FSUMF - Fortescue Metals Group: Turnaround Will Weigh On Returns

2023-05-12 17:06:37 ET

Summary

- Fortescue Metals Group Limited's iron ore production costs have been rising, and with Australian inflation still high, costs may rise further.

- Simultaneously, iron ore prices have been declining and Chinese demand for ore may gradually diminish over the longer term, putting further pressure on prices.

- Against this backdrop, Fortescue has embarked on a mission to decarbonize the business and become the world’s leading, integrated, fully renewable energy and green products company.

- Capital expenditures will, therefore, remain elevated over the coming years, and consequently, shareholder returns will be reduced.

- Management has shown it takes the long-term view, and, only for investors with a long investment horizon, Fortescue presents as a Hold.

Fortescue Metals Group Limited ( FSUMF , FSUGY ) is a major Australian iron ore mining company. Recently, management jumped the green bandwagon and decided to decarbonize its operations. It doesn't stop there, however, as management has shared the intention to become a renewable energy and green products company. These goals will require substantial capital, while the price of iron ore ( SCO:COM ) will most likely trend lower over the coming years.

Cost side

As the end of an highly inflationary environment appears to be nearing, it should come as no surprise that Fortescue's production costs have been rising. Whereas these costs were US$15.91/wmt in FY22, during 1H23 these costs increased to US$17.43/wmt. This means costs rose by nearly 10 percent in half a year.

As a result, the company reiterated the outlook for costs to reach a value of US$18.00 - 18.75/wmt in FY23. In all likelihood, actual costs will be at the high end of this range, as inflation in Australia has not been contained yet. This prompted Australia's central bank to surprise markets on May 2nd with a 25-bps rate hike.

The costs per tonne only give information about one side of the equation; equally important is the price for which the ore can be sold. For this reason, it's worthwhile to assess the metric "Underlying EBITDA per tonne," which Fortescue uses to manage the business.

Ending FY22, the company achieved an underlying EBITDA of US$63/dmt. Again, only half a year later this number was reduced to US$52/dmt. In other words, earnings dropped by 17 percent.

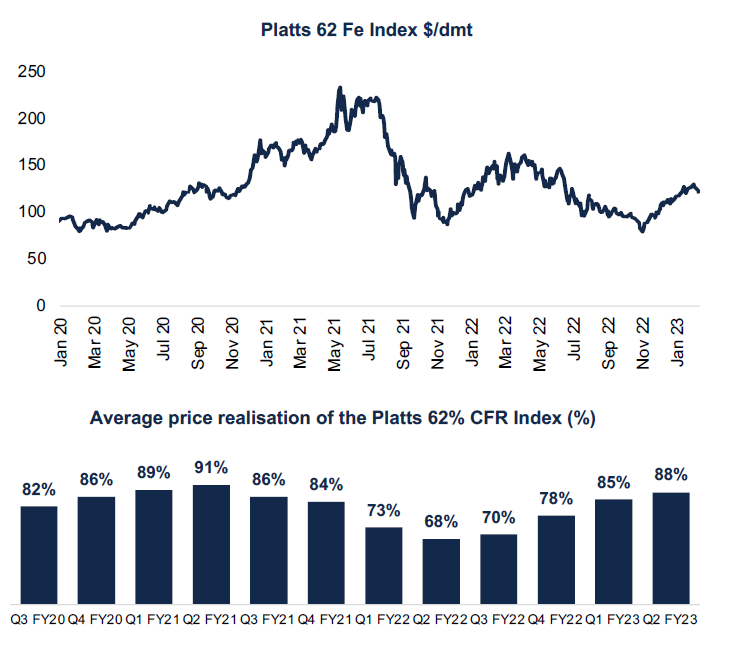

This reduction in Fortescue Metals Group Limited earnings was booked against a better price realization, as can be seen in Figure 1. During FY22, price realization was rather poor, but this was turned around. The downside however is that there is little upside potential left to increase the price realization. This implies rising production costs cannot be mitigated on the demand side, but will drive the underlying EBITDA per tonne further down.

Figure 1 - Price realisation, FY23 half-year results presentation (fmgl.au.com)

{kind=link}

Demand side

The demand side of the equation may experience further pressure as laid out in a recent assessment of iron ore (SCO:COM). With Fortescue being an ore producer with strong ties to China, it matters how Chinese demand will develop.

As laid out in the referenced article, there are several reasons why Chinese demand for ore may gradually diminish over the longer term. These reasons will not be repeated in this article as Fortescue has an action plan for the coming years to diversify and become less dependent on ore. To fund this plan, however, price developments of ore in the short term do matter.

While supply/demand imbalances are arguably the main driver for day-to-day prices, Chinese policymakers have the ability to influence commodity pricing on the short term.

The most direct way to do so has been the launch of the China Resources Mineral Group, an entity enacted to orchestrate the buying of iron ore on a national level. Additionally, there are other options which are more indirect. For example, policymakers are weighing production cuts, for the third year in a row, to meet emission targets.

All in all, the demand for iron is under pressure while simultaneously production costs are increasing as well.

Decarbonization dominating capex

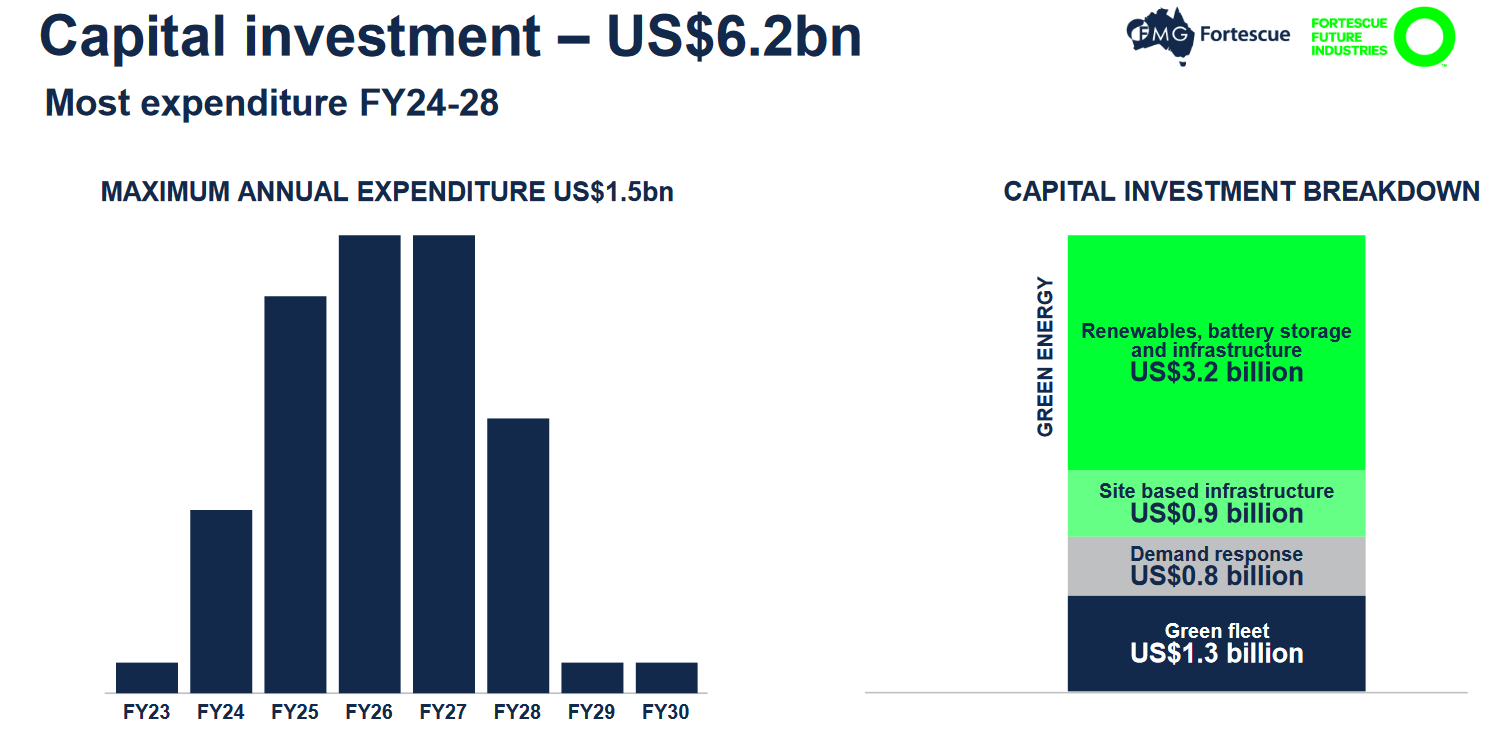

Against this backdrop, Fortescue embarked on a mission to decarbonize the business. Or, more colloquially, the company jumped on the green bandwagon. Figure 2 shows the expected investments required to achieve this goal.

Figure 2 - Capex required for decarbonization (fmgl.au.com)

{kind=link}

The total capex required for decarbonization is estimated to be US$6.2Bn with the program to be finalized in 2028. It's also clear the effect of this investment program is not visible yet in 2023, as the expenditures will start to take off in 2024. This does mean 2023 serves as a good baseline to estimate the total amount of capex to be expected in the coming years.

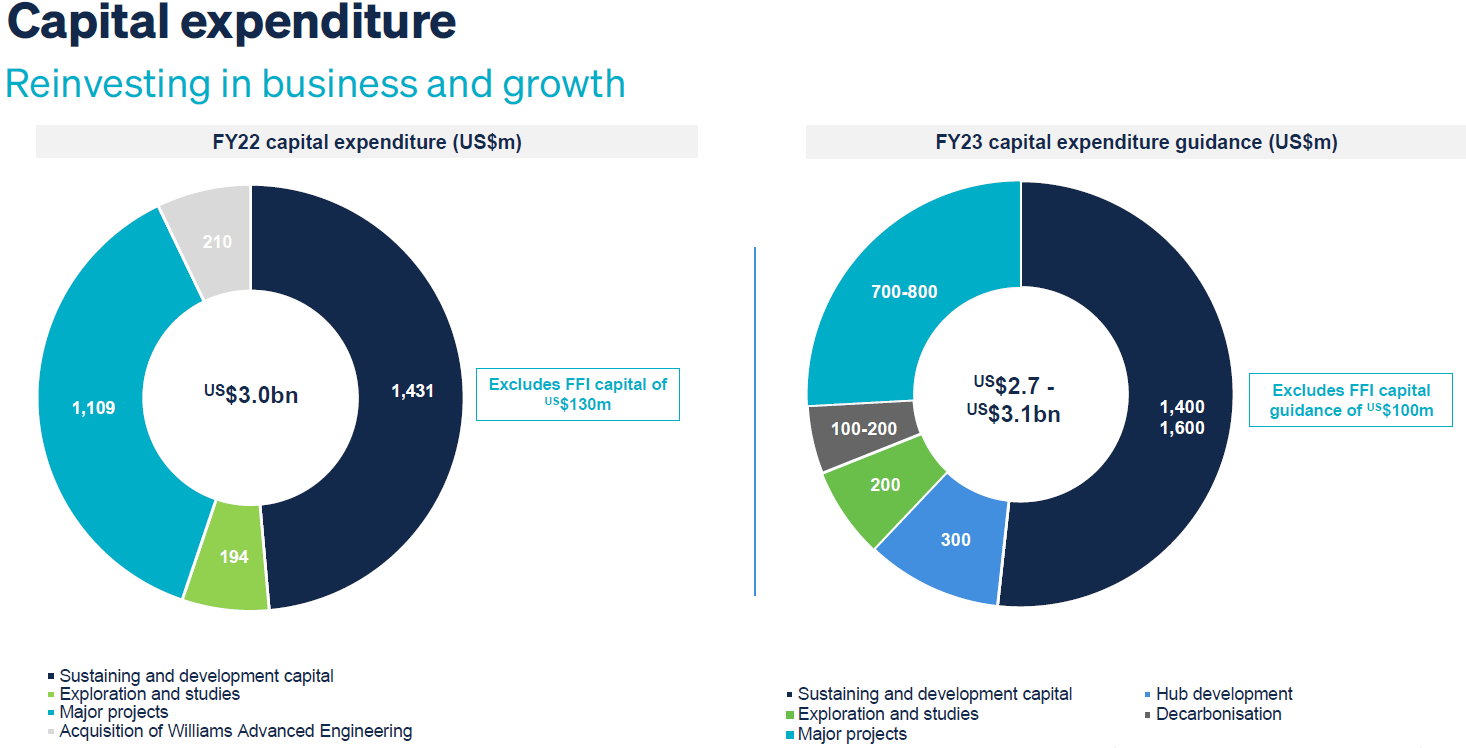

Figure 3 shows the FY22 capex on the left-hand side, and the FY23 guidance on the right-hand side. The guidance starts to show the capex allocated for decarbonization, but also the additional costs for the development of the green hydrogen hub in Queensland.

Ramping up decarbonization investments the question becomes which expenditures can be lowered to keep a lid on the total investments. The figure already shows the allocation for "Major projects" is reduced but "exploration expenses" and "sustaining capital" are about the same.

Figure 3 - FY22 capex and FY23 forecast, from FY22 results presentation (fmgl.au.com)

{kind=link}

Important to note is that the Fortescue Future Industry expenses are omitted from these figures. For FY23 the expectation is an additional US$230 million of capex will be allocated to FFI projects. On top of this, about US$0.5Bn opex is foreseen.

This information, combined with the data in figures 2 and 3 leads to the expectation capex will remain elevated at a level of approximately US$3Bn, but potentially more, for the coming years.

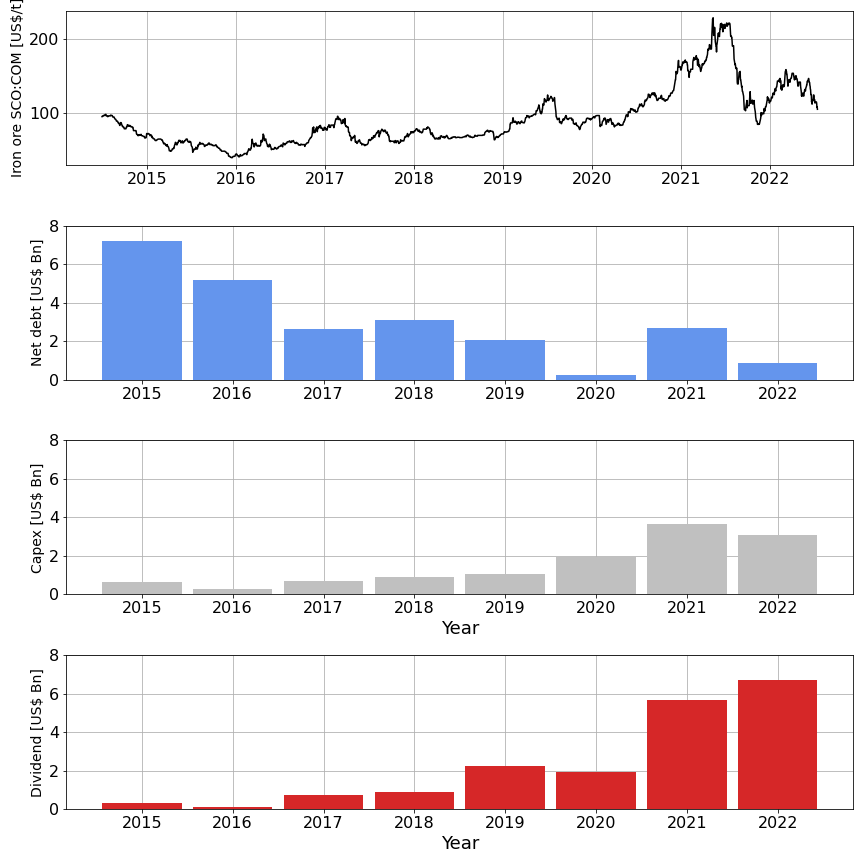

As visualized in Figure 4, Fortescue has generated substantial cash over the last years. But even before the ore price started its ascend in 2020, Fortescue deleveraged substantially in a time when ore prices were consistently trading at a sub-100 US$/t level.

This deleveraging was made possible in part as investments were kept low. For this decade management intends to keep capex elevated, even as the ore price will (potentially) trend lower. The difference with the last decade is that the company virtually has no debt. In spite of this, as earnings will reduce and the US$3Bn capex level is maintained, the lowering of dividend has already begun to preserve the health of the balance sheet .

Figure 4 - Different metrics versus ore price (data fmgl.au.com; chart by author)

{kind=link}

Shareholder returns

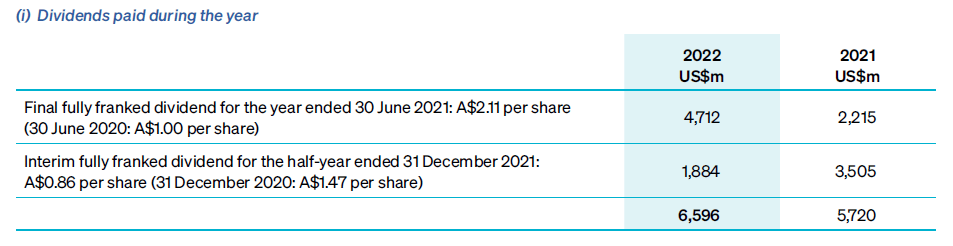

The fiscal year of Fortescue runs from the 1st of July till the 30th of June. The dividends are declared in the fiscal year, but the actual payment lags and is, therefore, recorded in the consecutive fiscal year. What this means, when assessing the dividend, becomes clear if the numbers in Figure 5 are considered.

Figure 5 - Dividend payments per (fiscal) year, AR FY22 (fmgl.au.com)

{kind=link}

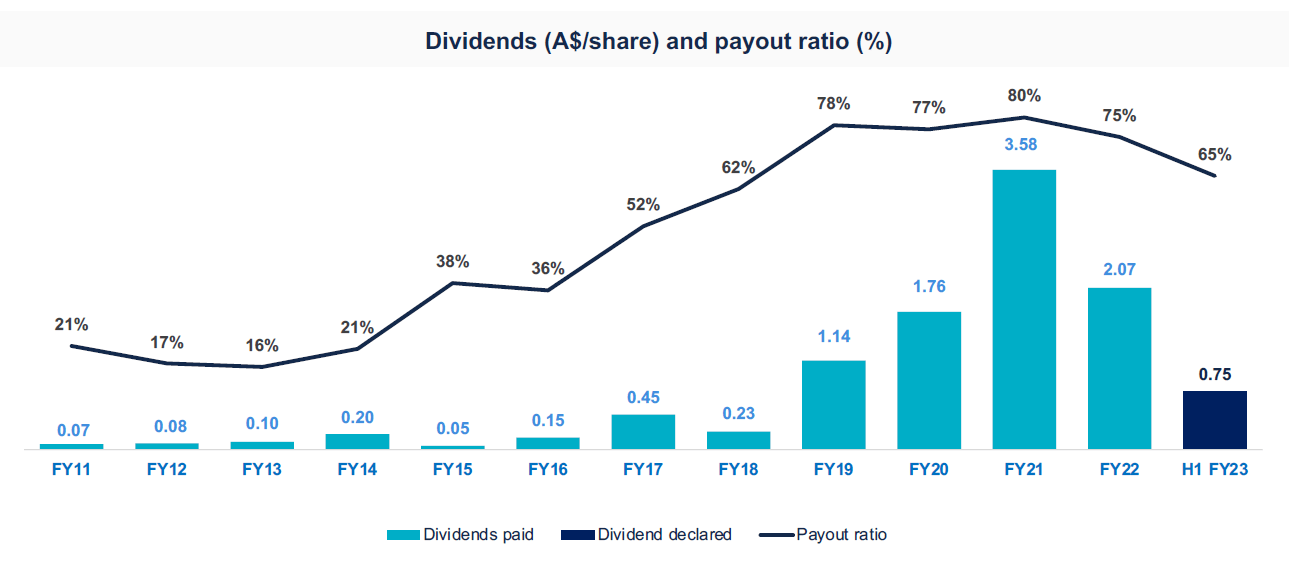

The cash flow statement in the annual report of FY22 shows a larger amount of dividends paid in 2022 than in the year prior. A situation one might not expect given the way the company presents the dividend per share, see Figure 6.

Figure 6 - Dividend per share, FY23 half-year results presentation (fmgl.au.com)

{kind=link}

Correcting the dividend per share information for the fact the fiscal year does not match with an actual calendar year, the total amount of dividend to appear in the FY23 cash flow statement is based on the two installments of A$1.21 and A$0.75.

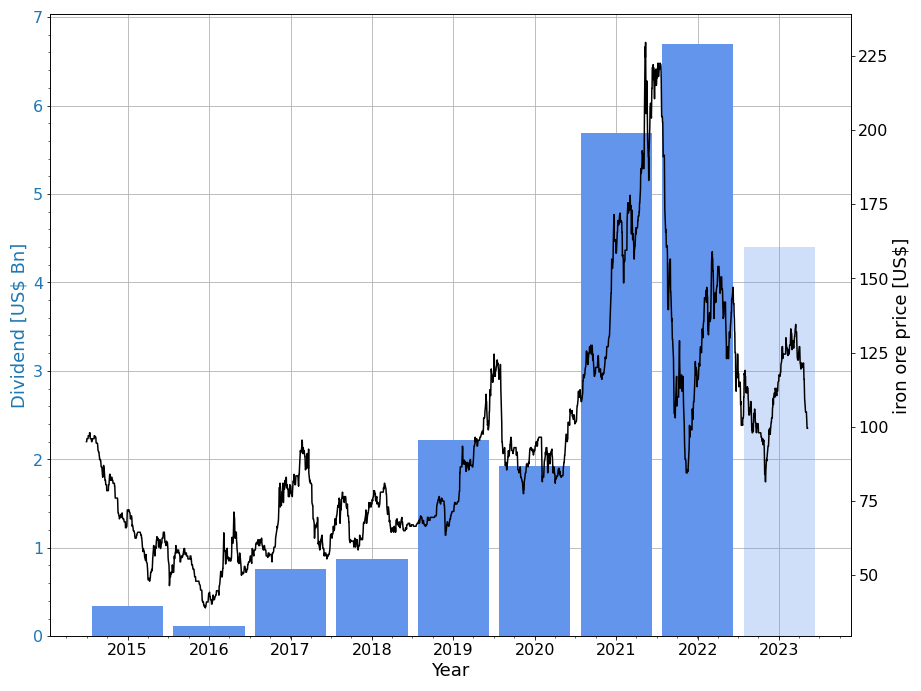

Assuming the amount of shares outstanding and A$/US$ exchange rate will remain constant, the FY23 cash outflow due to dividends will be approximately US$4.4Bn. This expected dividend, as well as the historic dividend, is plotted in Figure 7.

Figure 7 - Dividend versus ore price, 2023 number is an estimate (seekingalpha.com, fmgl.au.com; chart by author)

{kind=link}

The combined cash outflow due to capex and dividend is an estimated US$7.5Bn for FY23. In this respect, it should be noted net debt was reported to be US$2.1Bn at the 1H23 presentation (2022: US$0.9Bn). This implies the company needs to increase debt to fund the dividend.

Therefore, my base case is the dividend will return to the pre-pandemic level of about A$1.50 per share over the next two years. This implies the current estimated FY23 dividend payment of US$4.4Bn will drop further to about US$2Bn. Admittedly this may seem quite conservative, but with an A$/US$ 0.7 exchange rate this translates in a US$1.05 dividend and a yield of approximately 7.5%. This is a decent return, but looking beyond 2024 the question is if this level of dividend payout will be maintained.

Risks

Fortescue has solid, profitable operations in Australia. Yet, management intends to diversify and as such is exploring for minerals in Latin America, Africa, and Kazakhstan. On top of this, through Fortescue Future Industries, the company is developing green energy projects in the USA, Norway, and Germany amongst others.

Actually, management is betting heavily on "going green," to ensure its future license to operate. Instead of just decarbonizing the mining operations, a much more bold goal has been formulated :

FFI's goal is to become the world's leading, integrated, fully renewable energy and green products company

Essentially the iron ore operations will be used as a basis to fund a complete overhaul of the company. While this is a potentially positive prospect, investors should be aware setting up a new business in a capital-intensive industry (e.g., hydrogen fabrication) will weigh on shareholder returns. What's more, Fortescue is foraying into a field it has little knowledge of, in jurisdictions where it has little experience. The slightly comforting part is that the "green" projects are located in countries with stable political climates.

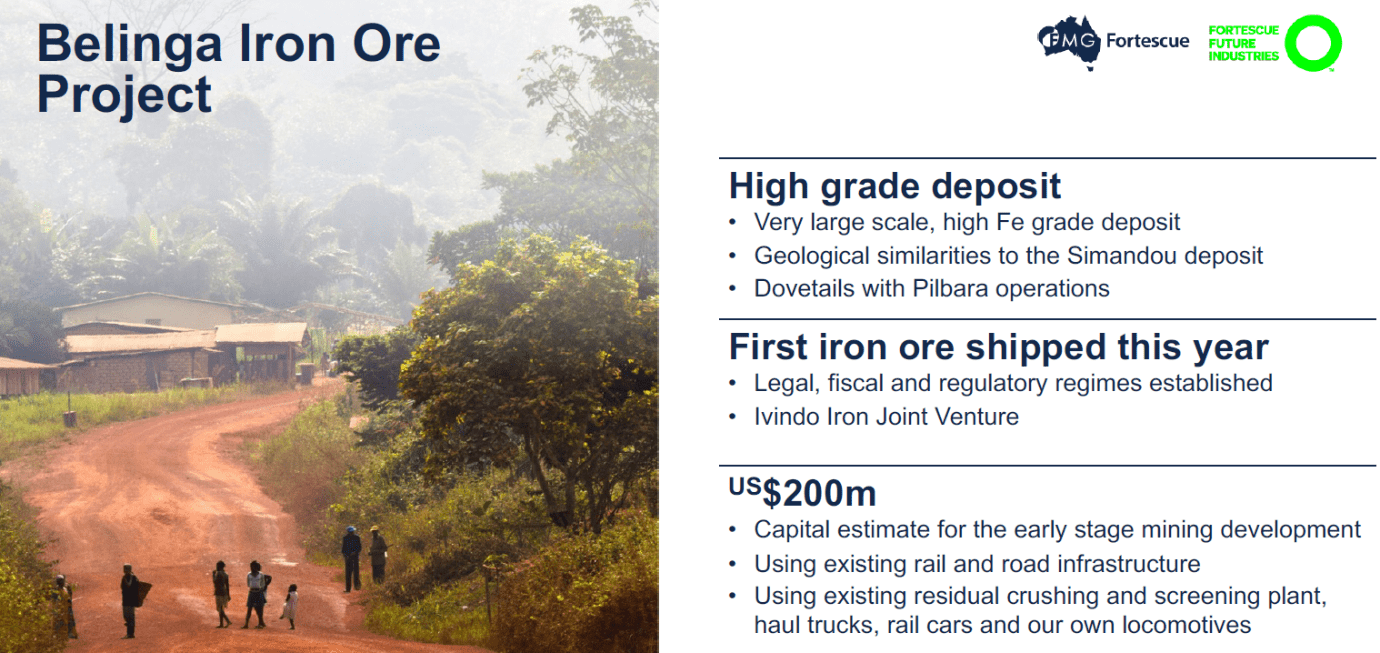

Concerning the core business of iron ore, management appears to have set its sight on the Belinga project in Gabon, see Figure 8. While undoubtedly Fortescue is able to successfully develop a large-scale mine, operations in Africa require a different set of skills.

Figure 8 - Belinga Iron ore project, 1H23 results presentation (fmgl.au.com)

{kind=link}

The referenced Simandou project, for example, located in Guinea, has been suffering delays due to political instability . While one could argue Gabon has a relatively stable political regime, it must be noted a presidential election will be held in the country this year.

Tellingly, the date for the election has not been fixed yet. Whoever will rise to power in the country, the situation that a government in the future will want to renegotiate terms, just as in Guinea, is a near certainty. Obviously, a perfect moment would be when the development has advanced past the initial stages, say several years from now, when sunk costs will be higher.

Next to the political environment, the state of infrastructure poses a matter of concern. Over the course of 2023 and 2024, an amount of US$200 million will be invested in the Belinga development. As Fortescue made this decision well-informed, I expect the initial production results to be promising.

The big issue however is getting the ore out of the country. Yours truly has spent time in Gabon and issues such as port congestion and deepening of access channels pose challenges. Therefore, in addition to the mine development, significant investments will be required in the infrastructure. In terms of money this implies required capex will be (much) more than the recently developed US$3.9Bn Iron Bridge development where a large part of the infrastructure was already in place.

All in all, it seems investments will take off in the second half of this decade, putting pressure on dividend distributions and potentially deteriorating the balance sheet to fund the turnaround of the company.

Conclusion

Production costs have been rising while demand has not developed according to plan and is expected to diminish over the coming years. Against this backdrop, management intends to decarbonize, expand geographically and foray into the business of renewable energy.

Capital expenditures will, therefore, remain elevated, and consequently, Fortescue Metals Group Limited shareholder returns should be reduced. Although the current dividend yield is decent, the envisioned turnaround of Fortescue Metals Group Limited should put pressure on shareholder returns. Management has shown to take the long-term view, and only for investors with a long investment horizon Fortescue Metals Group Limited presents a Hold.

For further details see:

Fortescue Metals Group: Turnaround Will Weigh On Returns