FSM - Fortuna Silver Mines: A Disappointing 2023 Outlook

Summary

- Fortuna Silver released its FY2022 production results last month, reporting quarterly production of ~259,400 ounces of gold and ~6.91 million ounces of silver.

- This translated to a 25% increase in gold production year-over-year and an 8% decline in silver production, with higher gold production attributed to the successful ramp-up at Lindero.

- However, the 2023 outlook leaves much to be desired, and the recent reserve deletion at Yaramoko added insult to injury, with increased cut-off grades not making reserve replacement any easier.

- With the stock offering limited margin of safety at US$3.75 after a more than 80% rally off its lows, I don't see any way to justify paying up for the stock here.

It's been a better few months for Fortuna Silver Mines ( FSM ) shareholders, with the stock rebounding more than 80% off its September lows following a brutal 18-month bear market. However, while the company met its 2022 guidance and the outlook at Seguela continues to improve, it's hard to argue the same for other assets. Not only have inflationary pressures severely impacted margin expectations at Lindero, but we've now seen a second reserve deletion at Yaramoko, giving the company two short-life assets that are struggling to replace reserves (Yaramoko & San Jose). Worse, although San Jose is still operating without disruption, permitting continues to be a headache for the Mexican asset.

Fortuna Silver Mines Article - August 2022 (Seeking Alpha Premium/Pro)

{kind=link}

As discussed in August of last year, much of this negativity (short mine lives at two assets, inflationary pressures impacting margins, San Jose permitting uncertainty) was priced into the stock below US$2.60, and pullbacks below US$2.30 were likely to provide buying opportunities. However, with the share price 65% higher than this ideal buy zone, there is no longer an adequate margin of safety to adjust for these risks, and I would not consider the stock cheap at more than 1.0x P/NAV as a high-cost producer in Tier-2/Tier-3 jurisdictions. Let's take a closer look at the FY2023 outlook and recent developments below:

Fortuna Silver Operations (Company Website)

{kind=link}

Q4 Results & FY2022 Results

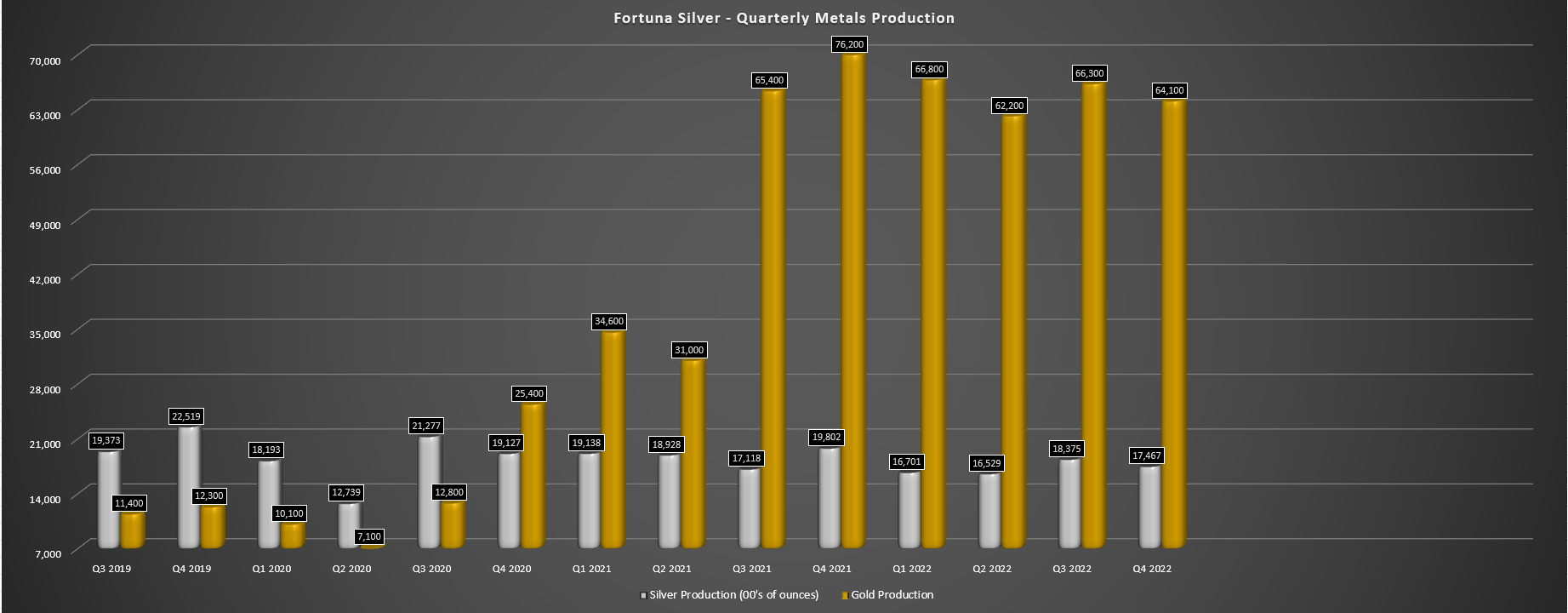

Fortuna Silver Mines ("Fortuna") released its Q4 and FY2022 production results last month, reporting annual production of ~259,400 ounces of gold and ~6.91 million ounces of silver. This translated to a 25% increase in gold production year-over-year and an 8% decline in silver production, with higher gold production attributed to the successful ramp-up of its Lindero Mine in Argentina. While silver production came at the top end of guidance, gold production was slightly below the guidance mid-point of ~262,000 (FY2022: ~259,400 ounces). Although it will increase next year, with Seguela set for a mid-2023 gold pour, we will see lower production at Lindero and Yaramoko due to declining grades.

Fortuna Silver - Quarterly Metals Production (Company Filings, Author's Chart)

{kind=link}

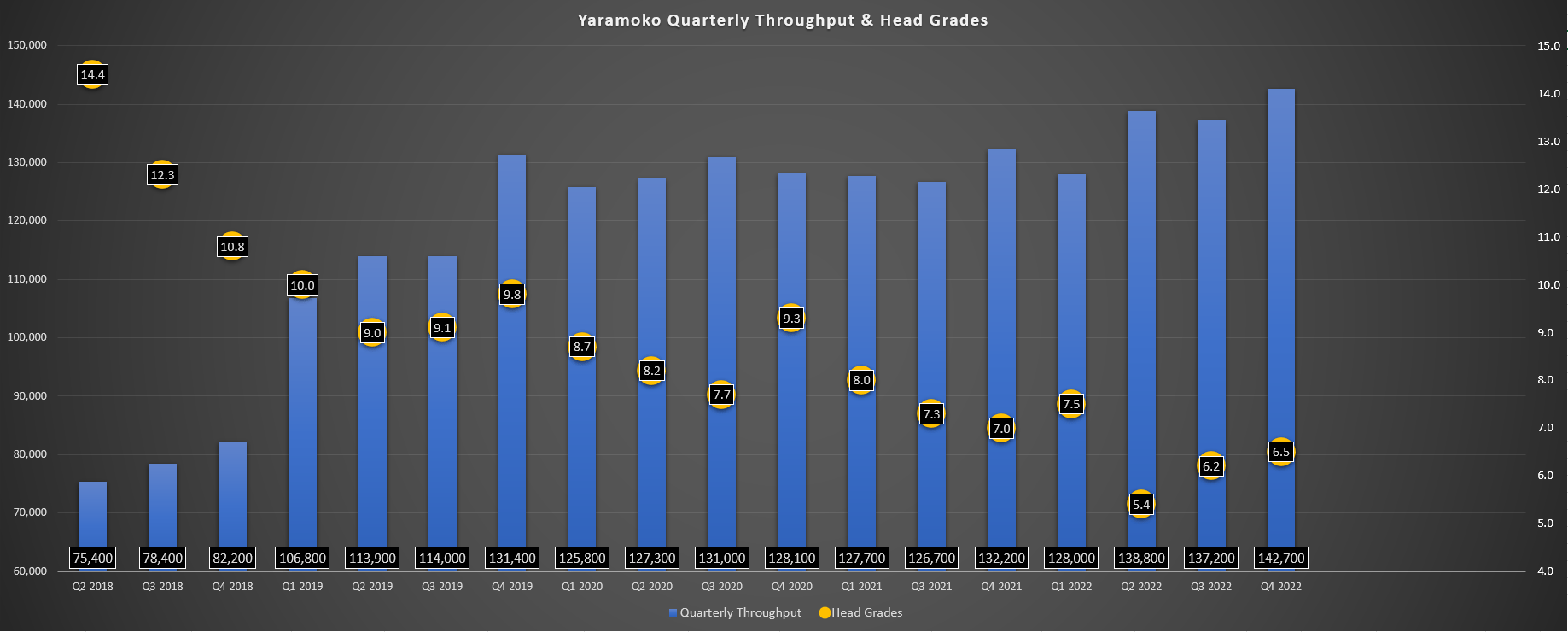

Digging into Fortuna's Q4 results, we can see that gold production came in at ~64,100 ounces, a 16% decline year-over-year, impacted by lower grades at Lindero, San Jose, and Yaramoko, plus lower gold production at Caylloma. In Lindero's case, the asset did meet its production guidance mid-point of 121,100 ounces (FY2022 production: ~118,400 ounces), but its other operations did meet or deliver into their annual guidance. Plus, while Yaramoko did meet guidance of 105,000 ounces (~106,100 ounces), we continue to see a trend of declining grades that is only partially offset by increased throughput, with further grade declines expected this year.

Yaramoko - Quarterly Throughput & Head Grades (Company Filings, Author's Chart)

{kind=link}

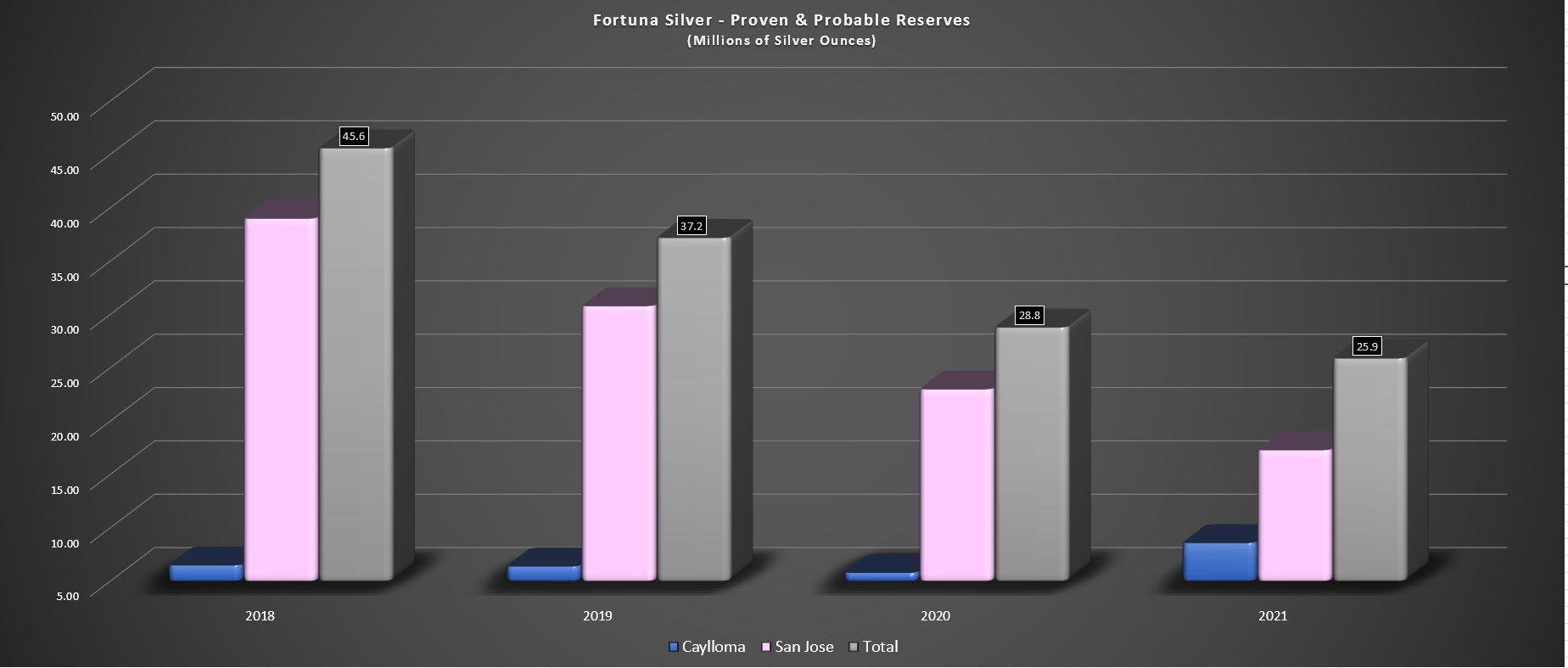

Unfortunately, we're seeing a similar trend for Fortuna's primary silver asset (San Jose), with a steady decline in silver production at this asset, with the production of ~1.47 million ounces of silver in Q4 2022. This compares unfavorably to ~2.0 million ounces in Q4 2019 and ~1.72 million ounces in the same period last year, impacted by an ability to replace reserves and a declining grade profile for these reserves. The result is a much less robust asset with a smaller production profile and much higher costs, especially when combined with inflationary pressures that have driven up per-tonne costs at the mine relative to pre-COVID-19 levels.

San Jose - Proven & Probable Silver Reserves (Company Filings, Author's Chart)

{kind=link}

As the chart above shows, the mine has a poor track record of replacing reserves to date, and this was before another year of double-digit inflation sector-wide that will likely drive up cut-off grades at this asset. This accelerated rate of change in per tonne costs due to elevated inflation could make reserve replacement more difficult, and the asset already has an uncertain future due to continued permitting headaches. For those that missed it, Fortuna received written notice of a resolution issued by the Secretaria de Medio Ambiente y Recursos Naturales (SEMARNAT), noting that SEMARNAT is re-assessing the 12-year Environmental Impact Authorization [EIA] assessment for San Jose, that it granted to Minera Cuzcatlan (100% owned subsidiary of Fortuna) in December 2021.

This follows a previous hiccup in late 2021, with SEMARANT suggesting that it had made a typographical error and that the correct term for the extension was two years, not 12 years. While this was solved in November 2022 with the Mexican Federal Administrative Court ruling in favor of Fortuna and re-confirming the 12-year EIA extension, we now have added uncertainty here, which management believes to be unfounded and is understandably a headache. Many investors might argue that this issue will be resolved, there's no disruption to operations to date, and it's immaterial to the investment thesis. While I would agree it's not that significant (given that San Jose represents less than 1/4 of Fortuna's total NPV [5%]), the belief that this is the sole reason for Fortuna's underperformance is incorrect, which I'll discuss below:

2023 Outlook

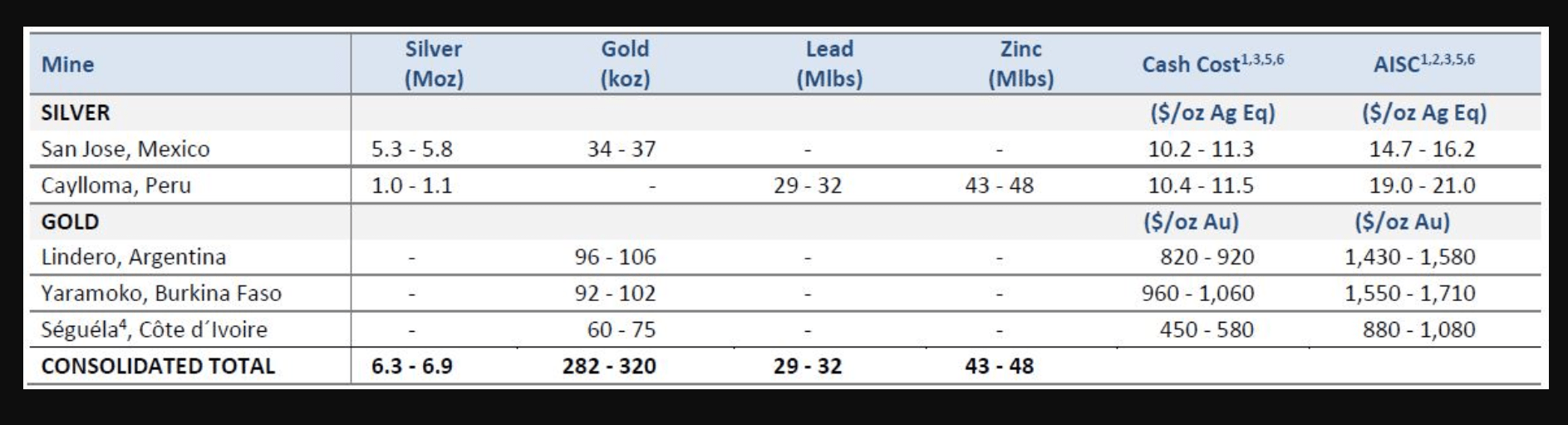

Although Fortuna met its FY2022 guidance of 262,000 ounces of gold and ~6.5 million ounces of silver, the company's 2023 outlook provided last month left much to be desired. For starters, silver production is expected to decline again year-over-year to ~6.6 million ounces of silver after lapping an 8% decline last year. Worse, costs are expected to come in at $20.00/oz at Caylloma and $15.45/oz at San Jose based on the mid-point out of guidance, meaning Fortuna will need silver prices to stay above $20.00/oz to generate any meaningful free cash flow at its primary silver asset. This is a significant cost increase from pre-COVID-19 levels, with FY2019 all-in-sustaining costs [AISC[ of $9.80/oz.

Fortuna Silver - 2023 Guidance (Company Website)

{kind=link}

If we look at the gold business, the outlook is much weaker for its two existing gold assets, and costs are expected to soar at Lindero due to declining grades and elevated sustaining capital. I warned about this in my previous update and stated the following in regards to why it made little sense to chase Fortuna above US$3.90:

"However, the rest of the portfolio leaves much to be desired, except Lindero, with two short mine-life assets, and Caylloma, which doesn't move the needle. Besides, Lindero's best years will be behind it by 2024, and the costs in the Technical Report remain far too ambitious, given the impact of inflationary pressures."

Lindero Mine Plan (Technical Report)

{kind=link}

Digging into Lindero specifically, the mine is expected to produce 96,000 to 106,000 ounces at all-in-sustaining costs of $1,430/oz to $1,580/oz. This is a massive decline from ~118,400 ounces produced in FY2022 and can be attributed to lower grades as the highest-grade ore has been mined with grades averaging less than 0.67 grams per tonne gold over the remainder of the mine life (FY2022 average grade: 0.81 grams per tonne gold). Although these are still respectable grades for a heap-leach operation, the combination of inflationary pressures (diesel, explosives, reagents), ~16% lower grades, and increased sustaining capital will put a severe dent in margins year-over-year.

Given that this was the breadwinner for Fortuna in 2022 ($33 million in operating income in the first nine months of 2022), the sharp increase in costs is not ideal. In fact, AISC is set to increase 41% over 2022 at the top end of guidance, while cash costs will rise 25% at the upper end of guidance. The good news is that some of this is temporary due to the Phase II leach pad expansion and elevated stripping costs. However, with sub 0.65 gram per tonne grades going forward (post-2024) and the impact of higher fuel and consumables costs, the days of this being a sub $1,100/oz AISC operation appear to be a distant memory.

Yaramoko Mine Plan (December 2021 Technical Report)

{kind=link}

Moving over to Yaramoko, the cost profile here isn't any better, with the recently released mine plan guiding for FY2023 production of ~102,300 ounces at $1,351/oz and Fortuna's guidance differing materially, with the production of 92,000 to 102,000 ounces at AISC of $1,550/oz to $1,710/oz. Even if the company were to hit the high end of production and low end of cost guidance, this would still be below the previous outlook at much higher costs ($1,550/oz vs. $1,350/oz). The lower production can be partially attributed to grades, with the 2021 Technical Report calling for an average grade of 6.3 grams per tonne of gold and ~516,000 tonnes processed and Fortuna's 2023 plan sitting at ~526,100 tonnes processed at just 5.9 grams per tonne of gold.

Adding insult to injury (at Yaramoko), the company's previous plan was to build an open pit at the 55 Zone based on extracting high-grade ore that formed the crown pillar by mining remnant mineralization adjacent to existing mine workings and additional sub-parallel structures. However, upon further inspection and further evaluation of the mineralization, Fortuna has identified a spatial discrepancy attributed to a surveying error that occurred prior to Q3 2020, resulting in "horizontal differences averaging from 2 to 3 meters between the drill holes used to define the 55 Zone main mineralization structured and the underground channel samples collected during underground development".

Unfortunately, the result is that after correcting for this inconsistency, we've seen an overestimation of 120,000 ounces of modeled remnant mineralized material. Worse, we've seen an additional 46,000-ounce deletion that cannot be economically extracted due to this ore being lower-grade and relatively isolated. Although we will see a lower strip ratio under the updated plans for mining the 55 Zone crown pillar, the mine life has decreased to three years from five years. As it stands, Yaramoko's reserves now sit at just 1.40 million tonnes at 5.80 grams per tonne of gold, representing ~264,000 ounces of gold (vs. ~464,000 ounces at 5.8 grams per tonne of gold previously).

Worse, although future exploration success could extend the mine life, cut-off grades have risen sharply due to inflationary pressures. This is evidenced by underground mining costs being estimated at ~$135/tonne vs. ~$102/tonne previously and processing costs increasing to ~$31/tonne vs. ~$28/tonne. Given the higher cut-off grade, 3.0 to 4.0 grams per tonne underground material will no longer suffice at 55 Zone Underground and Bagassi South Underground for material expected to be mined using sub-level stoping. Meanwhile, even at Bagassi South QV Prime, which can be mined via shrinkage stopping, cut-off grades have increased slightly to 3.1 grams per tonne of gold. To summarize, reserve replacement with a higher hurdle for material to be economical.

So, what does this all mean?

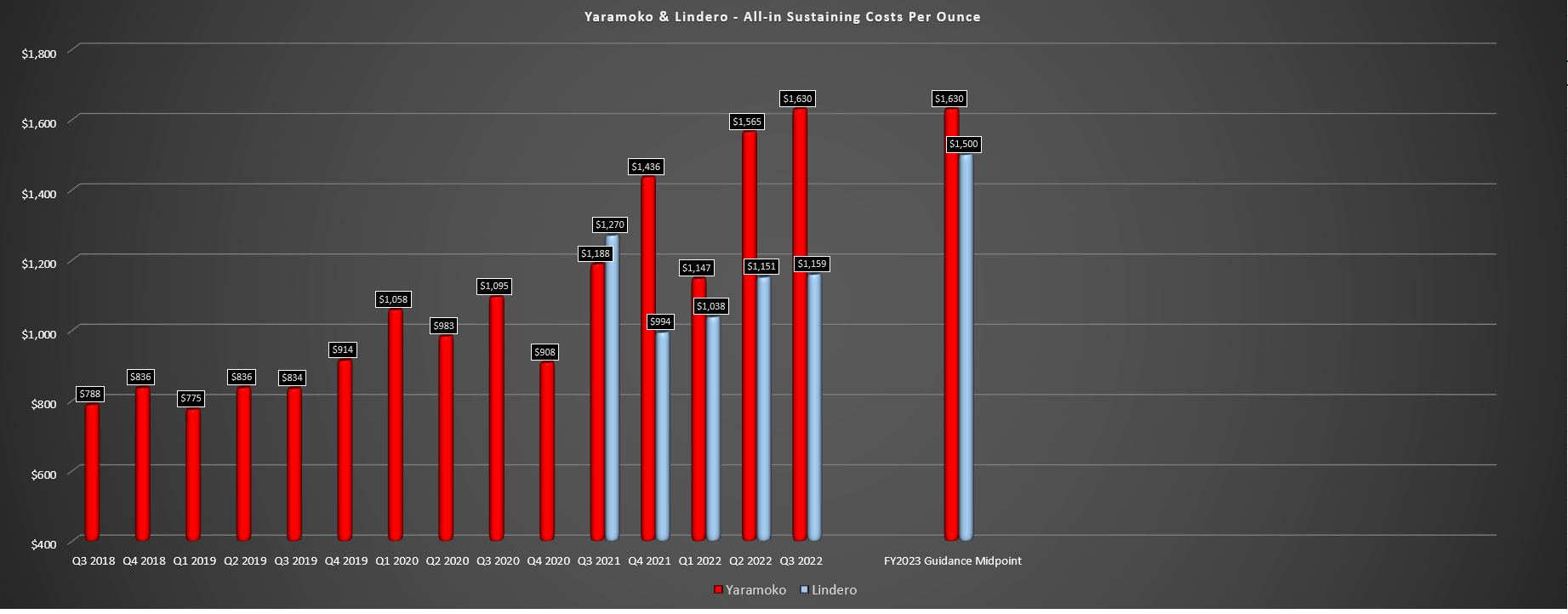

Aside from the fact that I'm even less optimistic about San Jose and Yaramoko continuing to remain in production by the end of this decade due to higher cut-off grades and already short mine lives, the costs at these assets are expected to rise considerably year-over-year based on Fortuna's FY2023 guidance mid-point. So, while Lindero was previously the bright spot to drag down the company's consolidated costs, we are now entering 2023 with much higher costs at Lindero, even higher costs at Yaramoko, and costs remaining elevated at its two silver assets in Mexico and Peru. The only silver lining is that Seguela is less than six months from its first gold pour and will be a high-margin operation.

Yaramoko & Lindero - Quarterly AISC & FY2023 Guidance (Company Filings, Author's Chart, Company Guidance)

{kind=link}

That said, while Seguela coming online is great news, and this is expected to be a cash-flow machine in 2024 with sub $900/oz AISC, the negative is that we won't see as meaningful of a production growth rate as I previously anticipated under the assumption that Yaramoko and Lindero would combine for a consistent ~200,000 ounces per annum until 2030, and Seguela would add an incremental 130,000+ ounces. This view was based on the assumption that if Fortuna was going to pay $800+ million for Roxgold, it wasn't paying that price strictly for Seguela and that Yaramoko had a bright future ahead that wasn't yet reflected in the current mine plan. In fact, the company stated in the acquisition release:

"Yaramoko and Séguéla are low-cost assets with low technical complexity contributing meaningfully to growth while reducing overall AISC".

- Fortuna Silver Mines, Press Release April 2021

While both assets may have low technical complexity, the resources were clearly overstated at Yaramoko. Plus, Yaramoko has done nothing to reduce overall AISC, with AISC near $1,500/oz in FY2022, above Fortuna's consolidated average. Hence, although Seguela will increase overall gold production and should contribute a minimum of 60,000 ounces this year and 125,000+ ounces in FY2024, this will be offset by much lower production at Yaramoko and Lindero. Hence, the margin improvement will not be as significant as previously expected on a consolidated basis due to the severe impact of inflationary pressures on Fortuna's existing operations.

So, while Fortuna previously looked like it could become a ~350,000-ounce gold producer (including San Jose's gold contribution) with an additional 7.0+ million ounces of silver by 2025 at sub $1,100/oz costs, the updated outlook appears to be a ~310,000-ounce producer at AISC above $1,250/oz (blended AISC of Lindero, Yaramoko, Seguela post-2024), with barely 6.0 million ounces of silver production. So, when we combine the company's relatively low margins for its silver business and AISC in line with the industry average for its gold business, Fortuna will be an average cost producer at best until Yaramoko is offline or unless we see a material increase in throughput at Seguela to help pull down consolidated margins.

Valuation

Based on ~294 million fully diluted shares and a share price of US$3.75, Fortuna trades at a market cap of $1.10 billion and an enterprise value of $1.22 billion. This places the stock at a premium to its estimated net asset value of ~$1.09 billion, which includes additional exploration upside assigned to Seguela, Boussoura, and Lindero ($200 million combined) and an adjustment for ~$260 million in corporate G&A. However, this assumes that one believes the appropriate multiple for a mid-tier producer in Tier-2 and Tier-3 jurisdictions (Mexico, Argentina, Burkina Faso, Cote d'Ivoire) that has two operations with a history of poor reserve replacement (Yaramoko, San Jose) is 1.0x P/NAV. I believe this to be a generous multiple.

Fortuna - Year-To-Date Corporate G&A (Company Filings)

{kind=link}

Using a more conservative multiple of 0.95x P/NAV to reflect its elevated jurisdictional risk and poor reserve replacement at two assets offset by a slight premium for silver exposure, I see a fair value for Fortuna of ~$1.02 billion or US$3.50 per share. Hence, I see the stock as fully valued at current levels using conservative metals price assumptions, and given that the gold price can be difficult to predict and inflationary pressures could continue to pressure margins (and also make reserve replacement more difficult), I believe it makes sense to be conservative from a commodity assumption standpoint.

Summary

While Fortuna continues to be a favorite among many investors, the adoration for the stock at these levels is a little puzzling, with it continuing to be a high-cost producer in less favorable jurisdictions trading at a premium to its net asset value. The fact that the company appears to have paid far too much for Yaramoko, given reserve deletions, doesn't help the story, and due to inflationary pressures, replacing reserves at this short mine life asset won't get any easier. In fact, underground cut-off grades have increased to 4.1 grams per tonne of gold (55 Zone Underground and Bagassi South - sub-level stoping) and 3.1 grams per tonne of gold at Bagassi South QV Prime (shrinkage stoping) vs. 3.4 and 3.0 grams per tonne of gold, respectively due to higher underground mining and processing costs.

Some investors will argue that Seguela is a game-changer for the company, and I agree. Still, there's only so much value one can assign to a medium-scale high-margin operation when it's located in a Tier-3 jurisdiction. This is because other predominantly African gold producers also have exceptional assets, such as Fekola, Lafigue, Sabodala-Massawa. Still, we don't see these companies commanding premium valuations with a discount due to their jurisdictional risk. Besides, Seguela is simply offsetting Fortuna's high costs and giving it a more respectable cost profile; it's not a case like Alamos ( AGI ), where it's going from being an average-cost producer to one of the highest-margin producers sector-wide due to Island Phase III.

Seguela Project (Company Website)

{kind=link}

The fact that Fortuna is a high-cost producer with two short mine life assets that have struggled to replace reserves doesn't mean that the stock can't go higher. Still, I see no way to justify paying up for the stock above US$3.70 given that the key is to buy sector leaders at a deep discount to fair value, and Fortuna is neither a sector leader nor is it trading at a deep discount to fair value. So, as noted in my previous update , I would view any rallies above US$4.00 as profit-taking opportunities. To summarize, I continue to see far more attractive bets elsewhere in the sector, and I see FSM as an Avoid at current levels with zero margin of safety baked into the stock here.

For further details see:

Fortuna Silver Mines: A Disappointing 2023 Outlook