FVI:CC - Fortuna Silver: More Share Dilution But A Decent Deal For Diamba Sud

2023-06-07 09:19:50 ET

Summary

- Fortuna Silver Mines is set to acquire Chesser Resources, reinforcing its position as a future West African gold producer.

- The acquisition includes Chesser's flagship Diamba Sud project in eastern Senegal, which has a resource of 860,000 ounces of gold.

- The deal is accretive on a NAV basis, and Fortuna has added over 3,600 square kilometers of land in West Africa with its past two deals.

2023 is shaping up to be a very busy year from an M&A standpoint, with B2Gold ( BTG ) acquiring Sabina Gold & Silver, Gold Fields ( GFI ) coming in for a half interest in Osisko's (OBNNF) Windfall Project , and SSR Mining ( SSRM ) announcing that it would acquire up to a 40% interest in the Hod Maden Project. However, among smaller producers, we've also seen quite a few deals, with one of the most recent ones being Fortuna Silver's ( FSM ) proposed acquisition of Chesser Resources (CESSF) (CHZ.ASX), an Australia producer with a large land package and mid-grade gold project in eastern Senegal. This acquisition has reinforced Fortuna's position as a future West African gold producer, a major-evolution from an Americas-focused silver producer last decade. Let's dig into the deal below and if this changes the forward outlook:

All figures are in United States Dollars unless otherwise noted

{kind=link}

Proposed Acquisition Of Chesser Resources

Fortuna Silver ("Fortuna") announced last month that it would be acquiring Chesser Resources ("Chesser"), with Chesser shareholders set to receive 0.0248 of a Fortuna share for each Chesser share held, translating to ~5.1% share dilution for Fortuna (~15.5 million shares), or a value of A$0.142 for each Chesser share (US$59 million in value at a 0.66 AUD/USD exchange rate). This deal comes just after the two-year anniversary of Fortuna's proposed acquisition of Chesser of Roxgold, which was successful, which added a development project (Seguela) in Cote D'Ivoire and a producing mine and exploration asset in Burkina Faso (Yaramoko and Boussara). And while Fortuna arguably paid up for Roxgold with the deal valued at nearly $900 million, it benefited from using cheap currency (expensive FSM shares), making the price paid more reasonable.

As for Fortuna's report card of acquiring assets, the Lindero Mine turned out to be a solid deal at an attractive price even if construction of the Argentinian gold mine went severely over budget. Meanwhile, Fortuna deserves an A [+] for its acquisition of Seguela as part of the Roxgold deal given the continued exploration success, but a D [-] for Yaramoko, which has not lived up to expectations, struggled to replace reserves, and saw a material reserve deletion that resulted in a shortened mine life than expected. So, on a blended basis, I would give the Roxgold transaction a rating of B [-] given that Seguela outperformed and has since recorded its first gold pour while Yaramoko will be a drag on margins for the rest of its mine life (reasons for reduction in mine life at Yaramoko discussed below) and may not remain in production past 2026.

55 Zone open pit: decrease of 26 percent or 120,000 ounces due to a reduction of remnant mineralized material related to a survey discrepancy identified in the historical model that was corrected in the updated resource model evaluation.

55 Zone open pit: decrease of 10 percent or 46,000 ounces due to changes in pit size as material at depth cannot be economically extracted from surface due to increased strip ratios as a result of the depletion of the aforementioned remnant material.

- Fortuna Updated Reserve & Resource Evaluation Work, January 27th, 2023

So, what's the newest Chesser Resources acquisition look like?

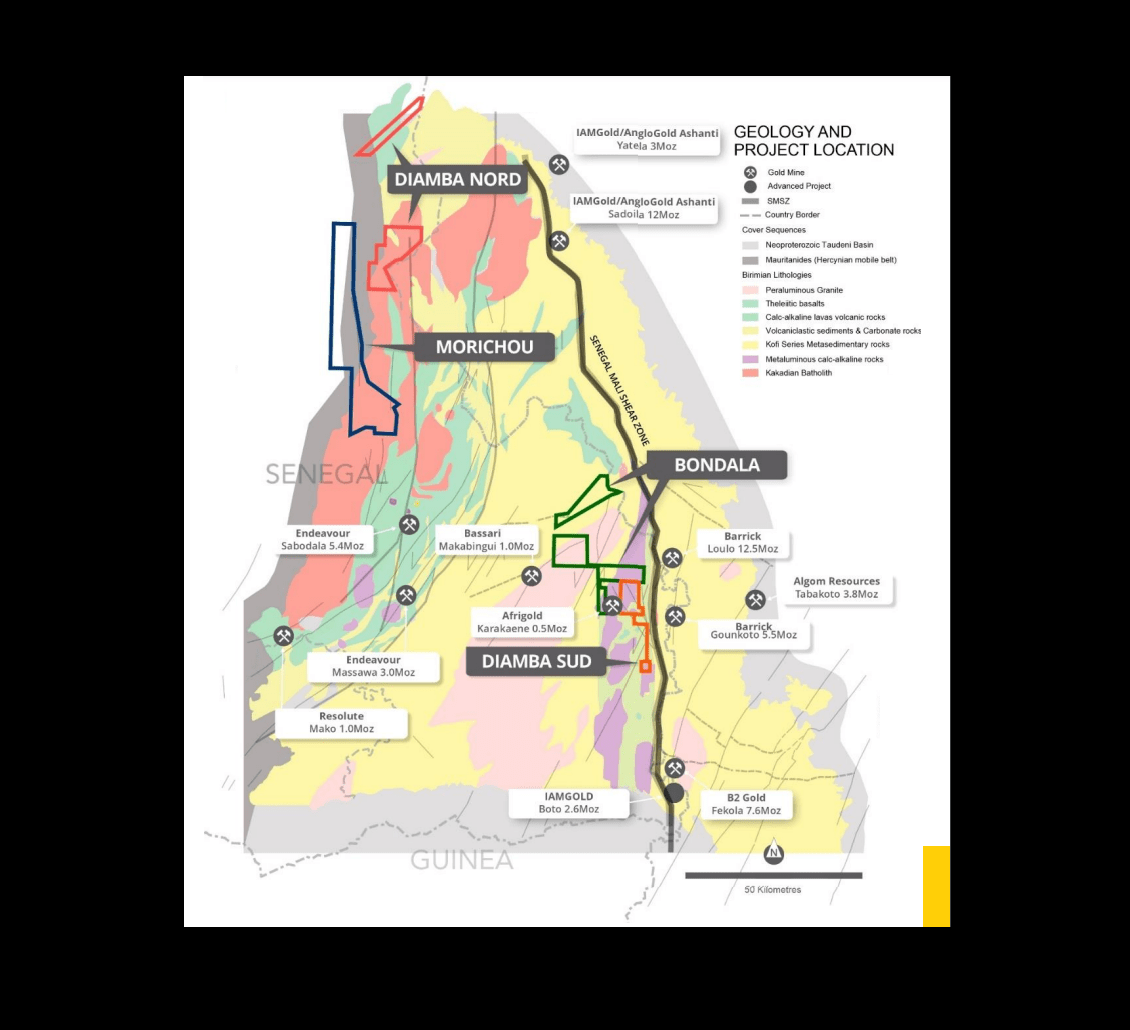

Diamba Sub Project

While the diversification into two new countries in West Africa in 2021 (Burkina Faso, Cote D'Ivoire) was a meaningful departure from its Americas-focused portfolio previously (Peru, Argentina, Mexico), the recent deal is continuing this trend of focusing on asset quality vs. keeping its sights solely in the Americas, with Chesser's flagship project being Diamba Sud, a mid-grade asset amenable to open-pit mining in eastern Senegal (five kilometers east of town of Gamba). Notably, this asset is in elephant country for gold deposits and surrounded by mammoth-sized mines, with Barrick's ( GOLD ) Loulo-Gounkoto Complex less than 10 kilometers away across the Mali/Senegal border, and B2Gold's Fekola Mine lying to the southwest, also along the Mai border and the Senegal Mali Shear Zone. Meanwhile, just 80 kilometers west is Endeavour's flagship asset, Massawa, which is part of its Sabodala-Massawa Complex which is currently under expansion (construction of BIOX plant to process high-grade refractory ore from Massawa).

{kind=link}

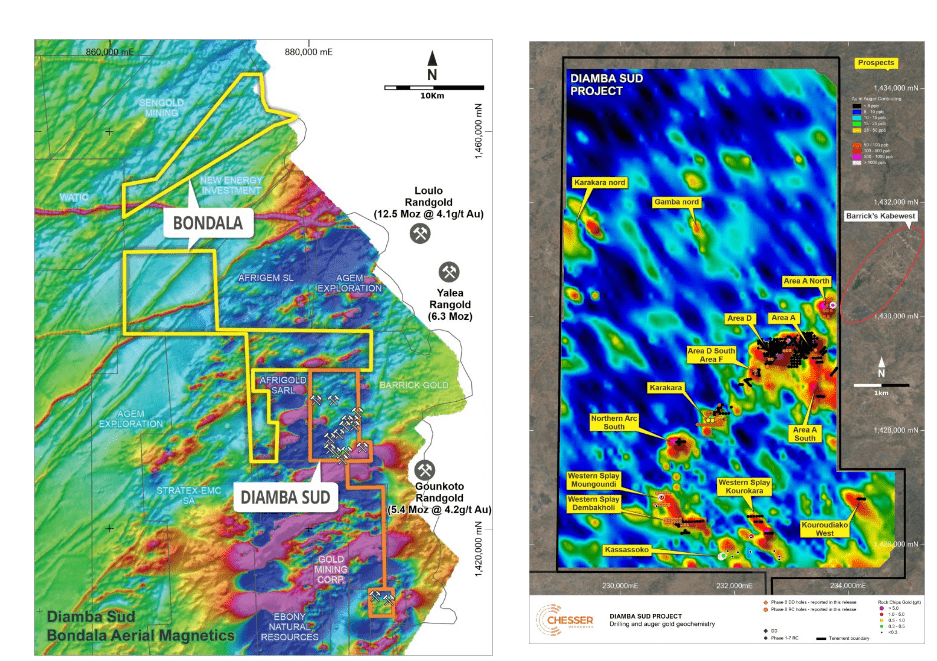

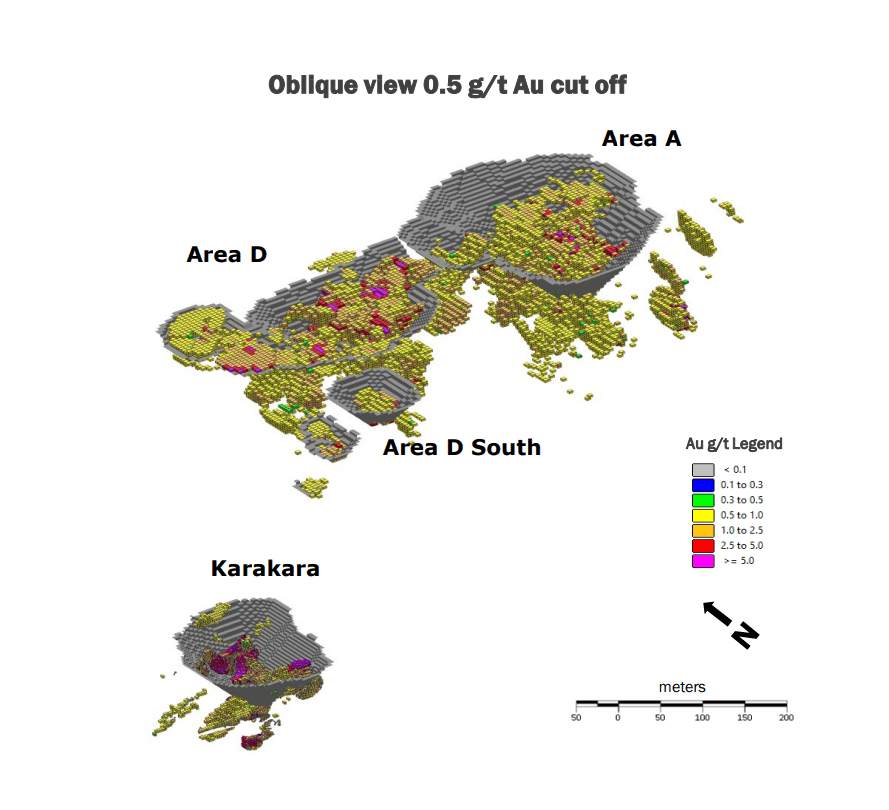

Just being near monster gold deposits isn't always enough since there's no guarantee that this will translate to a multi-million ounce discovery on a nearby project. However, Chesser has made solid progress over the past years at Diamba Sud, outlining a resource of 860,000 ounces (73% indicated category) at ~1.80 grams per tonne of gold, with the bulk of this resource based on two pits, known as Area A and Area D. Plus, Fortuna has secured a massive land package along the highly prospective Senegal Mali Shear Zone, with 872 square kilometers of tenements held by Chesser. Just as importantly, the project appears to have straight-forward metallurgy with 95% recoveries for oxide material and 93-95% recovery for fresh rock, and a relatively low strip ratio of 4.2 to 1.0.

{kind=link}

Looking at a scoping study completed by Chesser last year, the company envisioned building a 2.0 million tonne per annum CIL plant to process material, with multiple pits, with the two most productive pits being Area A and Area D (combined resource of 692,000 ounces). The expectation was that the asset would produce 715,000 ounces over a 7.5 year mine life (average of ~95,300 ounces per annum on average), but with much higher production in the first two years of ~111,500 ounces. Upfront capex to build the project was relatively modest at $149 million which is easily manageable for a company of Fortuna's size (~$1.10 billion), and the estimated After-Tax NPV (5%) came in at $296 million at an $1,800/oz gold price, translating to an attractive After-Tax NPV (5%) to Initial Capex ratio of 1.99 to 1.0.

Chesser Resources Land Package & Gold Geochem (Chesser Resources)

{kind=link}

In regards to exploration upside, this is an exciting asset similar to Seguela, with the core deposits looking like they can support a 100,000+ ounce per annum production over 8 years, but several targets in a close vicinity, and opportunity to add ounces near-mine. For starters, Area D is open to the west, northeast, and at depth, and the company has barely scratched the surface at Bougouda, a target to the south with two parallel quartz veins with extensive artisanal workings. Meanwhile, the company has made a new discovery five kilometers southwest of Area A at the Western Splay target, with highlight intercepts including 18 meters at 2.1 grams per tonne of gold, 16 meters at 1.9 grams per tonne of gold, 16 meters at 2.8 grams per tonne of gold, and 22 meters at 2.1 grams per tonne of gold.

Finally, given that Chesser was a smaller company, we've seen limited drilling outside of the main resource areas, but two new prospects recently highlighted solid results, with these being Gamba Gamba Nord (7 meters at 6.2 grams per tonne of gold from 60 meters), Kassaassoko (35.0 meters at 1.4 grams per tonne of gold from surface), and mineralization has been extended at Karakara and Area D South. Finally, this doesn't even include the other large land package separate from Diamba Sub which is Bondala, which is less than 20 kilometers away and long-term potential. Hence, while the current stands at 860,000 ounces, I ultimately would not be surprised to see a 1.70 million ounce resource base proven up, or a 1.20 million ounce reserve base at a slightly lower average grade of 1.60 grams per tonne of gold.

Resource Base & Conceptual Pits (Fortuna Presentation, Chesser)

{kind=link}

Given that I wouldn't expect production to start until Q1 2027 earliest and I would not be surprised to see a change in scope (2.4+ million tonnes per annum vs. 2.0 million tonnes per annum) to increase production to 120,000+ ounces per annum, plus the fact that scoping studies/PEAs are historically quite loose on their assumptions, I believe a more realistic initial capex estimate is $215 million ( Fetekro at ~3.0 million tonnes per annum [CIP/gravity] in PFS stage was estimated at $338 million prior to inflationary pressures albeit with a higher strip ratio and a 50% larger plant size). That said, this is still a very reasonable build cost for a company of Fortuna's size and there would be some offset from an NPV basis as the larger plant would push out an extra 25,000+ ounces per annum.

Obviously, it's early to model this asset, but assuming 24 million tonnes of reserves are proven up and taking into account a Q3 2026 build start, a Q1 2028 first gold pour and low single-digit inflation per annum, I believe a reasonable assumption for an NPV (5%) figure at $1,800/oz gold is $200 million. A reserve base of this size would support a 10-year mine life at 2.4 million tonnes per annum with an average production profile of ~120,000 ounces (1.6 grams per tonne of gold at ~94.5% recovery) at sub $1,070/oz all-in sustaining costs (adjusted for inflationary pressures). This would represent a very solid asset, and while not as robust as Seguela, it would help to pull down Fortuna's costs and make it a more competitive producer relative to other West African peers like Perseus Mining ( OTCPK:PMNXF ), Orezone ( OTCQX:ORZCF ), and Endeavour ( OTCQX:EDVMF ).

Acquisition Price

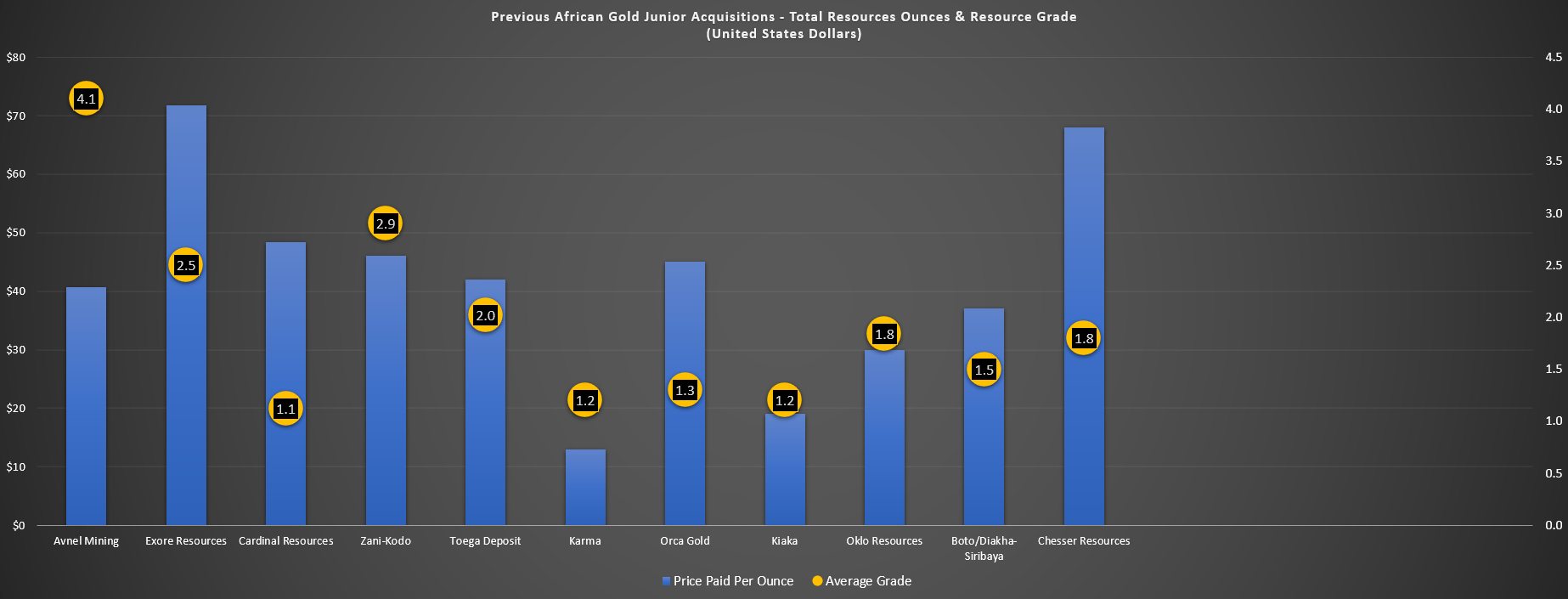

If we look at a sample of gold juniors (excludes producers) and projects/mines purchased in Africa since 2017, we can see that the average price paid was ~$40.00/oz, while the average grade of these projects/mines was ~1.90 grams per tonne of gold. In Chesser's case, Fortuna is paying ~$59 million to scoop up 860,000 ounces at 1.80 grams per tonne of gold, translating to a resource grade slightly below the average and a price paid per ounce that's 71% above the average of this sample group (~$69/oz vs. $40/oz). Hence, from a headline standpoint, an argument could be made that peers did better from a price paid standpoint, especially given that many of these deals benefited from synergies (resources were near a flagship mine/plant with the Toega acquisition and the Oklo Resources acquisition, meaning there was no need to build a stand-alone facility to process this material, a huge benefit that translates to a lower total acquisition cost per ounce.

Sample Of African Gold Junior/Project Acquisitions - Total Resource Grade & Price Paid Per Ounce (M&I+I) (Company Filings, Author's Chart)

{kind=link}

However, while Fortuna may have paid more than peers on a per ounce basis, I don't think is an unreasonable price to take over Chesser. Plus, the deal is certainly accretive on a NAV basis, with an NPV (5%) of ~$200 million ($1,800/oz gold) for Diamba Sud even under more conservative assumptions (adjusting for inflationary pressures), which translates to a near 17% increase in company-wide net asset value in an exchange for just ~5.1% share dilution. Therefore, I see this as a solid deal, and Fortuna has now added over 3,600 square kilometers of land in West Africa with its past two deals, including ~350 square kilometers at the now producing Seguela Project, and ~870 square kilometers with the Chesser Resources deal). And like Seguela, Diamba Sud looks to have several nearby deposits that could complement its existing 860,000 ounce resource base.

Valuation

Based on an estimated ~310 million fully diluted shares (post-Chesser acquisition) and a share price of US$3.55, Fortuna trades at a market cap of ~$1.10 billion and an enterprise value of ~$1.26 billion. If we compare this figure to an estimated net asset value of ~$1.43 billion (~$200 million assigned to Diamba Sud), this leaves Fortuna trading at 0.77x P/NAV, a slight discount to its peer group of mid-tier producers. However, as I've discussed extensively in past updates, Fortuna's more relevant peer group is not all mid-tier producers, but West African gold producers (which typically trade at much higher discounts), with the two closest examples being Perseus Mining and Endeavour Mining. The reason for my view that these are the closest peers for Fortuna is that its San Jose Mine has a short mine life and the investment landscape is less favorable in Mexico, Lindero's production is declining as grades normalize, and its two largest assets post-2027 will be Diamba Sud (up to 150,000 ounces in first two years), and Seguela (~140,000 ounces per annum).

{kind=link}

Currently, both Endeavour and Perseus trade at less than 0.90x P/NAV, but they are lower-cost producers, with both companies having sub $975/oz all-in sustaining costs vs. Fortuna's cost profile north of $1,200/oz plus. And if we compare Perseus Mining to Fortuna, given that their production profiles are more similar, Perseus trades at an enterprise value of just ~$1.18 billion despite having a much stronger balance sheet (~$480 million in net cash vs. ~$160 million in net debt for Fortuna), a similar production profile of ~450,000 ounces, but a project (Block 14) that could push its production to ~600,000 ounces per annum by 2026. Hence, Perseus is the larger producer with a stronger balance sheet, the lower-cost producer, it generates more cash flow ($300 million in FY2022 vs. ~$210 million for Fortuna), and it pays a dividend, and it can be purchased at the same valuation today.

For those that argue that Fortuna is cheap on a price to cash flow basis, Endeavour Mining and Perseus Mining trade at an average of 4.2x EV/CF, so they're actually cheaper than Fortuna Silver despite being peers of higher-quality that are more shareholder friendly (better balance sheets, paying dividends and or buying back shares + higher-margin assets).

Given that both companies trade at similar valuations, I struggle to side with arguments for Fortuna is undervalued relative to its peer group, unless one has purposely chosen to use the most favorable peer group possible, which is low-cost Tier-1 jurisdiction producers. This is not what Fortuna Silver is today under any stretch of the imagination, and we could make an argument that with the struggles Fortuna is having at San Jose (Mexico) plus the recent mining reforms and the security issues in Burkina Faso that its three best jurisdictions are Cote D'Ivoire, Senegal, and Peru, with none ranking in the top 30 jurisdictions globally. So, using what I believe to be a fair multiple of 0.90x P/NAV, I see an updated fair value of US$4.05 for FSM (14% upside from current levels). And given that I want a minimum 30% discount to fair value to justify buying mid-tier producers, FSM is nowhere near its implied low-risk buy zone of US$2.84.

Summary

Fortuna Silver's recent acquisition of Chesser Resources (if successful) was a solid move, adding nearly ~3,000 square kilometers of prospective land in a highly productive gold district surrounded by producing mines. And while I believe the company paid full price for Roxgold (especially considering that Yaramoko wasn't as robust as expected), they paid a more reasonable price for Diamba Sud, especially if this resource can grow to 1.5+ million ounces. That said, and as I've highlighted in past updates, although this deal is accretive from a NAV standpoint, I would expect multiple compression to continue, with this deal putting Fortuna on a path to be a West African gold producer, not an Americas-focused silver producer like it was last decade, and African gold producers typically trade at less than 0.90x P/NAV even with industry-leading margins.

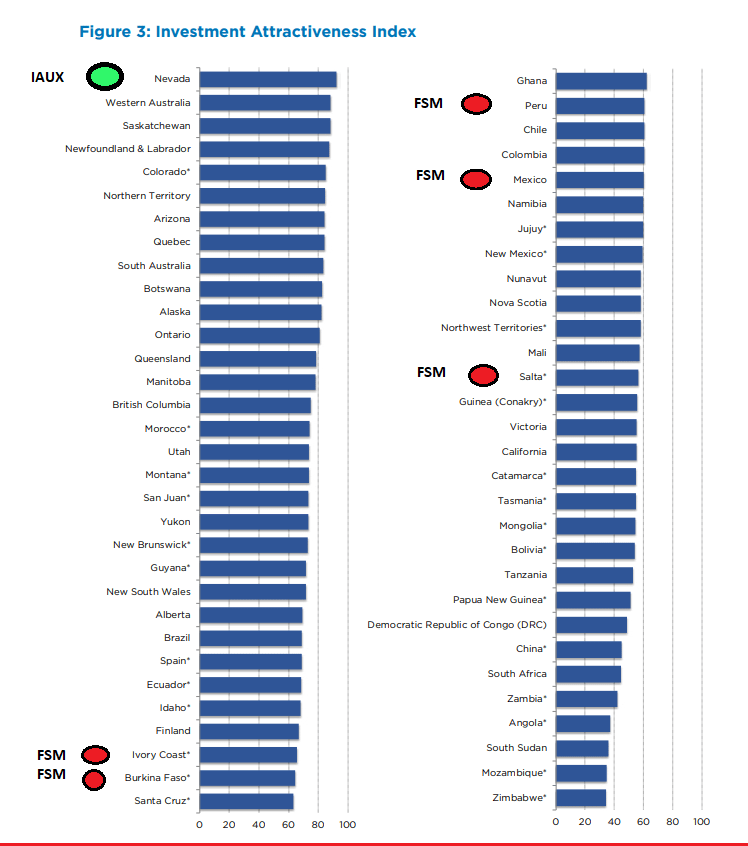

Jurisdictional Profile - i-80 Gold vs. Fortuna Silver, Author's Drawings (Fraser Institute Investment Attractiveness Index)

{kind=link}

Assuming the Chesser acquisition goes through successfully, I see only a slight increase in my fair value estimate following the deal with a more appropriate NAV multiple being 0.90x (0.95x NAV previously). And with some other miners trading at less than 0.60x P/NAV and being thrown out with the bathwater, I continue to see more attractive bets elsewhere in the sector. One example is i-80 Gold ( IAUX ), which trades at less than 0.60x estimated net asset value in the #1 ranked mining jurisdiction per the Fraser Institute 's Investment Attractiveness Index.

For further details see:

Fortuna Silver: More Share Dilution, But A Decent Deal For Diamba Sud