FVI:CC - Fortuna Silver: Impairments And Rising Costs Overshadow Seguela Progress

2023-03-16 10:17:13 ET

Summary

- Fortuna Silver Mines continues to be one of the worst-performing precious metals names in the sector, down ~65% from its highs above $9.00 per share.

- I attribute the underperformance to rising costs across its portfolio, negative surprises at its recently acquired Yaramoko Mine, and worsening sentiment around some jurisdictions where it operates.

- Unfortunately, despite this decline, I still don't see the stock as undervalued, with it trading near 1.0x P/NAV, a premium compared to many other Tier-2/Tier-3 jurisdiction gold producers.

- Although a rising tide (precious metals prices) will lift all boats and Seguela nearing commissioning is a positive, I see Seguela as a bandage for a mediocre portfolio, and I continue to see Fortuna Silver Mines as an inferior way to play the sector.

The Q4/FY2022 earnings season for the VanEck Vectors Gold Miners ETF ( GDX ) is nearing its end, and it was a disappointing year overall. While several companies delivered on production, several producers missed cost guidance, many by a country mile, like Equinox Gold ( EQX ) and SSR Mining ( SSRM ). This was mostly because of inflationary pressures but was exacerbated by lower output because of COVID-19 related exclusions, supply chain headwinds, labor tightness, and or extreme weather in some jurisdictions. The result was that sector-wide all-in-sustaining costs ((AISC)) soared 15% to ~$1,300/oz, and on a two-year basis (FY2022 vs. FY2020), AISC margins fell over 30% to ~$500/oz.

Investors in Fortuna Silver Mines Inc. ( FSM ) have continued to shrug off or look the other way from the rising cost profile of its current portfolio given that it has a high-margin project in the wings nearing commissioning, Seguela. However, the cost increases across the portfolio aren't insignificant, nor is the ability to replace reserves at its #2 (San Jose) and #4 assets (Yaramoko) with steadily declining grades and ounces at the former. Worse, the impact of inflationary pressures actually led to impairments at its #2 and #3 assets this year (San Jose and Lindero) with a massive ~$164 million impairment that led to net losses per share last year. Let's dig into the results below and see whether the stock has priced in the worsening margin profile at other assets and whether Seguela can come to the rescue.

{kind=link}

Q4 & FY2022 Production

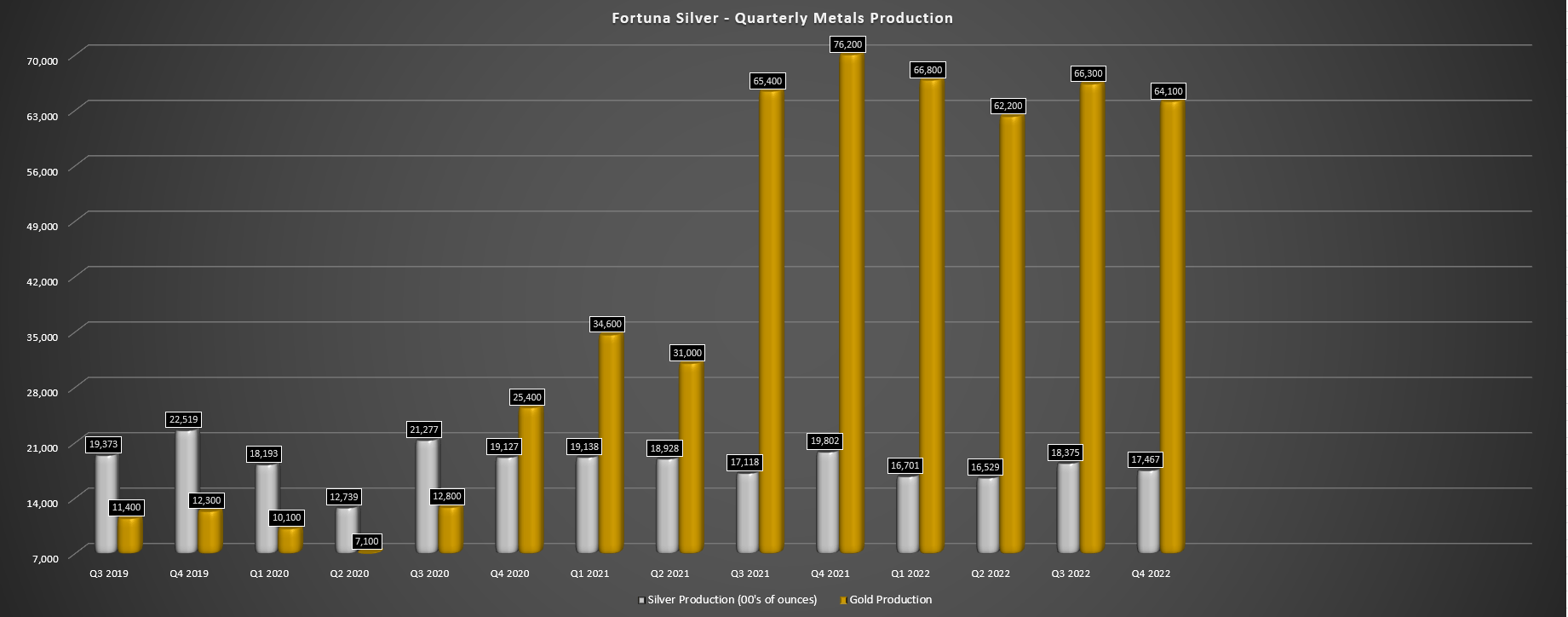

Fortuna Silver Mines ("Fortuna") released its Q4 and FY2022 production results earlier this year, reporting quarterly production of ~64,100 ounces of gold and ~1.75 million ounces of silver and roughly ~400,000 gold-equivalent ounces. This was an improvement from the year-ago period with a full year of contribution from its new Yaramoko Mine in Africa, with the high-cost asset contributing ~106,100 ounces for the year, up from ~57,500 ounces in a partial year in 2022. However, the clear theme across the portfolio is declining grades at its top-3 assets which is leading to higher costs, and even increased throughput at two of these assets (Yaramoko/Caylloma) has been unable to make up the shortfall.

Fortuna Silver - Quarterly Metals Production (Company Filings, Author's Chart)

{kind=link}

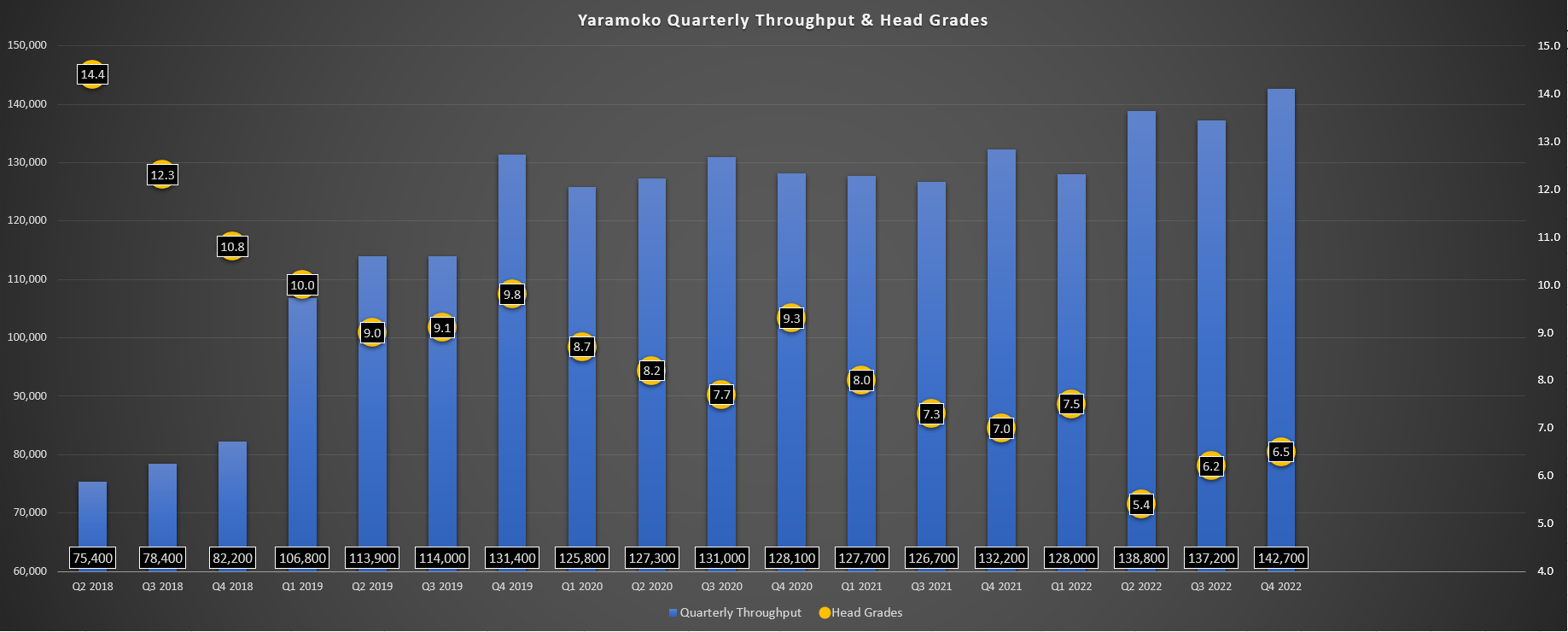

Yaramoko Mine - Operating Metrics (Company Filings, Author's Chart)

{kind=link}

Looking at the chart above, we can see substantial growth in production for Fortuna, and this growth is expected to continue with its high-grade development stage asset in Cote d'Ivoire (Seguela) nearing completion (93%). However, it's important to note that this growth came at quite a cost, with Fortuna's share count soaring from ~187 million fully diluted shares to ~294 million fully diluted shares (57% increase) in order to acquire Roxgold. At the onset, this looked like a great deal that would transform Fortuna into a high-margin producer with a production profile closer to 600,000 gold-equivalent ounces at sub $1,200/oz AISC (benefiting from sub $900/oz AISC at Seguela).

However, much has changed over the past 18 months and while Yaramoko looked like it might maintain an 80,000 to 100,000-ounce production profile out to 2029 at the time of the acquisition, the updated five-year outlook is for just ~70,000 ounces at all-in sustaining costs closer to $1,500/oz (impacted by reserve deletions). Meanwhile, low-grade heap leach assets that move a considerable amount of material have been some of those hit the hardest by inflationary pressures sector-wide, and Lindero had a much higher-cost year in FY2022, with costs increasing to $1,142/oz, up from $1,116/oz in the year-ago period despite lower sustaining capital. However, the best years are behind the asset from a grade standpoint and recovery standpoint, and costs are expected to rise to ~$1,500/oz this year, placing a further dent in Fortuna's margins at its current operations, which we'll highlight a little later below:

As for full-year production, the company's two silver assets saw lower production on a year-over-year basis, with San Jose producing just ~5.76 million ounces of silver and ~34,100 ounces of gold, down from ~6.43 million ounces of silver and ~39,400 ounces of gold in FY2021. This was related to declining grades and recoveries at the mine. At Caylloma, silver grades were higher which helped the asset to report a 7% increase in silver production (~1.14 million ounces), but gold grades fell off a cliff (0.14 grams per tonne gold vs. 0.49 grams per tonne of gold), more than offsetting the increase in silver production with gold output sliding 90% to just 600 ounces. Zinc grades were also lower year-over-year but fortunately offset by higher zinc prices ($1.57/lb vs. $1.36/lb).

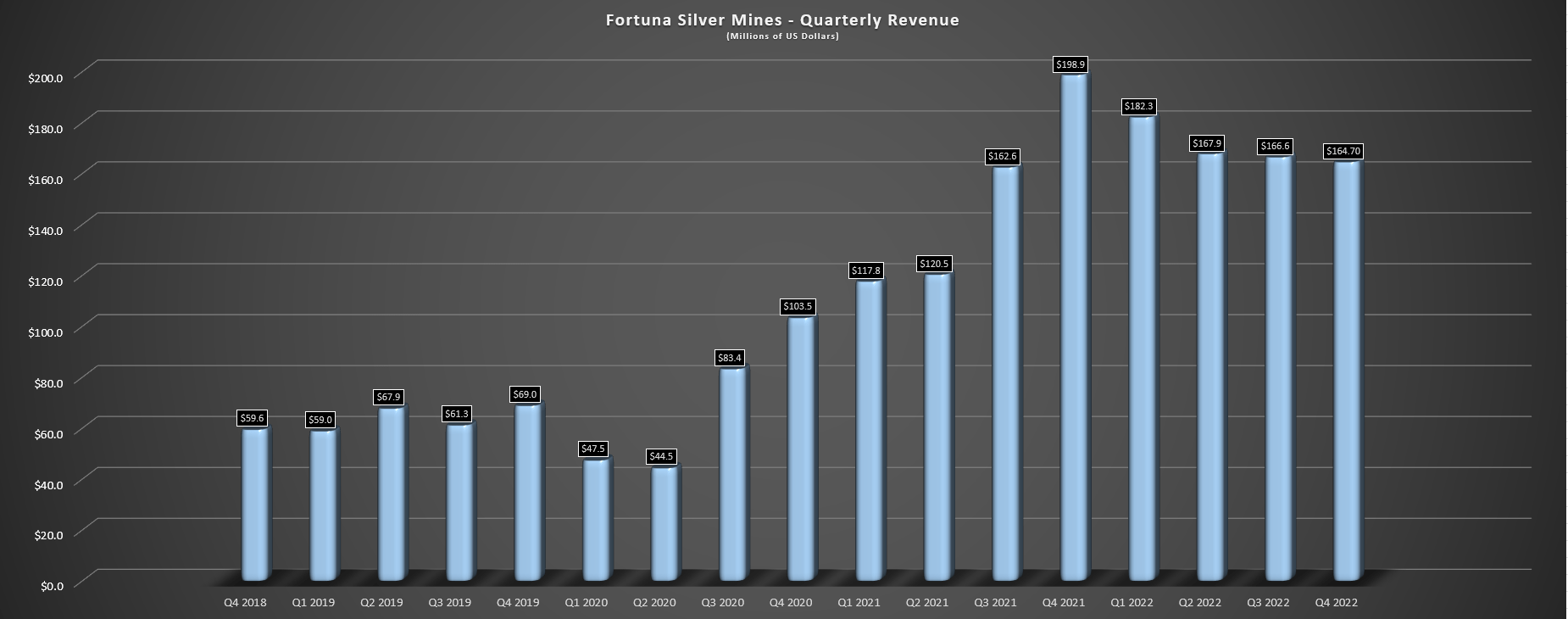

Fortuna Silver - Quarterly Revenue (Company Filings, Author's Chart)

{kind=link}

Based on the increase in gold sales with the addition of Yaramoko, revenue increased to ~$681.5 million for the year, a 14% increase from 2021 levels. This figure would have been much higher if not for the decline in metals prices, with this being the most pronounced in silver where the company's average realized metals price fell to sub $22.00/oz. However, while revenue increased substantially, we saw a decline in free cash flow to just $69.2 million (FY2021: ~$86.0 million) mostly related to increased capital expenditures and lower profitability due to the impact of inflationary pressures at its operations. In Q4, free cash flow came in at a paltry $4.4 million, a pretty depressing statistic for a company with four mines globally that's enjoying average realized gold prices near $1,750/oz, well within the upper portion of the metal's 10-year range.

While the production results were satisfactory and it's good to see Seguela nearing the finish line, this was overshadowed by significant impairments last year. In total, Fortuna reported impairment charges of $164.5 million in Q4 ($182.8 million before tax), with the bulk of this related to Yaramoko ($103.5 million pre-tax). Although this was already to be expected given the much higher cost profile at Yaramoko and the reserve deletion reported recently, we also saw impairments at San Jose and Lindero. At Lindero, we saw a $70.2 million impairment related to inflationary pressures on operating/capital costs and an increase in discount rates. At San Jose, we saw an $8.9 million impairment ($9.2 million pre-tax) related to inflationary pressures and exploration not fully replacing depletion. The result was that Fortuna reported a net loss of $135.9 million for the year.

Costs & Margins

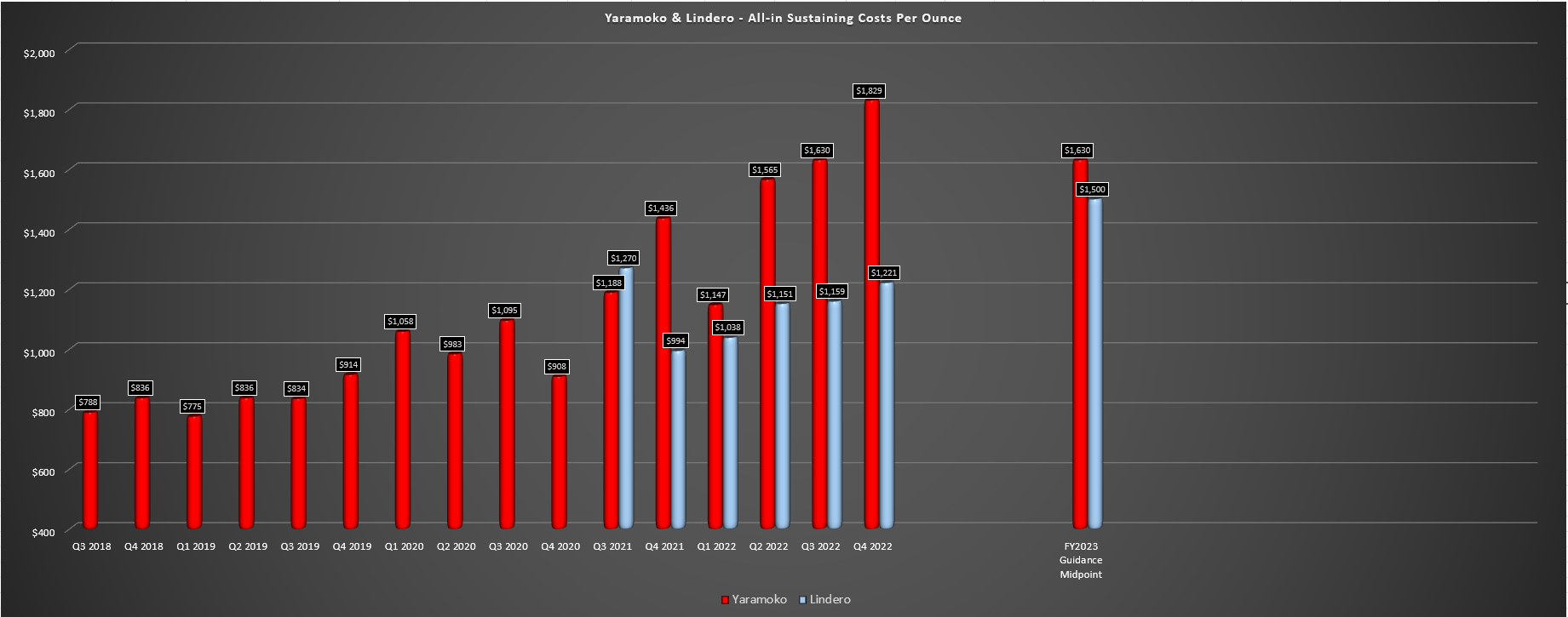

While the headline production results weren't terrible and showed growth, the 2023 outlook was disappointing as I highlighted in a recent update , and cost performance certainly left much to be desired. Looking at Fortuna's two gold assets, all-in sustaining costs ((AISC)) came in at $1,221/oz and $1,829/oz at Lindero and Yaramoko, respectively, impacted by higher sustaining capital at Yaramoko and lower sales volumes, leading to negative AISC margins of $87/oz in Q4 for the African mine. At Lindero, the combination of inflationary pressures and declining grades led to a considerable increase in costs of 23% year-over-year in Q4. On a full-year basis, the results weren't much better, with FY2022 AISC of $1,288/oz at Lindero and $1,529/oz at Yaramoko. As the chart below shows, this cost profile isn't expected to improve this year, putting further pressure on margins.

Yaramoko & Lindero - All-in Sustaining Costs Per Ounce (Company Filings, Author's Chart)

{kind=link}

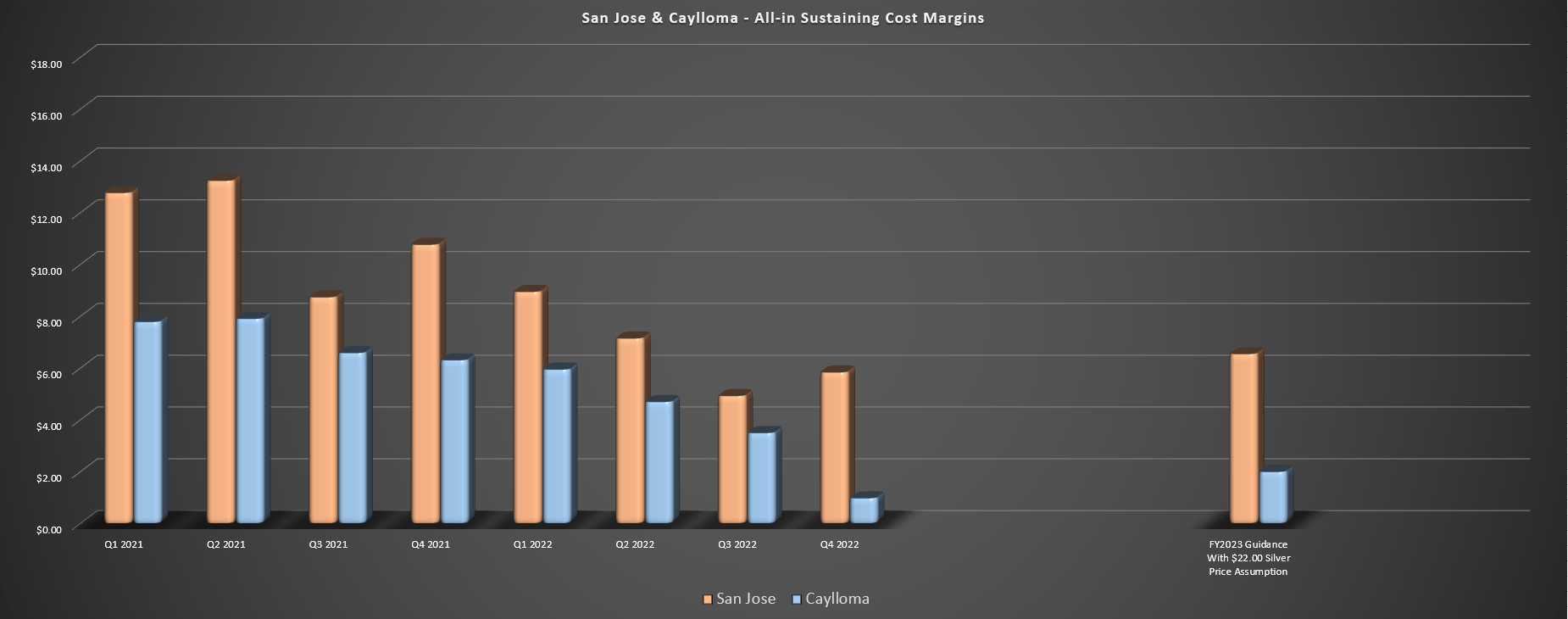

Moving to its silver assets, AISC increased to $15.53/oz at San Jose despite significantly lower sustaining capital ($3.7 million vs. $5.2 million), and on an adjusted basis (assuming flat sustaining capital), AISC would have come in well above $16.00/oz. For the full year, AISC increased to $15.11/oz from $14.38/oz, but costs are expected to increase again in FY2023 based on the guidance of $14.70/oz to $16.20/oz. Meanwhile, at Caylloma, the mine continues to report razor-thin margins, with Q4 AISC of $20.30/oz and FY2022 AISC of $17.97/oz. Although its annual AISC improved year-over-year, costs will rise to $20.00/oz at the mid-point in FY2023, meaning that Fortuna's gold and silver margin profile will worsen this year unless it gets help from metals prices.

San Jose/Caylloma - AISC Margins & FY2023 Outlook (Company Filings, Author's Chart)

{kind=link}

Finally, looking at margins for its silver business, there's nothing to get excited about here, with AISC margins for San Jose and Caylloma stuck in a steep downtrend over the past two years with only a brief relief from the attempted silver squeeze in 2023. Assuming an average realized silver-equivalent price of $22.00/oz in FY2023 and using the company's guidance mid-point provided in January, AISC margins per silver-equivalent ounce would shrink to $5.84/oz for San Jose and ~$1.00/oz for Caylloma, suggesting that if the recent rally in silver reserves, the company will be operating at or near its all-in cost and struggling to generate free cash flow from these assets.

Next, let's look at Fortuna's valuation to see whether this less ebullient outlook is priced into the stock.

Valuation

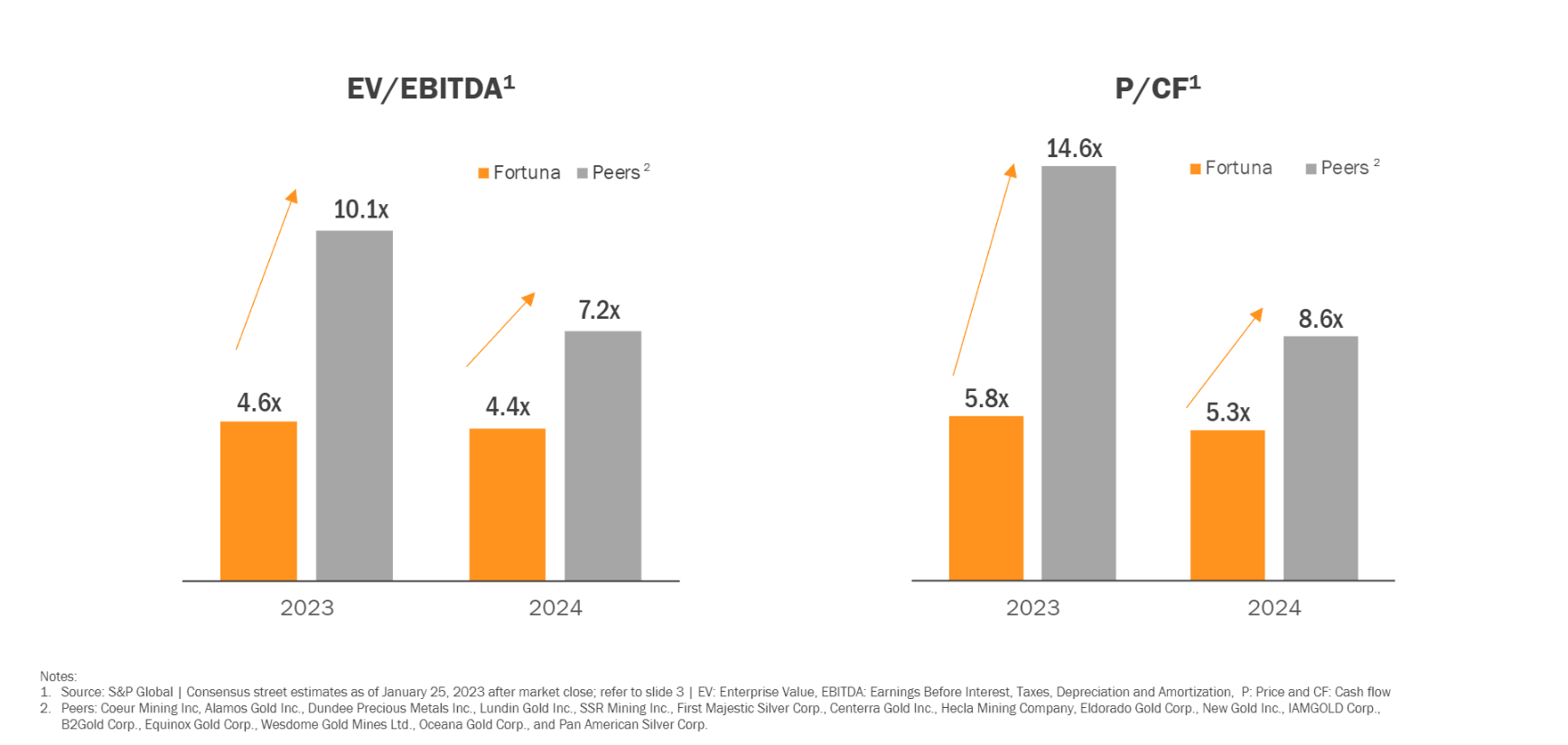

Scrolling through the company's presentation, one might conclude that Fortuna Silver Mines is undervalued, with the company highlighting that it trades at barely half the cash flow multiple of its peers. However, the company's peer group apparently includes Alamos Gold ( AGI ), Lundin Gold ( LUGDF ), and Hecla Mining ( HL ). Calling these companies relevant peers to Fortuna would be akin to calling Tom Brady, Aaron Rodgers, and Dan Marino relevant peers to JaMarcus Russell or Matt Leinart. The similarities aren't remotely there, and it's not even close. However, by placing these peers in its peer group, the cash flow multiple of the group to which Fortuna is being compared gets dragged higher given that these are elite companies with world-class assets (Fruta Del Norte, Island Gold, Greens Creek) and/or track records of impressive reserve replacement (Young-Davidson, Mulatos).

Fortuna Silver - Valuation Relative to Peers (Company Presentation)

{kind=link}

In Fortuna's case, a few glaring examples of its inferiority outside of the obvious is its poor reserve replacement, its lack of production from Tier-1 jurisdictions (Alamos has 80% of its production from Tier-1 jurisdictions, Hecla has 100% of production from Tier-1 jurisdictions), and its much higher cost profile vs. these peers. So, while the company has certainly done a great job of choosing some of its peers wisely to ensure it looks relatively undervalued, I don't see it as that undervalued at all. If we were to compare the company at all, I would argue it's a much lower-margin version of Perseus Mining ( PMNXF ), Endeavour Mining ( EDVMF ), or B2Gold ( BTG ) with a sprinkle of silver on top, and these companies all trade at less than 5x forward cash flow on average, but they're much higher margin, suggesting Fortuna should trade lower than this multiple given that its margins are inferior even with Seguela.

I have chosen these comparables as Fortuna will have five mines once Seguela online, which is like the group average and a mostly African production profile with ~50% of gold-equivalent production coming from West Africa and the rest of its production also coming from Tier-2/Tier-3 jurisdictions, like Peru, Mexico, and Argentina.

Based on ~294 million fully diluted shares and a share price of US$3.40, Fortuna trades at a market cap of $1.0 billion and an enterprise value of $1.14 billion. This leaves Fortuna trading at a premium to its estimated net asset value of ~$1.08 billion, which includes additional exploration upside assigned to Seguela, Boussoura, and Lindero ($200 million combined) and subtracting for ~$260 million in corporate G&A. If we place a 0.95x P/NAV multiple on the stock, which perhaps is generously given that it's actually above that of where larger African peers like Endeavour Mining plc ( EDVMF ) trade currently, I see a fair value for the stock of ~US$1.01 billion or US$3.45 per share. Hence, I see no upside in Fortuna Silver Mines Inc. stock from current levels to fair value.

Some investors will argue that this is an unfair assessment of fair value, but I would strongly disagree. Producers in Africa (whether it's fair or not) typically trade at a discount to net asset value to account for their jurisdictional risk sentiment towards Argentina (Lindero), Peru (Caylloma), and Mexico (San Jose). This has gotten no better over the past couple of years, nor has Fortuna's track record of reserve replacement at its main silver asset. So, with inflationary pressures and the Roxgold acquisition transforming Fortuna Silver from a silver producer with respectable costs (high premium) into a predominantly African gold producer with above-average operating costs (ex-Seguela), I believe the multiple compression is justified, and I see no reason the stock should trade in line with names like Hecla or others.

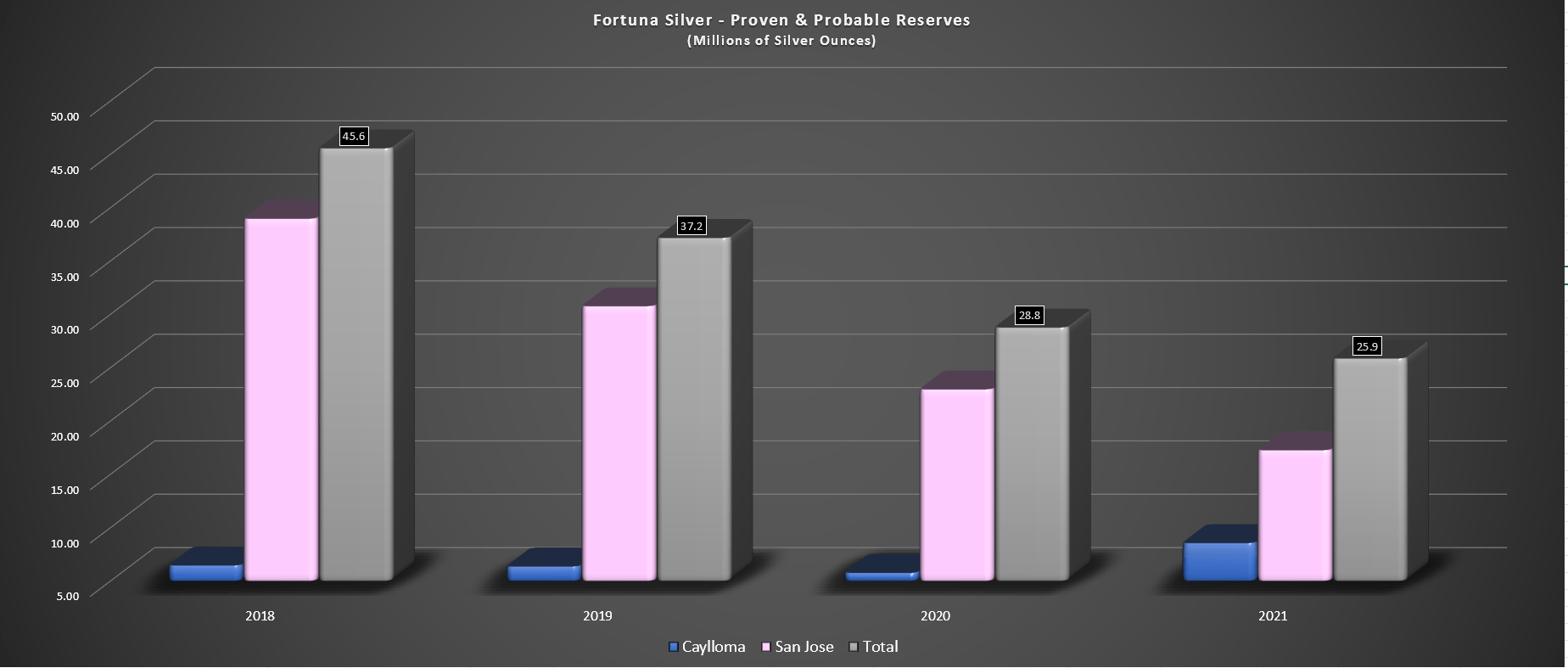

Fortuna Silver - Declining Reserve Profile - Silver Ounces (Company Filings, Author's Chart)

{kind=link}

Summary

Fortuna Silver Mines Inc. had another mediocre year in FY2022, with a satisfactory operational performance at its four mines and exploration success at Seguela being offset by impairments at three assets and rising costs across its portfolio. Worse, while the company has received a permanent injunction to Fortuna's Mexican subsidiary to operate interrupted under its 12-year EIA at San Jose despite SEMARNAT's pushback, I don't see the outlook improving in Mexico with permitting challenges for other companies, and hyper-inflation is hardly a positive development either at Lindero.

The silver lining is that Seguela is here to improve the portfolio with commercial production possible by late 2023, which will improve the company's margins. However, one can only place so much value on a single mine in a company's portfolio, especially when it's in a Tier-3 jurisdiction, regardless of its exceptional grades. Hence, while Seguela certainly helps Fortuna immensely, it isn't enough when I have a less optimistic view for other assets in its portfolio like San Jose and Yaramoko, and now we're seeing much higher costs at Lindero as inflationary pressures bite and grades decline. To summarize, I see far better ways to play the sector than Fortuna Silver Mines Inc., and I continue to believe rallies above US$4.00 will provide selling opportunities.

For further details see:

Fortuna Silver: Impairments And Rising Costs Overshadow Seguela Progress