FSM - Fortuna Silver: Another Quarter Of Margin Compression

2023-08-15 23:03:19 ET

Summary

- Fortuna Silver's reported declining gold (legacy operations) and silver production in Q2 is translating to lower revenue year-over-year and negative free cash flow.

- This was impacted by a stronger Mexican Peso, a temporary blockade at San Jose, and elevated sustaining capital at its legacy gold operations.

- In this update, I'll look at whether the stock is finally offering enough margin of safety to consider a long position, with a high-margin mine in Seguela nearing commercial production.

It's been a mixed Q2 Earnings Season so far for the Gold Juniors Index ( GDXJ ) and while there have been a few disappointments such as those from Coeur Mining ( CDE ) and Hecla Mining ( HL ), Fortuna Silver's ( FSM ) performance was not much better. Not only was silver production down sharply year-over-year, but gold production was down at its legacy operations and costs rose sharply at all of its operations as well. This resulted in lower sales revenue year-over-year despite the record gold price and another quarter of negative free cash flow. And while the future is brighter after some temporary hiccups with Seguela now online, there appears to be reduced appetite for owning West African producers with several names severely underperforming their peers over the past month. Read my previous coverage on FSM here. And, now let's look at Fortuna's Q2 results below:

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Q2 Production & Sales

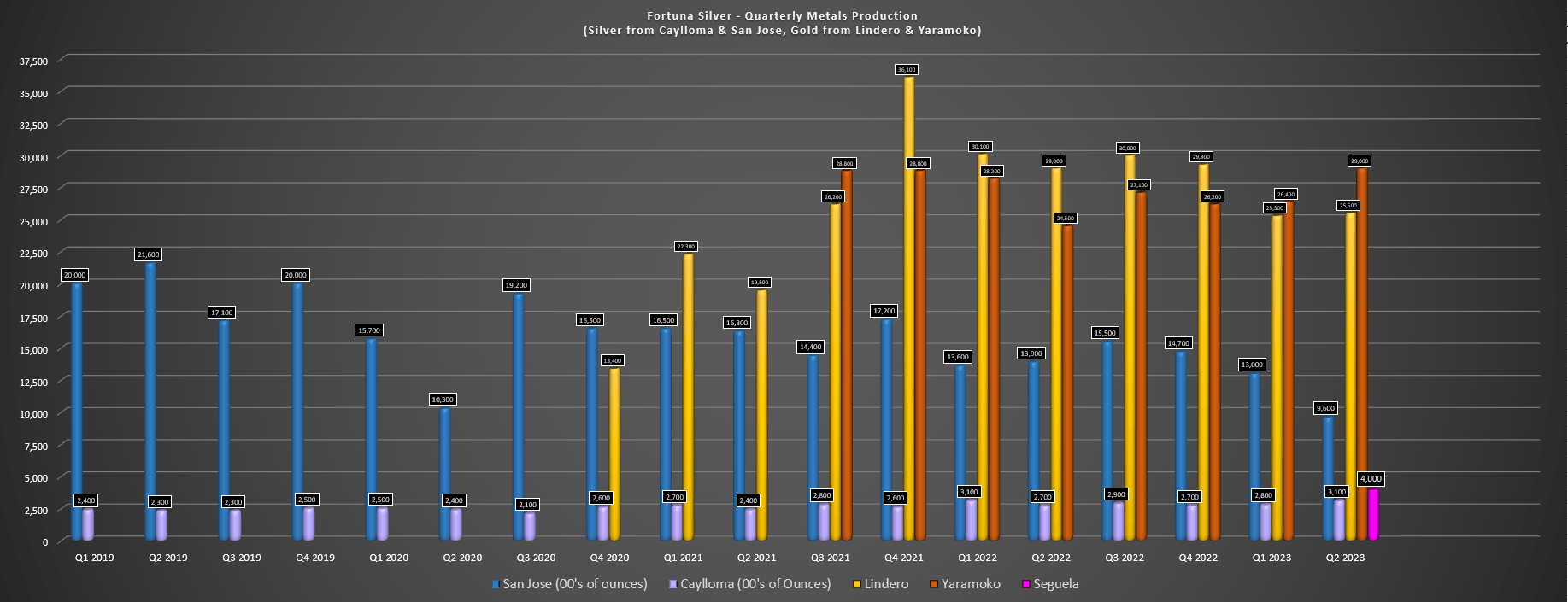

Fortuna Silver ("Fortuna") released its Q2 results earlier this month, reporting quarterly production of ~64,300 ounces of gold and ~1.26 million ounces of silver, translating to a 4% increase in gold production, offset by a 24% decline in silver production. The increase in gold production was driven by an initial contribution from its new Seguela Mine in Cote d'Ivoire (~4,000 ounces), while gold production from its legacy assets was down marginally in the period. The dip in gold output was related to a softer quarter at its Lindero Mine (lower grades in line with mine sequencing), fewer gold ounces produced at San Jose after a temporary blockade (lower throughput and limited access to high-grade stopes), offset by a better quarter at Yaramoko despite underground access being impeded by a failure of the Armtec tunneling structure at the portal. As for silver production, San Jose saw a sharp decline in throughput and grades related to the blockade discussed earlier.

Fortuna Silver - Quarterly Metals Production by Mine - Company Filings, Author's Chart

{kind=link}

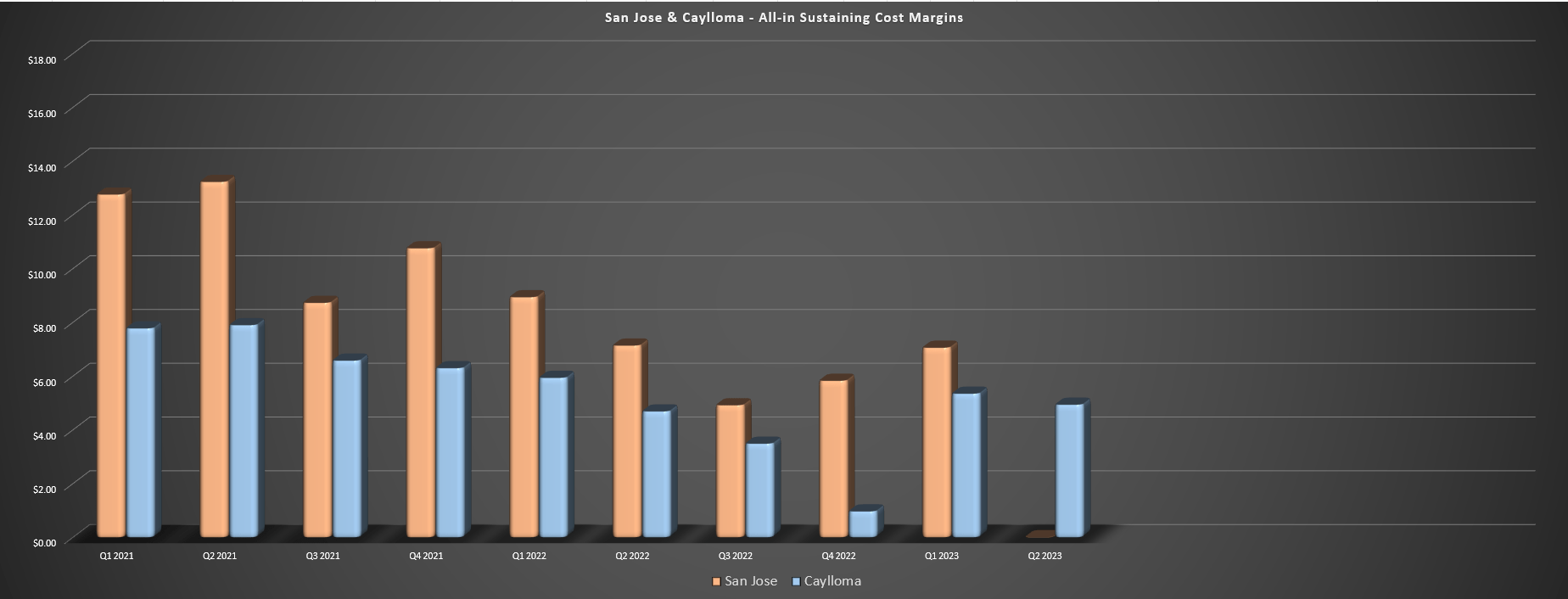

Fortunately, the blockade by the workers' union has since been resolved, but the company did note that it saw resignations of personnel following the resolution and higher absenteeism. And while access to planned higher-grade stopes will be available in Q3 to drive a better performance, a one-time payment of $2.8 million was made related to the new labor agreement. The result was that costs soared to $24.07/oz in the period (Q2 2022: $15.41/oz) despite lower sustaining capital, leaving the mine with an AISC margin of $0.02/oz for the period, down from $7.15/oz in Q2 2022 despite a higher average realized silver price. And while not much of a contributor, its Caylloma Mine in Peru didn't fare much better, with razor-thin AISC margins of $4.95/oz affected by inflationary pressures and weaker base metals prices.

San Jose & Lindero - AISC Margins - Company Filings, Author's Chart

{kind=link}

While the minor hiccup here isn't a big deal as San Jose has seen declining for years, it will lead to cost guidance being above the prior guidance range. And unfortunately at the company's new mine, we've seen some minor hiccups as well, with Seguela expected to be at the lower end of its production guidance range of 60,000 to 75,000 ounces in FY2023. As noted by the company, initial feed for commissioning was primarily oxide ore from the upper 10 meters at the Antenna Pit, but that section appeared to have been "heavily depleted" due to artisanal mining activities, with grades coming in lower than expected. The company also noted that "the nature of this oxide ore also caused issues within the first stages of the processing circuit leading to reduced throughput" .

{kind=link}

In addition to this setback, the mine experienced a failure of the primary transformer for the SAG Mill that resulted in a nine day shutdown and vendors needed to be brought in to help with repairs with modifications put in place to prevent any future issues. This should impact planned Q3 production levels even if the operation is now running more smoothly at nameplate capacity of 154 tonnes per hour. Overall, this isn't a big deal in the grand scheme of things and Seguela should have a strong FY2024 once better grades are hitting the mill and it ramps up to commercial production. Still, with Lindero's costs tracking to the high end, Seguela's output tracking to the low end and San Jose's costs tracking to the high end, this was certainly a disappointing quarter.

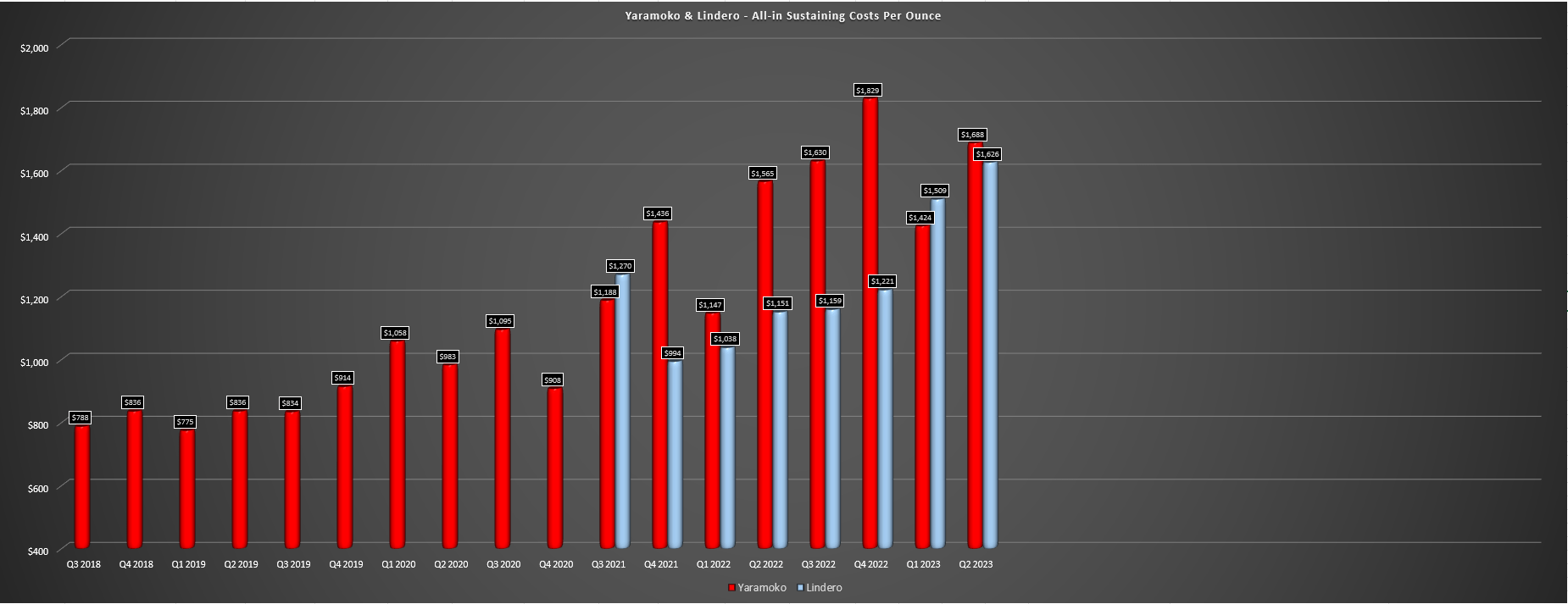

Finally, at the company's legacy gold operations (Lindero and Yaramoko), the two assets combined for production of ~54,400 ounces, with Yaramoko's output up year-over-year on the back of higher grades and throughput (~144,200 tonnes at 6.5 grams per tonne of gold). However, costs at these assets remain elevated, with increased sustaining capital resulting in all-in sustaining costs of $1,688/oz at Lindero (Phase 2 heap-leach expansion, capitalized stripping) and $1,626/oz at Yaramoko (increased underground development). And while these costs will normalize, this translated to consolidated AISC of $1,799/oz for the company, a massive increase vs. $1,434/oz last year, resulting in razor-thin AISC margins on a gold-equivalent basis of ~9% ($175/oz).

Yaramoko & Lindero - All-in Sustaining Costs (Company Filings, Author's Chart)

{kind=link}

Financial Results

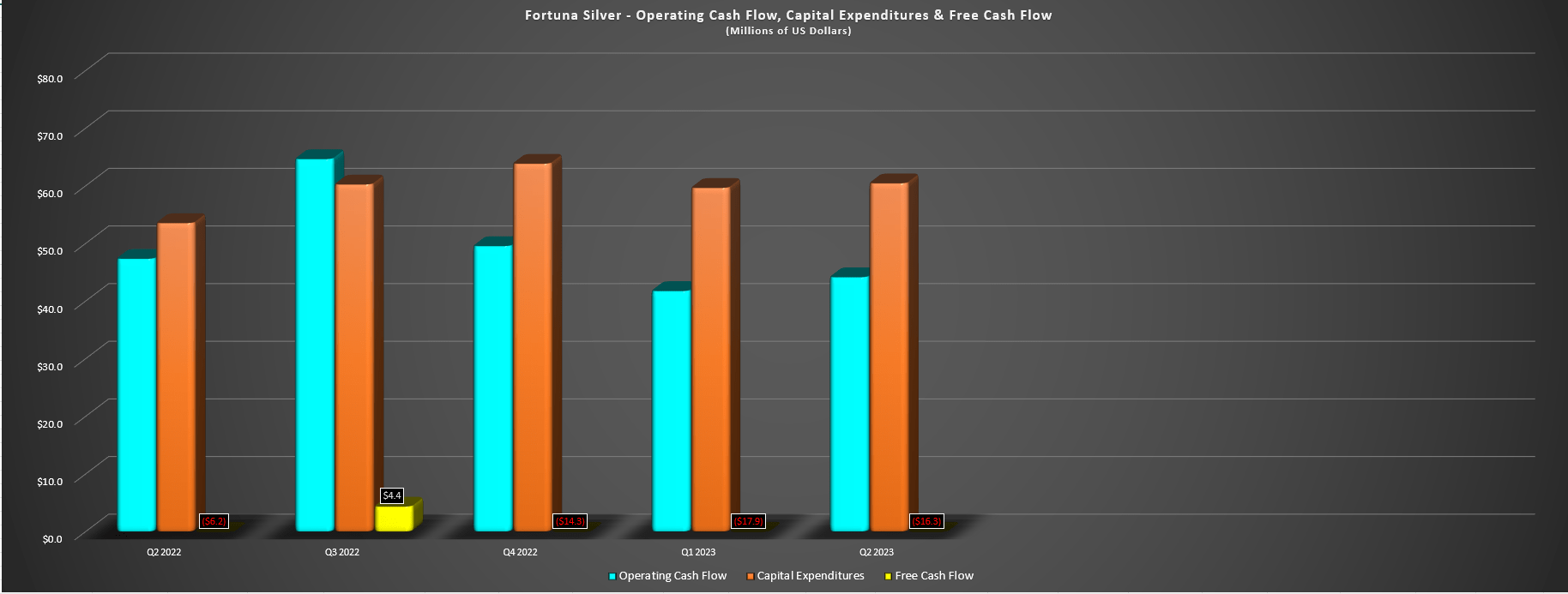

Moving over to the company's revenue, Fortuna reported a sharp decline in revenue to $158.4 million (down over 5% year-over-year) despite the benefit of higher realized prices. This was related to fewer ounces sold than produced in its gold segment and lower production levels for silver. The result was that operating cash flow sunk to $44.2 million (down 7% year-over-year), while we saw a free outflow of $16.3 million, down from a cash outflow of $6.2 million in the year-ago period. The good news is that these figures should improve with Seguela construction complete and it expected to be a solid free cash flow generator. However, while a return to free cash flow positive is welcome, I continue to be luke-warm on Fortuna's position as a silver producer with San Jose running low on reserves (and potentially dealing with higher profit sharing costs), and I don't see any way that the company will retrieve its previous multiple as a high-cost (consolidated basis) predominantly West African gold producer.

Fortuna Silver - Operating Cash Flow, Capex & Free Cash Flow (Company Filings, Author's Chart)

{kind=link}

Some investors will note that Fortuna is trading at an attractive valuation, with the company capable of generating up to $200 million in free cash flow next year if metals prices cooperate. And while this is a very reasonable valuation for a company with an enterprise value of ~$1.15 billion (~6x EV/FCF), it's worth noting that other producers with higher margins, more impressive operations and exposure to Tier-1 jurisdictions (unlike FSM) are trading at similarly attractive valuations.

One example is like B2Gold ( BTG ) which trades at just ~5.0x FY2025 EV/FCF estimates of ~$700 million with larger scale (~1.1 million ounces per annum), much lower costs (~$1,025/oz vs. FSM above $1,450/oz per GEO) and a team with a superior track record of creating shareholder value. So, while FSM may be getting more reasonably valued, I continue to see better relative value elsewhere, especially when we factor in that Goose could be a ~400,000-ounce operation at sub $900/oz costs long-term with permitted capacity of ~6,000 tonnes per day and the possibility of high-grade satellite operations (like George) to feed its plant.

Recent Developments

Unfortunately, while gold and silver prices were a tailwind in Q2 to make Fortuna's disappointing results look less bad, they have done little to since July. In fact, the average quarter-to-date price for gold and silver are sitting at $1,930/oz and $23.20/oz, respectively, down over 2% and 4% from their average prices in Q2. Simultaneously, the Mexican Peso strengthened substantially to start Q3 and has held onto most of its gains, suggesting another tough quarter from a cost standpoint ahead at San Jose, especially when combined with what appears to be a less favorable labor situation (resignations, absenteeism). So, while miners with operations outside of Mexico could see softer margins in Q3 related to weaker metals prices if the trend doesn't reverse soon, it will affect Fortuna more than the average company because of the unfavorable MXN/USD exchange rate.

"San Jose is at risk of finishing the year below the lower end of its guidance range as a result of an illegal blockade by the workers’ union related to demands on higher profit sharing distributions and increased absenteeism and resignations following resolution of the blockade."

The other recent development worth noting is that the security has not improved in Burkina Faso, and one West African miner that is certainly open to operating in riskier jurisdictions decided to divest two of its mines last month (Boungou and Wahgnion). And while Fortuna only has one operating mine in Burkina Faso (Yaramoko), this negative sentiment surrounding West African producers has weighed on the share prices of several companies, including Orezone ( ORZCF ), Endeavour Mining ( EDVMF ), and Perseus Mining ( PMNXF ). Although this has fortunately not affected operations, it doesn't help that a second jurisdiction of Fortuna's is seeing increased uncertainty, and this time one where it's heavily concentrated after its pivot to becoming predominantly a West African gold producer (~50% of FY2024 revenue coming from West Africa + a new development asset in West Africa).

{kind=link}

So, with Mexico and Africa being less in favor from an investment standpoint than last year with elevated uncertainty, it's possible that we could see discount rates higher and downside pressure on FSM continue.

Summary

Using what I believe to be more conservative multiples of 5.0x forward cash flow and 0.90x P/NAV and a 65/35% weighting (P/NAV vs. P/CF), I see a fair value for Fortuna of US$4.30. Although fair value estimate points to a 43% upside from current levels, I am looking for a minimum 40% discount to fair value to ensure an adequate margin of safety for small-cap producers that operate out of non-Tier 1 ranked jurisdictions. After applying this required discount to Fortuna to determine its low-risk buy zone, its ideal buy zone comes in at US$2.60 or lower, suggesting there is still not enough of a margin of safety in place. And while the stock could bottom here and I could be wrong, I prefer to pay the right price or pass entirely, especially when there are better deals in safer jurisdictions elsewhere in the sector.

Some investors might argue that there's a substantial upside for Fortuna Silver here and that it has traded at much higher multiples in the past. While true, its cost profile is far different (much higher costs even with Seguela), its silver reserves are shrinking, and it's transformed from a Lat Am precious metals with a significant portion of revenue from silver to a West African gold producer with only moderate (and dwindling) silver exposure. And if we compare Fortuna's multiples with higher-margin peers like Endeavour Mining and Perseus Mining which also trade at less than 5x forward cash flow, I don't see that much of a valuation disconnect here, especially with sentiment worsening for African producers recently. To summarize, I remain focused elsewhere for the time being, but I would become more interested if FSM were to dip below US$2.60 and filled its open gap.

For further details see:

Fortuna Silver: Another Quarter Of Margin Compression