FTCO - Fortitude Gold: Compelling Story And Currently Yielding 8%

Summary

- FTCO is a small gold mining company with assets in Nevada.

- It offers an above-average dividend yield and trades at a below-average valuation.

- FTCO is one of the more attractive gold miners, we believe.

Note: This article was written with Darren McCammon and was released on Cash Flow Club earlier this year in a more expanded form.

Article Thesis

Fortitude Gold Corporation (FTCO) is a Nevada-focused gold mining company that offers a high dividend yield that is well-covered by cash flows. From a valuation perspective, FTCO also looks stronger than many of its peers, which could result in relative upside potential. For those looking for a gold stock, FTCO is worthy of a closer look.

Nevada As A Gold Region

Nevada is mostly desert. However, it also contains immense mineral wealth along the Carlin and Walker Lane formations and thus is the fifth largest gold producer globally. These formations are highly fractured fault zones that can be very attractive for mining (and geothermal). Additionally, Nevada offers a stable, mining-friendly regulatory environment with transparent, easy-to-navigate regulations and permitting processes and a straightforward mining tax regime.

Because mining has been going on in Nevada for many decades, the state also offers well-established infrastructure plus the necessary equipment and people with applicable skill sets. As a result, Nevada is cost-effective and inviting for the world's gold miners. Global giants such as Newmont Mining ( NEM ), Barrick Gold ( GOLD ), and Kinross Gold ( KGC ) all have producing mines in the state.

The above gold miners have also seen the price of their stocks climb significantly over the last three months as the price of gold has risen by 12% in those three months:

On a relative basis, FTCO has significantly underperformed these larger peers in this time frame, despite benefitting from the gold price increase as well. The relative attractiveness versus peers has risen due to this stock price underperformance, we believe.

Fortitude Gold

Fortitude Gold is a thinly traded ~$150 million market capitalization Nevada gold miner. It has no long-term debt and pays a compelling 8% dividend yield with a unique strategy to grow organically using existing cash flow. Instead of focusing on large, long-life mines like its larger peers, Fortitude lives off the leavings that are too small for its much larger peers as they don't move the needle for a company like Newmont. The FTCO business plan thus is to mine small but high-grade deposits in a cost-efficient manner before eventually moving on to a new asset when the previous one has played out.

We estimate FTCO's dividend payout will average about 60%-70% of income over the next year. However, that coverage is likely to be variable from quarter to quarter due to changes in gold prices, the firm's tendency to stack ore when prices are low (instead of processing it into gold and selling it), and so on.

Fortitude was spun out of Gold Resource Corp. ( GORO ) in December 2020 and has experienced management that knows what they are doing.

FTCO

These executives have heavily invested in the company themselves: Insider ownership is approximately 13%. This appears to be a meaningful amount of the insiders' net worth. We thus consider the firm well aligned with investor interests, which is an important factor to consider, especially when investing in smaller companies.

Since FTCO is able to finance its capital expenditures and its dividend from organic cash flows, dilution is unlikely. Fortitude currently has the rights to develop and mine six properties in Nevada: five around Hawthorne, NV, and a sixth (Ripper) which is further to the northeast near highway 50.

FTCO

The Isabella Pearl Mine is located near Hawthorn, NV, and currently produces about 40k ounces of gold per year at an all-in cost of $918 per ounce ($1,687 average selling price in Q3). The all-in cost benefits from the relatively high grade of ore they are mining (3.1 average grams per tonne whereas many large mines operate profitably at <2 grams per tonne). The total mine life for this location at 40k ounces per year, however, is only three years (2025 is currently the estimated end of productive life on this mine). Pearl provides almost all existing cash flows, paying for G&A and the future development of the entire enterprise.

The Golden Mile property is likely to be FTCO's next project. It is showing a very attractive 36.6m play at an average of 10.3 grams of gold per tonne. This mine is also located near Hawthorne and is expected to take FID this year and to start production in 2025. The plan is for this open pit mine to take over most production if/as Isabella Pearl peters out to lower-grade ore. FID on Golden Mile, expected this year, could thus be a key trigger event for FTCO shares.

FTCO

Drilling at the County Line location also looks promising . We believe this will be the third mine they develop as it is only 26 miles from Pearl via paved Nevada State Route 361 and is showing good drill results. FTCO owns mineral rights to three additional properties in Nevada, two of which are also near the Pearl, Golden Mile and East Camp Douglas locations above. This close proximity can be advantageous. It allows the option for preliminary ore processing to be done onsite, then for that to be trucked to existing Pearl facilities for final processing. Thus, it can save capex but entails additional fuel and trucking costs. This thus can be an attractive option that reduces both cost and risk. Additionally, this strategy allows companies to use some of the same equipment and people at multiple mine sites.

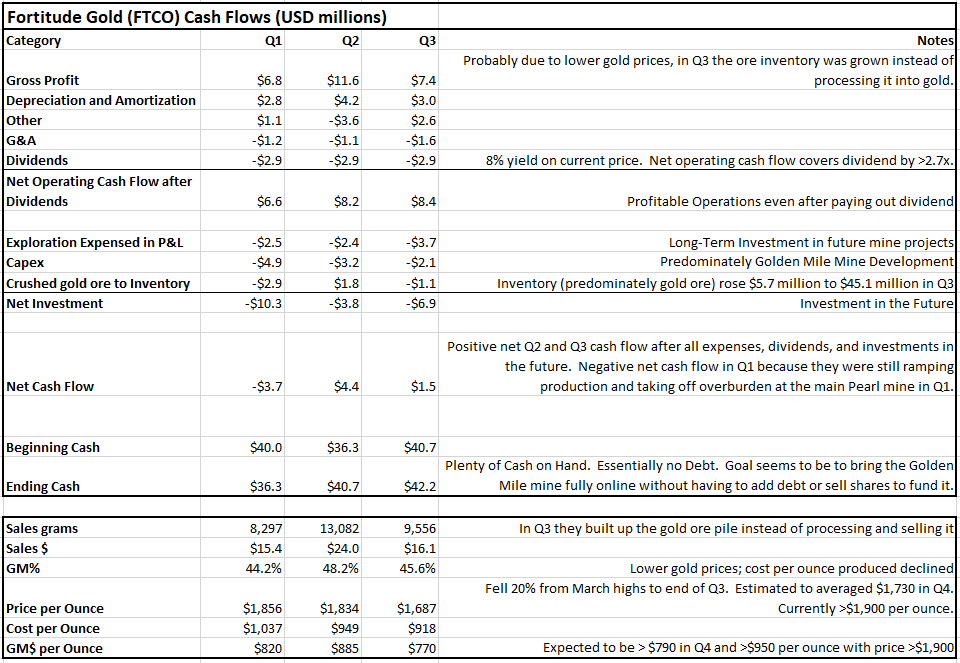

Cash Generation Looks Good

Below is a chart breaking down the last three quarters' cash flows:

{kind=link}

Note that the company currently has $45.1 million in inventory on its balance sheet, which is primarily crushed gold ore sitting in a leach field waiting for further processing into gold. The company adds to this inventory continuously but seems to be less eager to process it into gold and sell it when prices are lower.

Takeaway

There are three potential near-term drivers (and/or risks) for the price of FTCO stock:

- Continuing increases in the price of gold (or not).

- The firm making the final investment decision 'FID' on their Golden Mile property.

- Multiple expansion towards that of its peers as growing awareness and ability to invest in the firm by Wall Street expands with market cap.

While waiting for these potential drivers, investors get to collect a well-covered 8% dividend.

Fortitude's fortunes are clearly tied to the volatile price of gold, and the company is much smaller than many of its peers. This should rightly cause some hesitancy. For instance, only 38,000 shares trade hands on an average day.

FTCO's low valuation makes it look like it has considerable relative upside potential:

{kind=link}

With a well-below-average EBITDA multiple, cash flow multiple, and a way-above-average ROIC and dividend yield, FTCO looks like one of the better picks in the gold mining space right now. That doesn't guarantee compelling total returns, but for someone looking for a gold investment, FTCO could be more attractive than many of its peers, we believe.

For further details see:

Fortitude Gold: Compelling Story And Currently Yielding 8%