FET - Forum Energy Shares Encouraging Scenarios

2023-06-06 10:38:57 ET

Summary

- Forum Energy Technologies is expected to see a better time in the coming days, with the US drilling market set to pick up pace in 2H 2023.

- FET's strategy to diversify further in the international markets should pay dividends over the medium term, and the offshore market growth would put the company on a rapid growth path.

- Despite short-term concerns, such as a slowdown in order bookings in Q1, the stock is relatively undervalued versus its peers, making it a potential "buy" for investors.

FET Is Close To An Inflection

I discussed in my previous article how Forum Energy Technologies (FET) management is focused on the diversification and commercialization of its products. I believe FET is due to witness a better time in the coming days. The US drilling market, which softened up in early 2023, is set to pick up the pace in 2H 2023. Its handling tool business and coiled tubing product line have led the charge in recent times. The company's strategy to diversify further in the international markets should pay dividends over the medium term. As a result of the long contracts, energy services companies can avoid short-term energy price volatility and improve their pricing and margin. Moreover, the offshore market growth would put the company on a rapid growth path in the medium-to-long term due to its long lead time.

But the company's order booking slowed down in Q1, particularly in the Completion and Production segment, reducing the revenue visibility. Nonetheless, the drivers are sufficiently robust to alleviate the short-term concerns. Also, the management expects cash flows to turn positive in 2023. The stock is relatively undervalued versus its peers. Investors would want to "buy" the stock given the long-term strengthening drivers.

Market Outlook

{kind=link}

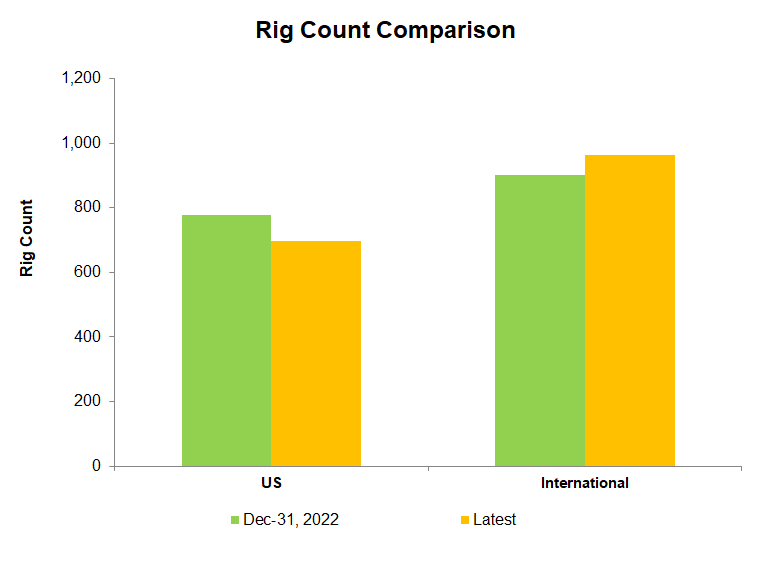

FET's business, critically dependent on rig count, saw the US and international markets diverging. While the US rig count has decelerated since the start of 2023 (down by 11%), the international rig count has increased (7% up) until now.

Lower crude oil and natural gas prices led to less drilling and completion activity, particularly from the private operators, during this period. It is, however, likely that the US onshore drilling activities will recover in 2H 2023. Also, equipment utilization remained high due to falling rig count and stable demand.

Demand And Pricing

{kind=link}

So, pricing for oilfield services equipment remained high, although there is a clear indication that efficient and upgraded equipment will receive disproportionately higher pricing than legacy equipment. This has led to a bifurcation in the market, and FET will depend increasingly on its upgraded products.

The international and offshore markets are recovering and should gain even more prominence, requiring further investment. In this environment, FET's management appears to expect the US market, which currently appears soft, to pick up pace in 2H 2023. They will see longer contracts, insulating services companies to avoid short-term energy price volatility. FET will continue to focus on strengthening its international presence over the next six to 12 months.

Q2 2023 Forecast

Over the past few years, FET's global reach has extensively expanded. FET's management expects continued international acceleration to mitigate the activity deflation in the US. In Q2 2023, it expects revenues to decrease by 2% compared to Q1. EBITDA, however, can improve by 18% (at the guidance mid-point).

Geographic Outlook

Geographically, its drilling capital equipment product increased nearly threefold in the Middle East over the past six months. FET's handling tool business and coiled tubing product line have recently experienced rapid growth. The coiled tubing product line accounted for approximately 50% of its international revenues in Q1. In other categories, aftermarket demand in the Subsea Technologies product line increased by 40%.

Bookings can increase for its new build, ROV, and trencher products over the medium-to-long term. In comparison, FET will primarily focus on the artificial lift product family in the US. It will also extend this product line to several Latin American countries and national oil companies in the Middle East and Asia Pacific regions.

New Technology

One of the critical innovations for FET in recent times has been the FASTConnect system, which is considered to be the direct replacement of the zipper manifold. FASTConnect not only increases efficiency by completing more frac stages per day, but it also improves safety measures and well-site environmental footprint by eliminating grease.

Backlog Softness And Q1 Performance

{kind=link}

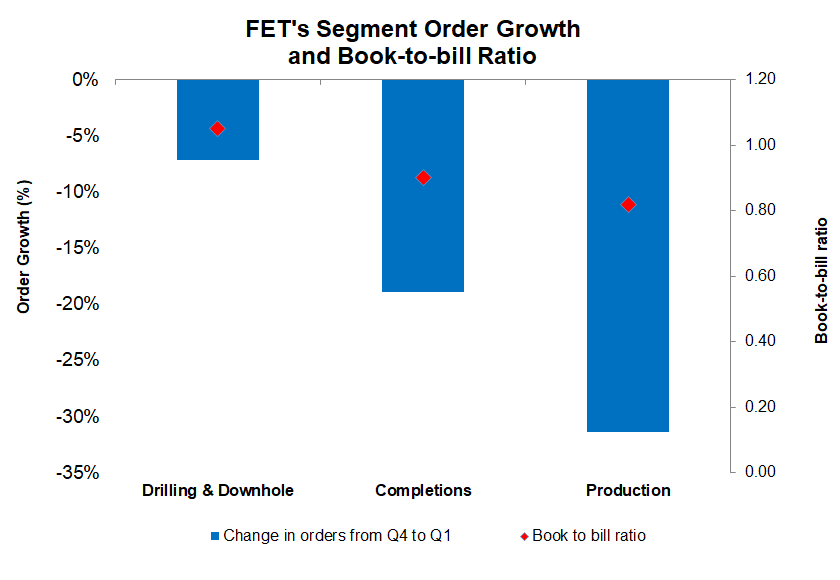

Despite these technological advances and market conditions, FET's order bookings and book-to-bill ratio met with a speed bump in Q1. Its book-to-bill ratio went below 1x (0.95x) as of March 31. Investors may note that its product orders typically involve longer lead time capital equipment. Order bookings especially suffered in the Completion (19% down) and Production (31% down) segments, quarter-over-quarter. The book-to-bill ratio was the lowest in the Production segment (0.82x) as of March 31.

In Drilling & Downhole, on the other hand, order bookings were robust in artificial lift, drilling handling tools, and drilling consumable products. Artificial lift bookings increased 33% from Q4 to Q1 2023, as completion work is picking up in the Gulf of Mexico and West Africa.

{kind=link}

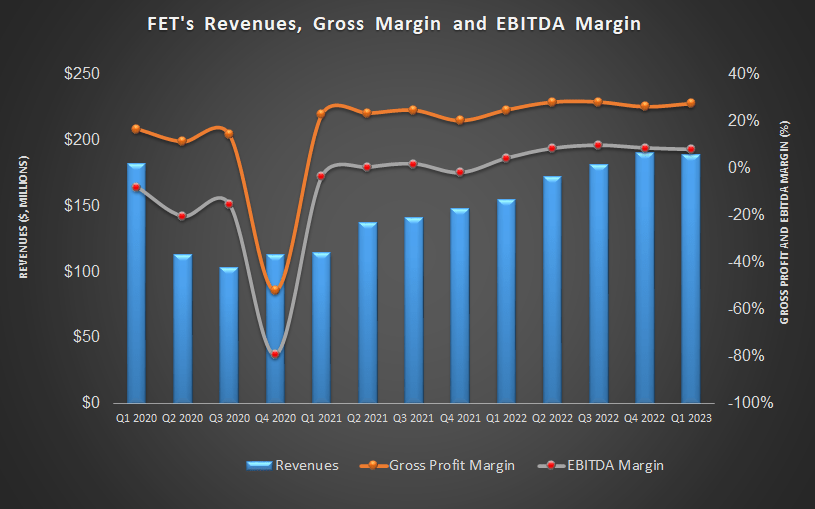

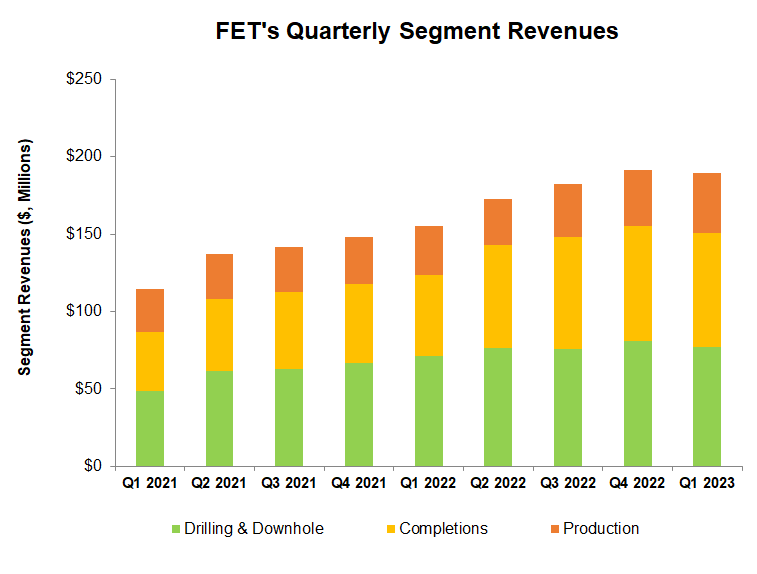

FET'S revenues decreased marginally from Q4 2022 to Q1 2023 (by 1%). International revenue increased by 17% during this period. On the other hand, adverse project timing caused the US revenues to fall.

Cash Flows And Debt

The company's cash flow from operations remained negative (-$23 million) in Q1 2023 versus a year ago. Although year-over-year revenues increased, a higher inventory led to a cash flow decline. The supply chain issues and logistical disruptions caused the inventory balance to remain high, causing a drain on its cash flows. The management expects the issues to dissipate in Q2. FET's management expects positive free cash flow in the next three quarters, resulting in $20 million-$40 million in FCF in FY2023.

FET's liquidity stood at $176 million as of March 31, 2023, while its debt-to-equity was 0.37x. During Q1, it repurchased ~$3.5 million of its shares, leaving $2.4 million under the repurchase authorization program. With sufficient liquidity and manageable leverage, its financial risks are low.

Why Do I Upgrade FET's Rating?

Late in 2022, FET was hit by supply chain issues and commodity price inflation, which lowered its margin. In response, it focused on international operations and set up manufacturing and distribution hubs worldwide to supply efficiently. I wrote :

FET is diversifying into hydraulic frac operations, which includes innovations like FASTConnect System. The international market, which accounts for a significant part of its total revenue, is the current focus after strategically selecting its manufacturing and distribution hubs worldwide to supply efficiently. The company's order booking also did not slowdown in Q4, leading to improved revenue visibility into 2023.

Early in 2023, the US market remained soft, so FET focused more on the international market. The international offshore markets are already on a recovery path. While the US onshore drilling activities are expected to recover in 2H 2023, equipment utilization has remained high due to falling rig count and stable demand. The company's balance sheet also looks robust, and the management expects the free cash flow to improve. So, I deem it fit to upgrade the rating to "Buy."

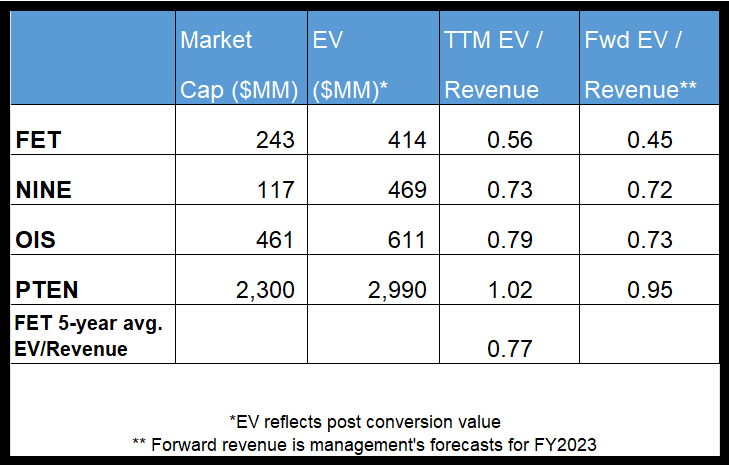

Relative Valuation

Author created and Seeking Alpha

{kind=link}

The company's revenue is expected to rise more sharply than its peers. FET's forward EV/Revenue multiple contractions (using the management's revenues forecast) versus the current EV/Revenue is steeper than its peers, typically resulting in a higher EV/Revenue multiple than its peers. The company's current EV/Revenue multiple (0.56x) is lower than its peers' (NINE, OIS, and PTEN) average (0.85x). It is also lower than its past five-year average. So, the stock is undervalued compared to its peers at this level in my view.

What's The Take On FET?

{kind=link}

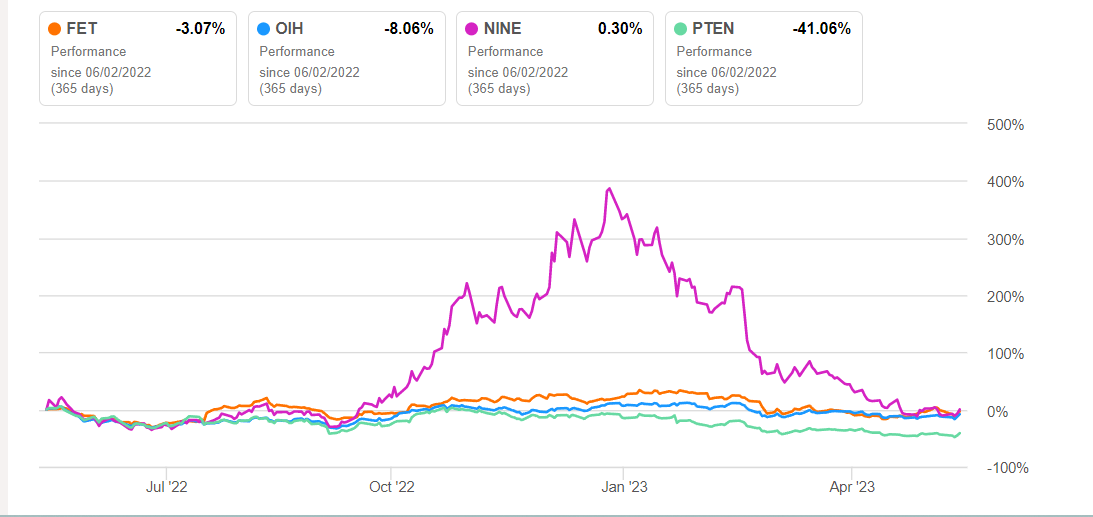

In the wake of the bifurcation in the market where efficient and upgraded equipment receives disproportionately higher pricing, FET's FASTConnect System can score fast because it is considered to be a replacement for the zipper manifold. Since the company's global reach broadened over the past few years, I believe drilling activity acceleration in the international market can more than offset the relative slowdown in the US onshore. So, the stock performed nearly in line with the VanEck Vectors Oil Services ETF (OIH) in the past year.

In the near term, FET faces two primary challenges - an order book slowdown and negative cash flow generation. Also, the company's balance sheet strengthened after the debt conversion in Q4. Although negative cash flow remains a concern, given the stock's relative undervaluation, it should turn out to be the right pick for investors looking to add to their portfolios.

For further details see:

Forum Energy Shares Encouraging Scenarios