FRA - FRA: A Good Way To Hedge Your 2024 Interest Rate Risk

2023-12-20 14:58:52 ET

Summary

- The BlackRock Floating Rate Income Strategies Fund Inc specializes in providing investors with a high level of current income, with an attractive 11.97% yield.

- The FRA closed-end fund invests in floating-rate securities, which are stable in terms of price regardless of interest rate movements.

- While the FRA fund has not seen significant gains in the current market environment, investors have made a 4.50% total return in four months.

- There are reasons to believe that bonds are overpriced right now, so FRA could help you hedge your interest-rate risk.

- The fund is managing to fully cover its distributions and trades at a discount to net asset value.

The BlackRock Floating Rate Income Strategies Fund Inc ( FRA ) is a closed-end fund, or CEF, that specializes in providing investors with a very high level of current income. The fund's very attractive 11.97% yield stands as a testament to its success in this area, as that is easily enough for many retirees or other income-seeking investors to satisfy their wants and needs in most areas of the United States. After all, that yield works out to $119,700 in annual income from a $1 million portfolio.

As the name of the fund suggests, the BlackRock Floating Rate Income Strategies Fund invests in floating-rate securities, which tend to be very stable in terms of price regardless of interest rate movements or macroeconomic events. This further adds to the fund's ability to provide investors with a high degree of safety.

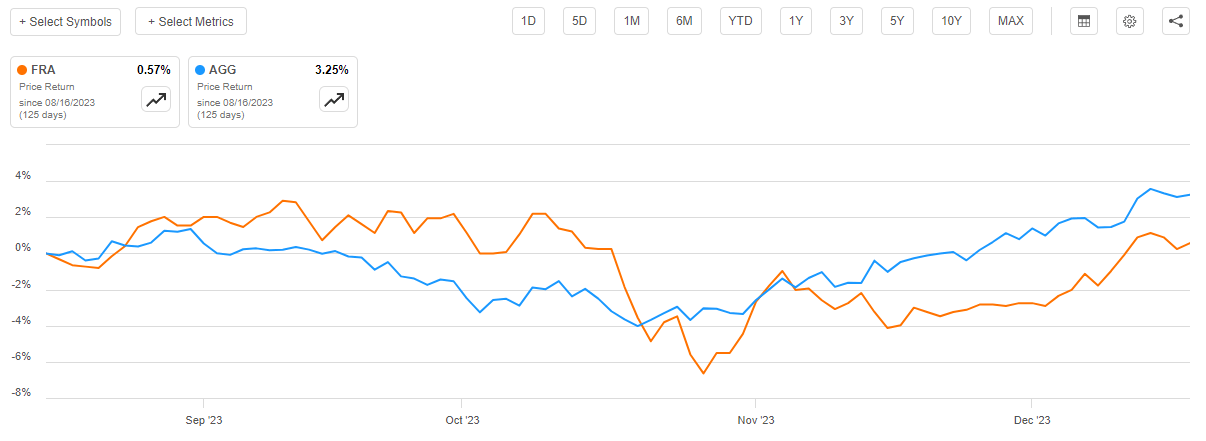

As regular readers may recall, we last discussed this fund in the middle of August. Obviously, the conditions in the market environment have changed significantly since that time. In August, the market was beginning to digest that the Federal Reserve might actually be serious about its "higher for longer" narrative and was selling off bonds and other debt securities, which had the effect of boosting yields. Today, the market is experiencing euphoria as it eagerly anticipates the return of quantitative easing and very low-interest rates. Unfortunately, this fund has not been an especially big beneficiary of that overall market strength. As we can see here, shares of the BlackRock Floating Rate Income Strategies Fund have been almost completely flat since the last time that we discussed it:

{kind=link}

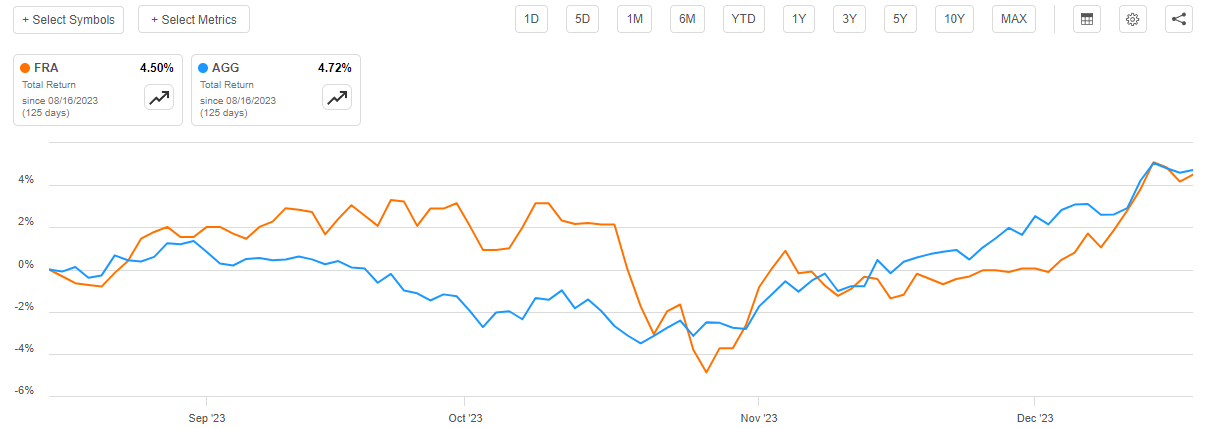

This is generally what we would expect from floating-rate securities though since their price tends to be pretty stable. They do tend to deliver relatively high yields though, especially in today's environment with short-term interest rates at more than 5.50%. The fund pays the money that it receives from these securities to its investors, which causes it to have a high distribution yield as well. Thus, in order to properly evaluate the fund's return, we should include the distributions that investors in the fund actually received. When we do that, we see that investors in the BlackRock Floating Rate Income Strategies Fund have actually made 4.50% in four months:

{kind=link}

That is not really a bad return for four months, although it certainly has not been as impressive as the gain in some other asset classes over the same period. Many income investors tend to be reasonably satisfied with a return of about 1% every month though, which is what this fund has managed to reliably deliver over the period.

Unfortunately, some investors may be losing interest in floating-rate securities due to the fact that these securities are actually hurt by falling interest rates. The Federal Reserve is generally expected to reduce the federal funds rate over the next year, so such investors may want to avoid floating-rate securities and funds that heavily invest in such. However, there could still be some reasons to include these securities and potentially this fund in your portfolio today.

About The Fund

According to the fund's website , the BlackRock Floating Rate Income Strategies Fund has the primary objective of providing its shareholders with a high level of current income while preserving the value of its principal. As is usually the case with BlackRock funds, the BlackRock Floating Rate Income Strategies Fund includes a very detailed description of its objectives and strategies on the webpage. Here is what it states:

BlackRock Floating Rate Income Strategies Fund, Inc.'s investment objective is to provide shareholders with high current income and such preservation of capital as is consistent with investment in a diversified, leveraged portfolio consisting primarily of floating rate debt securities and instruments. The Fund seeks to achieve its investment objective by investing, under normal market conditions, at least 80% of its assets in floating rate debt securities, including floating or variable rate debt securities that pay interest at rates that adjust whenever a specified interest rate changes and/or which reset on predetermined dates (such as the last day of a month or calendar quarter). The Fund invests a substantial portion of its investments in floating rate debt securities consisting of secured or unsecured senior floating rate loans that are rated below investment grade. The Fund may invest directly in such securities or synthetically through the use of derivatives.

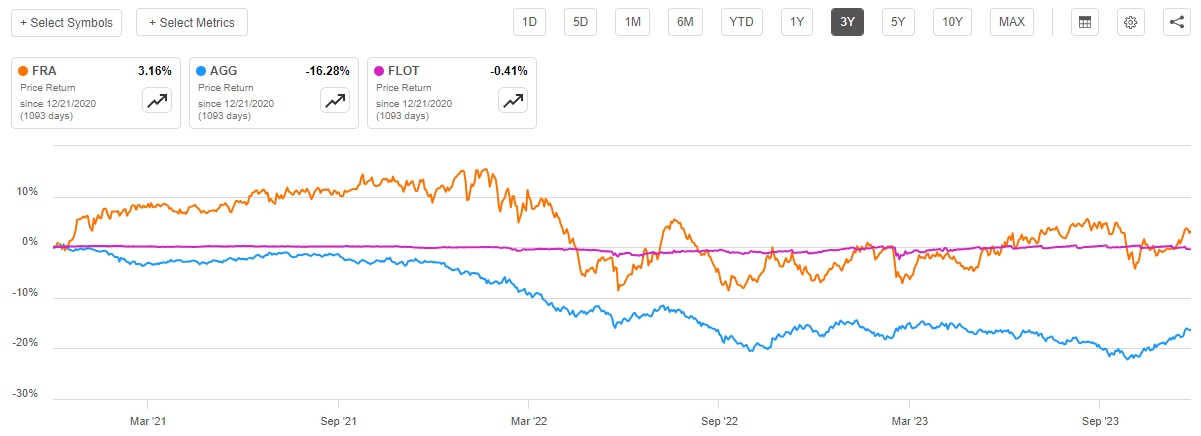

As we can clearly see here, the fund invests in a portfolio that primarily consists of floating-rate debt securities. These securities have a significant advantage over ordinary fixed-rate debt during periods of rising interest rates. This is something that has helped these securities a great deal over the past three years. We can quite clearly see this by looking at the performance of the BBG US Floating Rate Notes 5 Yrs. And Less Index, iShares Floating Rate Bond ETF ( FLOT ) compared to the performance of the Bloomberg U.S. Aggregate Bond Index over the period. Here is how the two indices compared over the past three years:

{kind=link}

As we can clearly see, the floating rate note index did not really vary much at all over the period, despite the bursting of the post-pandemic bond bubble. However, the traditional bond index handed its investors very severe losses. This comes from the reason why bond prices vary inversely with interest rates. In short, a newly issued bond will have a yield that corresponds to the market interest rate at the time of issuance. As such, during a period of rising interest rates, it will have a higher yield than an older bond that was issued when rates were lower. Nobody will ever pay full price for the older, lower-yielding bond in that situation unless the price adjusts so that it delivers a comparable yield to the brand-new bond with otherwise identical characteristics.

Floating-rate securities do not suffer from this problem because they will always deliver a yield that is competitive with similar bonds due to the adjustable interest rate. As such, the price of these securities will remain relatively stable no matter what interest rates do. This means that they avoid the losses that ordinary bonds suffer when interest rates rise. Unfortunately, they also do not benefit when interest rates decline. This may make some investors avoid them given that interest rates are expected to decline significantly over the coming year, but avoiding these securities may not be a wise decision. We will discuss this in more detail in just a few moments.

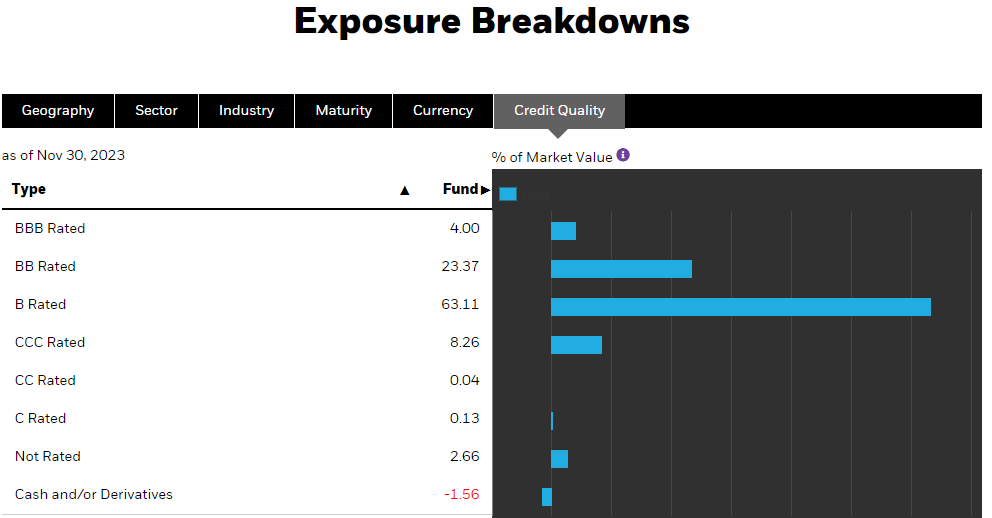

Floating-rate debt securities are typically backed by companies that may not have the strongest balance sheets. This is one reason why these securities are frequently called "leveraged loans." Essentially, this fund is investing in junk bonds that have adjustable interest rates. That is something that may be concerning to highly risk-averse investors who are worried about the safety of their principal. After all, we have all heard about how financially weak companies tend to be at a much higher risk of defaulting on their debt obligations. However, the risk of default-related losses may not be as great here as many investors may fear. We can see this by looking at the credit ratings that have been assigned to the securities in the fund's portfolio. Here is a high-level summary:

{kind=link}

An investment-grade security is anything that is rated BBB or higher. As we can clearly see, that only describes 4.00% of the total assets of this fund. The remainder of the fund's assets are classified as speculative-grade securities, which are what are colloquially known as "junk bonds." However, not all junk bonds are of equal risk or quality. We can see above that 86.48% of the fund's assets are invested in BB-rated or B-rated securities. These are the two highest possible ratings for speculative-grade securities. According to the official bond ratings scale , issuers whose securities have either of these two ratings have sufficient financial capacity to carry their existing debt even in the event of a short-term economic shock such as a recession. As such, we probably do not need to worry too much about the default risk that is associated with these securities, although it will certainly be higher than that of investment-grade assets. When we combine this 86.48% weighting with the 4.00% weighting to the BBB-rated securities, we can see that 90.48% of the fund's assets are invested in securities that are B-rated or higher. That is a fairly high percentage weighting towards the higher speculative-grade tiers so this fund may be a little safer than some of its peers.

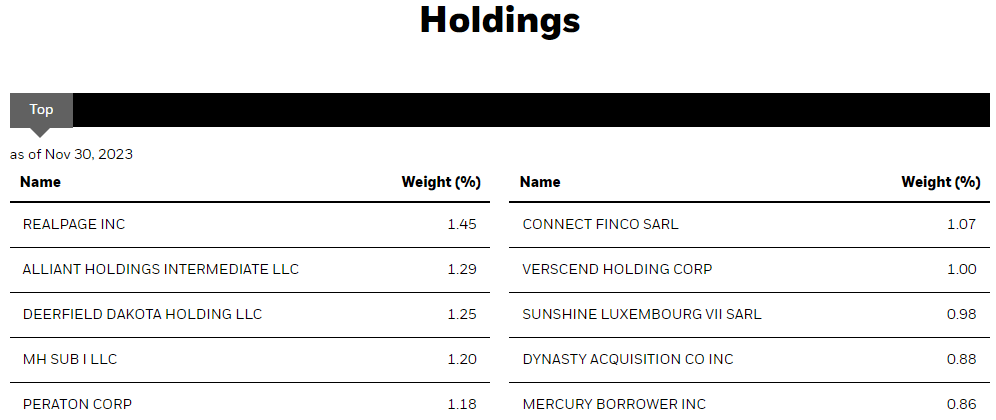

The fund also reduces its risk of losses to defaults by ensuring that only a very small percentage of its assets are exposed to any individual issuer. Here are the largest positions in the fund:

{kind=link}

As we can immediately see, there is nothing in here that has more than a 1.45% weighting. As regular readers on the topic of closed-end funds are likely aware, I generally do not worry much about idiosyncratic risk if all asset weightings are below 5% of the portfolio because that is about the point when the performance of any single security can begin to affect the fund as a whole. In this case, these weightings are so low that even a default from one of the largest positions in the fund should be easily offset by the coupon payments coming in from the other securities. It is unlikely that we would even notice the loss when evaluating the fund as a whole.

RealPage, the largest holding in this fund, is a software company that provides property management software for both residential and commercial properties. Unfortunately, this is a business that has gotten the company into trouble recently as many renters across the country are very angry about surging rents that have been seen in some metro areas over the past few years. An article from Reuters explains:

The U.S. Justice Department has thrown its weight behind private lawsuits accusing technology company RealPage of conspiring with property managers and owners to overcharge rent for student and multifamily housing.

…

The class-action lawsuits on behalf of students and other renters claim landlords have shared non-public information - including vacancy data - with RealPage and relied on its algorithms to keep rental prices inflated above competitive levels.

I cannot really comment on the merits of this lawsuit, as it seems that politics may play a role in its outcome. It is generally difficult to actually fix prices in rental real estate due to the lack of any major player in most markets. However, regardless of the merits of the suit, the company could incur significant costs fighting it and that could put pressure on the company's ability to service its debt. Investors in this fund may want to keep an eye on this case, however as RealPage is not a public company anymore, it can be difficult to truly analyze what impact these lawsuits could have on the company's ability to service its debt. Thus, it is uncertain what impact this could have on the fund's portfolio.

Interest Rate Analysis

Earlier in this article, I mentioned that investors may want to consider having some exposure to floating-rate assets in their portfolio despite the fact that they do not benefit from declining interest rates. The rationale for this comes from the fact that the market may have come too far too fast.

In a few recent articles, I have stated that the market is currently expecting that the Federal Reserve will cut interest rates six times over the course of 2024. According to a recent article from Barrons:

Investors are penciling in even more cuts to interest rates following the latest news on monetary policy from the Federal Reserve.

Federal Open Market Committee members updated their projections for future interest rates on Wednesday. Officials' median estimate now calls for the federal funds rate to end 2024 at 4.6% - implying three quarter-point cuts from the committee's current target range of 5.25% to 5.50%. That compared with futures-market pricing before the meeting that pointed to a target rate of around 4.00% to 4.25% at the end of 2024, which would mean four or five quarter-point cuts.

Markets took an even more dovish message from the committee's statement announcing the decision, its economic projections, and a press conference from Federal Reserve Chair Jerome Powell. The greatest odds implied by futures pricing on Wednesday afternoon were for a year-end 2024 fed funds in the range of 3.75% to 4.00%. That would mean 1.5 percentage points of reductions in the Fed's target next year or six cuts of a quarter-point each.

Barron's goes on to suggest that interest rate cuts of the magnitude that the market is currently pricing into asset prices are highly unlikely. I have to agree with this assessment, as the Federal Reserve only meets eight times per year. Here are the current meeting dates for 2024:

NAFCU

The market believes that the rate cuts will start with the March meeting, so if that is the case then the Federal Reserve would have to cut at all but one of the remaining meetings. That is highly unlikely to happen unless the economy is in a rather severe recession. As 2024 is an election year, the Federal Government and the central bank will be very hesitant to declare a recession or make major changes to policy during the year unless it is very obvious to everyone that a near-term crisis is at hand (such as the 2008 subprime mortgage crisis or the 2020 COVID-19 pandemic). As the Federal Reserve would pretty much be constantly cutting in order to achieve the market's expectations, that would be an implicit assumption that the economy is in a great deal of trouble and that would look very poorly for any politician that is seeking re-election. As such, this seems pretty unlikely unless something really does break (a financial collapse caused by the high level of leverage in the economy and the massive unrealized losses sitting on the balance sheets of banks is one possibility). That scenario would disrupt the entire "soft landing" narrative, as it seems unlikely that the stock market will be able to hold onto its recent gains in such an event. Thus, if the market was genuinely expecting a severe recession, stocks should not be rising in anticipation of interest rate cuts.

If the Federal Reserve does not deliver the interest rate cuts that are implied by the market, then bonds are substantially overpriced right now. As such, there will almost certainly be a reversal that causes bonds to give up some of their recent gains. Thus, investors should probably not be going all in on traditional bonds right now. It is probably best to have some exposure to an asset that will be generally unaffected by interest-rate policy. This fund can help achieve that goal, as the floating-rate securities that it holds are generally interest-rate neutral in terms of price. We already discussed this.

Leverage

As is the case with most closed-end funds, the BlackRock Floating Rate Income Strategies Fund employs leverage as a method of boosting its effective portfolio yield and returns beyond that of any of the underlying assets in the fund. I explained how this works in my previous article on this fund:

In short, the fund is borrowing money and then using that borrowed money to purchase floating-rate debt securities. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio.

As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will usually be the case. It is important to note though that this strategy is not as effective today at boosting the portfolio yield as it was three years ago. This is because the difference between the borrowing rate and the yield of the purchased assets is much narrower than it was back when the borrowing rate was basically zero.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to an excessive amount of risk. I generally do not like any fund to have leverage above a third as a percentage of its assets for this reason.

As of the time of writing, the BlackRock Floating Rate Income Strategies Fund has leveraged assets comprising 24.10% of its overall portfolio. This is relatively in line with the leverage ratio that the fund had the last time that we discussed it, which makes sense as the fund's net asset value has been relatively flat. This is well below the leverage that is employed by many other closed-end funds, and it is well below the one-third of assets threshold. As such, we probably do not need to worry too much about the fund's use of leverage today. The balance between the risk and reward here is acceptable.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the BlackRock Floating Rate Income Strategies Fund is to provide its investors with a very high level of current income. In order to accomplish this objective, the fund invests in a portfolio of leveraged loans that will typically pay a yield that is a few hundred basis points above the federal funds target rate. In today's market environment, that obviously represents a very high yield. This fund takes things a step further though, as it borrows money and then uses that borrowed money to purchase more income-producing securities than it otherwise could with its own equity capital. The fund collects all of the money that it receives from these securities and then pays it out to its own investors, net of the fund's own expenses. In most cases, it will not have much in the way of capital gains due to the inherent stability of floating-rate securities so the money available for distribution will probably usually only consist of the coupon payments that the fund receives from the securities in its portfolio. However, we can still expect that the fund's yield will be quite respectable considering the high current yield on leveraged loan securities.

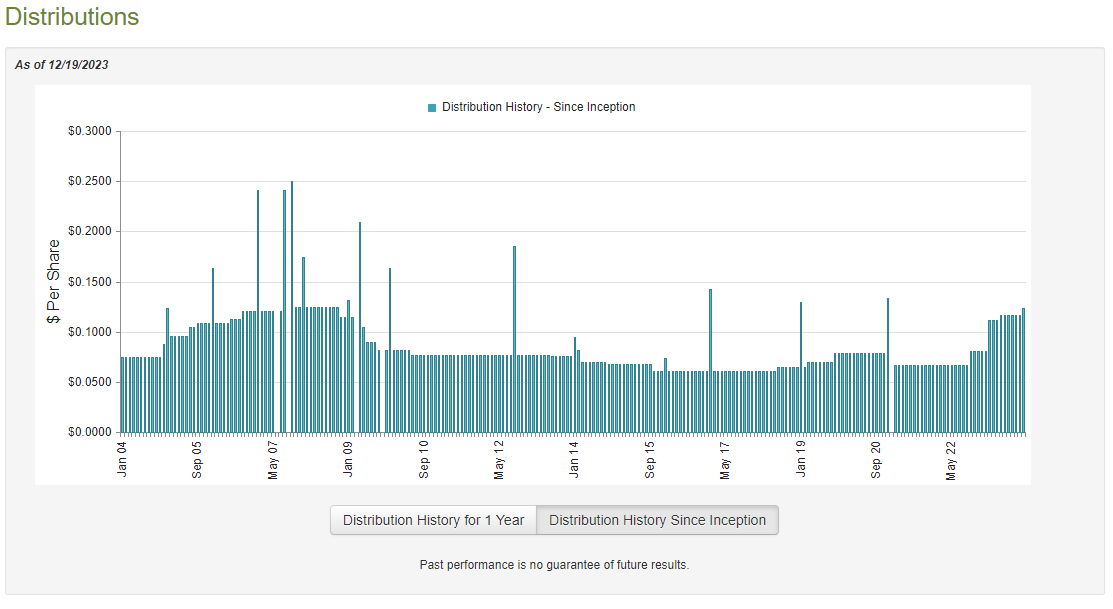

This is certainly the case, as the BlackRock Floating Rate Income Strategies Fund pays a monthly distribution of $0.1238 per share ($1.4856 per share annually), which gives it a very impressive 11.97% yield at the current market price. Unfortunately, the fund has not been particularly consistent with respect to its distribution as it has both raised and cut the payout many times over its lifetime:

{kind=link}

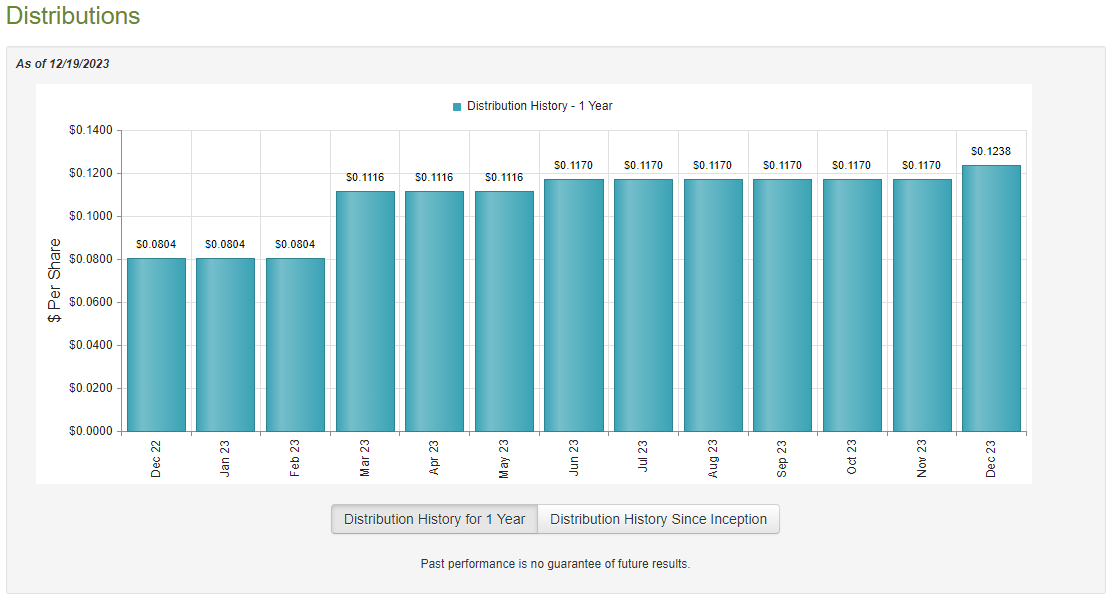

This variability with respect to the distribution may prove to be a turn-off for those investors who are simply seeking to receive a safe and secure income that can be used to pay their bills and finance their expenses. However, the variation is not particularly surprising considering that the returns provided by floating-rate securities depend very much on interest rates. After all, these securities will not have their prices change very much over time, so their returns will almost entirely consist of coupon payments, and these are heavily dependent on interest rates. That has been a good thing recently though, as this fund has increased its distribution three times over the past twelve months, including most recently in December:

{kind=link}

The fact that the fund's distributions have increased over the past year is quite nice to see, especially since inflation is still a long way from being beaten and we all need ever greater quantities of money to pay our bills.

As is always the case, we should have a look at the fund's financial condition as we do not want it to be paying out more money than it can afford. Such a scenario is quite destructive to the fund's net asset value and as such is not sustainable over any extended period of time.

Fortunately, we have a relatively recent document that we can use for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on June 30, 2023. This is a considerably newer report than the one that we had available to us the last time that we discussed this fund, which is quite nice to see. As everyone reading this is no doubt aware, the first half of 2023 was characterized by a great deal of euphoria in the market as investors generally tried to front-run a Federal Reserve pivot that was expected to come during the second half of this year. Obviously, that pivot did not actually happen, but the potential for capital gains may have presented itself. Events such as this do not really have much impact on the price of floating-rate securities though, so it does seem unlikely that the fund would really be able to make outsized profits here, but it is possible. This report should overall just give us a better idea of how well the fund is financing its distribution than the report that we had available the last time that we discussed it.

During the six-month period, the BlackRock Floating Rate Income Strategies Fund received $192,006 in dividends along with $26,980,800 in interest from the investments in its portfolio. When we combine this with a small amount of income from other sources, we see that the fund had a total investment income of $27,547,045 during the six-month period. It paid its expenses out of this amount, which left it with $21,276,524 available for shareholders. This was, unfortunately, not enough to cover the $21,583,948 that the fund paid out in distributions to its investors. It did manage to get very close to accomplishing this task, though. With that said, it may still be concerning that the fund did not manage to fully cover its distribution out of net investment income since that is generally what we would like to see with any debt-focused closed-end fund.

However, there are other methods through which the fund can obtain the money that it requires to cover the distribution. For example, it might be able to earn some money by trading appreciated assets in a favorable market. Realized capital gains are not considered to be part of investment income for tax or accounting purposes, but they obviously do result in money coming into a fund. Fortunately, the fund did enjoy a certain amount of success in this area. During the six-month period, the BlackRock Floating Rate Income Strategies Fund reported net realized losses of $2,500,756 but these were more than offset by $14,483,774 net unrealized gains. Overall, the fund's net assets increased by $11,675,594 after accounting for all inflows and outflows during the period.

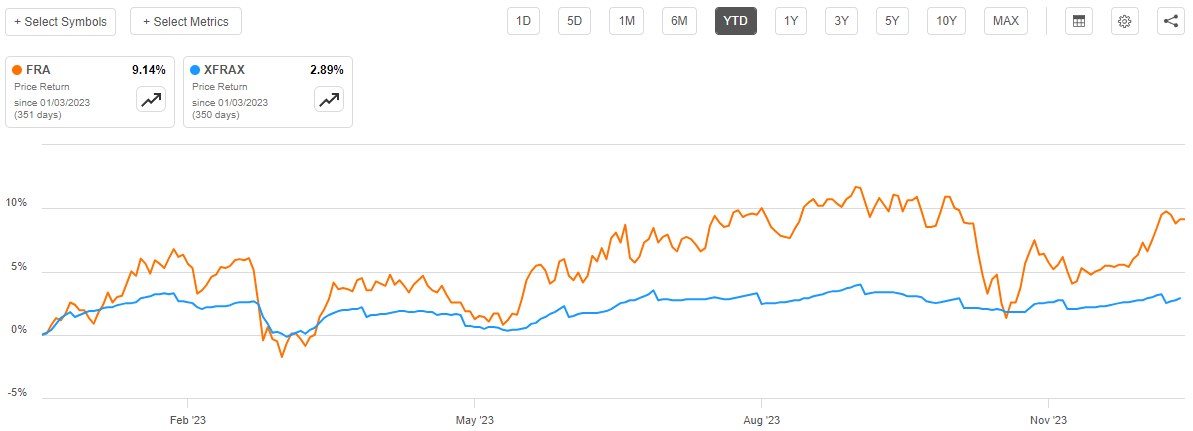

As we can see, the fund technically did manage to cover all of its distributions during the period, although it had to rely on unrealized capital gains to do so. As everyone reading this is well aware, unrealized capital gains can quickly be erased by any market correction. Thus, the fund's situation in the first half of 2023 may not be sustainable over the long term. However, as we can see here, the fund's net asset value per share is up 2.89% year-to-date:

{kind=link}

While this does not necessarily tell us how the fund is financing the distributions that it has paid out year-to-date, it does strongly suggest that the distributions that are being paid out are not destructive to the fund's net asset value. That is the most important thing, and overall, it looks like the fund's distributions are probably safe for the time being. It is likely that the fund could cut the payout next year though if the Federal Reserve follows through on its current plans to pivot its monetary policy.

Valuation

As of December 19, 2023 (the most recent date for which data is currently available), the BlackRock Floating Rate Income Strategies Fund has a net asset value of $13.19 per share but the fund's shares currently trade for $12.35 per share each. This gives the fund's shares a 6.37% discount on net asset value at the current price. That is a reasonable discount, although it is nowhere near as attractive as the 8.60% discount that the fund's shares have had on average over the past month. As such, it may be possible to obtain a better price on the shares by waiting for a bit. The current discount is not really that bad though, if you desperately need to buy the shares today for some reason.

Conclusion

In conclusion, the BlackRock Floating Rate Income Strategies Fund looks like a very good way to add a portfolio of floating-rate securities to your assets today. There could be some reasons to do this right now despite the expectation of falling interest rates next year. The biggest reason, of course, is that the market is probably wrong about the magnitude of the impending rate cuts and that sets anyone buying traditional fixed-income securities up for losses given today's prices. However, if part of your portfolio is invested in floating-rate securities, your risk is reduced. BlackRock Floating Rate Income Strategies Fund Inc appears to be covering its distribution and it is trading at a discount, so we may have a reason to initiate or add to a position today.

For further details see:

FRA: A Good Way To Hedge Your 2024 Interest Rate Risk