FOX - Fox: The Upside Is Higher Than Some Believe

2023-09-25 03:55:40 ET

Summary

- Fox Corporation is a controversial investment due to its political lean, but it has the potential for double-digit earnings growth.

- The company has a strong balance sheet and impressive revenue growth, despite the decline in overall advertising.

- Analysts predict a potential RoR of over 25% for Fox, and the company has a history of beating estimates.

Dear readers/followers,

Surprisingly enough, at least to me, my position and stance on Fox Corporation ( FOX ) has become one of my more controversial picks and where I've actually received the most messages over the past few months. Investing in broadcasting and communications companies is not easy. They tend to be incredibly volatile, with a political lean, by which I also mean a political-economic lean (in that political years typically see a lot higher revenues.

It's also understandable given the broadcaster's lean that there is a host of readers that don't agree with investing in a business such as this. To those, I remind them that I don't apply political bias to any of my investments. I'm interested in making money.

And FOX is pretty damn good at making money if you buy it at the right price.

What's more, I believe that in the next few years, with the next presidential election incoming as well as other trends, FOX will be positioned for a double-digit earnings growth rate that will see my investment in the business see a double-digit, 20-40% annualized RoR for the 2025-2026E fiscal.

So, let me show you what I mean here. My latest article on the company can otherwise be found here - so this is an update.

FOX - Ignoring the politics may be impossible, but I try

So, FOX. I've been reviewing the company for about a year at this point. Journalism, broadcasting, and Media in the USA is a political firestorm, it seems like - and this is coming from someone looking in from the outside. While other nations have politically tilted news and broadcasting services, the two sides seem far clearer in the US than elsewhere in the Western world, and this has only grown more and more true over the past 24 months since I've been following and analyzing Fox.

So, first question that some readers actually have.

What makes Fox attractive?

FOX IR (FOX IR)

That, among other things. Over 10,000 employees serving the population of the country with news and broadcasting make Fox Corporation attractive. Yes, it doesn't have much straight history - the company is owned by R. Murdoch with almost 40% voting power and goes back to 2019 when it was spun off due to the Disney ( DIS ) 21st Century Fox merger.

To be clear, going through all of the company's various operations and media libraries would be an article series , so as before I'll try to keep the appeal concise, and as visual as possible.

The main two segments are Cable Networks and Television. The former focuses on producing and licensing news and sports content, which in turn moves through traditional TV cable and digital media. The second focuses on producing, acquiring, marketing, and airing television content throughout the network. This includes advertising-supported programming, 29 full-power broadcasters, and 11 duopolies. So it's a substantial and impressive operation that includes many well-known brands.

These brands are well-loved ones such as Simpsons, Family Guy, Bob's Burgers, Hell's Kitchen, MasterChef, and Next Level Chef. The company is also a sports leader, enjoying leadership around news, sports, and entertainment.

So those saying "What makes Fox attractive", I say "How can you not consider this to be attractive?"

In a world where legacy television seems to be mostly in the gutter and people are moving to streaming, Fox is one of the only operators that seems to have found a mix between appointment-based programming types that actually seems to work. By work, I mean that the company's business model generates revenues and an impressive set of net earnings.

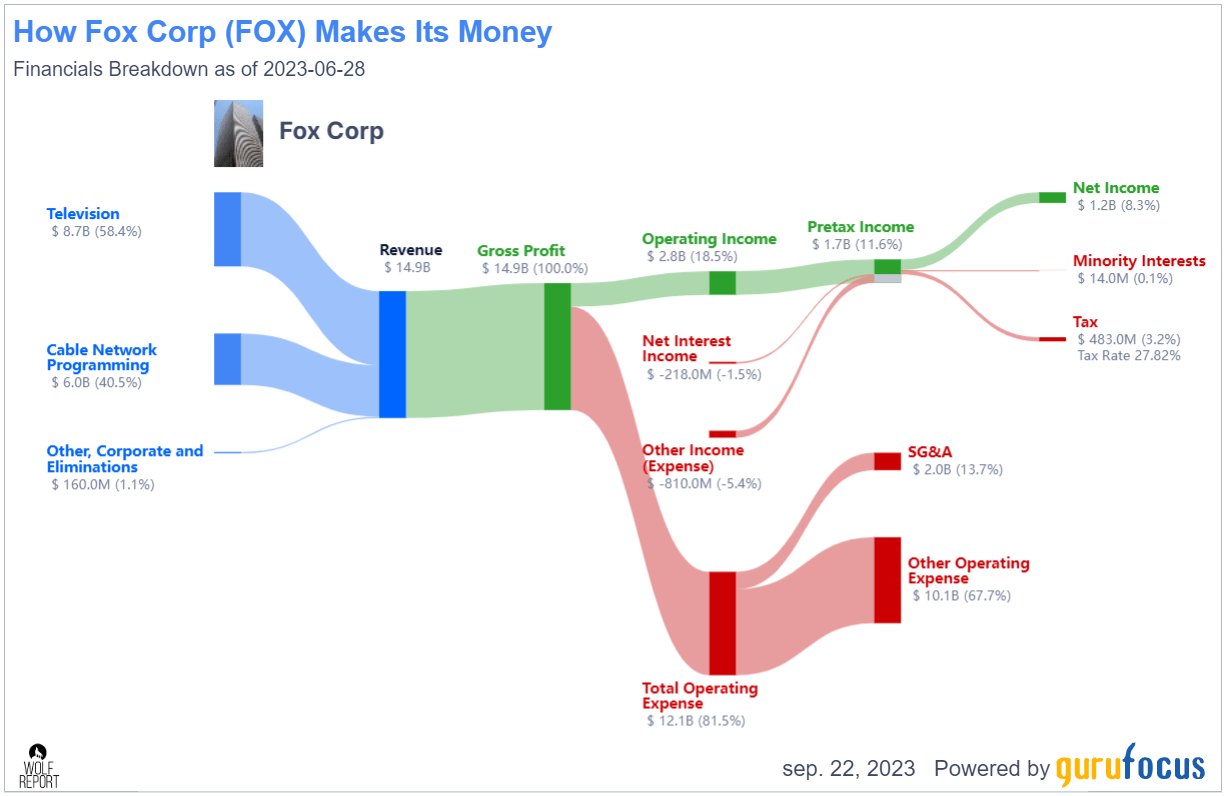

Oh, Fox has its own problems - but operating margins and profitability are not part of that. Fox is a profitable media empire - and that's more than you can say for some other media empires. Here is a snapshot of what can be seen in terms of its business model, and where the costs for the company are going.

{kind=link}

FOX revenue/net (GuruFocus)

And, equally obvious, I'm far from the only one to be positive on Fox. All you have to do is a basic analysis of the projected company free cash flow to see that even a conservative estimate here would put the company well above $35/share on that basis alone, compared to the current price of $29.5.

My own association with Fox is relatively small. It's primarily US-based, and being a European, I get most of the programming through third parties or licensing. However, within the US, it has availability in 70 million households, for News and Business, with FOX Network being available essentially in every household in America. (Source: Annual Report )

And what's more, the company has been able to deliver significant, double-digit revenue growth rates over time, with impressively low leverage given what is usually common in the communications industry. It's at almost 8x interest coverage with a debt/leverage to EBITDA of below 3.3x. (Source: GuruFocus)

And the latest results do not make things worse either. The company reported 4Q23 and full-year results back in August of 2023. The company, despite some of the headlines with certain personalities departing, recorded record annual revenue as well as record EBITDA levels. These positive results were not just in sports, but also good growth in Tubi. This was a 3% annual fee revenue growth, and 9% television growth, in the face of a 4% advertising decline. Unlike some other media, the company is able to grow its other vectors faster than the expected decline in overall advertising.

Here in Sweden, plenty of news outlets are taking a chainsaw to their departments due to the lower advertising revenues across the board. But Fox is reporting increased quarterly net income to the tune of almost $370M, compared to $300M YoY - though some of that was restructuring and fair-value investment estimates. EBITDA was down on a quarterly basis, and it's fair to say that Fox in no way is immune to cost trends, since expenses were up. But much of this was also investment CapEx going into Tubi as well as programming rights and higher amortization.

Full-year results are where Fox shines in the 2023 fiscal. 7% revenue growth, affiliate fees up 3%, 8% growth in television, and a 12% advertising increase, going against the grain in such of an industry.

Full-year net income was also up and at a record level, coming in at $1.25B with an annual EBITDA of almost $3.2B.

The expense mix for this company is primarily from programming rights, production costs, broadcasting costs, and investments.

Questions that I would be looking closely at on a forward basis to determine the continued appeal of this investment is how Fox protects its premium sports content. The pay-tv model seems still to be working quite well, and the company echoes this, believing the pay-tv to be part of its business model for many years to come (Source: 4Q23 Fox Corporation). The notion that Fox is an over-politicized channel is also disproved, at least to me, by the fact that even with ex-political revenues, the company's advertising including digital is up. We're talking things like Auto, finance, health, retail, and other things.

I say that Fox has one of the strongest and most impressive balance sheets in the entire communications industry, as it stands in the USA today. This to me is a massive advantage going into this environment that we're seeing here - and that's what I'll continue to focus on as one of the major advantages.

While recent trends in certain personalities leaving the network and other political concerns are not invalid, it does not to me make this an uninvestable, or even poor company.

Fox is a great investment because the numbers, to me, dictate that it is. So let me clarify the current upside I see in those numbers.

Fox Corporation - The upside seems clear enough to me.

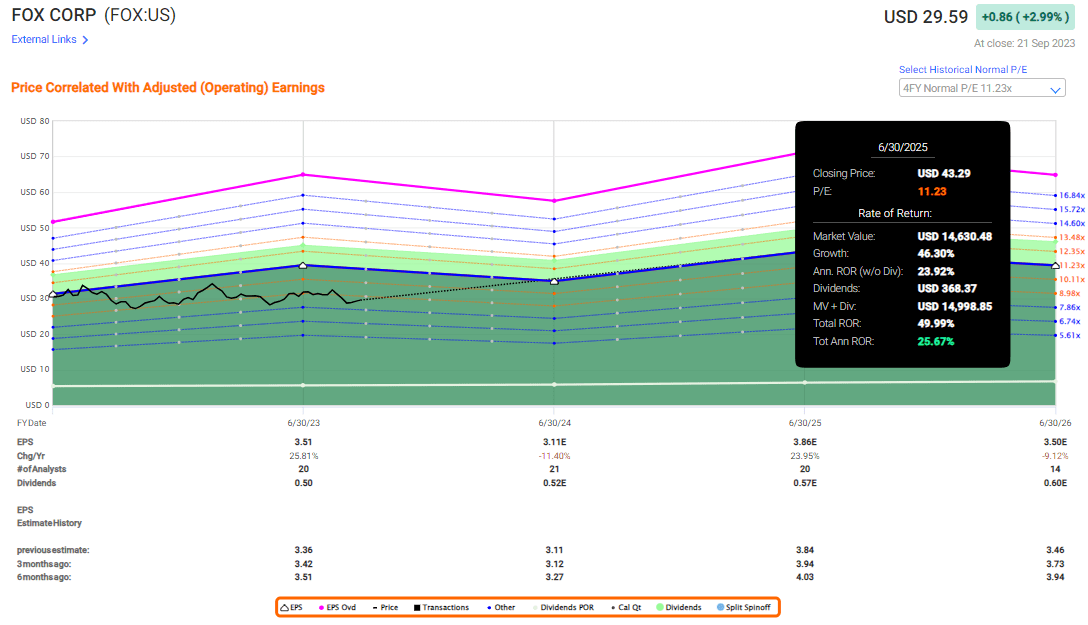

So, the upside to Fox is clear to me. If you look at the company's P/E it tends to trade between 11-15x P/E, and currently trades at 8.65x. If we see normalization to 11.23x, which is 4-year normalized, by 2025E when the earnings spike is currently estimated to hit (about 2 years from now), that's a potential RoR that looks like this.

{kind=link}

Fox Upside (F.A.S.T graphs)

Fox has an upside of over 25% here on an annual basis. How likely are these estimates to actually materialize?

Fox does not miss estimates. Analysts hit 75% of the time on a 1-year basis - the rest of the time the company beats estimates. This gives me a fairly good degree of conviction that the directional trend is going to be somewhat correct - just as I expect things, based on continued inflation, programming costs, and somewhat lower political ad contributions, to somewhat decline in this next fiscal - though I would estimate it at 9.5%, not 11.5% decline.

I do want to point out though, that Fox quite often trades at a P/E closer to 15x. That was the case in 2020 as well as 2021 and at times in 2022 as well - close to it.

If we see a 15x P/E for this company, then your total upside could be closing in on triple digits. I don't view this as likely or conservative enough - so I would be careful investing with this as a basis.

However, what I am saying is that I consider it less likely that Fox will decline further. The company is already at a low level. I don't see it going much lower than this. The only time it did was during COVID-19. If you invested at that time and kept an eye on valuation, you could have seen returns of over 100% in less than a year (Source: F.A.S.T graphs, S&P Global).

The company's yield is nothing to write home about - 1.76% - but it's not terrible either.

What do other analysts say about Fox? I would invest in FOXA over FOX, but this doesn't change what's presented above in terms of upside, or the statistical accuracy. FOXA is now at $32.14. 21 analysts follow the company, giving the symbol a range of $28/share on the low side to $44/share on the high side, averaging at around $37/share, with 9 out of 21 analysts currently at "BUY" or equivalent rating.

Most are currently at hold - but this is something we see as quite common here in this market environment, not just for Fox but for other companies as well. People are understandably hesitant to trust their money to the market at this time.

That's why I focus on the cheaper and better opportunities available, such as a broadcaster with a realistic 20%+ annualized upside.

I continue to go against the grain here. Fox is a "BUY" to me - I own the company and intend to buy more.

Here is my update in terms of the company thesis.

Thesis

- Fox is one of the more appealing broadcasters and television companies in all of the US. It has solid fundamentals, it has a history, and it seems to have a great future, going forward. Its solid fundamentals and growth prospects make me consider it a "BUY" at a conservative share price.

- The current targeted share price I would consider fair based on targets and estimates is around $38/share. This is a reiteration of my previous share price target.

- Despite ongoing political issues for the broadcaster, I view Fox mostly on a financial level and as a fundamental investment. On that basis, this is a very attractive overall company with a great upside, and one I continue to be happy investing in.

- I consider Fox Corp a "BUY" here.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (Italicized) .

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company is no longer cheap as such, but I still view it as a "BUY" here.

For further details see:

Fox: The Upside Is Higher Than Some Believe