FSM - Fortuna Silver: Earnings Miss On Weaker Silver Price Mostly Priced In

- Fortuna Silver released its Q2 results this week, reporting quarterly production of ~1.65 million ounces of silver and ~62,200 ounces of gold, translating to a meaningful increase in revenue.

- However, with the impacts of provisional pricing adjustments, an inventory write-down, inflationary pressures, and weaker silver prices, earnings were down sharply in the period.

- While FSM has guided for the upper end of cost guidance following the report, I believe the Q2 earnings miss on weaker silver prices and one-time items is mostly priced in.

- So, with Seguela in the wings and on schedule/budget and easier year-over-year comps ahead now that FSM has lapped tough comps, I would view pullbacks below US$2.30 as buying opportunities.

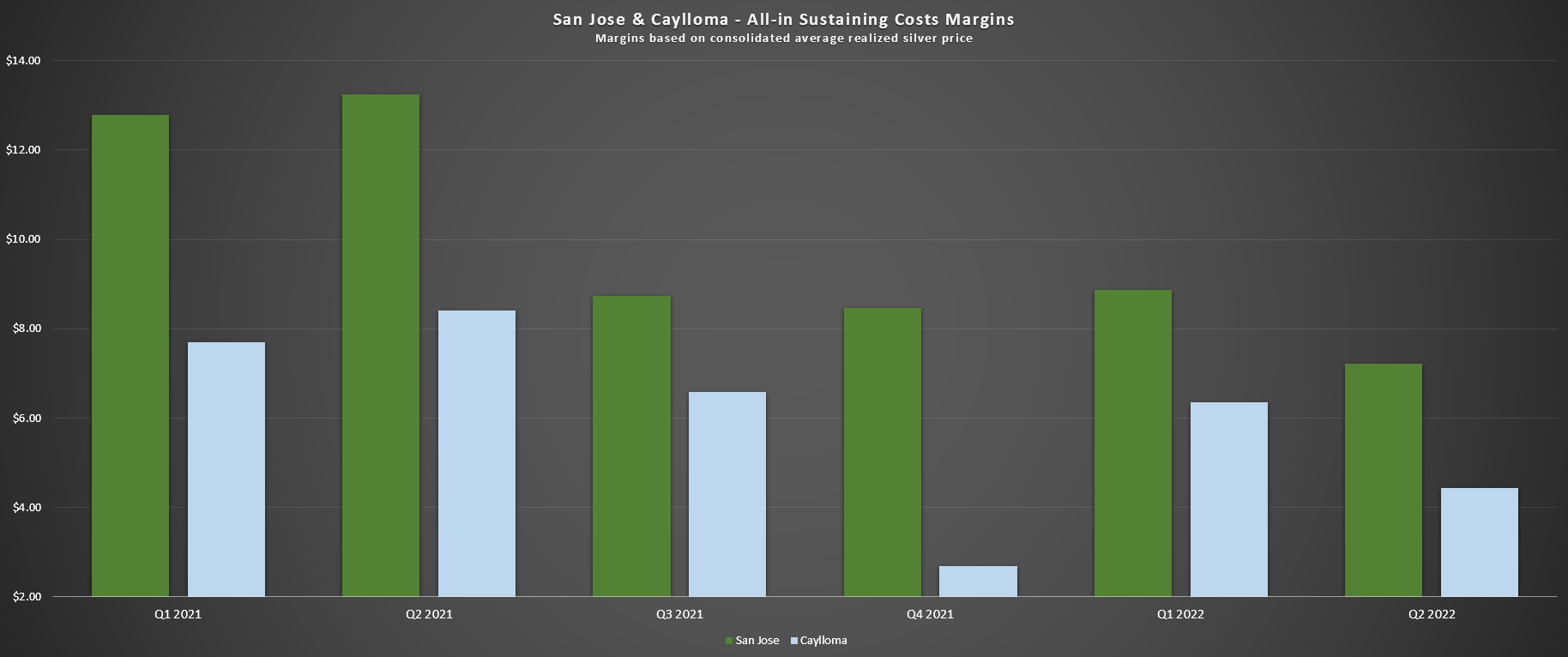

As I discussed in my May article on Fortuna Silver ( FSM ), the softer silver price was likely to produce a much uglier quarter for its silver business (which is why it made zero sense to chase the stock above US$3.50 in May). This was especially true given the difficult year-over-year comps Fortuna was up against, enjoying an average realized silver price of $26.65/oz. The result was that AISC margins were likely to dip below $8.00/oz at San Jose and below $5.00/oz at Caylloma, translating to meaningful margin compression and making it harder to beat estimates. The results were worse than expected, given inflationary pressures and the weaker silver price - one reason I have avoided silver producers this year.

Not only were silver producers dealing with higher per tonne costs due to the impact of inflationary pressures (which didn't show up in FY2021 margins due to the strong silver price), but the tailwind of a strong silver price had reversed sharply as of May. Fortuna- tely , Fortuna Silver is more like Fortuna Gold following its Roxgold acquisition, so while the margin compression is negative, it's only impacting a portion of the business vs. names like Endeavour Silver ( EXK ) that have razor-thin margins on a consolidated basis. Let's take a closer look at the quarter below.

Seguela Construction Update (Company Presentation)

{kind=link}

Q2 Production & Financial Results

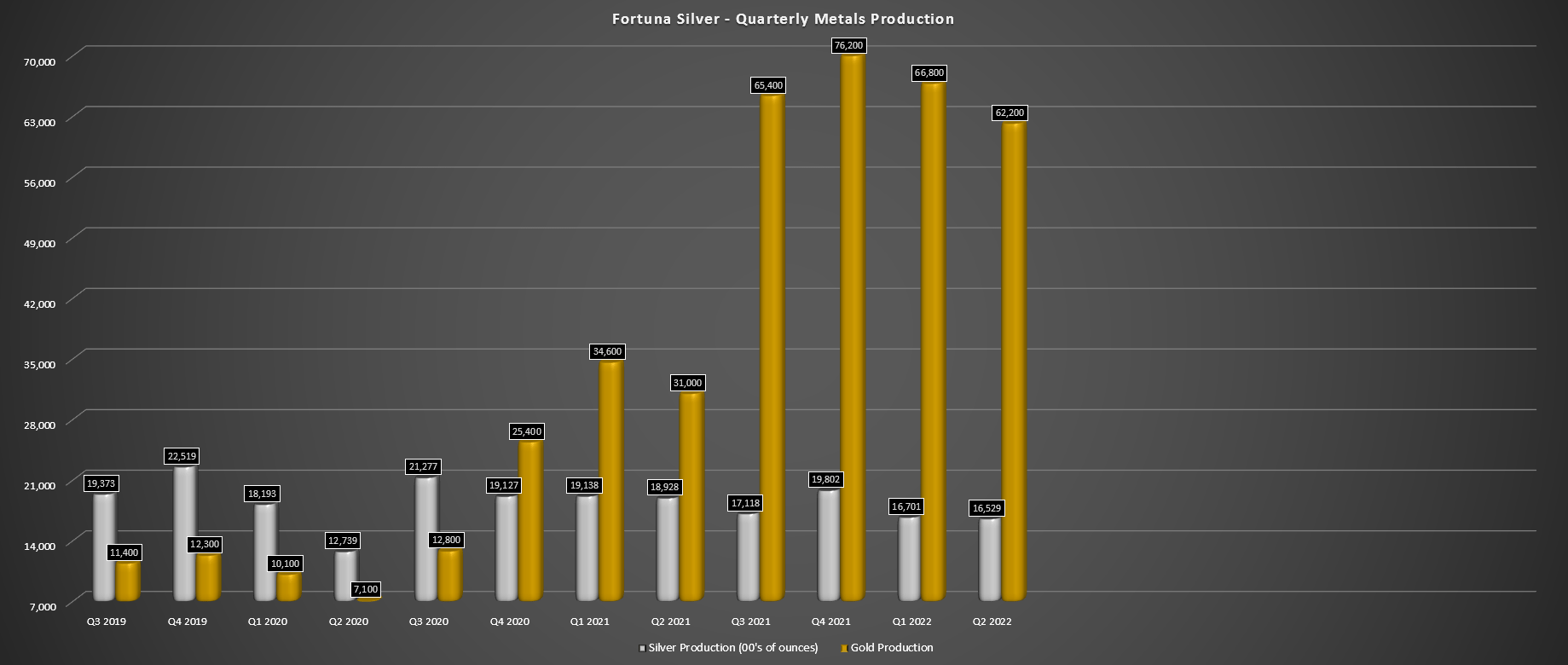

Fortuna Silver ("Fortuna") released its Q2 production results in July, reporting quarterly production of ~62,200 ounces of gold (100% increase) and ~1.65 million ounces of silver (15% decline). The 100% increase in gold production was related to the acquisition of Roxgold (addition of the Yaramoko Mine) and a successful ramp-up at the company's newly constructed mine in Argentina. This meaningful increase in gold production (helped by ~24,500 ounces from Yaramoko) helped the company to deliver a 39% increase in revenue, offset lower production due to softer grades, and fewer tonnes processed at San Jose.

Fortuna Silver - Quarterly Production (Company Filings, Author's Chart)

{kind=link}

While the headline EPS number ($0.01 vs. $0.09) was ugly due to the sharp decline in the realized silver price ($22.62/oz vs. $26.85/oz), operations performed well overall. However, earnings per share were mostly impacted by inflationary pressures, silver price softness, and one-time items. These included negative final price adjustments, which impacted by-product credits, similar to what Newmont ( NEM ) saw, leading to a very messy Q2 report. Additionally, Fortuna had a $4.0 million write-down in low-grade inventory at Yaramoko, a further headwind in the period.

Fortunately, despite the one-time items, lower production at San Jose (~1.39 million ounces of silver and ~8,300 ounces of gold vs. ~1.62 million ounces of silver and ~10,300 ounces of gold), and inflationary pressures, Fortuna still delivered positive free cash flow in the period. That said, the $19.2 million in free cash flow was well below estimates, declining year-over-year despite the much better production at Lindero (improved performance of stacking/crushing circuits) and adding a new asset to the portfolio, Yaramoko.

Overall, I don't see any reason to be negative about the production results in the period, and the company continues to track well against its guidance. Besides, for investors familiar with the story, Segeuela is a game-changer for Fortuna and arguably a top-10 asset in Africa once in production. In fact, with the benefit of new high-grade zones (Sunbird), the potential to increase throughput to 1.6+ million tonnes per annum and potentially displace lower-grade ounces with higher-grade material, this could be a ~155,000+ ounce per annum asset with sub $875/oz all-in sustaining costs vs. the projected production profile of ~120,000 ounces in the most recent technical report.

Costs & Margins

While production came in at respectable levels, we did see cost creep, and like other producers, Fortuna noted that it had experienced inflationary pressures. Fortuna called out diesel, reagents, consumables, cement, and steel as items that were impacting unit costs. At San Jose, costs increased to $15.41 (Q2 2021: $14.51/oz), while Caylloma saw costs decline to $18.19/oz, but the asset was up against easy year-over-year comps. This translated to AISC margins of $7.21/oz and $4.43 at San Jose and Caylloma, respectively, compared to $13.24/oz and $7.91/oz in the year-ago period. All-in sustaining cost margins are based on the consolidated average realized silver price.

San Jose / Caylloma AISC Margins (Company Filings, Author's Chart)

{kind=link}

Obviously, this is significant margin compression, and it's no surprise that the company had trouble beating estimates with the negative impact of provisional pricing adjustments and inflationary pressures. However, as discussed earlier, Fortuna Silver is more like Fortuna Gold, so while the margin compression here is disappointing and exploration success will be needed at San Jose to make this a viable asset long-term, I don't see the margin compression in the silver segment as a huge issue, given that the gold business is much more important, contributing ~$120 million of revenue (71%).

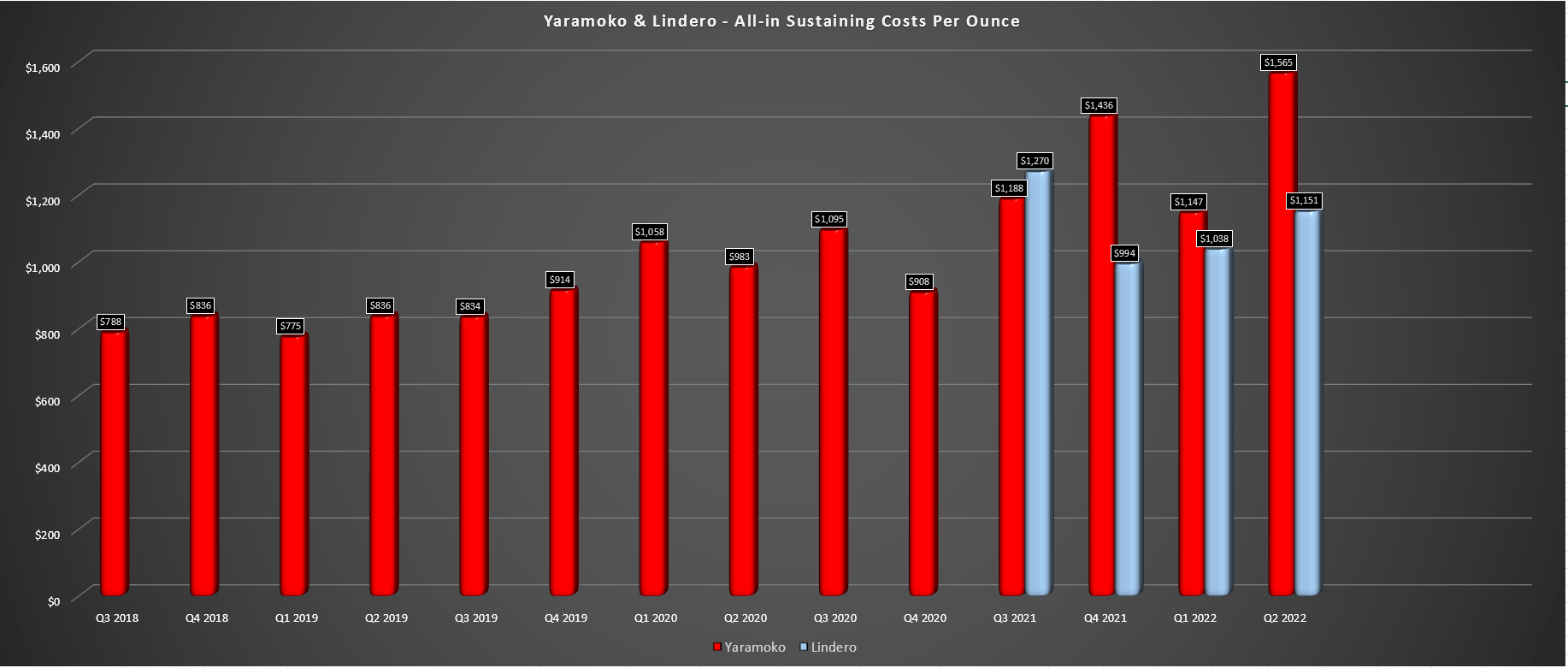

Looking at the gold business, costs were up here as well, with Lindero's all-in sustaining costs [AISC] coming in at $1,151/oz and Fortuna noting that costs will trend towards the upper end of guidance due to inflationary pressures ($900/oz - $1,100/oz). Meanwhile, Yaramoko is also expected to see costs come in well above guidance. However, this is related to accelerated capital spending to provide earlier access to the QV Prime Zone at Bagassi South Mine. During the quarter, Yaramoko's costs spiked to $1,565/oz, though this was related to the write-down of low-grade stockpiles and elevated sustaining capital expenditures.

Yaramoko / Lindero - All-in Sustaining Costs (Company Filings, Author's Chart)

{kind=link}

Based on the higher costs for Lindero and Yaramoko in the period, all-in sustaining cost margins slid to $719/oz (Q1 2022: $846/oz) and $305/oz (Q2 2021: $737/oz), respectively. These are significant declines and judging by the comments on cost guidance, they're not expected to improve in the second half, and it looks like Fortuna will be working with a lower gold price ($1,800/oz vs. $1,880/oz in H1 2022). While I'm not that optimistic about meaningful margin improvements at Yaramoko under its new mine plan ($1,380/oz AISC), we could see some minor improvements at Lindero with cost improvement initiatives underway.

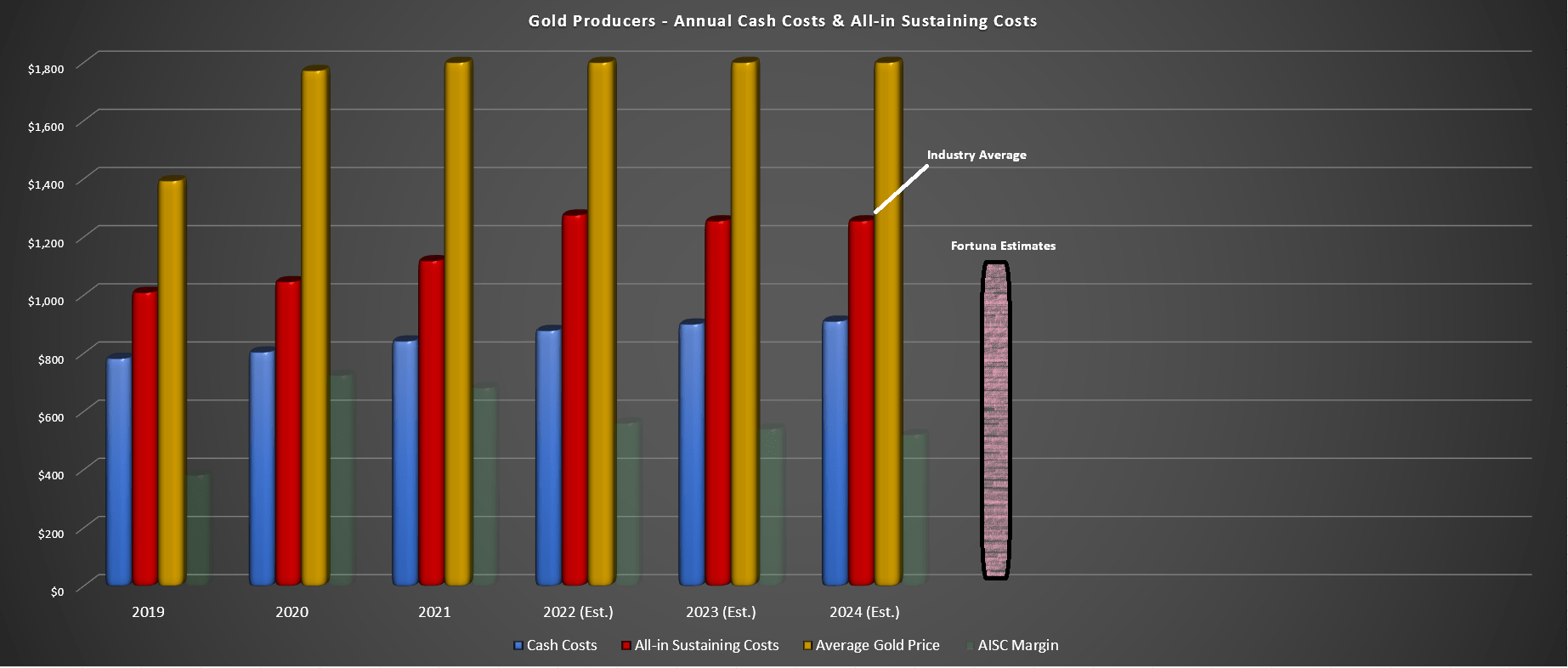

The good news is that Seguela (if it performs to plan, which looks likely under strong leadership) will lead to a dramatic improvement in consolidated all-in sustaining costs once in commercial production for 2024. This is because it should increase annual gold production by over 70% (2024 figures) at 30% lower consolidated costs. So, Fortuna should see its consolidated costs for its gold business dip below $1,110/oz once Seguela is in commercial production, giving it a cost profile slightly below its peer group (2024 estimates: ~$1,260/oz). Let's see where the valuation stands after the recent sell-off.

Gold Producers - Cash Costs, All-in Sustaining Costs (Company Filings (Historical), Current Guidance, Author Estimates)

{kind=link}

Valuation

Based on an estimated ~294 million fully diluted shares at year-end and a share price of US$2.60, Fortuna trades at a market cap of ~$764 million. With an estimated NPV (5%) of $1,220 million for Lindero, Seguela [+] exploration upside, Caylloma, and Yaramoko combined, Fortuna now trades at a valuation where the negativity surrounding its asset with the most uncertainty (poor reserve replacement, permitting dispute) is mostly priced into the stock. Hence, while any reserve deletions or inability to replace reserves could weigh on FSM short-term, the stock looks to be worth $2.50 per share on these four assets alone. In other words, investors are getting San Jose, Boussoura, and any additional regional discoveries (not including Sunbird) for free.

To arrive at a fair value of $2.50 per share for these assets, I have adjusted for projected corporate G&A and applied a 0.85x multiple to these assets.

This doesn't mean the stock has to go higher immediately, and as we've seen with higher-quality companies like Agnico Eagle ( AEM ), the fundamentals go out the window during secular bear markets, like what we've experienced in the GDX (2-year decline of 46%). That said, investors can finally be comforted by the fact that there is value here if the stock dips below US$2.50. Additionally, they can be comforted by the fact that prevailing sentiment on Fortuna has turned from "this is a quadruple", coming from those that apparently thought that a PE multiple of 30 was the right valuation for a Tier-2 jurisdiction producer, to disgust and possibly despondency for those that aren't willing to cut losses.

Analysis of Fortuna Silver (Twitter)

{kind=link}

When valuation and sentiment are both in one's favor, this can create excellent buying opportunities, and while I wouldn't rule out a lower low below US$2.40 on Fortuna to shake out weak hands, I think this would create the conditions for many long-term investors to throw in the towel. This is because this capitulation would occur near multi-year support for the stock. So, if the budget allows, I would view this as a great place to retire more shares using its share repurchase program to soak up some of the softness in the market and improve per share metrics that will get a major boost once Seguela comes online.

Summary

Fortuna had a decent quarter in Q2, but it's clear that inflationary pressures are impacting the business, like most other producers. Given that many inflationary pressures look stickier than expected and the weaker silver price (sub $22.00/oz), I am less optimistic about the reserve trend at San Jose, which was already in sharp decline during a period of rising silver prices. So, even if the permitting dispute is resolved, I think the more significant issue is the declining reserves, suggesting this asset should be discounted accordingly.

The good news is that Fortuna is past the difficult year-over-year comps in its silver segment (and it's actually looking at easy comps for (Q2 2023/Q3 2023), and Seguela is coming to the rescue from a consolidated margin standpoint. This has set Fortuna up for a much better period in H2 2023, and this team deserves praise for keeping this project on schedule and budget, which isn't surprising under the strong leadership of Chief Operating Officer Paul Criddle, who did a phenomenal job with Yaramoko (on budget and on time).

Given this brighter future and the negativity surrounding the stock, I think we've seen most of the downside here at US$2.60. Therefore, if I wanted to own FSM, pullbacks below US$2.30 should present buying opportunities. It's easy to be negative given the price action, but I think the true potential of Seguela has been lost in the noise, and at current levels, one can justify much of the valuation for Fortuna on Seguela, Lindero, Yaramoko, and Caylloma alone. So, while negative developments at San Jose and Yaramoko could impact the stock short-term, the worries about the long-term viability of these assets are mostly priced into the stock here.

For further details see:

Fortuna Silver: Earnings Miss On Weaker Silver Price Mostly Priced In