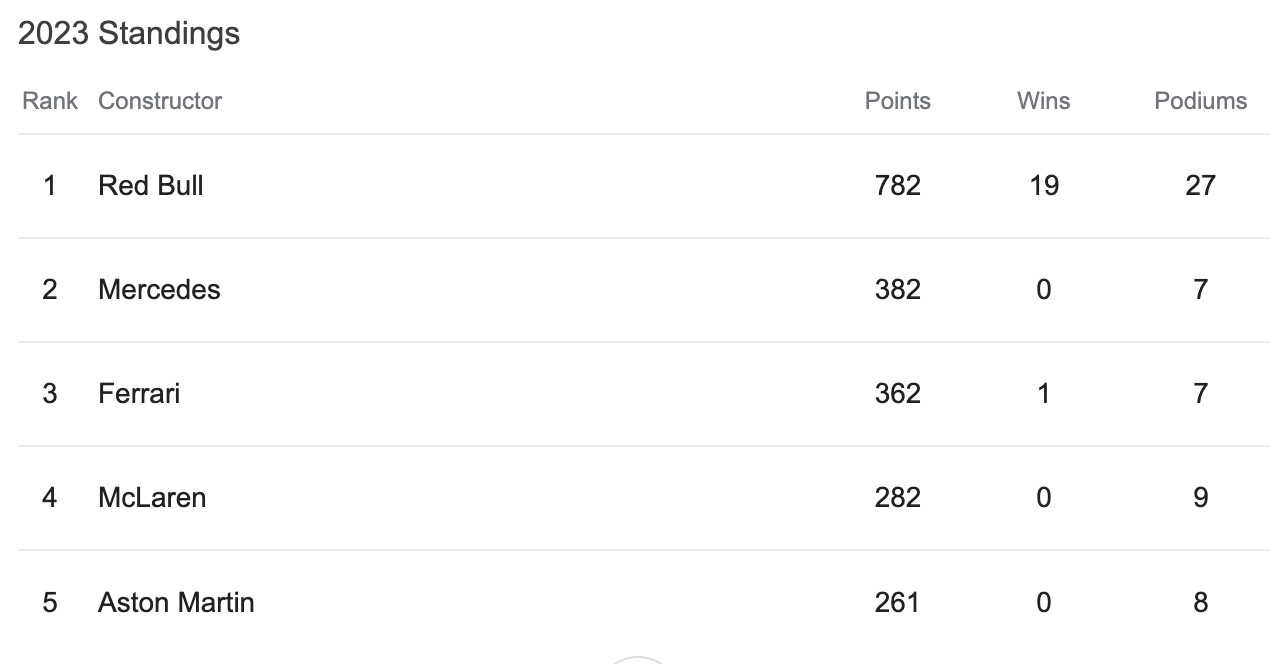

However, the 2023 standings reflect that while Red Bull and Max Verstappen were the ones with most wins, there were closely fought matches with the other teams with Top 4 teams in close finish and each having about 7-9 podiums.

{kind=link}

We believe the popularity of Formula One is just about to grow further and expect a better media rights deal which could further propel its growth. Initiate with a Buy.

For further details see:

Formula One Group: Racing Ahead