FSM - Fortuna Silver: Limited Margin Of Safety At Current Levels

Summary

- Fortuna Silver is one of the best performing stocks since September, rallying nearly 100% off of its lows and now knocking on the door of the US$4.00 level.

- The company recently reported solid ounce additions at Sunbird and continues to see exploration success with regional drilling at Seguela, suggesting the potential for a larger operation here.

- However, most of this upside was already accounted for in my previous valuation, and with FSM trading at ~1.01x P/NAV, I see limited margin of safety at current levels.

- For this reason, I continue to maintain my view that further strength in the stock should provide an opportunity to book some profits.

It's been a solid few months for stocks in the silver space, with the Silver Miners Index ( SIL ) rallying 39% from its September lows, and Fortuna Silver ( FSM ) has been one of the outperformers with a 90% plus return. However, while its name may dictate that it is a silver producer, it derives a significant portion of gold revenue, which will be even more true once its Seguela Project comes online in mid-2023. Still, this outperformance can be attributed to the stock being hated in August/September and priced attractively, and the company's drilling success has helped to put a firm bid under the stock, with Seguela's resource base growing at a torrid pace. Let's take a closer look at recent developments below.

{kind=link}

Fortuna Silver Operations (Company Presentation)

More Ounces Added At Seguela

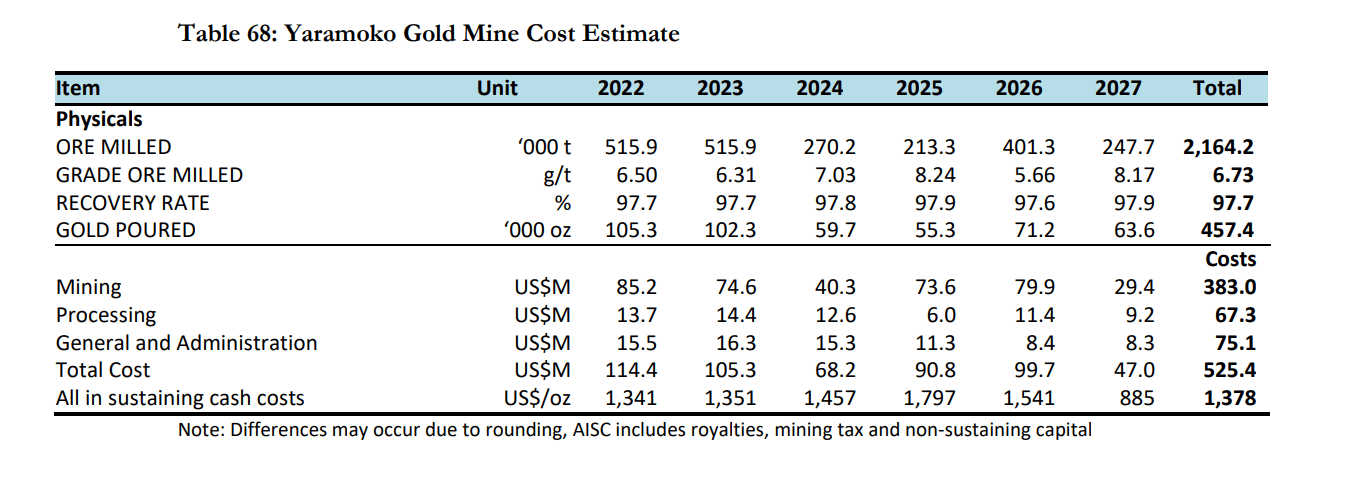

While Fortuna Silver may be best known for its San Jose Mine in Mexico and its polymetallic Caylloma Mine in Peru, which gave it leading silver exposure vs. its precious metals peers, the company has added several gold assets over the past year, including Lindero (Argentina), Yaramoko (Burkina Faso), and its nearly complete Seguela Project in Cote d'Ivoire. Lindero has continued to perform well, though costs have come in higher than expected due to inflationary pressures. Meanwhile, Yaramoko has been a disappointment with an updated mine plan that leaves much to be desired. However, the real reason for paying to acquire Roxgold was Seguela, a phenomenal project that continues to churn out new high-grade discoveries.

{kind=link}

Yaramoko Mine Plan (Company Presentation)

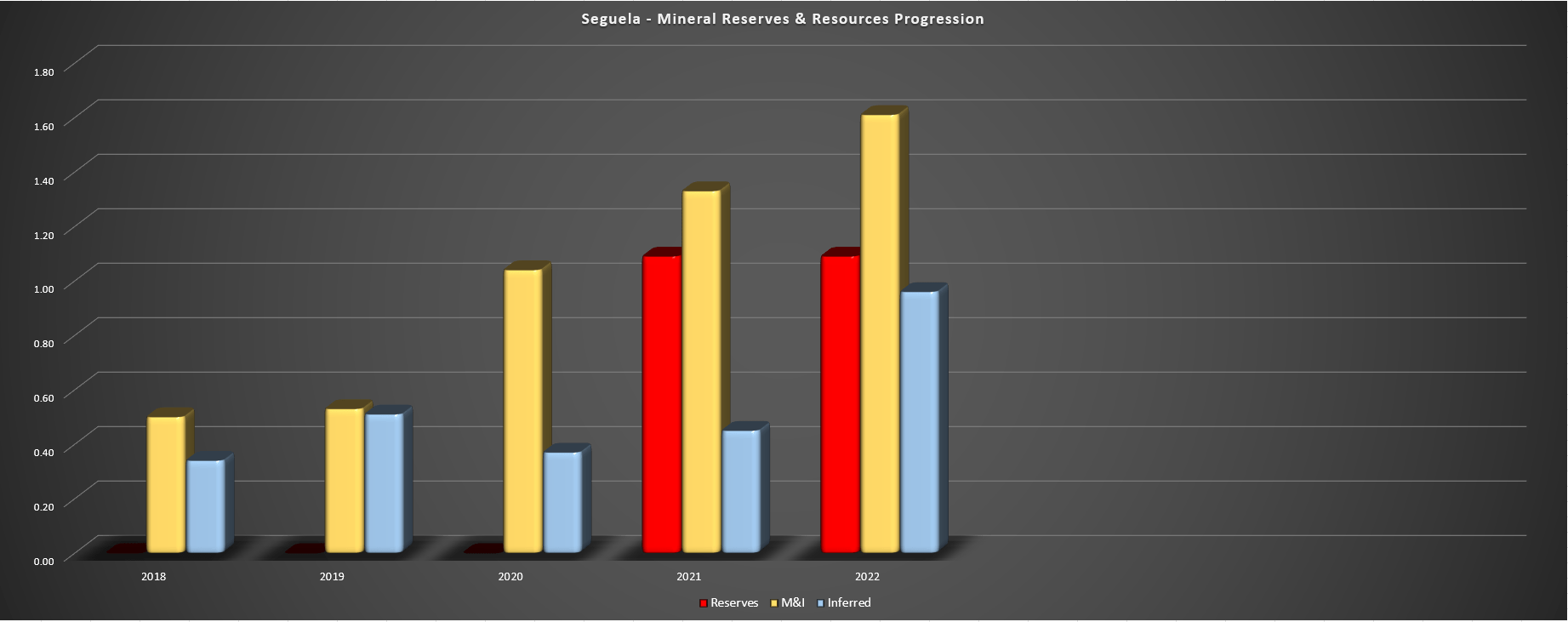

For those unfamiliar, the project was acquired for a song ($20 million + $10 million contingent payment) from Newcrest ( OTCPK:NCMGF ), and Roxgold parlayed this into a $500+ million valuation in barely 30 months, at least based on what Fortuna was willing to pay to acquire Roxgold. The chart below shows the progression in resources and reserves at the project. As we can see below, the most recent ounce addition at Sunbird suggests this could end up being a 2.5+ million-ounce reserve base eventually, given the consistent resource growth. As it stands, resources have grown from ~840,000 ounces in 2019 to ~2.57 million ounces, but with several deposits open, this could turn into 3.50+ million ounces of resources with more drilling.

Reserves are shown inclusive of M&I resources.

{kind=link}

Seguela - Mineral Resources & Reserves Progression (Company Filings, Author's Chart)

Digging into the most recent resource update a little closer, Fortuna reported a significant increase in resources at high-grade deposit to ~785,000 ounces (including 279,000 ounces in the indicated category), up from just 350,000 ounces in the solely inferred category previously. While the indicated grades were a little lower than I expected and are in line with the mine plan reserve grade (~2.8 grams per tonne of gold), we could see a lift in grades if inferred ounces can be successfully converted, and this is certainly a nice addition to the mine plan. The result will be a boost to NPV (5%) at the Seguela Project and potentially a larger boost if these ounces are pulled forward or if the company looks at a mill expansion to ~1.6+ million tonnes per annum.

{kind=link}

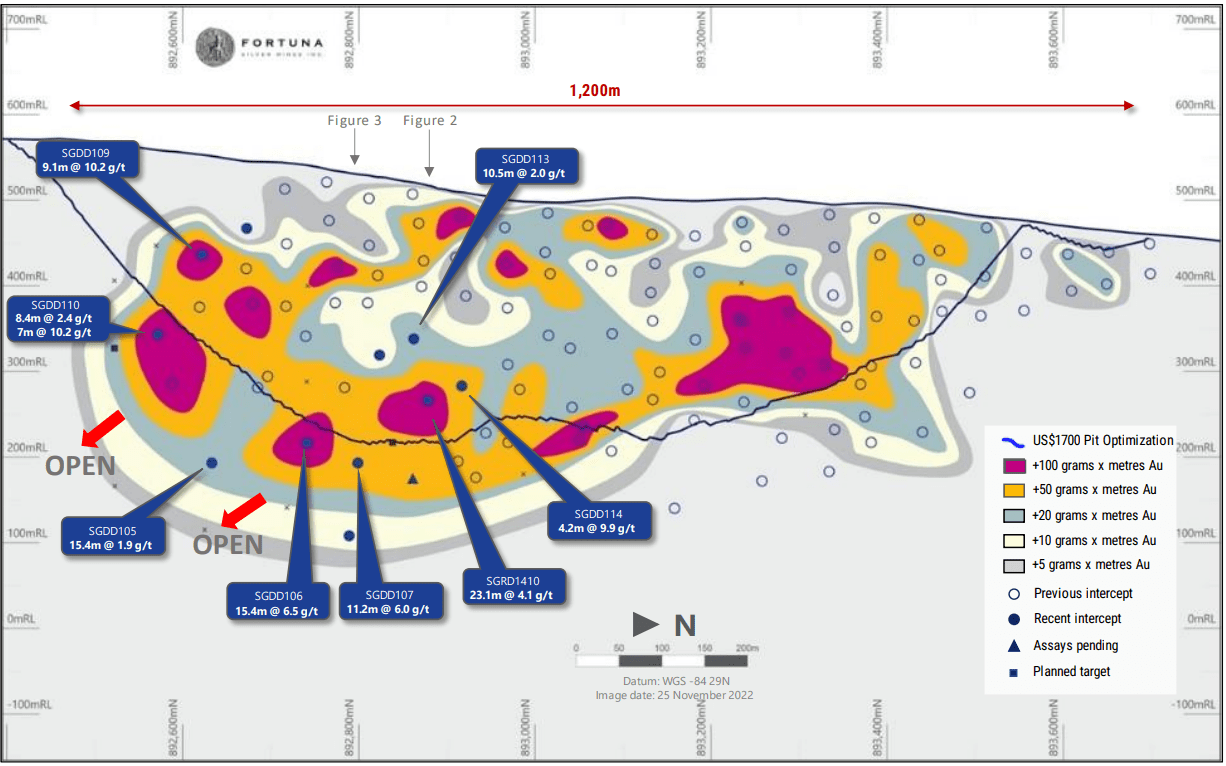

Seguela Project Drilling & Updated Resource Pit (Company Website)

The positive takeaways from the updated resource were that drilling confirmed the continuity of mineralization between the southern and central high-grade shoots, and the high-grade southern shoot continues to extend to the south, with a new intercept of 9.1 meters at 10.2 grams per tonne of gold. Meanwhile, the increased likelihood that the two main high-grade shoots are part of a continuous lode with a 700+ meter strike length (initially being modeled as separate) has increased the underground potential at Sunbird.

For now, we can see that grades certainly remain attractive at depth, with multiple hits, including 11.2 meters at 6.0 grams per tonne of gold, 2.1 meters at 11.0 grams per tonne of gold, 11.2 meters at 4.3 grams per tonne of gold, 6.3 meters at 13.6 grams per tonne of gold, and 15.4 meters at 6.5 grams per tonne of gold. Overall, I see this update as very positive for Fortuna, and it's beginning to justify the rich price that the company paid for Roxgold ($880 million), even when factoring in the benefit of using expensive currency (FSM shares) to get the deal done. That said, I was already assigning $150 million in exploration upside to Seguela, so this hasn't changed my price target for the stock.

Seguela Regional Upside

While the meaningful growth at Sunbird is exciting, it's worth noting that Fortuna continues to have exploration success from a regional standpoint, with high-grade hits from Kestrel (south of Antenna deposit) released in September and two new opportunities to the north also showing solid grades. In terms of Kestrel, recent highlight hits include 5.8 meters at 4.2 grams per tonne of gold, 3.5 meters at 20.3 grams per tonne of gold, which are in addition to 2.8 meters at 24.0 grams per tonne of gold, and 1.4 meters at 14.3 grams per tonne of gold released in September. Fortuna noted that it had defined a 200-meter strike to date with a high-grade core hosted in the same lithological package as Koula, Sunbird, and Ancien, the company's three highest-grade deposits at Seguela.

Seguela Regional Targets (Company Website)

Meanwhile, Fortuna released some solid results from Badior, which is nearly 10 kilometers north of Koula, with the following highlight holes:

- 15.4 meters at 11.5 grams per tonne of gold

- 8.4 meters at 12.0 grams per tonne of gold

- 9.1 meters at 4.2 grams per tonne of gold

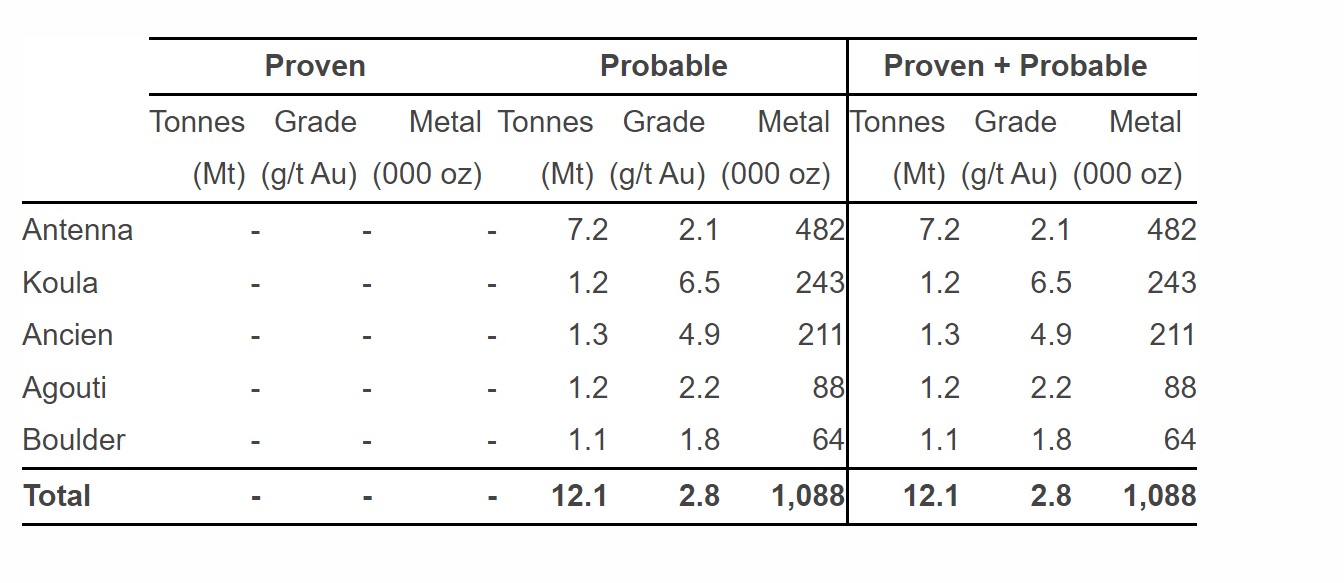

These are exceptional intercepts and a very nice start to drilling in a potential future satellite pit in what could ultimately be multiple pits within the near vicinity of the plant and a larger area feeding its central processing facilities. Fortuna noted that Badior has similar alteration and mineralization to its Antenna deposit, which currently hosts nearly 40% of Seguela's reserves (482,000 ounces at 2.1 grams per tonne of gold). In addition, Fortuna reported decent intercepts from Barana, which is a little further north, intersecting 5.6 meters at 2.3 grams per tonne of gold and 4.9 meters at 4.1 grams per tonne of gold.

{kind=link}

Seguela Reserves (Company Website)

Given that there are significant sunk costs here with associated infrastructure and plant that will be operational and processing ore by August of this year, any new low to mid-grade discoveries within close proximity still offers a nice upside to add onto the back end of the mine life or potentially feed a larger plant. However, it's certainly encouraging that the grades at the project appear to be consistently above 1.5 grams per tonne of gold or better. Let's dig into the valuation below and see whether the stock is a Buy following its recent exploration success and resource growth.

Valuation & Technical Picture

Based on ~294 million fully diluted shares and a share price of US$3.90, Fortuna trades at a market cap of $1.15 billion and an enterprise value of $1.25 billion. This leaves the stock trading at a premium to its estimated net asset value of ~$1.14 billion, which includes additional exploration upside assigned to Seguela, Boussoura, and Lindero ($200 million combined) and an adjustment for ~$360 million in corporate G&A. However, this assumes that one believes a mid-tier producer in Tier-2 and Tier-3 jurisdictions that has two operations with a history of poor reserve replacement (Yaramoko, San Jose) should trade at 1.0x P/NAV. I would argue that this is a rich multiple.

{kind=link}

Fortuna Silver - Year-to-date Corporate G&A (Company Filings)

In fact, Endeavour Mining ( OTCQX:EDVMF ) regularly trades at below 1.0x P/NAV, and it is a much larger producer with a similar jurisdictional profile (Africa-focused), a superior pipeline, and much higher margins. So, if we use a more conservative multiple of 0.95x P/NAV to reflect Fortuna being a Tier-2/Tier-3 jurisdiction gold producer regardless of its name (silver represents only a fraction of revenue), Fortuna's fair value would decline to $1.06 billion or US$3.61 per share. Obviously, stocks can trade well above fair value, and in this sector, they often overshoot to both the upside and downside. Still, I've never found any value in paying a premium to net asset value unless it is truly an exceptional story like KL Gold in the 2016-2019 period, so I don't see any way to justify chasing the stock here at US$3.90.

{kind=link}

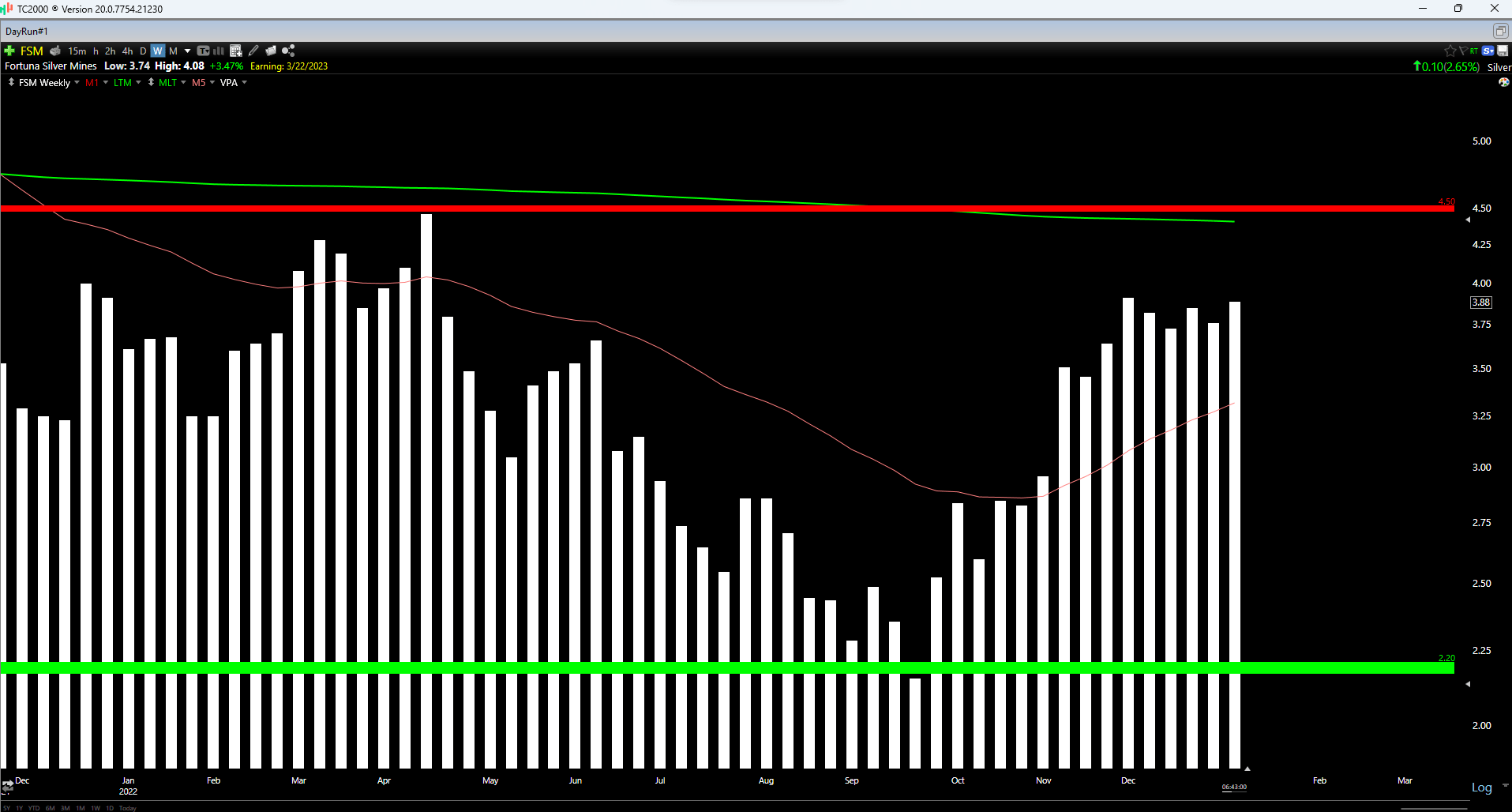

FSM Weekly Chart (TC2000.com)

Moving to the technical picture, Fortuna is currently in the upper portion of its expected trading range, with strong support at $2.40 and strong resistance overhead at $4.50. I typically prefer a minimum 5.0 to 1.0 reward/risk ratio to justify starting new positions in small-cap names. With $0.60 in potential upside to resistance and $1.50 in potential downside to support, the current reward/risk ratio comes in at 0.40 to 1.0, miles away from the ideal ratio to start a new position. This corroborates the view that Fortuna is nowhere near a low-risk buy zone and that any further strength in the stock would provide an opportunity to book some profits.

Summary

Fortuna Silver continues to enjoy consistent exploration success at Seguela, and I see this as an incredible project that could ultimately boast an NPV (5%) north of $500 million for its 90% interest (2021 Report: $380 million before inflationary pressures). However, the rest of the portfolio leaves much to be desired, with the exception of Lindero, with two short mine-life assets, and Caylloma, which doesn't move the needle. Besides, Lindero's best years will be behind it by 2024, and the costs in the Technical Report remain far too ambitious, given the impact of inflationary pressures.

{kind=link}

Lindero Mine Production Schedule (Company Technical Report)

{kind=link}

Fortuna Silver Update - August 2022 (Seeking Alpha Premium/Pro)

Some investors will argue that Seguela will result in a significant re-rating in the stock, but I don't see that being the case when the stock is heading into its first gold pour (summer 2023) trading at a premium to its net asset value. Instead, the time to be more open-minded to owning the stock to play this re-rating potential was below US$2.30, where I noted that too much negativity was priced in already. To summarize, I don't see any way to justify chasing FSM here regardless of the solid ounce additions at Sunbird, and if I were long the stock, I would view further strength above US$3.90 as an opportunity to begin to scale out of my position.

For further details see:

Fortuna Silver: Limited Margin Of Safety At Current Levels