FURCF - Forvia: The 2025 Guidance Makes The Stock Attractive

2023-10-04 04:00:00 ET

Summary

- Faurecia rebranded to Forvia after acquiring Hella to diversify and create economies of scale.

- Forvia had a good first semester with strong revenue and operating income, despite non-recurring expenses and high finance costs.

- Forvia has set ambitious targets for 2025, including increased revenue, operating margin, and reduced debt ratio. The company's debt ratio has already improved.

Introduction

About two years ago, I thought Faurecia was trading at an interesting valuation as most car suppliers were still not properly appreciated by the market. Faurecia subsequently completed the acquisition of Hella ( HLKHF ) ( HLLGY ) in a move to diversify and create additional economies of scale by becoming the seventh largest parts supplier in the world . That acquisition was completed in 2022 and the company underwent a rebranding from Faurecia to Forvia ( FURCF ) ( FAURY ). And although the world economy is pretty volatile these days, I wanted to have another look at the stock and its mid-term targets.

{kind=link}

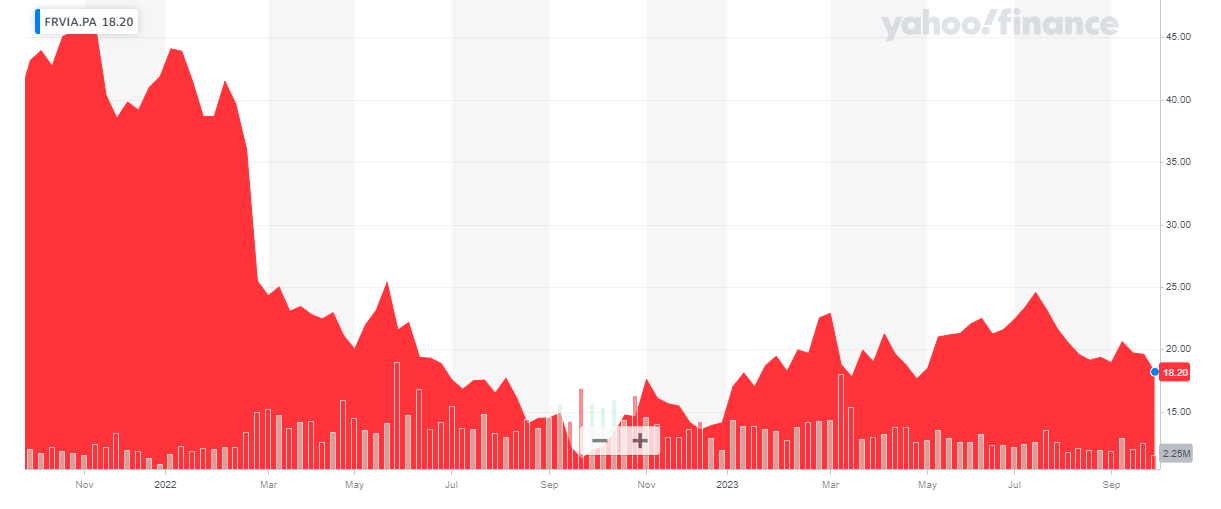

Faurecia has its primary listing in France where it’s trading on Euronext Paris with FRVIA as its ticker symbol . The average daily volume is approximately 750,000 shares per day (for a value of 14M EUR). I will use the Euro as the base currency throughout this article as that’s the currency of the company’s most liquid listing and the currency it reports its financial results in. There are currently 197M shares outstanding, resulting in a market capitalization of just over 3.5B EUR.

A look at the first semester

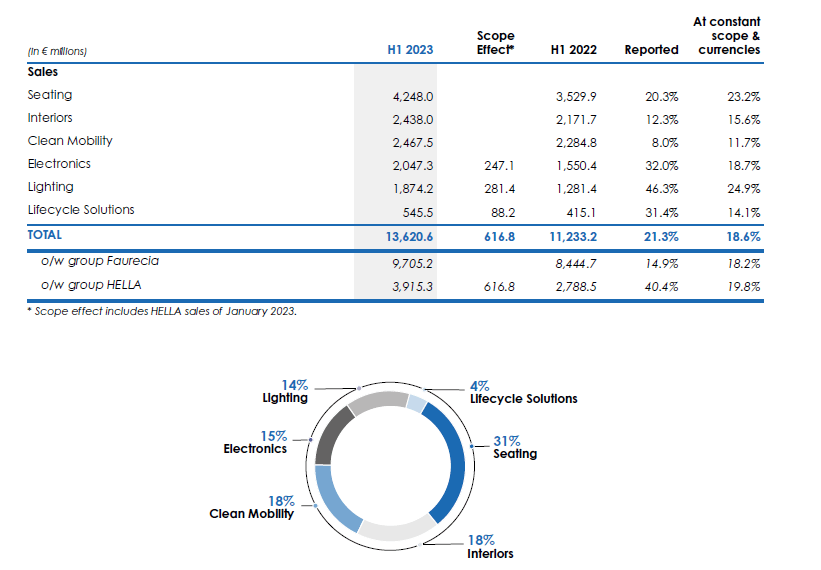

The first half of the year was a good semester for the automotive industry. The total automotive production increased by in excess of 11% to 43.3 million units and that's already pretty close to the assumption of 88 million produced units Forvia has based its 2025 targets on (see later). Forvia provides an array of products to the car manufacturers but seating is by far the most important division, representing almost a third of the total consolidated revenue, as you can see below.

{kind=link}

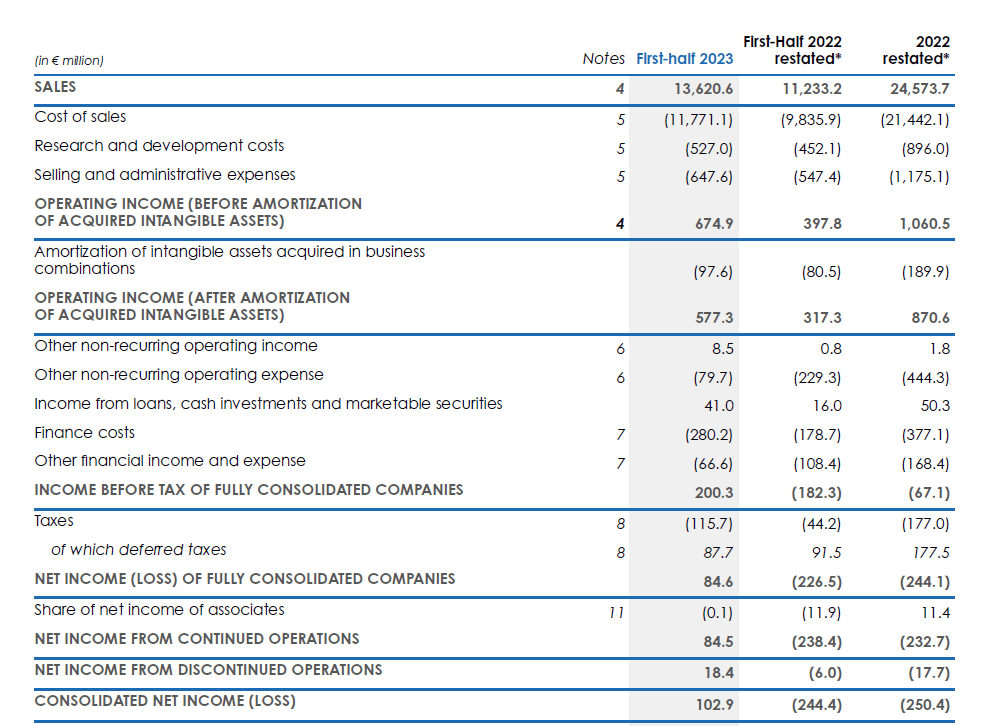

Forvia reported a total revenue of 13.6B EUR and this resulted in an operating income before the amortization of intangibles of about 675M EUR and roughly 577M EUR after the incorporation of that amortization.

{kind=link}

There were in excess of 70M EUR in net non-recurring expenses while the finance cost remains very high at 280M EUR. The total amount of interest expenses will likely remain high but Forvia is working hard to rapidly reduce the total debt position and that should have a positive impact on the total interest expenses. And while the interest income also increased, it's clear the higher interest rates on the financial markets have a negative impact on Forvia’s performance.

Despite that, the company’s first semester was still quite decent. The net income in the first semester was approximately 84.5M EUR, and after adding the contribution from discontinued operations, the reported net income was approximately 103M EUR. Unfortunately the majority was attributable to the minority owners and the EPS attributable to Forvia was just 0.14 EUR and even just 0.05 EUR per share excluding the positive impact from the discontinued operations.

This doesn’t mean the company has to be avoided. As mentioned above, a portion of the negative elements are non-recurring but also non-cash. The cash flow statement helps to understand this a bit better despite seeing the company capitalize a substantial chunk of its R&D expenses.

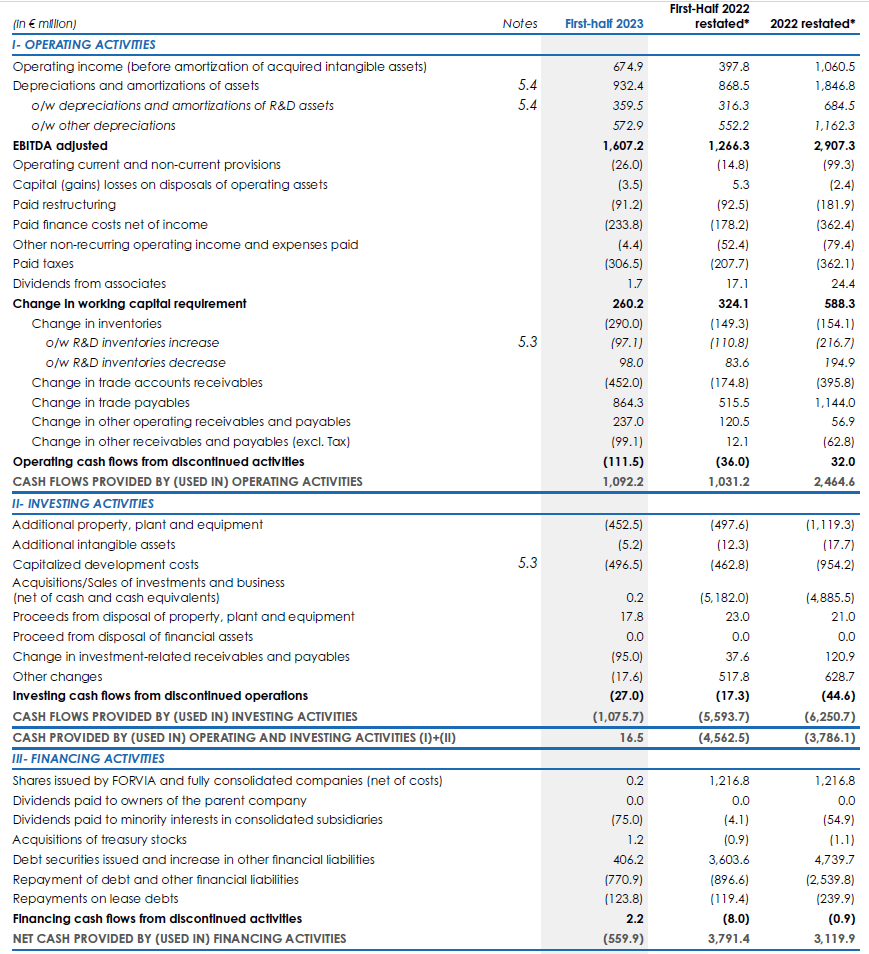

The reported operating cash flow was 1.09B EUR but this includes about 260M EUR in working capital contributions. On the other hand, the cash flow statement indicates about 306.5M EUR has been paid in cash taxes but only 30M EUR was due in H1 (the difference between the total tax calculation and the deferred taxes). On top of that, we also should deduct the 124M EUR in lease payments and the 75M EUR in dividends payable to minority interests.

{kind=link}

After making all these adjustments, the underlying operating cash flow was approximately 910M EUR and this almost covered the 950M EUR in capex and capitalized R&D. This means the majority of the free cash flow reported by Forvia (172M EUR) came from the changes in the working capital during the first half of the year.

I’m all for investing in new products as that’s what’s a leader in the sector is expected to do. But actually generating a positive free cash flow will be an important element to convince the investment community Forvia is serious about boosting its free cash flow. As part of its 2025 targets, the company expects to reduce its total capex to just 4.5% of the revenue by 2025. This should boost the net cash flow margin and accelerate the net free cash flow. The free cash flow will still predominantly be spent on debt reduction as Forvia has put forward an anticipated payout ratio of 40% for the dividend.

Thanks to the robust performance in the first semester, Forvia has now increased its full-year guidance . The company now expects to report a total consolidated revenue of 26.5-27.5B EUR ( up from 25.2-26.2B EUR) and expects a full-year operating margin of 5.2%-6.2%. This is an important development given the rather weak margin in 2022 and the 5% operating margin in the first half of the year. This means that in order to meet the lower end of the guidance, the operating margin should increase by approximately 10% in the second half of the year. That’s very encouraging to hear and it lends more credibility to the company’s targets for 2025. The improvement is mainly caused by an acceleration of the synergy benefits after the acquisition of Hella while a loss-making division in Michigan will be shut down.

{kind=link}

What about the roadmap to 2025?

About a year ago, Forvia unveiled its mid-term targets as part of its Power25 plan which discusses the company’s objectives for 2025.

By the end of 2025, the company wants to achieve a consolidated revenue of 30B EUR (that is lower than the 33B EUR it initially anticipated in 2021) with an operating margin of in excess of 7% of the revenue. The strong net profit and free cash flow result (and of course the expected higher EBITDA as well) should reduce the debt ratio to less than 1.5 times the adjusted EBITDA by the end of 2025.

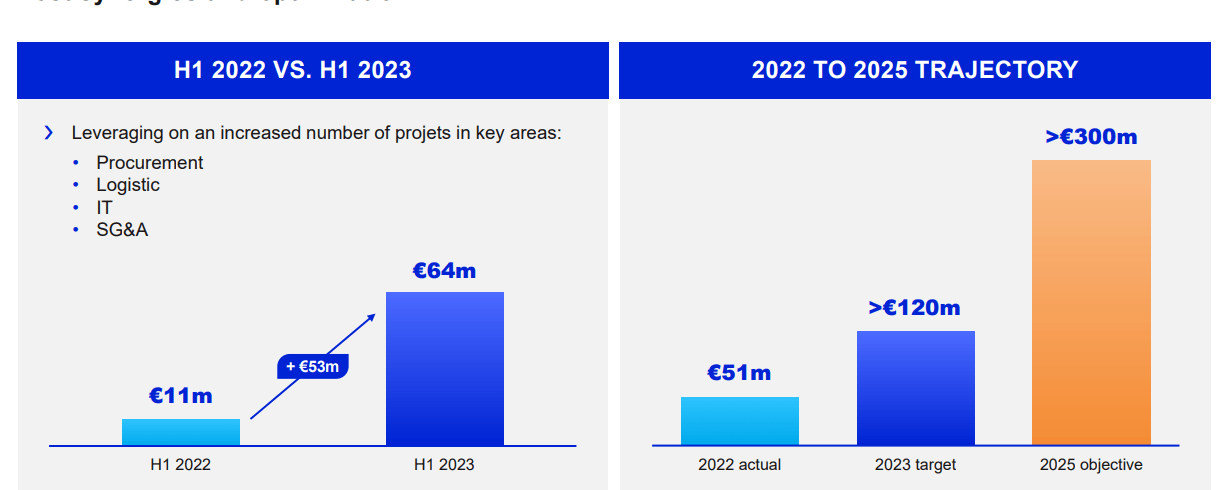

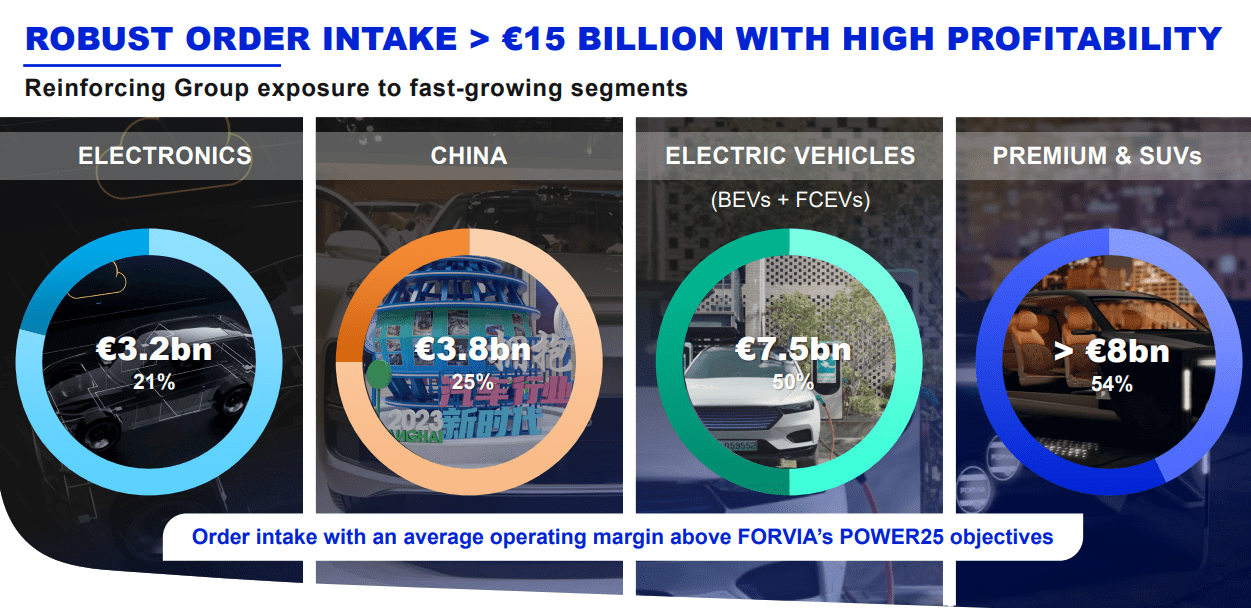

Those are ambitious targets (based on an assumed automotive production of 88 million units and including the impact of a 1B EUR disposal program which is in full swing), and it would be pretty impressive if Forvia is indeed able to increase the operating margin to 7% from the 5% it reported in the first half of the current financial year. Interestingly, the company did mention that the 15B EUR order intake is expected to have a profitability of in excess of the Power25 requirements, so that's encouraging.

{kind=link}

The debt target, on the other hand, appears to be quite achievable. As of the end of June the debt ratio had already dropped to 2.4 times the adjusted EBITDA which is a substantial improvement compared to the 3.1 ratio one year ago. Forvia also confirmed its asset disposal program remains on track and it anticipates a year-end debt ratio of 2-2.2 times the adjusted EBITDA. The company is selling a 16.66% stake in Symbio to Stellantis for 150M EUR, SAS Cockpit Modules will be sold to the Motherson Group for 540M EUR while the exhaust aftertreatment business will be sold to Cummins for 142M EUR and this should bring the total proceeds from asset disposals to the eyed 1B EUR. All transactions will be closed by the end of this year.

Investment thesis

The plans for 2025 look very attractive, and based on that guidance, Forvia is a "buy" at the current levels. That being said, I also would like the free cash flow result to actually pick up and Forvia’s guidance to gradually reduce the capex as a percentage of the revenue is a very important element for me.

I currently have a small position but I would like to see an improvement in the reported free cash flow (adjusted for working capital changes) before adding to that position. I was not the biggest fan of the Hella acquisition as Forvia paid pre-war multiples and will have to deal with increasing interest rates when the debt has to be refinanced throughout the second half of this decade.

For further details see:

Forvia: The 2025 Guidance Makes The Stock Attractive