FRG - Franchise Group: A Master Class In Capital Allocation

Summary

- Brian Kahn, sitting at the helm of the Franchise Group, is displaying a master class in capital allocation that turned a relatively negligible company into a formidable franchise holding conglomerate.

- Management incentives are completely aligned with the rest of the shareholders as the CEO and the rest of the insiders own more than 30% of the company and are still buying more.

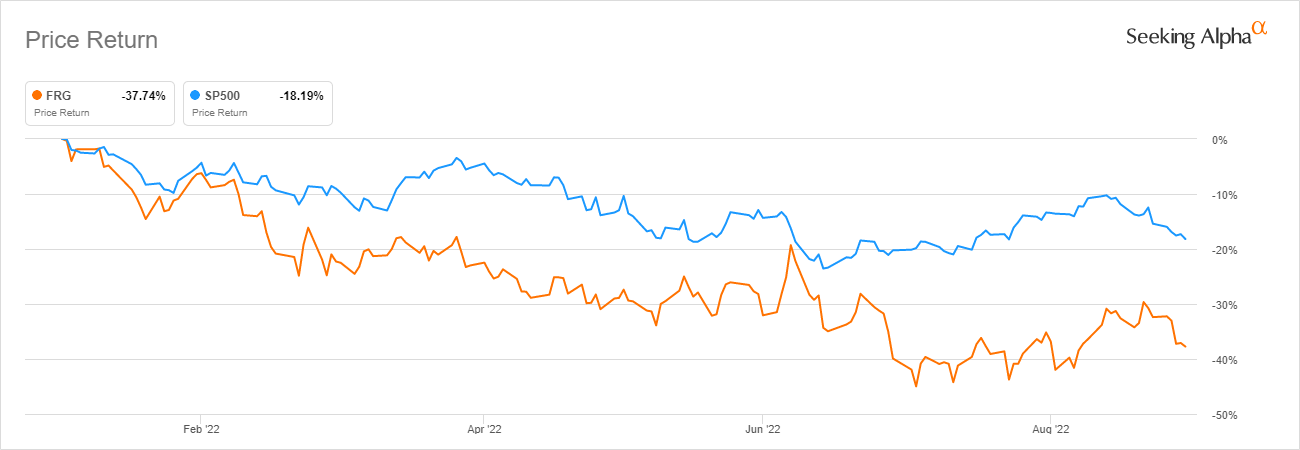

- A degrading macroeconomic environment and a downgrade in guidance resulted in tremendous down-pressure being applied to the company's stock price, which is now down 37.74% year-to-date.

- The $1.1B market cap has a $500mm buy-back program approved and in place while at the same time distributing 25% of EBITDA in terms of dividends to the shareholders resulting in a 7.43% yield.

- A multi-layered approach to creating shareholder value has seen investors enjoy the company delivering a five-fold market alpha while at the same time collecting extremely generous dividend distributions.

Franchise Group ( FRG ) is a very unique and intriguing company that is led by top-class management with skin in the game that is successfully executing a brilliant business model creating significant shareholder value through a multilayered approach. The rapidly degrading macroeconomic environment began taking its toll on some of the franchises with the most vulnerable business models, which ultimately translated itself into the bottom line and led to a disappointing downgrade in guidance. This fact combined with a recent failed bid to acquire the retail giant Kohl's Corporation ( KSS ) for $60 per share at a roughly $8 billion valuation resulted in tremendous down-pressure being applied to the company's stock price. More keen followers might have already caught up with the fact that we are dealing with a relatively small $1.1 billion ($1.5 billion at that time) market cap that attempted to close down a deal valued at slightly more than five times its equity size. This is exactly where the brilliance of the strategy the company is utilizing comes under the spotlight.

Franchise Group is operating a roll-up strategy of acquiring mostly poorly-led, in-distress businesses through leveraged buyouts. The acquirees often have one thing in common, they operate businesses that are franchisable but remain corporate-led and operated to a large extent. This is where management led by Brian Kahn steps in and realigns the acquiree to a much leaner franchisee business model that requires very little capital to maintain but still generates significant cash flow to the owner of the franchised brand. Management seeks to rapidly restructure the acquiree and refranchise the now-owned corporate locations leading to an influx of cash which is directed to aggressively deleverage the company. At the end of an acquisition cycle, the company no longer owns and operates a retail chain but instead becomes the owner of the brand, running a much leaner operation while dictating the rules and collecting the royalty checks in the meantime. It's all right there in the name.

{kind=link}

What is the Franchise Group?

The exact process described above has allowed the relatively small and unknown company to grow into a formidable franchise conglomerate in a matter of only a few years. This impressive story began when current CEO Brian Khan's investment vehicle, Vintage Capital Management, acquired control of Liberty Tax, then publicly traded under the stock ticker "TAXA". The former was subsequently merged with Buddy's Home Furnishings in order to form the "The Franchise Group" we know today. New management had the idea to turn the former publicly traded tax preparer into a scalable franchise holding conglomerate through a series of aggressive acquisitions.

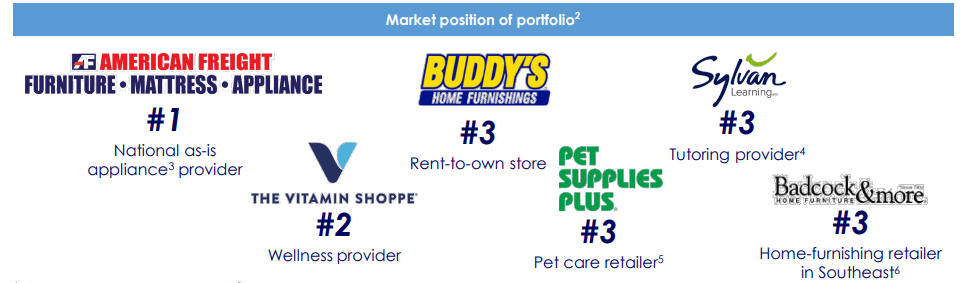

A series of accretive and well-thought-out acquisitions have created significant value for shareholders. The conglomerate is currently consisting of the rent-to-own retailer Buddy's, health and wellness retailer The Vitamin Shoppe, affordable furniture retailer American Freight, pet store supplies retailer Pet Supplies Plus, tutoring services company Sylvan Learning, and the home-furnishings retailer W.S. Badcock. The M&A track record of the company has been superb in our humble judgment and left us impressed.

{kind=link}

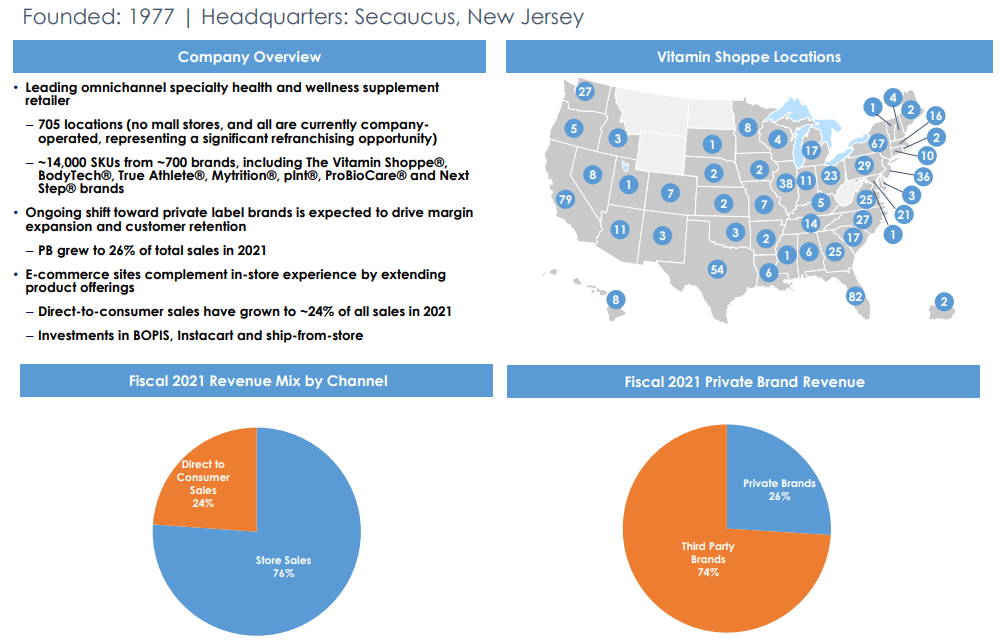

The Vitamin Shoppe - was the first major step management took in building the franchise conglomerate we know today. The company, then facing multiple headwinds and an uncertain future, was acquired by Franchise Group for just $208 million in Q3 2019 . TVS is an omnichannel specialty health and wellness supplement retailer which is offering an assortment of nutritional solutions, including vitamins, minerals, specialty supplements, herbs, sports nutrition, homeopathic remedies, and others. The segment delivered $137.20 million in EBITDA for the last year and so far in the first six months of 2022 has generated $78.90 million in EBITDA.

The Vitamin Shop Overview (FRG August Investor Presentation)

{kind=link}

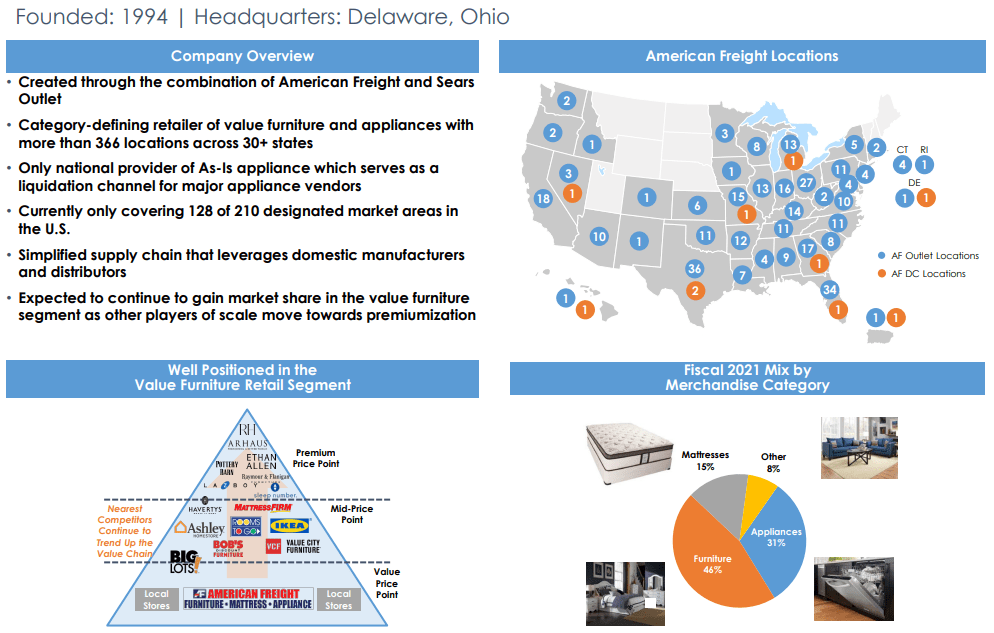

American Freight - represents a key acquisition in the process of building FG's franchise conglomerate. AF was acquired by the conglomerate in late December of 2019, for a sum of $450 million. The business was envisioned as a one-stop shop for affordable furniture, mattresses, and appliances operating in the bottom value segment of the market. A key step in establishing American Freight's footprint in the market was the integration of Sears Hometown and Outlet Stores, which was acquired by FG for only $132 million in Q3 of 2019 . In Q1 of 2020, the business was fully integrated into American Freight. The business generated $93.4 million in EBITDA for 2021 but has been struggling recently due to the complex macroeconomic environment and generated only $23.32 million in EBITDA for the past six months, being one of the most affected businesses.

American Freight Overview (FRG August Investor Presentation)

{kind=link}

Pet Supplies Plus - was one of the major and somewhat pricier acquisitions by the franchise conglomerate. Franchise Group acquired the business for $700 million in Q1 of 2021 from Sentinel Capital Partners, a private equity firm. PSP is one of the leading US pet care stores with more than 644 locations across the country, with 414 of them currently franchised. This business segment generated $93.2 million in EBITDA for 2021 and has been one of the best-performing segments during the macroeconomic downturn as it generated $51.46 million in EBITDA in the first two quarters of 2022.

Pet Supplies Plus Overview (FRG August Investor Presentation)

{kind=link}

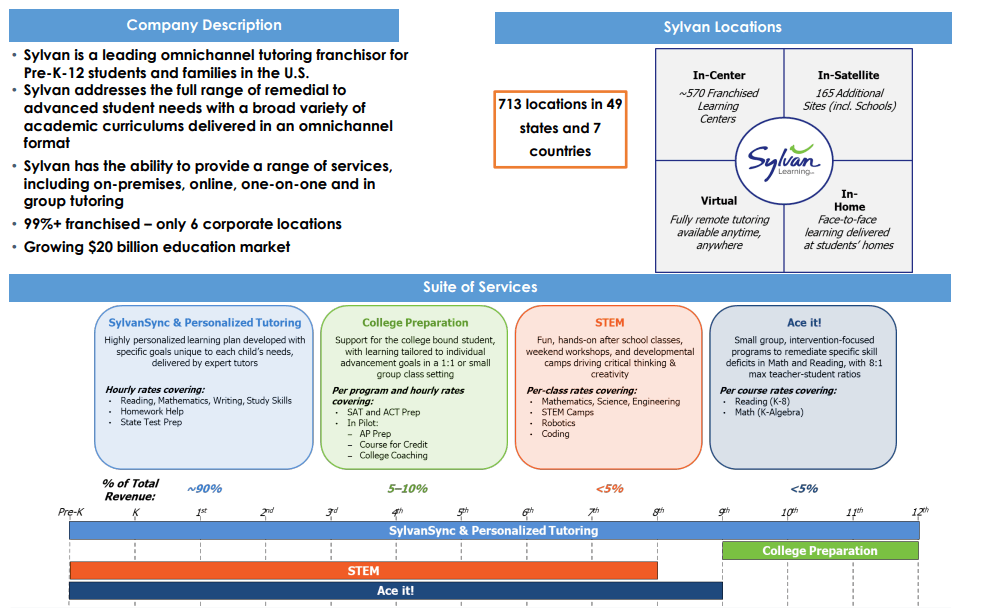

Sylvan Learning - has been one of the smaller and stranger acquisitions completed by FG. The company was acquired in Q3 of 2021 for $81 million in an all-cash transaction that was financed with available cash. Sylvan Learning is envisioned as an omnichannel tutoring franchisor. This business segment generated only $12.4 million in EBITDA for 2021 and slightly more than 6.70 million over the course of the last six months.

Sylvian Learning Overview (FRG August Investor Presentation)

{kind=link}

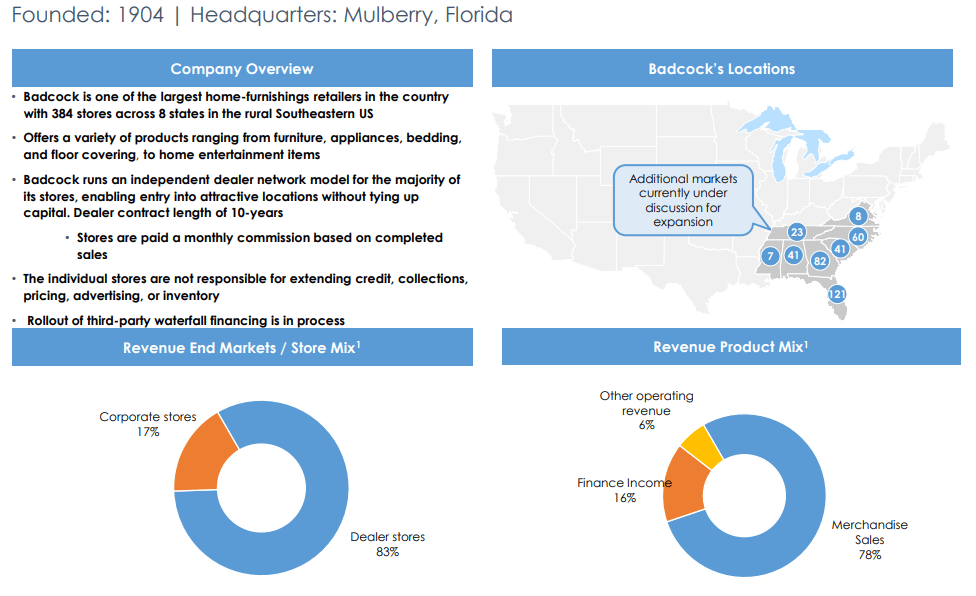

Badcock Home Furniture & More - is the latest successful acquisition by the franchise conglomerate. Badcock has been acquired through an all-cash transaction in Q4 of 2021 for $580 million . The company is one of the largest home-furnishing retailers in the country with 384 stores mostly operating through the independent dealership model. This is possibly the best testament to the efficiency of the management capital allocation. Management was able to move a $400 million receivable portfolio off their books to a third party while at the same time gaining close to $270 million through asset sale-leasebacks shortly after the acquisition. They were able to recuperate around $670 million in less than six months after the transaction which were then mostly directed to deleveraging their balance sheet. Badcock as a business segment has generated $52.27 million in EBITDA over the last two quarters.

Badcock Home Furniture Overview (FRG August Investor Presentation)

{kind=link}

Management with "skin in the game"

There are few things in a company we like to see more than a management team that has its incentives completely aligned with the rest of the shareholders. Franchise Group is a textbook example of a management team that has "skin in the game" and then some. Insiders currently own close to a third of the shares outstanding and there has been a very clear historic record of major insider ownership. On top of that, the company has institutional ownership estimated at 54.55%, with roughly 190 institutional holders owning 22 million shares. Institutional ownership has been on a steady rise.

Company Ownership Structure (TIKR Terminal)

{kind=link}

The company is being led by an experienced and well-respected value-oriented investor, Brian Kahn. He is also the founder and managing partner of Kahn Capital Management, which later became Vintage Capital Management, through which the entire story of Franchise Group began. I find it also tremendously interesting that Brian was an operator and franchisor of Buddy's Home Furnishings rent-to-own stores, a company that would be later merged with Liberty Tax in order to form the Franchise Group. Brian is almost fully committed to the company in terms of his personal wealth, and represents the definition of the phrase "walking the walk".

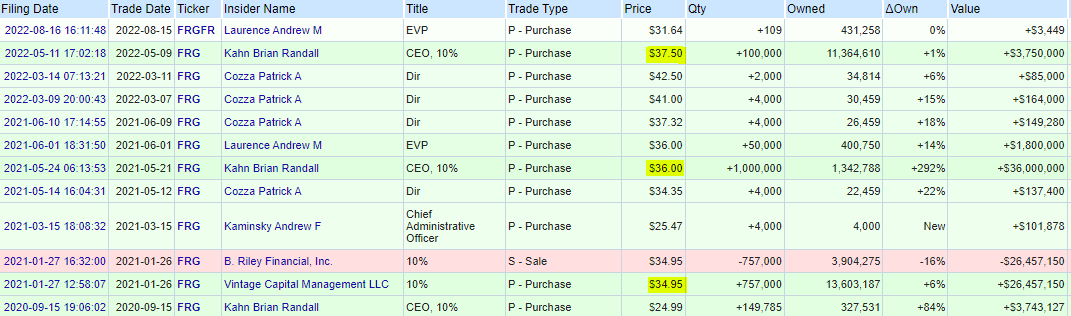

Besides the large insider and institutional ownership at Franchise Group, there is a rich history of insider buying. We always like to refer back to a famous Peter Lynch quote at this point: "Insiders might sell their shares for any number of reasons, but they buy them for only one: they think the price will rise".

{kind=link}

Brian took multiple opportunities to acquire more shares in the company around the $34-37 range, either directly or through his investment vehicle Vintage Capital Management. As a reminder, the company currently sells for $33.62 per share. He is estimated to own roughly 30% of the entire company, which is a clear statement he fully stands behind the business, for better or worse.

Lucrative and accessible shareholder returns

The company has been often lately compared to Berkshire Hathaway ( BRK.B ) ( BRK.A ) in multiple ways due to the similarities in the efficient capital allocation, but there are rather obvious differences in terms of differences in approach to shareholder returns. The nature of Franchise Group's business model can leave the company with a lot of cash on hand but little room to deploy it. As a matter of fact, the entire model relies upon carefully thought-through M&A execution, and such opportunities are by definition not plentiful. On top of that, the capital used in the said acquisitions is usually outside capital; ultimately meaning capital the company can afford to have a multilayered shareholder return policy with.

This can in no way be compared to Warren Buffett's brainchild, which is in its own way first and foremost an insurance company with multiple benefits in keeping significant amounts of cash on hand. Furthermore, its sheer size does not allow the conglomerate to delve into the companies with which Franchise Group does business. They are never returned to the shareholders in the form of dividends, something the company is notorious for. Franchise Group on the other hand returns value to shareholders both through a generous dividend policy and a share buy-back program.

{kind=link}

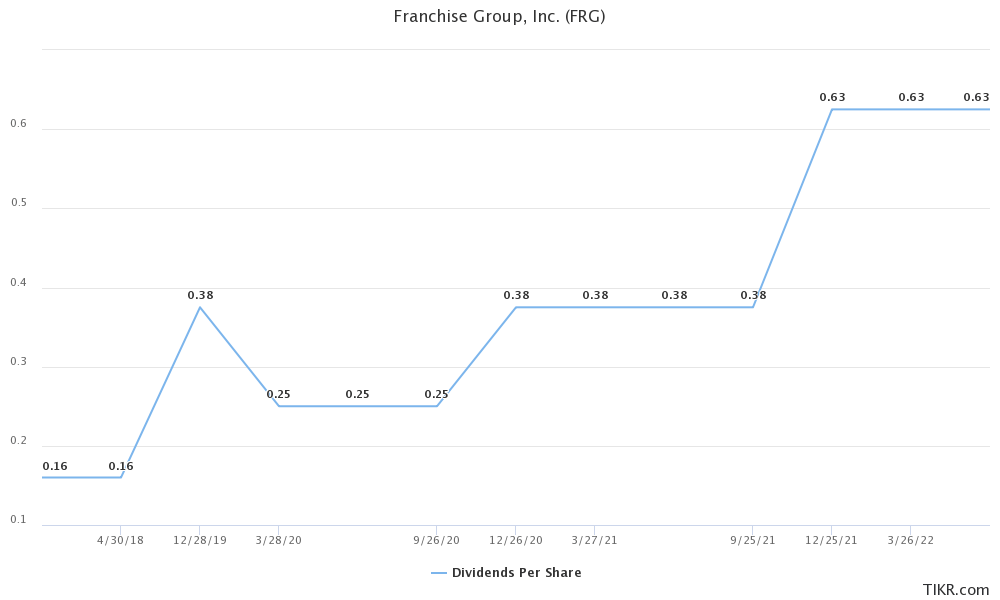

A multi-layered approach to creating shareholder value has seen investors enjoy Franchise Group dominating the S&P 500 ( SPY ) while at the same time showering them with dividends. Management has established a long-term dividend policy planning to redirect approximately 25% of EBITDA towards shareholders via dividends in the upcoming years. There is something about avoiding a "fixed" dividend and having it tied towards a performance goal that resonates extremely well with me. The dividend itself has been on a stark rise, as the series of accretive acquisitions and some steady internal organic growth resulted in an attractive payout which is currently annualized at $2.50 per share. This means that a dividend of $0.16 per share in the times before Brian took over has been nurtured to a $0.63 per share quarterly dividend today. While the growth aspect of the company remains largely subservient to M&A execution down the road, the dividend is still well supported by fundamentals, even when accounting for the downgraded guidance, which lowered EBITDA estimates to $390 million for this year.

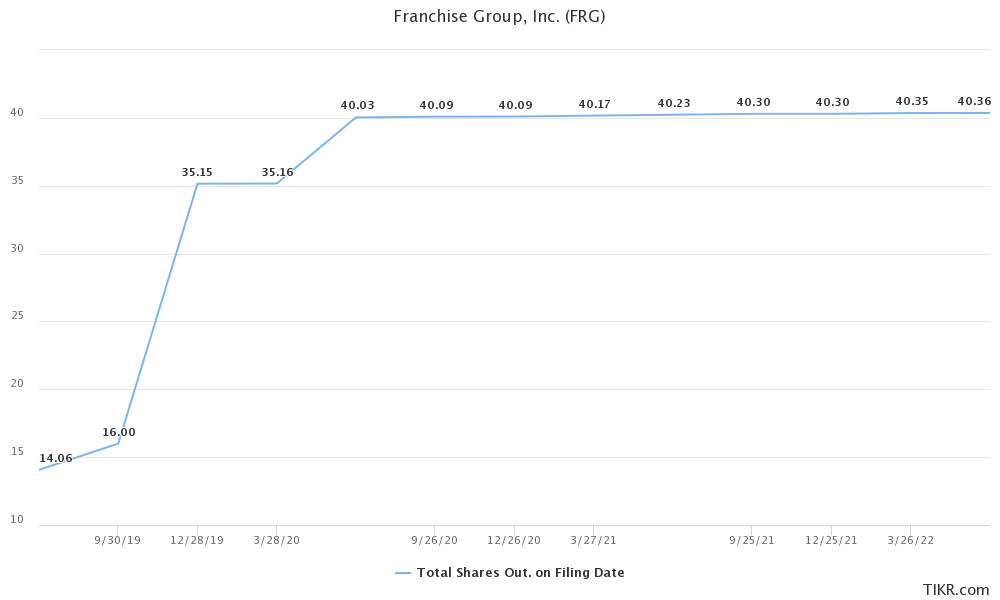

With limited access to outside funding in the early days, management was forced to rely on equity financing to get the first major deals across the finish line. This leaves a somewhat negative impression when taking a look at the rapid rise in outstanding shares over the past couple of years, as potential investors might fear further dilution. But this is not the case. The series of successful acquisitions left the company in good relations with possible backers as well as a much better-looking balance sheet. Brian emphasized this point during the first quarter earnings call, issuing equity to finance further M&A action is largely off the table.

As far as issuing equity, generally, we're -- it's highly unlikely that we would issue equity anywhere near the current FRG valuation for M&A purposes. I just, I think, it would be very difficult to find something that that makes sense. I think there are other ways to structure transactions that hopefully would not require us to do that if there was a large transaction but that is not something that we have an appetite to do.

Brian Khan, CEO - Q1 2022 Earnings Call

{kind=link}

The truly interesting part comes when we analyze their latest $500 million share buy-back initiative . At current market prices, the buy-back program would in theory be able to acquire close to 15 million shares, or just shy of 40% of the entire market capitalization of Franchise Group. Now, in practice, there are just not enough sellers at this price for the buy-back program to be able to have this sort of effect. Given the density of the ownership structure, the initiative would significantly inflate the share price which would degrade its effectiveness. It is worth keeping in mind that the distressed economic situation is causing havoc in the retail space, potentially creating multiple acquisition opportunities that management would want to explore. In that context, management might rule that capital is to be much better deployed externally, seizing the opportunity. A hint of this can be seen from the latest earnings call.

Yeah, so we authorized, at our two Board meetings ago, we authorized a $500 million buyback over the next few years. We did not intend to do a 10b5-1. We want to be strategic about when and how much we acquire. Certainly, it is something that we - just say we've not had an open window, still don't have an open window. We didn't have an open window because of the Kohl's transaction and then we got into the quiet period. So we haven't had an open window yet to speak of but, look, we will - we now have the ability to weigh, buying more of our existing businesses against buying other businesses that's not a tool that we've had in the toolbox before. We have it now, we're very excited about that and I don't think anybody knows our businesses better than we do, which is a good thing. So I think we'll be opportunistic as we can be.

Brian Khan, CEO - Q2 2022 Earnings Call

Still, we believe that a part of the program will be unleashed in the short-term nonetheless, with management not being able to afford to deny an enticing opportunity like this one. With some back of the paper math, deploying just slightly less than $200 million of the share buy-back package would bring shares outstanding down to 35 million, lowering them by roughly 15% and almost immediately pushing the dividend yield to 8.55%.

Risks to the thesis

While we maintain a very bullish outlook on the company, as with any investment, the thesis itself carries its fair share of challenges. The more obvious one is that the recession-headed economy has the capacity to cause plenty of headaches for a part of the more home improvement-oriented portfolio. This is also a small sub-thesis about American Freight being essentially a recession-resistant business, given it operates as a bargain furniture store that might have largely gone down the gutter given the recent developments. Management still reinforces this thesis as of the last earnings call, drawing differences between the current environment and a "real recession" as they have referred to it. Either way, the end result is the same, demand for the products has been on the decline.

The noise surrounding the recent developments has been picked up by shorts sellers who at this point sold short roughly 10% of the float, another indication that there is no clear consensus on the future prospects of Franchise Group, at least in the short to mid-term. However, the much larger issue at hand is that the relatively small size of the company poses a risk considering the business model, as the company remains highly vulnerable to failing acquisitions, being effectively two failed acquisitions from disaster. A major acquisition failing and leaving the balance sheet in a poor condition loaded with debt that the organic business will take a long time to clear should be considered. Trusting the management and their ability to deliver on execution is the most important in this investment thesis. This individual acquisition risk will deteriorate given time, but so will the outsized return potential as the company grows larger.

Final thoughts and closing arguments

We already believe that the company is selling at an immensely attractive valuation, but this investment opportunity represents something much more than a mispriced company with the potential of realigning itself towards its intrinsic value. Rather, we are discussing a very simple but effective business model, that if executed with a similar level of excellence, could grow into a brand fortress numerous times its current size, generating extraordinary shareholder returns in the meantime.

The multifaceted approach to creating shareholder value that Franchise Group is implementing creates difficulties in describing the true nature of the company. Facing multiple short to mid-term headwinds that are affecting its organic growth potential has seen tremendous down-pressure applied to the share price, slashing the already attractive price by almost 38% year-to-date and thereby presenting an enchanting value investment opportunity. Even after taking the downgraded guidance into consideration, the company is still selling at approximately 9.36x EV/EBITDA, 5.75x P/FCF, and an 8.25x P/E. The current dividend yield is in line with the most attractive dividend payers in the market, while dividend growth over the past couple of years casts a tall shadow upon even the most appealing dividend growth players. On the other hand, the case for it being a growth-oriented company is solid, as the company operates an aggressive high-growth business model through which it has managed to outperform the market fivefold since the new management took over. No matter which way one looks at things, Franchise Group is a unique and mesmerizing special situation investment that could quite possibly be the most attractive investment opportunity we have encountered this year.

For further details see:

Franchise Group: A Master Class In Capital Allocation