FSUMF - Fortescue Metals Group: A Good Call Option On The Iron Ore Price

2023-09-07 10:30:00 ET

Summary

- Fortescue Metals has seen a ten-fold increase in share price since 2014, with dividend income exceeding the initial investment.

- The company's financial results for FY 2023 were strong, but iron ore prices have since decreased.

- The Iron Bridge project, producing a higher grade concentrate, is expected to compensate for the impact of lower iron ore prices.

Introduction

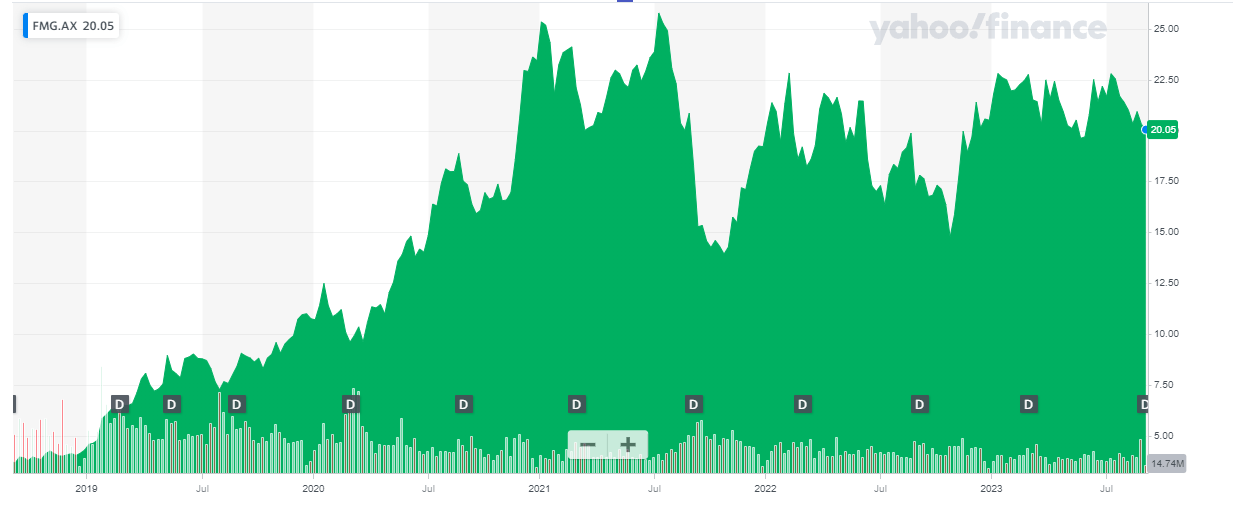

This article is not meant as a victory lap. It would have made sense as I have been bullish on Fortescue Metals (FSUMF) (FSUGY) for several years during 2014 and 2016 and since my last article on Fortescue was published, the share price has ten-folded before coming down to its current levels (US$13.63 on its US OTC listing). And since that article was published in March 2016, the company has paid a total of US$7.95 in dividends, or in other words, the total dividend income already represents in excess of 400% of the initial purchase price. Needless to say, the financial risk of owning Fortescue is zero at this point. Less than zero, as the total amount of dividends received exceeds the initial investment.

This does not mean I still own all my shares. As the iron ore frenzy heated up in the initial post-COVID phase, I liquidated almost all my iron ore holdings. I retained a token amount of Fortescue shares, a placeholder to keep an eye on the share price. And as the iron ore price recently came down again and the futures market pointing in the direction of a US$95-105/t price of the 62% Fe benchmark concentrate, I wanted to re-assess the situation to see if I should start building my position again.

{kind=link}

Fortescue's primary listing is in Australia where it is listed with FMG as its ticker symbol. The average daily trading volume is approximately 6.5 million shares, for a total monetary value of around A$130M. The current market cap of the company is A$61.7B. Fortescue reports its financial results in US Dollar so I will use the USD as base currency throughout this article.

FY 2023 was strong, but iron ore prices are substantially lower now

Although Fortescue has been trying to establish itself as a 'green' company focusing on the energy transition that's taking place in most western countries, it still is and should be seen as an iron ore company. It shipped 192 million tonnes of iron ore, resulting in an EBITDA of US$10B and a net income of $5.5B. The reported net income was a bit lower at $4.8B after Fortescue had to record an impairment charge on its high-grade Iron Bridge project.

The total revenue reported during FY 2023 was $16.9B , resulting in a gross profit of $9.05B. That's a good result, especially when you see a substantial chunk of the COGS is related to the shipping and transportation expenses.

{kind=link}

Fortunately, those shipping expenses are decreasing which helped the company to keep the total operating expenses under control despite an increase of more than 10% in the mining and processing costs.

The total operating income was $7B and this resulted in a net income of $4.8B for an EPS of $1.56. This represents in excess of A$2.25 per share using the current exchange rate.

{kind=link}

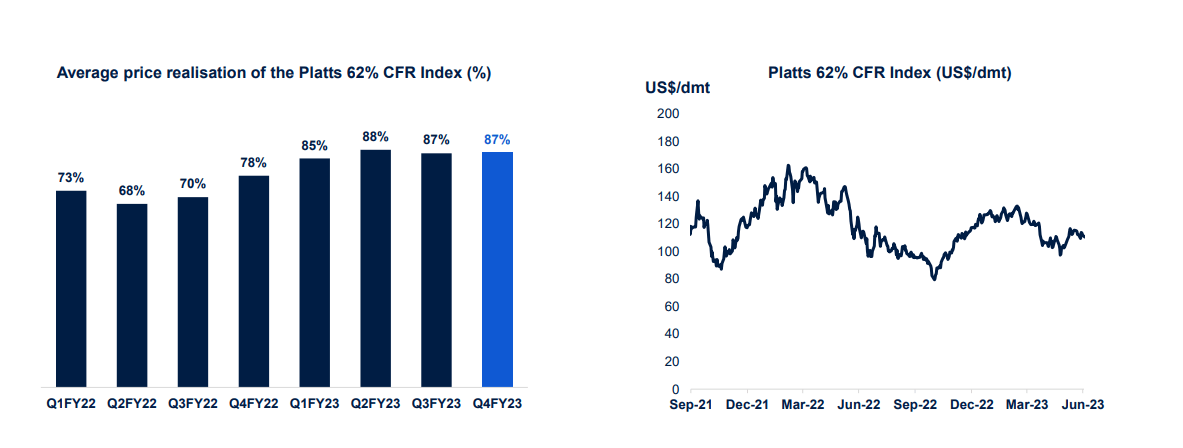

And throughout the year, Fortescue was able to secure a price equal to about 87% of the benchmark price for its iron ore.

{kind=link}

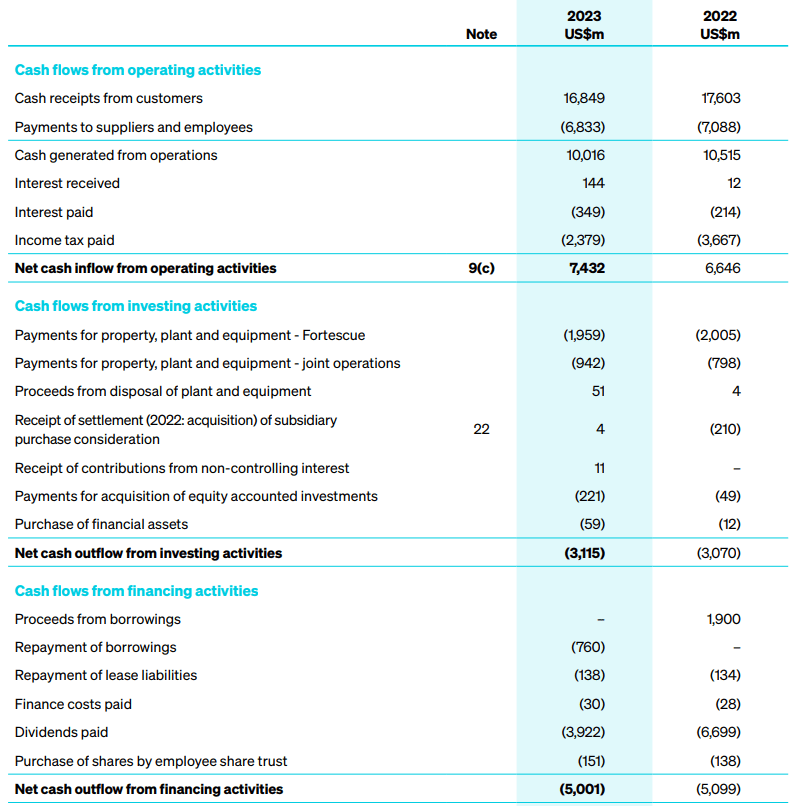

Fortescue reported a total operating cash flow of $7.43B and after deducting the $168M in lease and finance expenses, the net operating cash flow was $7.25B.

{kind=link}

As you can see in the image above, the total capex was about $2.9B. This means the underlying free cash flow result was approximately $4.35B. That being said, it's important to understand a substantial portion of the total capex was related to growth investments (in Gabon and on the Iron Bridge project). The total sustaining capex was just $1.25B and the image below shows the total sustaining capex and hub development investments were just $1.45B.

{kind=link}

The total hub development capex will increase this year but will still be comfortably covered by the anticipated cash inflow from operations. While the iron ore price is weaker, shipping expenses will likely mitigate the impact a little bit as the bulk shipping expenses have also been on a downward trajectory. But more than anything else, I expect the Iron Bridge project to fully compensate for the impact of lower iron ore prices.

One of my issues with Fortescue was that it was originally shipping iron ore concentrate with an average grade below the 62% Fe benchmark grade, and that obviously meant it received an average price for its product that was substantially lower than the benchmark price. Fortunately, Fortescue is addressing this and has recently commissioned the Iron Bridge magnetite project where it produces a concentrate with an average grade of 67% Fe. This should result in a normalized premium of around US$25-35/t (or even more) over the 62% Fe benchmark, and could easily fetch a price that's 50-75% higher than the 58% concentrate it has been shipping so far.

I think the Iron Bridge project is ready just in time to deal with the lower iron ore prices. With a capacity of 22 million tonnes per year and a C1 cash cost of US$45/wmt, this mine should generate operating margins of in excess of A$2B per year based on a price of US$100/t for the benchmark concentrate.

Investment thesis

While Fortescue tries to establish itself as a 'green' company focusing on the energy transition , we should still predominantly look at the company from its iron ore perspective. During FY 2024, Fortescue expects to ship 192-197 million tonnes of iron ore at a C1 cash cost of US$18-19 per wet metric tonne. The iron ore price is currently pretty low but I expect the Iron Bridge project and its 67% Fe concentrate to compensate for the low realized prices on the lower grade concentrate.

I currently have a small position in Fortescue, but I'm in no rush to add to this position. Fortescue is not expensive (even if you would assume a 30% EBITDA decrease compared to last year) but the iron ore price remains flattish. But if you're looking for a call option on the iron ore price, Fortescue Metals Group fits the bill.

For further details see:

Fortescue Metals Group: A Good Call Option On The Iron Ore Price