FET - Forum Energy Strives To Bounce Back From The Current Headwinds (Rating Downgrade)

2023-09-21 02:58:08 ET

Summary

- Forum Energy's drilling and hydraulic fracturing activity is expected to decline in the US, leading to more idled fleets in 2023.

- However, the company's international and offshore operations will lead to strong performance in 2024.

- It has a steady backlog and has introduced innovative products, positioning it for improved returns in the medium term.

FET To Get Past The Inertia

I have been discussing Forum Energy Technologies ( FET ) in the past, and you can read the latest article here . Most new drilling and hydraulic fracturing activity appears to be deferred to 2024, indicating that FET can idle more fleets in 2023. Most of the decline is confined to the US market, though. With a growing backlog, the company's international and offshore operations will have sufficient tailwinds. Offshore, it has booked new and refurbished ROVs. It has also strengthened its portfolio by adding innovative products like next-generation iron roughneck and greaseless cable systems.

Lower fracking activity adversely impacted the company's frac-related power end and radiator sales in Q2. Its cash flows were negative in 1H 2023. So, it aims to improve working capital supply chain tightening and inbound raw material reduction. With robust liquidity, its financial risks are low. The stock is relatively undervalued compared to its peers. I recommend investors "hold" the stock for an improved return in the medium term.

A Close Look At The Frac Market

I am not overly optimistic about the US drilling and completion activity outlook in the near term. The operators remained disciplined with their capex plans. So, many US drillers and pressure pumpers idled their equipment, which helped stabilize the pricing for high-spec rigs, wireline, and coiled tubing units. The softening of hydraulic fracturing activity has resulted in lower utilization for the pressure pumpers, who have resorted to reducing their capex on frac fleet upgrades and additions.

When demand defers to 2024, FET's idled fleet count can increase in this environment. However, the crude oil price has strengthened over the past few months. Crude oil prices have increased by 27% since July, while natural gas prices have recovered. Since rig count follows energy prices with a lag, I expect rig count to bottom in early Q3 and back up in Q4 through early 2024. Also, during the recent downturn in energy activity, the demand for more efficient equipment has remained high in the US. So, while drilling and completion activity remain low in 2023, it can rebound in 2024.

Q3 And FY2023 Outlook

{kind=link}

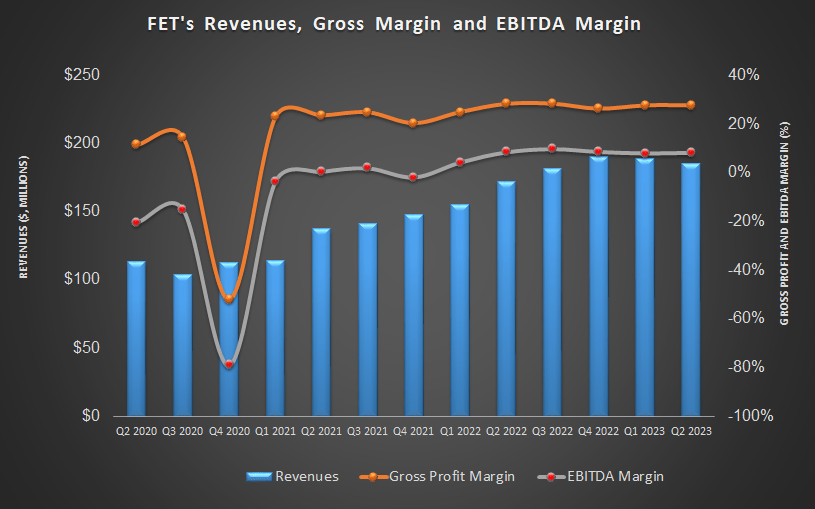

FET's management expects to realize $80 million in adjusted EBITDA in FY2023, which is lower than its earlier target of $100 million for the year. Despite the lower guidance, it would still be 36% higher than FY2022. Its international and offshore revenues in 2H 2023 can outperform the US as large international field development, production, and LNG projects have recently been approved.

While its US revenues can decline in Q3, higher international sales can keep its aggregate revenues steady and increase its adjusted EBITDA compared to Q2.

Backlog And New Products

As customers gain extended revenue visibility, FET's backlog grows. In Q2, FET's total backlog increased by 13% from a year ago. Backlogs in drilling and downhole technologies increased by 20%-25%. Its production equipment product backlog saw the highest year-over-year growth (46%). Notably, its ForuMix technology sales benefited from the Saudi Arabia desalter project.

FET's August 2013 Presentation

{kind=link}

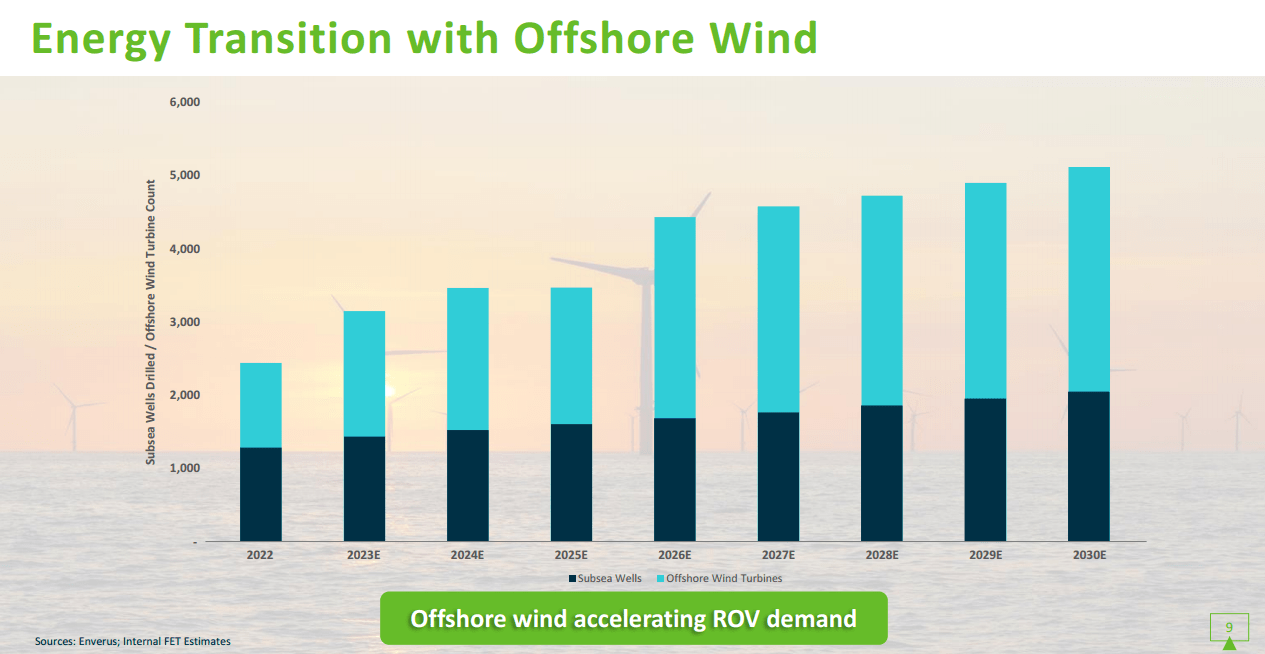

FET has gained market share through new product development in the international and offshore markets. It sees opportunities in 20 newbuild rigs in the Middle East to provide iron roughnecks, catwalks, cranes, and handling tools. In offshore, it has booked new and refurbished ROVs and may receive the award of several ROV newbuilds in Q3. The ROVs will be used in traditional energy production and offshore wind construction.

The company aims to build a portfolio by creating products that enhance value through environmental and safety benefits. In Q2, these products accounted for ~50% of stimulation product family revenues. Its innovations include the next-generation iron roughneck called FR120 and the Envirolite greaseless cable system.

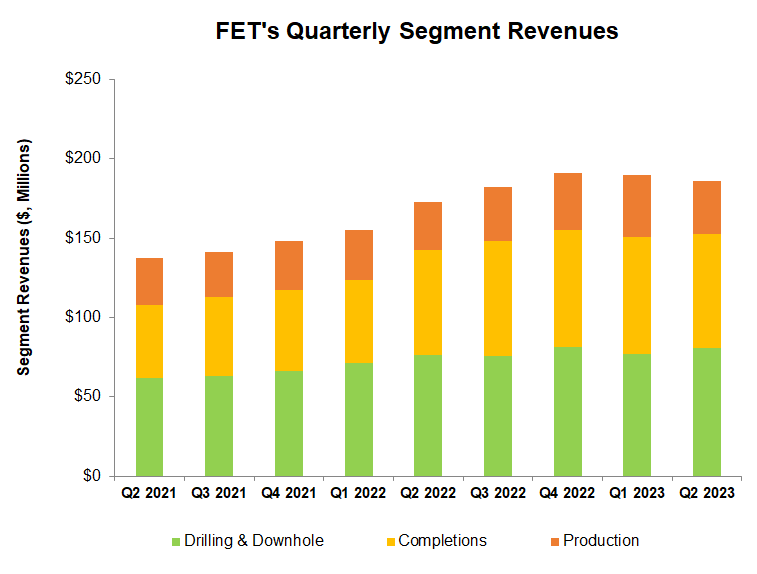

Q2 Segment Result Analysis

FET's revenues increased by 5% in Q2 compared to Q1 in the drilling and downhole segment due to higher sales in drilling and subsea technologies product lines. Subsea bookings rose 35% from Q1 to follow higher demand for subsea ROVs and drilling capital equipment.

{kind=link}

FET'S revenues from the Completion segment decreased from Q1 to Q2 (by 2%) due to slowing frac-related power end and radiator sales. Production revenue decreased by 15% during this period. However, the segment saw a book-to-bill of 1.26x due to strong orders for ForuMix technology and US production-based awards.

Cash Flows And Debt

The company's cash flow from operations remained negative (-$30 million) in 1H 2023 but improved over a year ago. The company's year-over-year revenues increased. Plus, its working capital improved due to the tightening of the supply chain and reduction in the flow of inbound raw materials. The management expects working capital to enhance further. FET's management expects a positive free cash flow of $20 million in FY2023, suggesting $50 million of FCF in 2H 2023.

It reduced its FY2023 capex guidance to $8 million from $15 million set earlier. FET's liquidity stood at $170 million as of June 30, 2023, while its debt-to-equity was 0.33x. So, it has ample liquidity.

Relative Valuation

Author Created and Seeking Alpha

{kind=link}

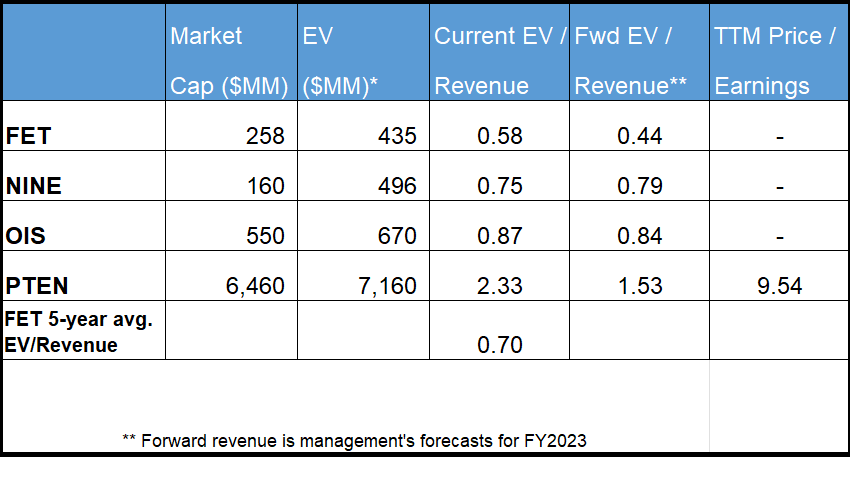

Applying the management's revenue forecast, FET’s forward EV/Revenue multiple versus the current EV/Revenue will contract. The rate of contraction is steeper than its peers. This suggests its revenue can rise more sharply than its peers, typically resulting in a higher EV/Revenue multiple. Although the topline faces a few constraints in Q3, I think the backlog growth will sustain a recovery in early 2024, following the execution of orders in the international offshore projects and the Saudi Arabia desalter project. So, I agree with sell-side analysts’ views on the relative valuation multiple.

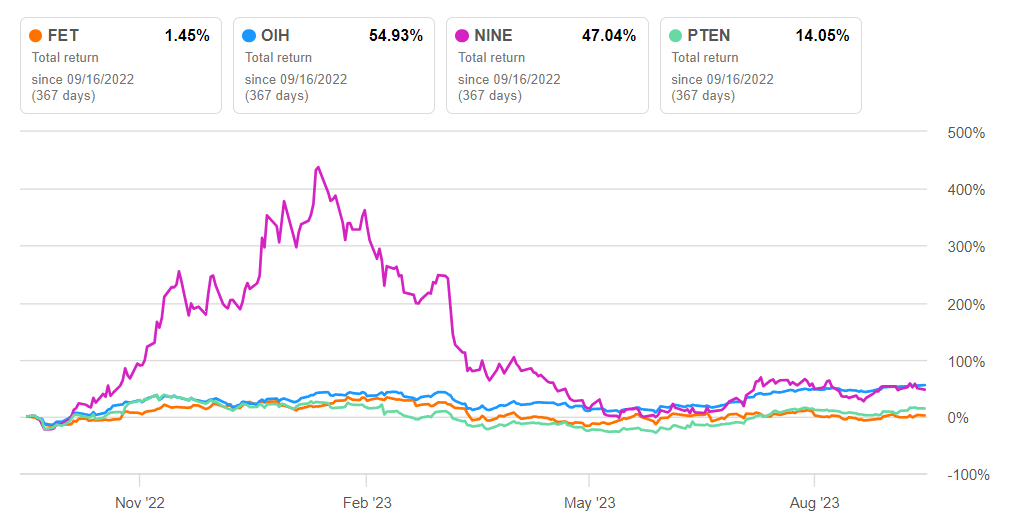

The company's current EV/Revenue multiple (0.58x) is lower than its peers' ([[NINE]], [[OIS]], and [[PTEN]]) average (1.3x). It is also lower than its past five-year average. So, the stock is undervalued versus its peers. I do not see returns exceeding 10% in the near term. If the stock trades at the historical average, the target price would be ~$40, suggesting 59% returns in the next year.

Why Do I Downgrade FET?

I did several iterations of my analysis about FET in the past. The common themes that cut across the analysis are the company's focus on benefiting from international offshore market growth and diversifying into methane emissions control, carbon capture use, and storage. On the other hand, the supply chain issues troubled its margin expansion efforts until early 2023. However, drilling and completion works have been inconsistent, given the US rig count's volatile movement.

In my previous article, I was fairly optimistic about FET's outlook due to robust growth in the handling tool business and coiled tubing product line. I also expected the offshore market growth to put the company on a rapid growth path, validating my "buy" call. I wrote :

Since the company's global reach broadened over the past few years, I believe drilling activity acceleration in the international market can more than offset the relative slowdown in the US onshore.

After Q2, I see that the softening of hydraulic fracturing activity resulted in lower utilization for the pressure pumpers. So, the company lowered its revenue and EBITDA estimates. On a positive note, its backlog increased in Q2. Its new product introductions and diversification into the offshore energy industry will open up new growth opportunities. I would recommend investors to "hold" the stock.

What's The Take On FET?

{kind=link}

Over the past year and a half, many US drillers and pressure pumpers have idled their equipment following the fall in drilling and completion activity. The US's demand for more efficient equipment has remained high despite that. Its US revenues can decline in the near term, while higher international and offshore sales can mitigate most of the adverse effects. Its drilling technologies and downhole technologies backlog increased handsomely in Q2. The company has introduced various innovative products in offshore drilling and ROVs where new projects have been implemented.

But FET's woes are not over yet. Pressure pumpers' utilization has decreased due to the softening of hydraulic fracturing activity. Its negative cash flows have also been a concern for investors. So, the stock underperformed the VanEck Vectors Oil Services ETF ( OIH ) in the past year. Nonetheless, given the stock's relative valuation discount, investors would do well to "hold" the stock for moderate returns in the medium term.

For further details see:

Forum Energy Strives To Bounce Back From The Current Headwinds (Rating Downgrade)