FSUMF - Fortescue Metals: An Unfavorably Skewed Risk/Reward

Summary

- Fortescue finishes off FY22 with a strong Q4 operational performance.

- The near-term guidance isn't as rosy, however, particularly on the cost and capex run-rate.

- With FFI spending needs also weighing on the future capital return, the risk/reward seems unfavorable.

Australia's third largest iron ore producer, Fortescue Metals (FSUMF) (FSUGY), posted a strong operational result to cap off its FY22 results , with record shipment numbers coming in well ahead of its prior guidance. That said, the increased cost and capital expenditure run-rate are key concerns - capital spending, for instance, is expected to hit $2.7-3.1bn even before accounting for the green division, Fortescue Future Industries ((FFI)). While the balance sheet deleveraging is progressing well, Fortescue is likely at a crossroads in its capital allocation roadmap - either fund the ambitious FFI strategy at the expense of the capital return or retain the dividend payout ratio (the annualized yield is currently in the double digits %) at the expense of growth investments. For now, my bias is towards the latter, and my base case is for the payout to fall to ~50% from FY24 (vs. the current 80%) to accommodate the growth initiatives in the pipeline. In the meantime, there are additional risks to be mindful of, including management turnover and uncertainties related to the FFI projects.

Capping Off the Year with a Strong Operational Performance

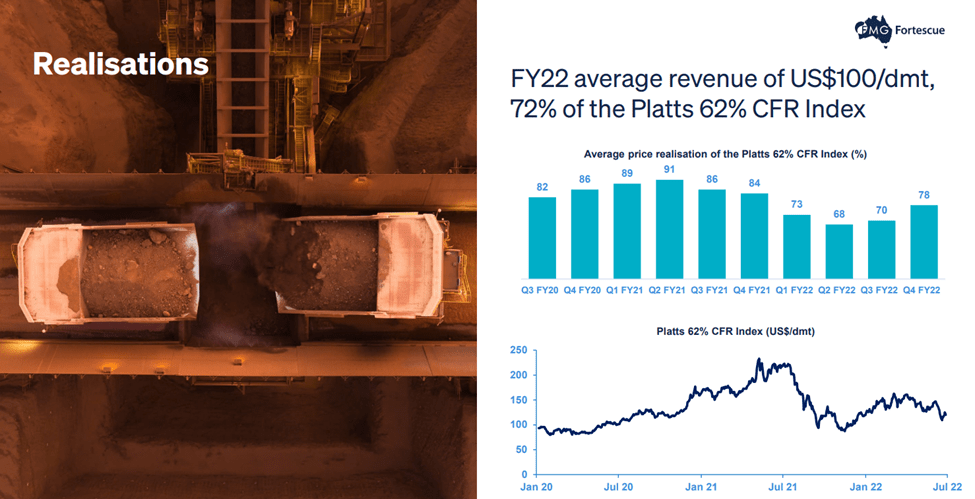

With shipments coming in strongly at 49.5Mt for Q4 2022 and 189Mt for the full year, Fortescue has exceeded its full-year guidance (185-188Mt). The product mix was broadly in-line, but price realization was the key highlight - at an average revenue of $108 per dry metric tonne (dmt) on 78% realization of Platts for Q4, this was a positive trend reversion towards historical levels of ~80% despite a one-month lagged product quality discount posing a temporary headwind. That said, production of higher grade West Pilbara Fines ((WPF)) product was the key drag within the production metrics, declining YoY to ~15Mt due to the ongoing Heritage/Traditional Owner issues at the Eliwana mine (well below the initial ~40Mtpa target outlined in the high-grade strategy from five years ago).

{kind=link}

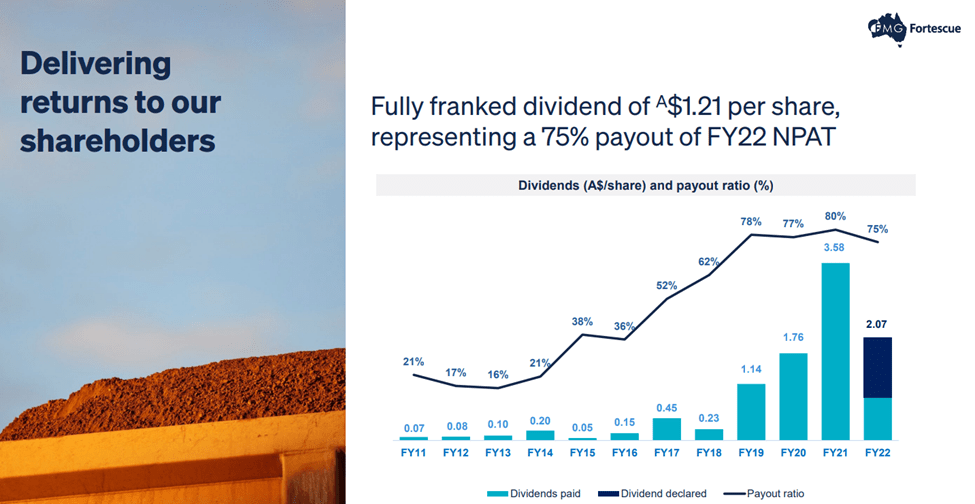

Headline unit costs of $17.19 per wet metric tonne (wmt) were also largely within expectations, but given it benefited from a lower strip ratio at 1.1x (likely to revert back to the 1.5x level in FY23), underlying cost trends were underwhelming, in my view. Plus, this was yet another quarter that the company's shipment volumes were greater than processed ore, implying favorable inventory movements that should reverse over time. Fortescue deserves a lot of credit, though, for its balance sheet deleveraging efforts - net debt is down to $0.9bn as of quarter-end, a significant reduction from the ~$2.4bn of net debt in the March quarter. With the overall FY22 cash generation also solid, there is ample room for the proposed 75% dividend payout (as a % of net profit after tax), which sees the full-year dividend up to A$2.07/share (an impressive ~11% yield at the current stock price).

{kind=link}

Increased Cost and Capex Run-Rate Cloud FY23 Guidance

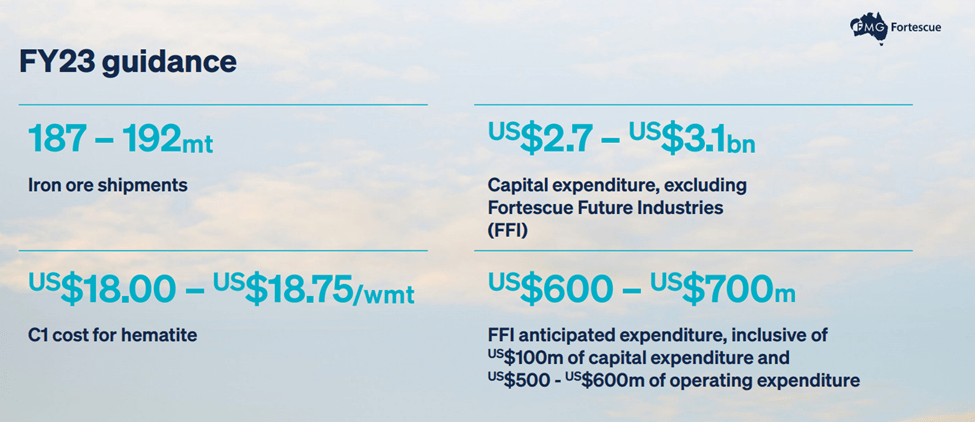

Near-term production is guided to a solid 187-192Mt (including ~1mt from Iron Bridge), though this could increase if negotiations for a hematite shipment allowance increase from Port Hedland be successful. The key negative was costs - while costs only slightly missed guidance this quarter, next year's guidance represents a significant increase in the expense run-rate at $18-18.75/t on higher cost inflation across fuel, labor, and ammonium nitrate, as well as mine development. In addition, the FY23 capex guidance stands at $2.7-3.1bn, comprising sustaining capex of ~ $1.5bn, hub development of ~$300m, decarbonization at ~ $100-200m, Iron Bridge and Pilbara Energy Connect at $700-800m, as well as exploration at ~$200m. Of note, the headline capex range excludes the $0.6-0.7bn allocation to FFI, so there could be incremental capex pressure in the coming quarters.

{kind=link}

The implied capex delay for the Iron Bridge Magnetite project is far from a good sign - the guidance for the first production remains for the "March 2023 quarter", but up to ~ $500m (out of the $3.6- $3.8b capex allocation) has been pushed back into FY23. Assuming the 18-24 months to full production target holds, this likely implies a lower ~7-11mt contribution in FY24 as well. In the meantime, there has been no decision yet as to whether magnetite concentrate will be sold as a stand-alone product (vs. blended with hematite product). Fortescue is currently in advanced negotiations with the Hedland port regulator to provide flexibility around the proposed 22mtpa concentrate/188mtpa hematite split from the increased port allocation, though, so updates here will be worth keeping an eye on. Still, with the updated spending guidance set to be higher than expected in the years ahead, exacerbated by increased FFI spending, I have concerns about Fortescue's resilience to an iron ore downturn going forward.

Unsustainable FFI Expenditure Could Strain the Balance Sheet

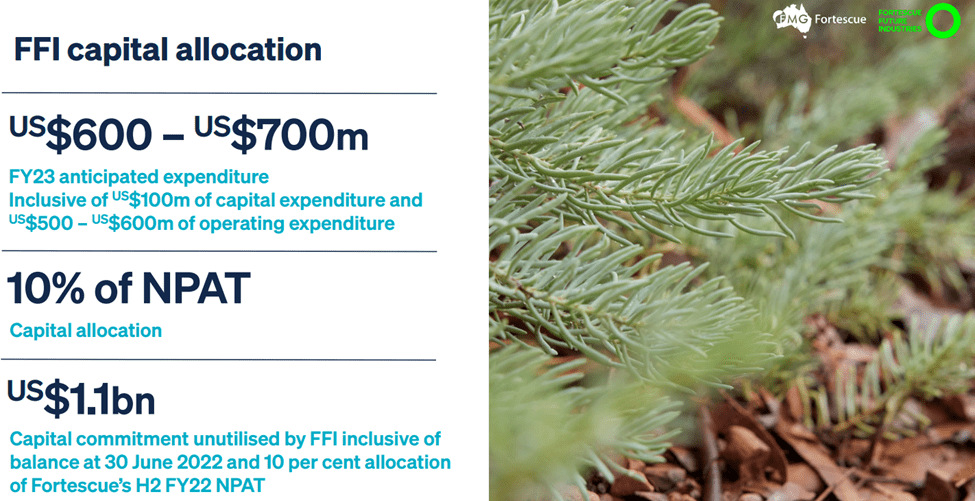

Looking beyond FY23, expect increased scrutiny from investors on the Fortescue capital allocation and FFI investment plans. To date, FFI has underspent relative to its ~10% allocation from group earnings, implying ~$728m unutilized at the end of FY22. As a result, FFI will likely need to maintain an aggressive schedule, pointing toward its spending likely running at >10% of earnings going forward. In the meantime, FFI is moving forward with initiatives that will take some time to pay off, including the self-charging "infinity train" and battery electric haul trucks. Plus, the hydrogen part of the business, which has driven much of Fortescue's premium valuation thus far, has offered little to be optimistic about. In sum, the outsized spending needs at FFI leave Fortescue exposed to any cyclical weakness in iron ore prices, likely constraining the capital allocation budget beyond the near term.

{kind=link}

An Unfavorably Skewed Risk/Reward

Fortescue's Q4 2022 operational performance rounded off a strong FY22 result, as outperformance on sales and realized prices more than offset higher cash costs. The solid cash flow should, in turn, support an attractive dividend payout for the year, with the annualized yield now in the double digits %. On the flip side, the FY23 guidance update warrants caution - both cash costs and capex numbers were higher-than-expected and look set to hit profitability next year, even in a stronger production scenario. As a result, the company is likely nearing a capital allocation inflection point as it does not have the balance sheet capacity to accommodate the ambitious new growth strategy and the current dividend payout. Given management's commitment to the growth plan, my base case is for the dividend payout ratio to fall significantly into FY24 or so - a likely de-rating catalyst down the line. Additional downside risks include future inflationary cost pressures, FFI-driven uncertainties, as well as management churn risks following CEO Elizabeth Gaines' decision to step down.

For further details see:

Fortescue Metals: An Unfavorably Skewed Risk/Reward