ATGFF - Fortis: A Dividend King In The Making

Summary

- 49 years of consecutive dividend increases are rare and Fortis has accomplished just that.

- The diversified utility has a lot to boast about including great execution and an A-rating from S&P.

- What it cannot boast about today, though, is the valuation.

All values are in CAD unless noted otherwise.

49 years, that's how many consecutive dividend increases Fortis Inc. ( FTS ) (FTS:CA) has had.

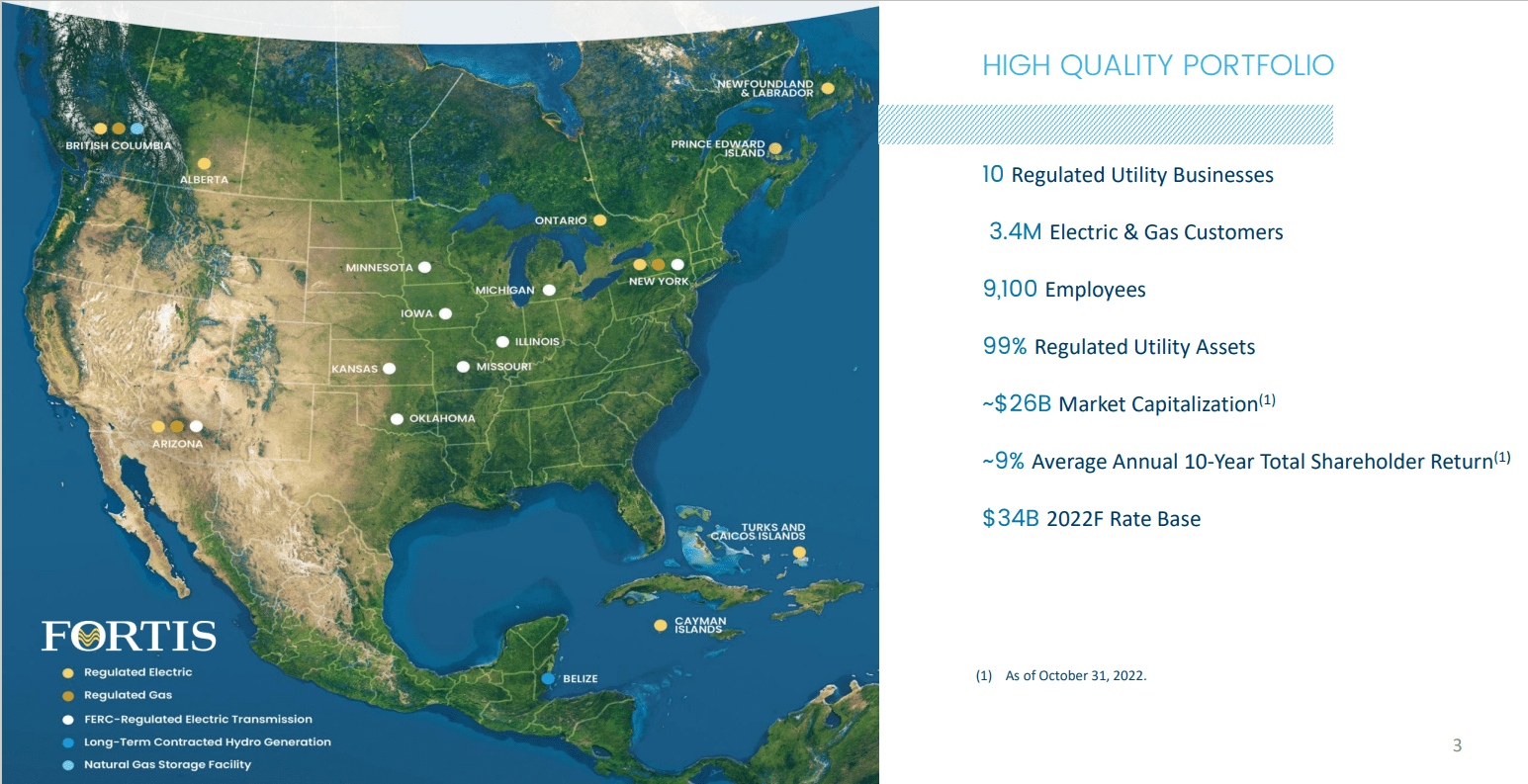

November 2022 Presentation

This includes a few years when this dividend aristocrat operated under the name, Newfoundland Light & Power Co. Limited. Headquartered in Canada, Fortis is a regulated electric and gas utility company with customers across North America and the Caribbean. As at October 31, 2022, the company's footprint looked like this.

{kind=link}

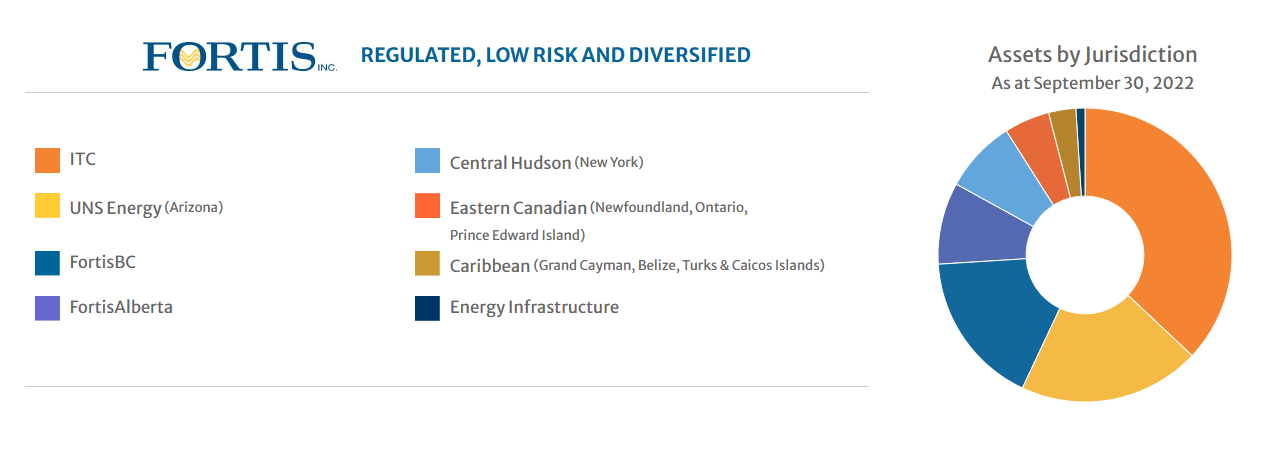

Over 60% of its assets are located in the US, and expectedly the foreign operations also contribute more than 50% of its revenue.

{kind=link}

Overall, most of its assets pertain to energy transmission and distribution. Fortis operates via independent utility businesses covering its various operational locations, with each business unit operating as a substantially autonomous entity.

Emera Incorporated (EMA:CA) (EMRAF) is another Canadian utility we recently covered and found too rich for our value conscious taste. Our current protagonist has gone toe to toe with Emera in terms of total returns over the last decade.

This despite offering a comparatively lower dividend yield. Besides the expensive valuation, we did not like the high payout ratio and high debt load in Emera's case. Let us explore Fortis and see where it stands vis a vis its compatriot in our books.

Q3-2022

Fortis delivered a solid third quarter for 2022 with adjusted earnings per share of 71 cents coming above estimates. The bulk of the beat came from the US side of operations and the weak Canadian dollar certainly helped. For the year, the company should earn about $2.75 a share and this should create a 6% growth rate, year over year.

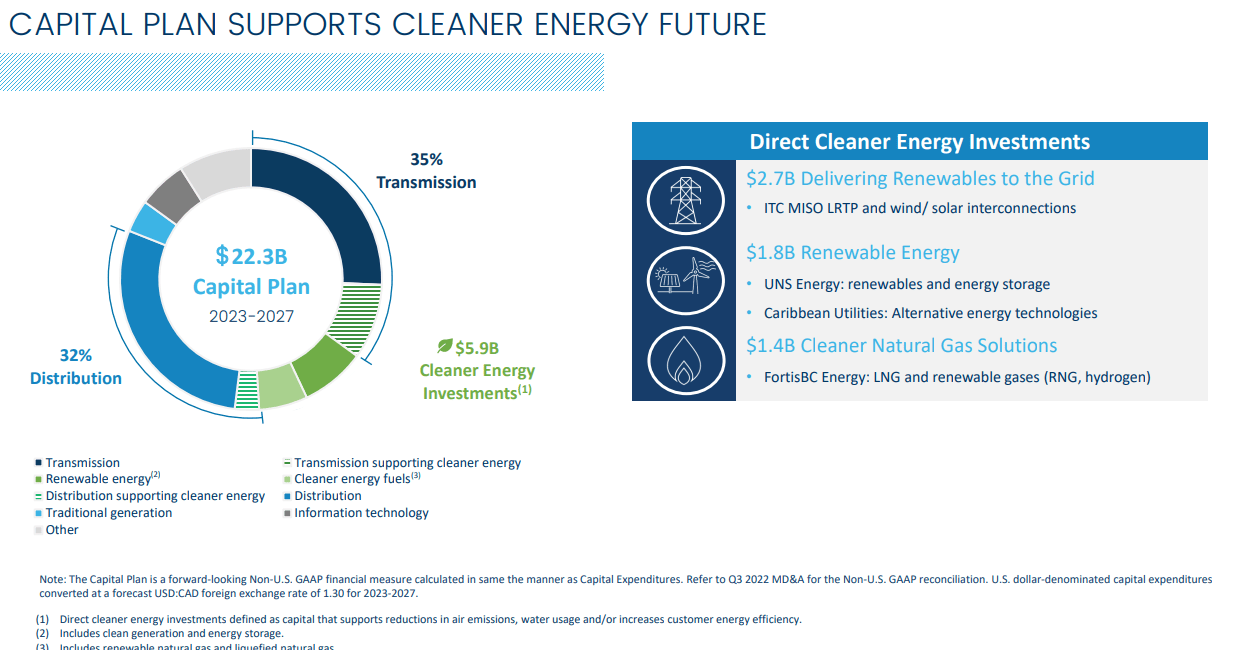

Company's Outlook

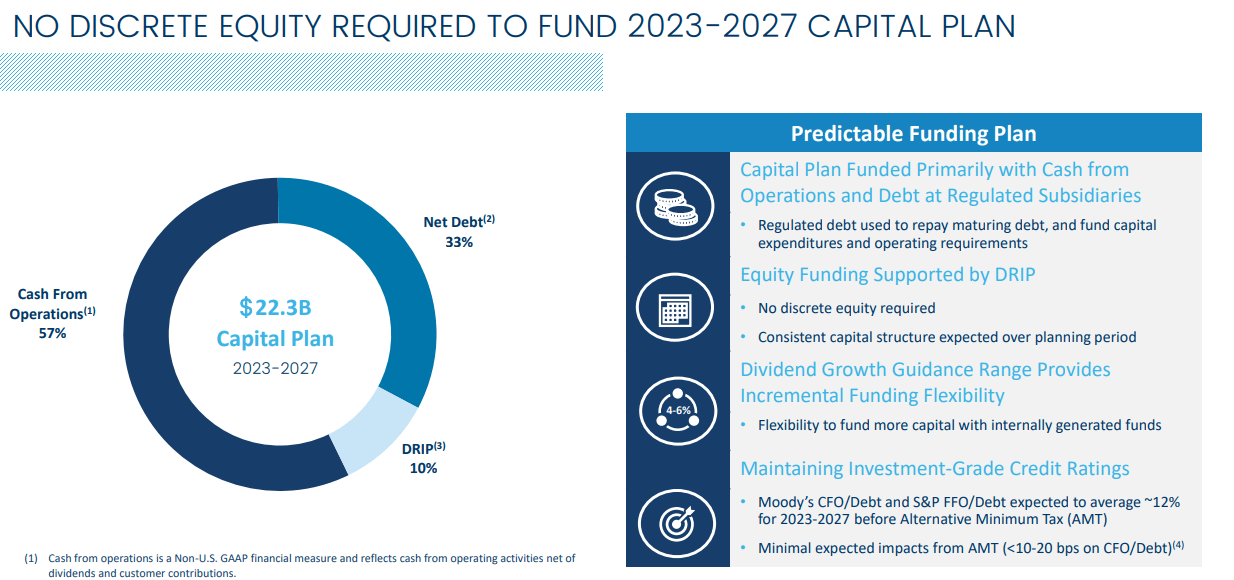

Fortis rolled forward its 5-year outlook as 2022 was dropped off and 2027 was entered into the equation. Spending plans are about 11.5% higher for this period than the previous one.

November 2022 Presentation

The bulk of this is regulated utility growth with Forex boosting total amounts by $0.5 billion. Cleaner energy will make up about 25% of total spend.

{kind=link}

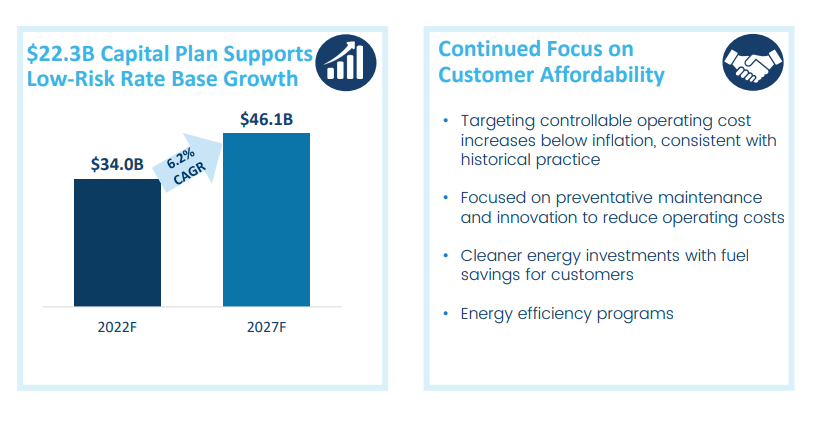

Fortis sees this supportive of an annual base rate growth of 6.2% per annum over the next 5 years.

{kind=link}

The same growth should allow a solid growth mantle for the dividend.

November 2022 Presentation

With a 4% current yield and at least 4% growth for the near future, the company looks like a delight to income investors who want predictable results. But does the entire case make sense?

Valuation And Risks

Fortis trades at 20.3X 2022 earnings per share. That number is hardly cheap in the best of times, let alone one where rates are rising rapidly. But in Fortis' defense, the company has historically traded on the expensive side and the market has been happy to extend it the credit for solid execution.

Most of the time when valuations reset, the pressure comes from either company faltering in some way, or via a recession. On the first front, Fortis has a solid plan to not issue any dilutive equity over the next 5 years. Equity issuance will be limited to the DRIP plan.

{kind=link}

It will still have to access the debt market for its maturing obligations and an additional $7.5 billion of debt. Currently its bonds are very well behaved and the market is not giving it any grief. The A-rating from S&P definitely helps it in this case. We don't see the situation as benign as the credit markets. Fortis is at 6.0X net debt to EBITDA, in the same zone as Emera. What is different vs. Emera is that Fortis is not facing any hostile regulatory body like Emera is. What is also different is that Fortis has a lower dividend and far more retained cash that reduces the need to tap credit markets to the same extent. Nonetheless, if you add the 20.3X earnings multiple and the 6X debt to EBITDA, we have to conclude the shares are not cheap by any stretch of the imagination.

Verdict

Fortis is an excellent company to keep on your watch list. We suspect you will get a chance to pick this up under 17X earnings at some point in the near future. At the current valuations we can salute the performance, but cannot jump in. Especially when Canadians have alternatives like ATCO Ltd. ( ACLLF ) ( ACO.X:CA ) and AltaGas Ltd. ( ALA:CA ) with far lower debt and both are trading at 5-6 earnings multiples lower. ATCO also has an equally enviable dividend streak . We rate the stock a Hold/Neutral while acknowledging that it is dangerously close to a Sell rating.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Fortis: A Dividend King In The Making