FSM - Fortuna Silver: Seguela Mine Begins Contributing On Schedule

2023-07-13 12:03:13 ET

Summary

- Fortuna Silver reported solid production in Q2, producing ~93,500 gold-equivalent ounces with initial contribution from Seguela on schedule.

- The start of production from Seguela is positive, given that it will be FSM's highest margin asset, but the bigger issue will be adding reserves at its two short-life assets.

- That said, while FSM is reasonably valued, I continue to see far more attractive betters with higher-quality assets elsewhere in the sector and no margin of safety here just yet.

The Q2 Earnings Season for the VanEck Gold Miners ETF (GDX) is just around the corner, and we've seen strong results from Victoria Gold (VITFF), Calibre Mining (CXBMF), and Sandstorm Gold (SAND). One of the most recent companies to report was Fortuna Silver (FSM), and despite a temporary shutdown at its San Jose Mine in Mexico, the company put together a solid Q2 , with production of ~93,500 gold-equivalent ounces [GEOs]. The strong performance was helped by initial production from its new Seguela Mine in Cote d'Ivoire, offsetting a softer quarter from San Jose and Lindero, which saw ~30% and 12% declines in production on a year-over-year basis, respectively. And while Seguela may have contributed less than 5% of the ounces in Q2, this figure will improve dramatically by Q4 as we see initial contribution from the high-grade Ancien Pit. Let's take a closer look at the quarter below:

All figures are in United States Dollars unless otherwise noted.

{kind=link}

Q2 Production

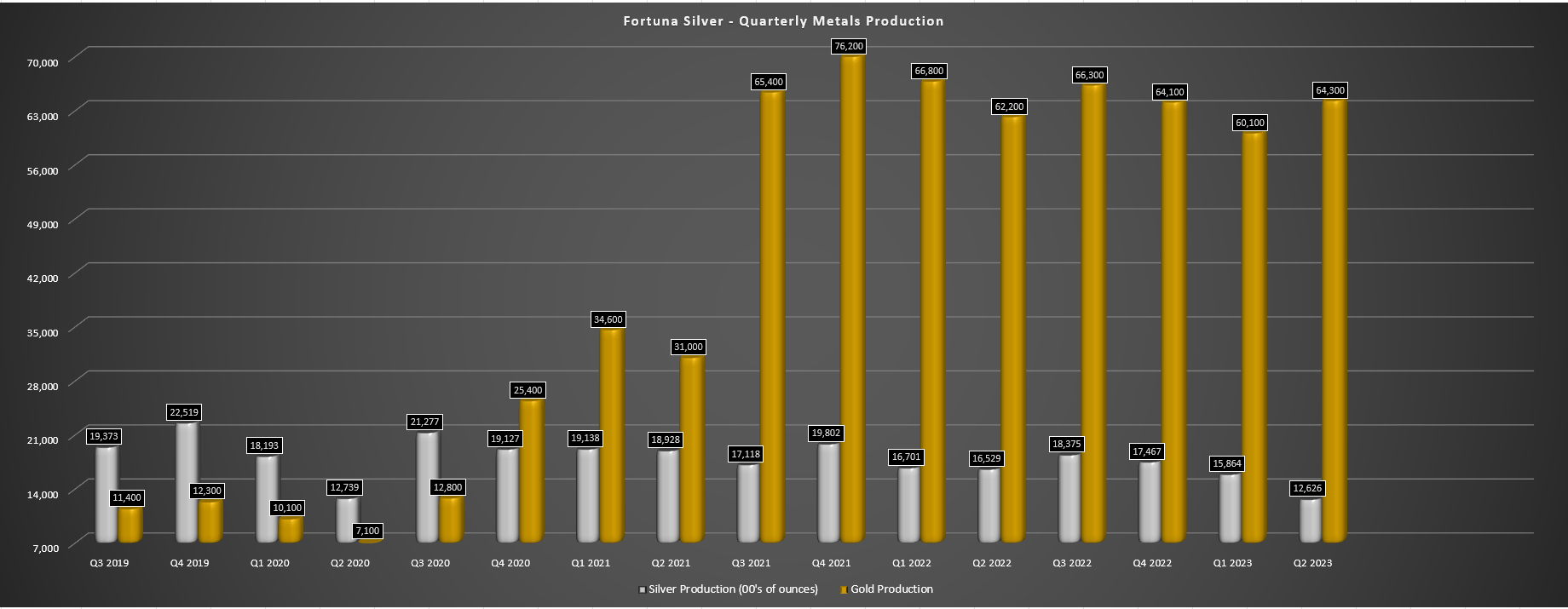

Fortuna Silver ("Fortuna") released its preliminary Q2 results this week, reporting quarterly production of ~93,500 GEOs, which comprised ~1.26 million ounces of silver and ~64,300 ounces of gold. The result was a 4% increase in gold production offset by a 24% decline in silver production, with the company's San Jose Mine seeing a steady trend in lower production as we see lower head grades, with the additional impact of a 15-day shutdown in the period. Fortunately, the shutdown has been resolved and Fortuna is now operating a record five mines (Lindero - Argentina, Seguela - Cote d'Ivoire, Yaramoko - Burkina Faso, Caylloma - Peru, San Jose - Mexico), and on track to have its first 100,000 GEO quarter in Q3 2023 with access to high-grade stopes that were expected to be mined in Q2 and a full production quarter from Seguela with the benefit of slightly higher feed grades.

Fortuna Silver - Quarterly Metals Production (Company Filings, Author's Chart)

{kind=link}

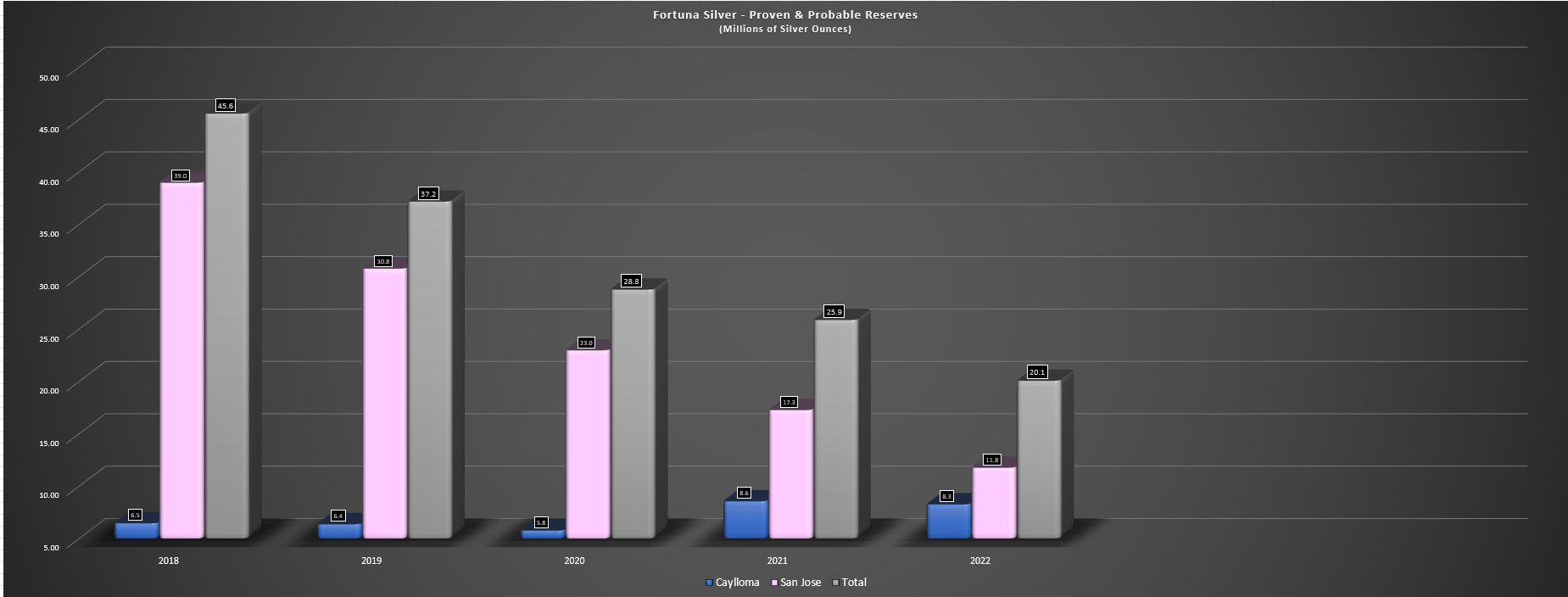

As the above chart highlights, while Fortuna's gold production has grown materially with the addition of Yaramoko and Lindero coming online and will hit new quarterly highs once Seguela moves into commercial production, the company's silver production has fallen off a cliff and will only get worse. The latter is evidenced by silver production sliding from ~4.15 million ounces of silver in H1 2017 to ~2.84 million ounces of silver in H1 2023. Worse, costs are significantly higher at San Jose vs. the $7.15/oz all-in sustaining costs [AISC] reported in H1 2017 with H1 2023 AISC likely to come in above $17.00/oz. As discussed in past updates, the downtrend in silver production is related to the inability to replace silver reserves at its San Jose Mine and the declining grade profile combined with the impact of inflationary pressures.

Fortuna Silver - Declining Silver Reserves (Company Filings, Author's Chart)

{kind=link}

Unfortunately, the future of this asset remains a question mark which would mostly strip Fortuna of its silver title, given that San Jose's reserves are sitting at a mere ~2.1 million tonnes vs. a trailing two-year average throughput rate of ~1.03 million tonnes, pointing to a two-year mine life at this asset (reserves only). And while it's possible that the company could extend this mine life past 2025, I am not overly optimistic, which could have a negative impact on the company's multiples given that gold producers trade at far lower P/NAV and cash flow multiples than silver producers on balance. That said, while San Jose's reserves are dwindling, the good news is that it's back online after a brief shutdown in Q2 and Q3 should be a better quarter with higher throughput than the ~194,900 tonnes processed in Q2 and better grades, with Q2 production coming in at just ~957,300 ounces of silver and ~5,800 ounces of gold, and the asset likely to deliver into the low end of its guidance.

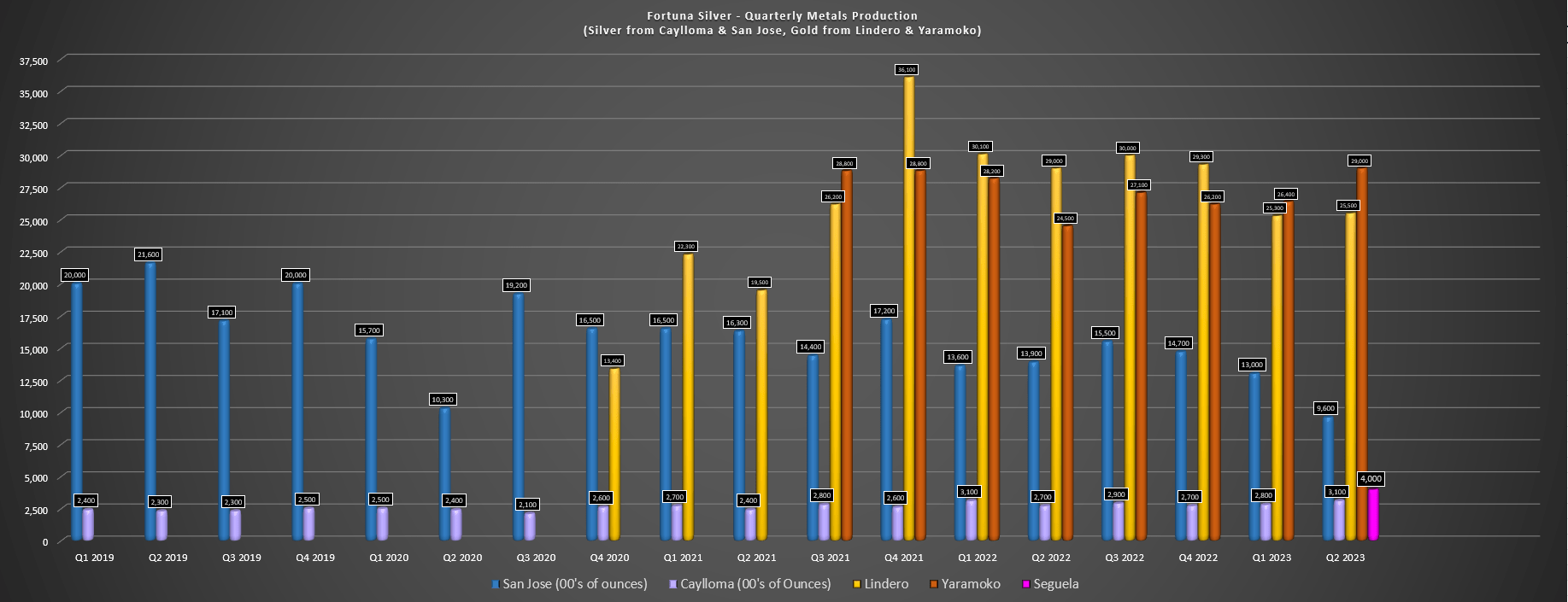

Fortuna Silver - Quarterly Metals Production (Silver from Caylloma, San Jose in 00's of Ounces) (Company Filings, Author's Chart)

{kind=link}

Moving over to Fortuna's other operations, there wasn't much to write home about at Lindero either, with production coming in at ~25,500 ounces, a 12% decline year-over-year. As I warned in previous updates, this was likely to be a drag on Fortuna's results in 2023 with tougher comps until Seguela came online, given that the best years were in the rearview mirror from a grade standpoint. And this was evidenced by the Q2 results at Lindero with similar tonnes stacked on the pads (~1.5 million tonnes) but at much lower grades (0.62 grams per tonne of gold vs. 0.74 grams per tonne of gold), resulting in the double-digit decline in production. And while this was in line with the mining sequence, the lower grades don't help from a unit cost standpoint with significantly less production per tonne processed vs. previous years.

Fortunately, Fortuna's Yaramoko Mine picked up some of the slack in the period, with the asset producing ~29,000 ounces of gold with higher throughput and grades on a year-over-year basis (~144,200 tonnes at 6.51 grams per tonne of gold). The company noted in its prepared remarks that grades came in above planned levels which benefited quarterly output, and it now expects production to come in at the high end of the guided range, with over 55,000 ounces produced year-to-date. In addition, the company has identified extensions of mineralization on the fringes of its resource boundary at the 55 Zone, which could translate to a slight boost to resources and reserves, which are expected to be updated by year-end - a positive development.

Seguela's First Gold Pour

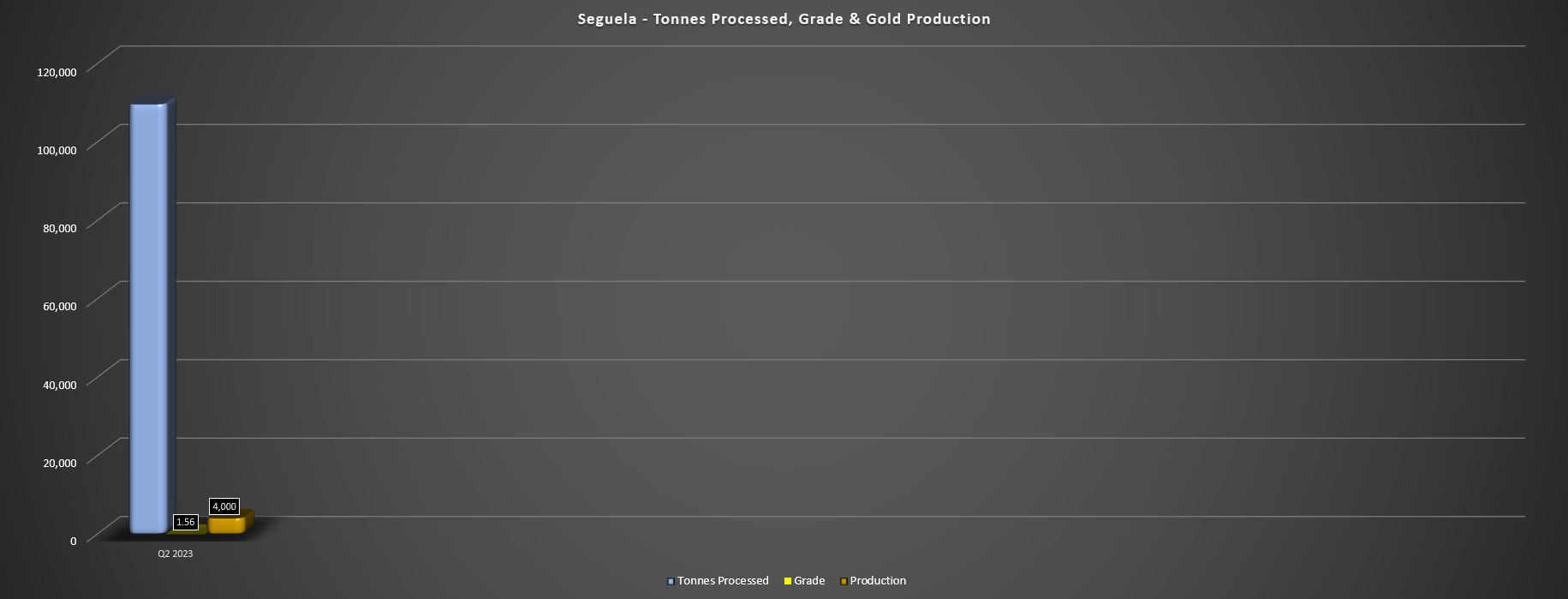

Although the Q2 production results from its primary three operations were mediocre with lower production at two assets offset by a better quarter at Yaramoko, the major news was the company's first gold pour at its new Seguela Mine in Cote d'Ivoire. Fortuna noted that the first pour was achieved on July 7th in line with schedule and the mine contributed ~4,000 ounces of gold in its first quarter with ~109,600 tonnes processed (1,611 tonnes per day) at an average grade of 1.56 grams per tonne of gold. At first glance, this might seem like relatively low production, but it's important to note that the feed was made up of lower grade saprolite ore during the ramp-up phase and was well below mined grades of 2.35 grams per tonne of gold at Antenna, and the much higher grades from Ancien that should hit the mill by Q4. The result is that this will be Fortuna's largest and lowest-cost mine by a wide margin.

Seguela - Tonnes Processed, Grade & Gold Production (Company Filings, Author's Chart)

{kind=link}

The other positive news worth reporting is that Seguela's mill throughput ramped up to 154 tonnes per hour at the end of the quarter, and grade control drilling completed at Antenna showed 2% higher tonnes and 13% higher grades, which could end up translating to positive reconciliation vs. the reserve model. This is certainly encouraging for an asset that's already expected to be a consistent ~130,000 ounce producer in its first six years, with the opportunity to optimize this production profile if it decides to pull forward higher-grade ounces from newly delineated deposits like Sunbird.

For those unfamiliar, Sunbird is a high-grade deposit that lies just southeast of Antenna, with an M&I resource of 279,000 ounces at 2.74 grams per tonne of gold, well above the average grade of Agouti, Boulder, and Antenna, with the former two being lower grade pits that will start contributing post-Year 5. Assuming Sunbird continues to deliver, it's possible higher-grade feed here could sequence in ahead of Agouti and Boulder ore, helping to maintain a 130,000-ounce production profile for longer. Plus, there's also the possibility of a mill expansion given the growing resource base here, which could push annual gold production closer to 150,000 ounces with optimized feed depending on the scale of any mill expansion. Hence, Seguela coming online is certainly an upgrade to the Fortuna story.

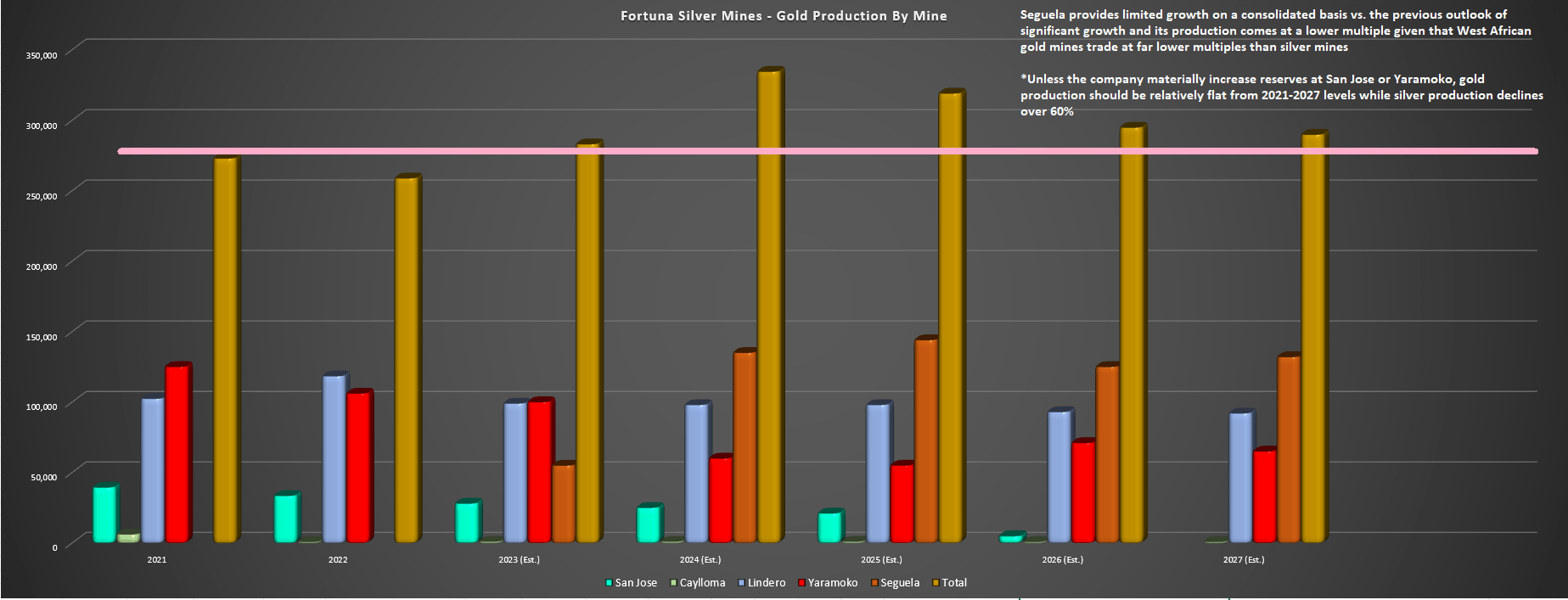

Fortuna Silver - Conceptual Production Profile & Historical Production (Gold Ounces) / Forward Estimates (Company Filings, Author's Chart)

{kind=link}

The problem, though, which I've addressed in past updates, is that while Seguela adds a new 10-year mine low-cost mine to Fortuna's stable, the company has two high-cost and short mine life assets that could cease production by 2028, with San Jose potentially set to head offline much earlier (reserves only support production into 2025). Hence, while I was more optimistic on reserve replacement at these assets and the ability for Seguela to translate to growth, it's looking like this asset will simply offset declining production at these two mines on a gold-equivalent basis. And while this is higher-margin production, small-scale West African gold mines do not command the same multiples as silver mines, meaning that San Jose heading offline would be a blow from a valuation standpoint. So, unless the company can materially increase reserves at San Jose/Yaramoko, gold production will flatline, while GEO production peaks in 2024 and begins to decline materially post-2024.

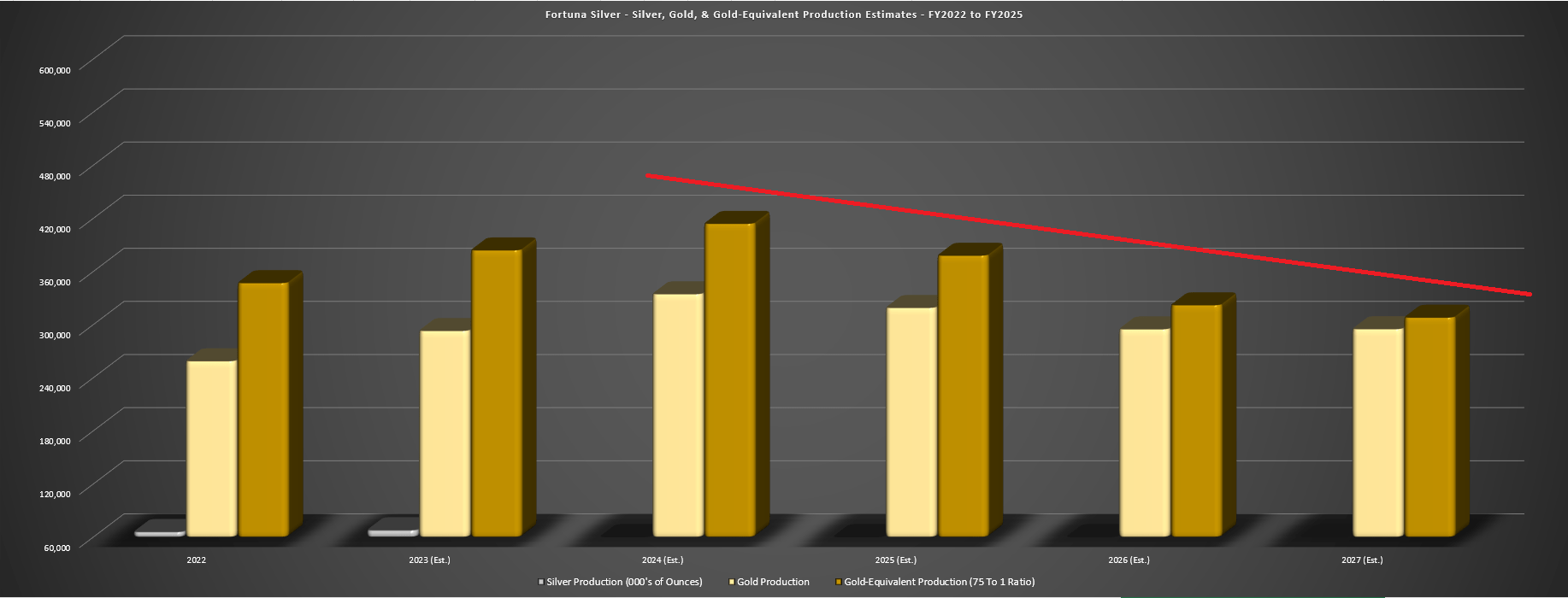

Fortuna - Gold, Silver, & Gold-Equivalent Ounce Production & Forward Estimates (Company Filings, Author's Chart)

{kind=link}

Let's take a look at the valuation and see how Fortuna stacks up vs. peers:

Valuation

Based on ~310 million shares and a share price of US$3.50, Fortuna trades at a market cap of $1.09 billion and an enterprise value of ~$1.30 billion. This has left the stock at a more reasonable valuation than where it traded two months ago when I warned against paying up for the stock at US$4.00 per share. However, while the Diamba Sud acquisition was accretive from a NAV standpoint, it's clear that the company is morphing from a Latin American silver-gold miner into primarily a West African gold producer (two of its largest mines in West Africa). As I've noted in past updates, this pivot could continue to weigh on its multiples as gold producers with West African exposure trade at much lower multiples than precious metals companies with ~55% of their revenue coming from silver, which is where Fortuna stood pre-Lindero in 2019.

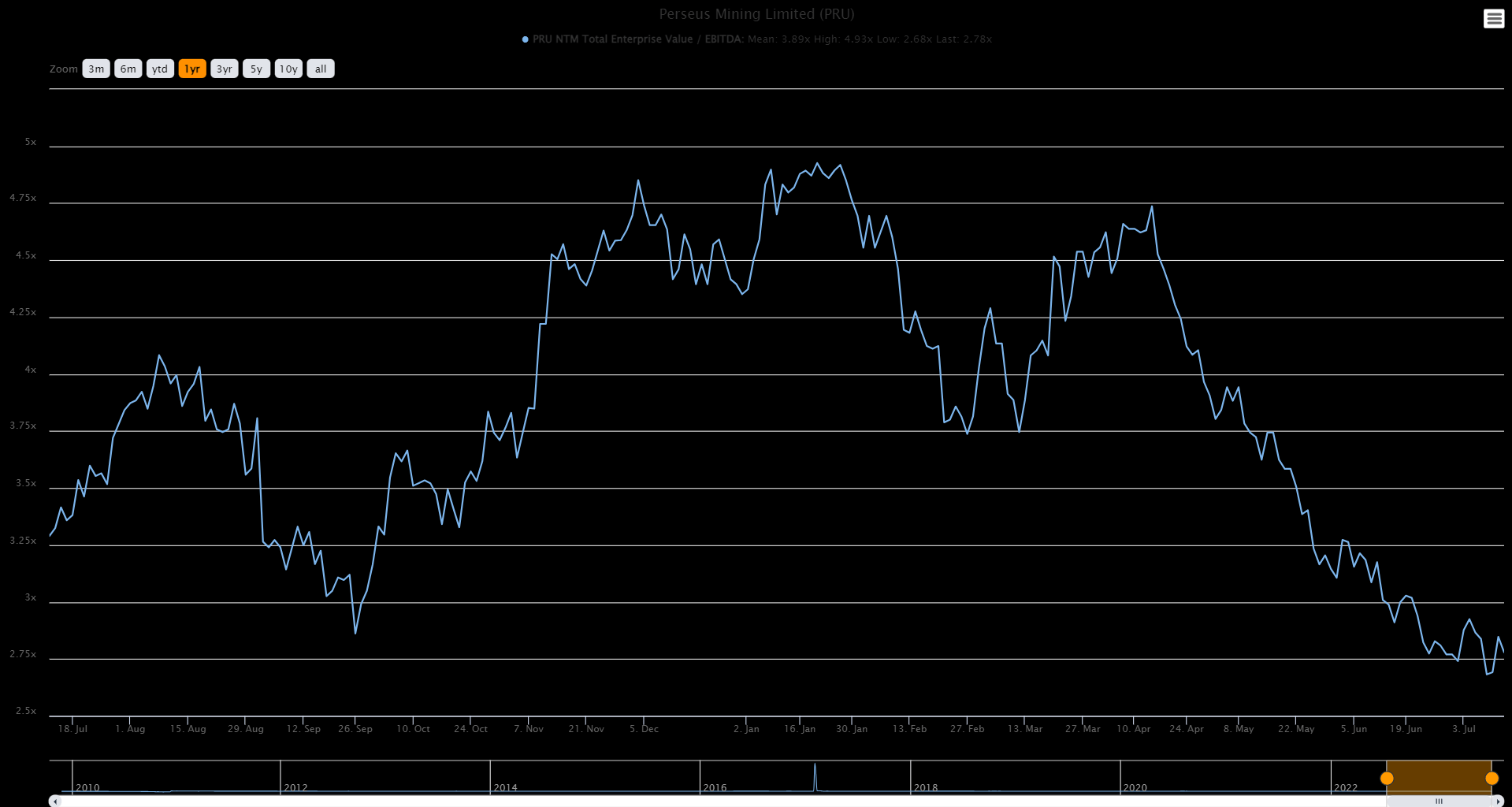

For those skeptical of this multiple compression argument, they can look no further than Perseus Mining (PMNXF), which has a stronger balance sheet ($470 million in net cash vs. $200 million in net debt), a larger production profile (~500,000 ounces of annual gold production) and much higher margins than Fortuna ($1,050/oz AISC vs. ~$1,300/oz across its assets) yet trades at less than 3.5x EV to FY2023 cash flow estimates and one of the lowest cash flow multiples sector-wide. And given that San Jose could run out of reserves by 2026 and reduce Fortuna's silver production to barely 5% of annual revenue (erasing any silver premium), I don't see any reason the stock should trade above 6.0x cash flow when higher-margin peers trade at much cheaper valuations.

{kind=link}

So, using what I believe to be more conservative multiples of 5.0x forward cash flow and 0.90x P/NAV using a 65/35% weighting (P/NAV vs. P/CF), I see a fair value for Fortuna of US$4.40. And while this fair value estimate points to a 35% upside from current levels, I am looking for a minimum 40% discount to fair value to ensure an adequate margin of safety for small-cap producers in non-Tier 1 jurisdictions. If we apply this required discount to Fortuna, its ideal buy zone comes in at US$2.65 or lower, suggesting the stock is nowhere near a low-risk buy zone currently. Obviously, this doesn't mean that the stock can't trade higher, but I prefer to only buy at the right price or pass entirely, and I still don't see an attractive reward/risk setup here with Seguela online, given that its main silver asset's reserves are dwindling and multiple compression from its transformation into a Tier-2/Tier-3 jurisdiction gold producer (that's West Africa dominant) could continue to weigh on the stock.

Summary

Fortuna Silver put together a solid Q2 operationally and it's encouraging to see that Seguela has come online on budget and schedule with higher grades expected as the asset moves towards commercial production. That said, the rest of its portfolio leaves much to be desired, with short mine lives at San Jose and Yaramoko, an operation that's seeing steadily declining grades at Lindero with its best years behind it, and a high-cost asset in Caylloma with razor-thin all-in cost margins. And while I recognize Seguela is an exceptional asset, there's only so much value that can be ascribed to a single asset, especially when it's in a Tier-3 jurisdiction where multiples are typically much lower. In summary, I continue to see far more attractive bets elsewhere in the sector, with Perseus being far more undervalued among West African producers, and Pan American Silver (PAAS) being the higher-quality option for gold/silver exposure.

For further details see:

Fortuna Silver: Seguela Mine Begins Contributing On Schedule