DTM - FPL: Underwhelming Compared To The Index But Not Too Bad

2023-04-18 17:29:29 ET

Summary

- Master limited partnerships are among the best investment vehicles for retirement income, but they are difficult to use due to tax problems.

- First Trust New Opps MLP & Energy Fund invests in a portfolio of these companies and is structured as a corporation so it avoids the tax complications of the partnership structure.

- The FPL closed-end fund has severely underperformed the MLP index and has a lower yield.

- The 7.39% yield appears reasonably secure.

- The fund is currently trading at a very attractive discount on the net asset value.

For quite some time now, master limited partnerships, or MLPs, have been among the favorite investment vehicles of those looking for income. This is not surprising, as these companies offer a number of very appealing things for this group such as generally stable cash flows and high yields. In fact, the yields of these companies are even more appealing than one might think because their distributions come with certain tax advantages that corporate dividends do not possess.

Unfortunately, these partnerships are not without their flaws. In particular, it can be difficult to include them in most retirement accounts due to tax rules with regard to the distributions paid by partnerships. In addition, it can be difficult to put together a diversified portfolio of these companies without having access to a considerable amount of capital. These flaws are rather disconcerting because otherwise, most midstream partnerships would be some of the perfect investment vehicles for someone looking to generate income in retirement.

One way around both of these problems is to purchase shares of a closed-end fund, or CEF, that specializes in investing in master limited partnerships. These funds are typically structured as corporations so they avoid all of the tax problems that would otherwise be present if a partnership is put into a retirement account. In addition, these funds provide easy access to a diversified portfolio of assets that can typically deliver a higher yield than any of the underlying assets possesses.

In this article, we will discuss the First Trust New Opps MLP & Energy Fund ( FPL ), which is one such fund that falls into this category. As of the time of writing, the fund yields 7.39%, which is admittedly a little below the yield of the Alerian MLP Index ( AMLP ) but is still reasonable for any income-focused investor. I have discussed this fund before, but some time has passed since that article so obviously a few things have changed. This article will focus specifically on those changes as well as provide an updated analysis of the fund’s financial condition. Let us investigate and see if this fund could be a worthy addition to your portfolio today.

About The Fund

According to the fund’s webpage , the First Trust New Opportunities MLP & Energy Fund has the stated objective of providing its investors with a high level of total return. That is not particularly surprising considering that this fund primarily invests in common equity. As we can see here, the fund’s portfolio consists entirely of common stock, along with a small amount of cash:

CEF Connect

Please note that in this case, the term “common stock” refers to both stocks issued by corporate entities as well as the partnership units issued by master limited partnerships or limited liability companies. The reason that the fund’s objective is not surprising in light of this is that common equity by its very nature is a total return vehicle. After all, investors purchase these securities both for the income that they pay out through dividends and distributions as well as the capital gains that typically accompany the growth and prosperity of the issuing company. In the case of many of these companies though, the majority of the return comes in the form of direct payments from the issuing company. This is because most midstream master limited partnerships have fairly low growth rates, which limits their capital gains potential.

As a result, they distribute a substantial percentage of their cash flows to investors in order to provide a return that is comparable to what companies in other industries can provide. As the market does not typically assign high multiples to the common equity issued by these companies, these dividends and distributions are a significant percentage of the market value, which equates to a high yield. This high yield is quite evident in the fact that the Alerian MLP Index currently yields 7.82%.

As my regular readers are no doubt well aware, I have devoted a considerable amount of time to discussing midstream corporations and partnerships here at Energy Profits in Dividends and on the main Seeking Alpha site. In fact, these companies have been something of my specialty for the past six or seven years. As such, most of the companies that comprise the largest positions in the fund will likely be familiar to most readers. Here they are:

First Trust

I have discussed all of these companies except for Hess Midstream ( HESM ) multiple times over the years, so they should all be reasonably familiar. The majority of them are among the largest and most financially secure pipeline operators in the United States. In fact, the sole exception here is Cheniere Energy ( LNG ), which is one of the largest producers of liquefied natural gas in the world. For the most part, these are among the best companies in the industry. Overall, I see nothing particularly wrong with the selection of companies that make up this portfolio.

However, one thing that we do note is that the fund’s portfolio is not as diversified as we really want to see. As I have noted in various past articles, I do not generally like to see any individual position in a fund accounting for more than 5% of the fund’s portfolio. That is because this is approximately the point at which a given asset begins to expose the fund to idiosyncratic risk. Idiosyncratic, or company-specific, risk is that risk that any asset possesses that is independent of the market as a whole. This is the risk that we aim to eliminate through diversification, but if the asset accounts for too much of the portfolio, the risk will not be completely diversified away. Thus, the concern is that some event may occur that causes the price of a given asset to decline when the market as a whole does not, and if that asset accounts for too much of the portfolio, then it could end up dragging the entire fund down with it.

As we can see above, there are four companies that each account for more than 5% of the portfolio. Thus, any potential investor should ensure that they are willing to be exposed to the risks of these companies individually before taking a position in the fund.

As I have pointed out before, it is not uncommon to see a midstream fund like this have a high weighting to one or a few companies. This is because there are a very limited number of such companies in the United States. The Alerian MLP Index only contains sixteen companies and when we consider midstream corporations like Kinder Morgan ( KMI ), The Williams Companies ( WMB ), ONEOK ( OKE ), and a few others, there are still not likely to be more than thirty or forty companies that a fund like this can even invest in. Thus, by default, it will almost certainly have to have something with more than a 5% weighting. This one does not do as poorly in this area as some midstream funds though, as the First Trust New Opportunities MLP & Energy Fund has 65 total positions as of the time of writing and there is nothing with over a 10% weighting as some comparable funds possess.

There have been relatively few changes since we last discussed this fund. In fact, the only change to the largest positions in the fund is that DT Midstream ( DTM ) was removed and replaced with Plains All American Pipeline ( PAA ). This change is not particularly surprising as a few other funds have also done the same swap. DT Midstream has been one of the poorest performers in the market over the past year and, while it does have strong growth prospects, arguably it was previously overvalued. Plains All American Pipeline, meanwhile, has benefited from the rising production of crude oil in the Permian Basin over the past year. The fact that there were relatively few changes may lead us to expect that this fund has a fairly low turnover, but that is not actually the case. Indeed, the fund had a 57.00% annual turnover in 2022.

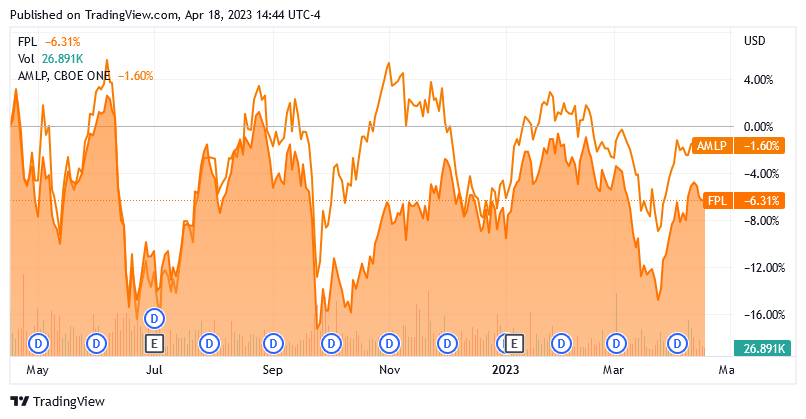

Although this is not especially high for an equity closed-end fund, it is still much higher than most index funds possess. The reason that this is important is that it costs money to trade stocks or other assets, and these expenses are billed directly to the fund’s shareholders. This creates a drag on the performance of the portfolio and makes management’s job more difficult. After all, the fund’s management needs to generate a sufficiently high return to cover its expenses and still have enough left over to satisfy the investors. That is something that very few funds manage to achieve on a consistent basis, and it is one of the reasons why most actively managed funds fail to beat their benchmark indices over any extended period of time. This one is certainly not an exception to this. As we can clearly see here, the Alerian MLP Index outperformed this fund by quite a lot over the past year:

{kind=link}

The index fund also has a higher yield, so we cannot count on that to close the difference. Overall, the index fund delivered a much larger total return over the period than the First Trust New Opportunities MLP & Energy Fund, although both funds did deliver a positive total return when we consider that both funds have a yield that is greater than their share value declines. In addition, both funds managed to outperform the S&P 500 Index (SP500), which has generally been true for anything related to the oil and gas industry over the past two years.

Admittedly, the Alerian MLP Index is not a perfect benchmark to use for the First Trust New Opportunities MLP & Energy Fund. One reason for this is that the First Trust fund includes a number of things that are not master limited partnerships. For example, as we can see here, 19.24% of the fund’s assets are invested in electric utilities:

First Trust

Electric utilities as a group performed worse than most midstream master limited partnerships over the past year. The presence of these companies likely dragged on the fund’s performance compared to the index. At the same time though, the presence of the electric utilities in the fund’s portfolio does offer some diversification benefits as well as improves its exposure to the energy transition, which is a major theme for this fund. We also see three midstream corporations among the fund’s largest positions, although the performance of these companies tends to be pretty similar to the performance of midstream partnerships.

Leverage

One of the interesting things about closed-end funds like the First Trust New Opportunities MLP & Energy Fund is that they have the ability to employ certain strategies that have the effect of boosting their yields and returns beyond that of the underlying assets. One of the strategies that is employed to accomplish this is the use of leverage. In short, the fund borrows money and then uses that borrowed money to purchase the common equity of master limited partnerships, corporations, and utilities. As long as the purchased securities have a higher total return than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the overall yield of the portfolio. Since this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. This, therefore, could account for some of the underperformance of this fund relative to the Alerian MLP Index. As such, it is important for us to ensure that the fund does not employ too much leverage as that would expose us to too much risk. I generally do not like to see a fund’s leverage exceed a third as a percentage of its assets for this reason. Fortunately, this fund fulfills that requirement. As of the time of writing, the First Trust New Opportunities MLP & Energy Fund had levered assets comprising 20.23% of the portfolio. Thus, it appears that this fund is striking a reasonable balance between risk and reward.

Distribution Analysis

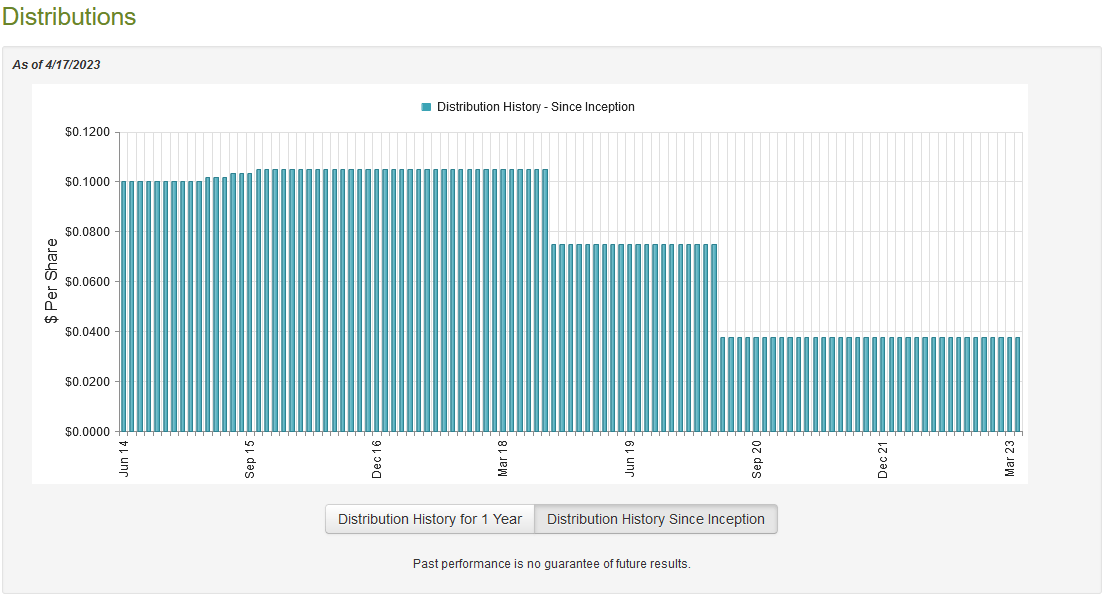

As mentioned earlier in this article, the primary reason why many people purchase units of midstream master limited partnerships and corporations is because of the incredibly high yields that most of these companies possess. The same is true for utility companies, although the yield of these stocks is not typically as attractive. This fund purchases these securities and then applies a layer of leverage to artificially boost the yield beyond that possessed by the stocks. Thus, we can assume that this fund will have a fairly high yield itself. This is certainly true, as the First Trust New Opportunities MLP & Energy Fund currently pays a monthly distribution of $0.0375 per share ($0.45 per share annually), which gives it a 7.39% yield at the current price. That is certainly a reasonable yield for nearly anybody that is seeking income. Unfortunately, the fund has not been particularly consistent with its distribution over its history:

{kind=link}

As we can see, the fund’s distribution has steadily declined since September 2018, as there have been two distribution cuts since that time. The second of these was certainly not unexpected, however. In April 2020, crude oil prices hit an all-time low, with the price of West Texas Intermediate briefly going negative. This was largely due to the steep reduction in demand that accompanied the pandemic and the lockdown orders. This situation resulted in many upstream companies cutting back on their production growth plans and resulted in some of the growth projects that midstream companies had under development no longer being needed.

As I have pointed out in numerous previous articles, the cash flows of most midstream corporations and partnerships held up just fine, but many of them still cut their distributions. This caused the fund’s income to decline and naturally, it ended up cutting its own distribution in response. The disappointing thing here is that this fund has not raised its distribution since that time, despite the fact that the sector has largely recovered and many of its peer funds have begun raising their distributions.

However, it is important to keep in mind that anyone buying today will receive the current distribution at the current yield. As such, the fund’s history is not exactly the most important thing. Rather, what we are most concerned with is whether the fund can maintain its current distribution going forward.

Unfortunately, we do not have an especially recent document that we can consult for the purposes of our analysis. The fund’s most recent financial report corresponds to the full-year period that ended on October 31, 2022. As such, it will not contain any information regarding the fund’s performance over the past few months. That is disappointing because energy prices have weakened considerably since October, particularly in the case of natural gas. However, crude oil peaked in the middle of 2022 and then started to decline for the rest of the year so this report should give us some idea of how the fund handled that volatility. During the full-year period, the First Trust New Opportunities MLP & Energy Fund received $3,933,995 in dividends along with $12,918 in interest from the assets in its portfolio. This gives it a total investment income of $3,946,913 over the period. However, it is important to note that this figure does not include any distributions that it received from the master limited partnerships contained in the portfolio, as those distributions are considered either a return of capital or capital gains depending on the situation. Interestingly, the fund’s net investment income actually came in at $6,444,372 over the year due to substantial tax benefits. That was the amount that the fund had available to pay distributions to its own shareholders after covering all of its expenses.

Unfortunately, this amount was not sufficient to cover the $10,940,992 that the fund actually paid out to its shareholders. At first glance, this is likely to be concerning as the fund had insufficient net investment income to cover the distribution.

However, the First Trust New Opps MLP & Energy Fund does have other methods through which it can obtain money to cover the distribution. For example, it receives a considerable amount of cash from master limited partnerships that is not included in net investment income. The fund also reported capital gains from the strong performance of pretty much everything in the energy sector over the period. During the full-year period, the fund had net realized gains of $10,172,548 and had another $9,665,186 in net unrealized capital gains. The fund’s assets increased by $8,968,686 even after paying its distributions and buying back more than $6 million of its own stock.

Overall, this fund easily covered the distribution with a great deal of money left over. There is nothing to worry about here in terms of distribution sustainability.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a sure-fire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the First Trust New Opportunities MLP & Energy Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund’s assets for less than they are actually worth. This is certainly the case with this fund today. As of April 17, 2023 (the most recent date for which data is currently available), the First Trust New Opportunities MLP & Energy Fund has a net asset value of $7.15 per share but the shares currently trade for $6.10 each. That gives the shares a 14.69% discount to net asset value at the current price. This is an extraordinarily large discount for any fund, although it is in line with the 14.33% discount that the shares have had on average over the past month. Overall, the price looks very reasonable here.

Conclusion

In conclusion, the First Trust New Opportunities MLP & Energy Fund looks like a reasonable way to play the energy transition and generate a high yield at the same time. Admittedly, though, I am a bit underwhelmed with the First Trust New Opps MLP & Energy Fund because of the severe underperformance relative to the Alerian MLP Index. With that said, this fund is a bit more diversified and trades at a substantial discount to the net asset value, so First Trust New Opps MLP & Energy Fund certainly looks acceptable.

For further details see:

FPL: Underwhelming Compared To The Index But Not Too Bad