FRG - Franchise Group: The Dividend Is Possibly Safe But Company Faces Headwinds

2023-03-08 04:49:45 ET

Summary

- FRG's dividend is safe, but its variable debt and ties to furniture brands are headwinds.

- Refranchising Vitamin Shoppe could be an option if it needs to deleverage.

- The stock is more a "Hold" at the moment.

Franchise Group’s ( FRG ) dividend is safe, but its variable-interest, high debt load and consumer-facing furniture brands could hurt the stock in the medium term if the economy weakens.

Company Profile

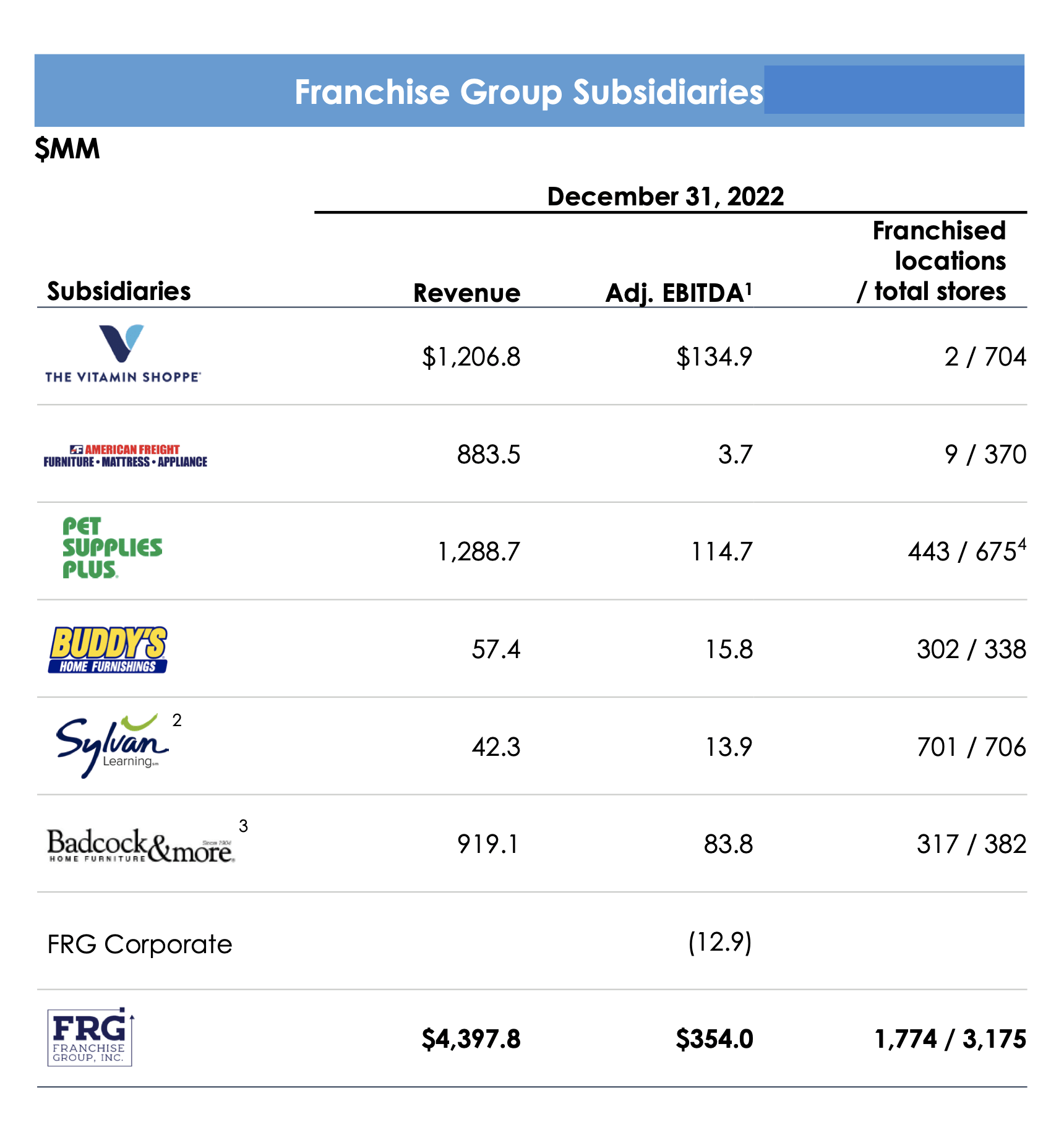

FRG is an owner and operator of a portfolio of various brands. Its brands include The Vitamin Shoppe, Pet Supplies Plus, Badcock Home Furniture, American Freight, Buddy's Home Furnishings, and Sylvan Learning. At the end of 2022, these brands combined had over 3,000 locations, of which 1,310 were franchised locations, 1,401 were company-run, and 318 were dealer locations.

Looking at the company’s brands, Pet Supplies Plus is the largest by revenue. It sells pet supplies and services through its stores and online, as well as offers grooming services through its Wag N’ Wash brand.

Vitamin Shoppe is its largest brand based on EBITDA. It is a specialty retailer that sells wellness products such as vitamins and supplements both through its stores and website.

Looking at FRG’s other brands, Badcock uses a showroom format to sell furniture, appliances, bedding, electronics, and seasonal items. American Freight also sells furniture, appliances, and bedding, but in a warehouse-store setting. It also is used as a liquidation channel for appliance makers. Buddy’s also sells electronics, furniture and appliance, but uses a rent-to-own model.

Sylvan, meanwhile, provides Pre—K to high school supplemental education and tutoring services. This is done on-premise and virtually.

{kind=link}

Opportunities and Risks

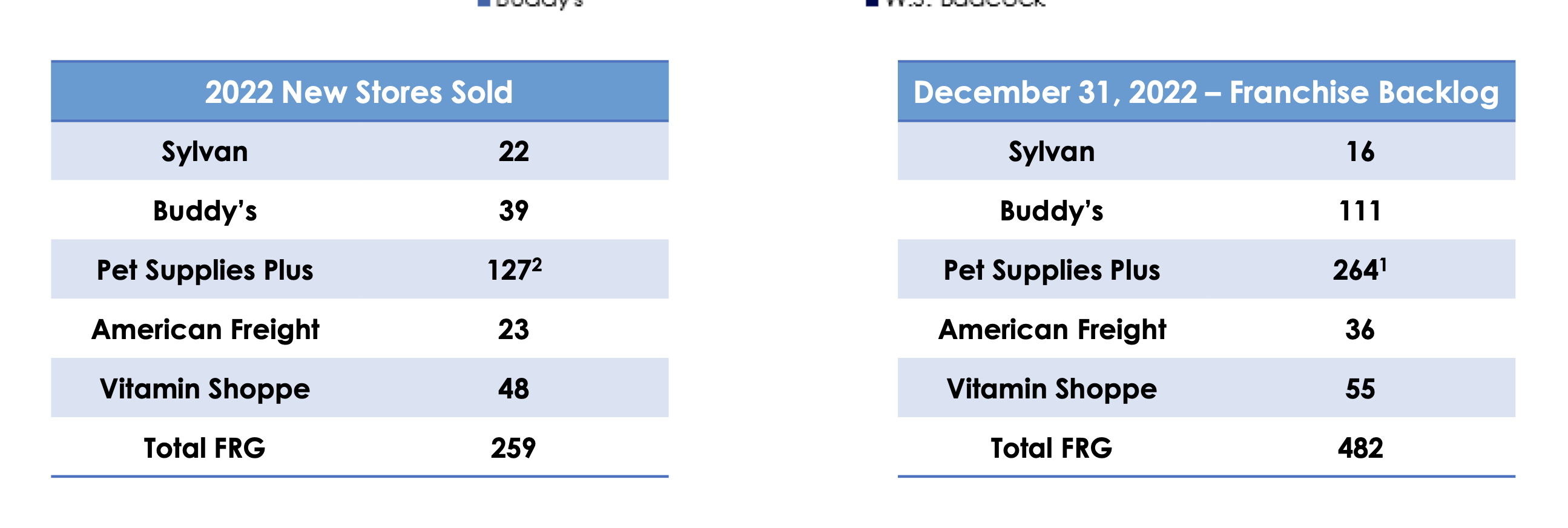

Within its current business set, FRG still has a lot of runway to continue to franchise out locations of its various brands. The benefit of this strategy is that the company gets an initial upfront cash payment with the sale of a territory, and then a high-margin recurring revenue stream. The company says it typically takes a franchise location 2-3 years to mature and really start doing well.

In fiscal 2022, the company sold 259 new territories and opened 92 new franchise locations. Across its brands, meanwhile, it says it has a backlog of 482 locations.

{kind=link}

With the bulk of stores for Vitamin Shoppe and American Freight being company owned, FRG also has refranchising opportunities, where it can sell existing stores to franchisees. The company has used this strategy in the past, most recently with Buddy’s in 2020.

M&A is another tenant to FRG’s growth. The company likes businesses with strong unit economics that can be franchised and which generate strong free cash flow. It says these business generally fit one of three categories: 1) a multi-unit franchise that can be scaled; 2) a multi-unit business that is largely corporate owned that can be refranchised and grow through franchising; and 3) a multi-unit business that be immediately accretive. These businesses typically are consumer facing and FRG looks to improve them through its buying scale, marketing efficiencies, and shared technology.

While M&A will eventually be on FRG’s radar, currently acquisitions are not a priority for the company until it reduces its debt.

On its Q4 call, CEO Brian Kahn said:

“The significant and rapid increase in interest rates has further reduced our discretionary cash flow and increased the bar for capital deployment into outside acquisitions. … While significant acquisitions are not a priority until we've delevered in this difficult environment, there may be one-off opportunities for small tuck-in acquisitions or franchise conversion that can create step function growth in our franchise unit count and royalty contribution. Case in point, today, PSP acquired 20 new locations from a competitor in bankruptcy, and they expect to sell those stores to existing franchisees in the coming months. All of these locations will be rebranded under the PSP or Wag N Wash banner.”

This leads into some of the risks that FRG faces, starting with its debt. With about $1.3 billion in net debt and adjusted EBITDA of nearly $355 million, the company is just over 3.5x levered. That’s a little high at the moment, and adds some extra risk if the economy goes into a severe recession. It’s also notable that FRG’s debt is by and large variable. As such, it is being hurt by high interest rates. FRG also just added $300 million to its first lien term loan in order to add liquidity, paying down its ABL.

FRG’s businesses are also consumer facing, and thus can be more economically sensitive. Three of the brands that FRG owns sell (or rents to own) furniture and appliances, which can be particularly affected by consumer weakness. Badcock and American Freight both saw large same-store sales declines in Q4, down -14.8% and -12.5%, respectively. It is projecting Badcock to struggle in 2023.

American Freight has had some issues in 2022, at one point seeing a -27% decline in transactions and having to work through high-cost inventory. FRG is expecting the brand to rebound in 2023, but that could depend on the economy and state of the consumer. However, FRG believes the turnaround is largely in its own hands, with CEO Brian Kahn saying:

"American Freight consumed a tremendous amount of cash last year from operations, including working capital usage. We certainly think that those days are behind us. I don't think that the turnaround in American Freight's financial performance is dependent on the economy. I think it's really within our control.

"But one of those things that we need to control is how quickly we can turn the high-cost inventory that we discussed back in November and have continued to have coming in as we've been moving the inventory out, but we still have old orders that are coming in, we need to get through that cycle. I think we did a really good job, a tremendous amount of focus and the team really focused on moving inventory, and that required us to take prices down closer to the value levels that the customers have grown to expect from American Freight.

“But I think that as you go through this year, we should be through the cleaning out of the inventory for the most part by midyear. I do expect a very significant increase in their profitability this year. I don't think it's going to get back to normalized levels, but I do expect that we will see a material increase.”

FRG’s other businesses have been holding up well, with Pet Supplies Plus being the standout with 5.2% comps in Q4. Vitamin Shoppe, though, is projected to see an EBITDA decline in 2023 due to the “continued mix shift in favor of lower-margin sports nutrition products.” Sylvan tends to be a pretty steady business.

Valuation

FRG currently trades at about 10.4x the 2023 consensus calling for $350.6 million in EBITDA. Based on the 2024 consensus of $416 million, it trades at 8.8x.

On a PE basis, its trades at a forward PE of 10x based on the 2023 consensus of $2.85.

Revenue is projected to be flat this year, with growth of 2.6% in 2024.

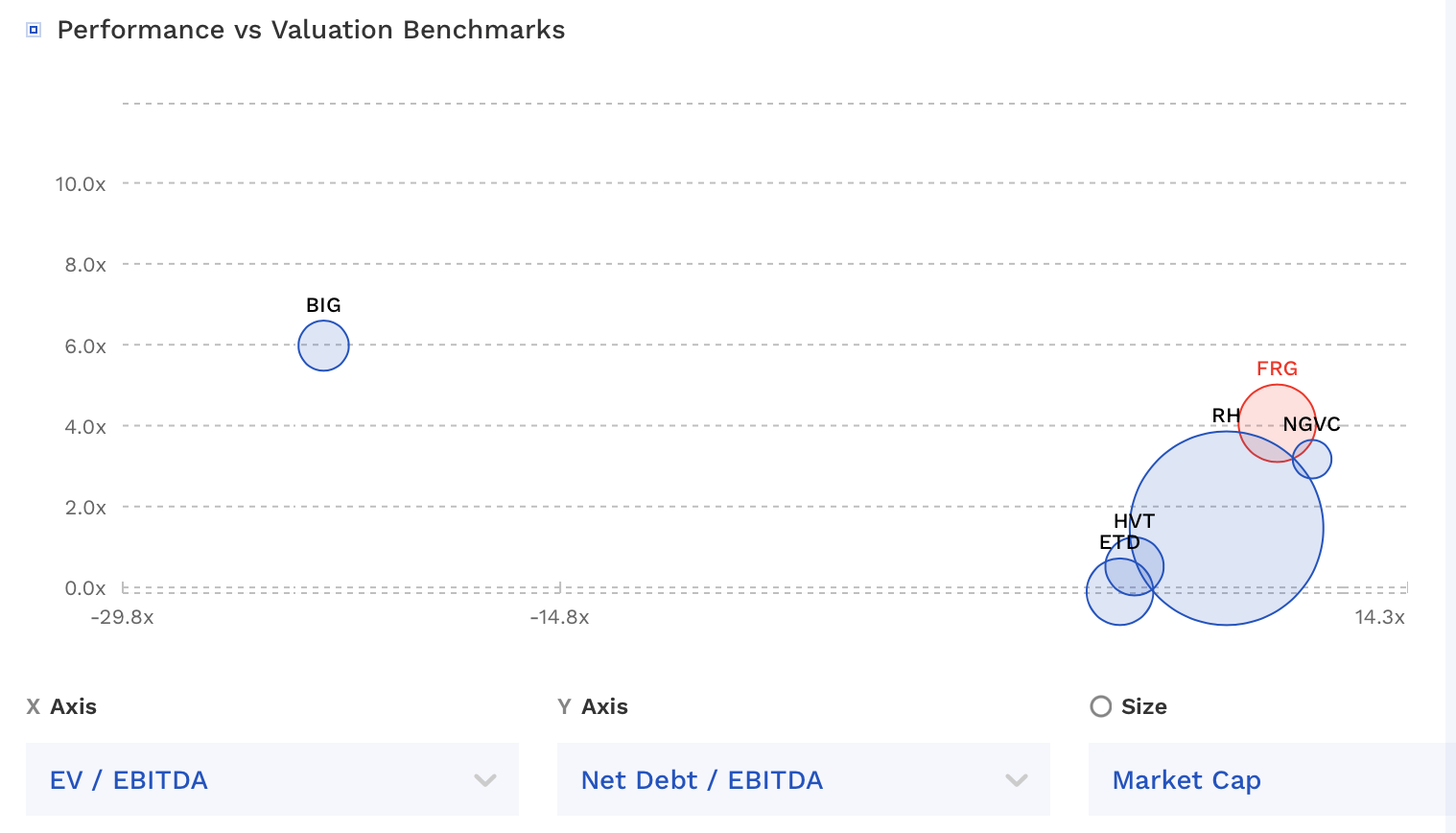

The company doesn’t particularly have any great comps when trying to compare its valuation to others.

{kind=link}

Conclusion

Investors like FRG’s over 8.5% yield, and that appears safe. However, the company’s leverage is a bit high and its variable interest rate debt has put a dent into its free cash flow, which will make it difficult for the company to de-lever.

With nearly $1.3 billion in net debt and adjusted EBITDA of just over $350 million, FRG is about 3.5x levered. Given that it has $100 million in cash tied up in excess working capital that will start to unwind, it should generate between $200-225 million in free cash flow this year. Excluding that unwind, it would be closer to a $135 million runrate. The cash flow will cover its dividend payment but not help pay down much debt. FRG, however, has the ability to refranchise its Vitamin Shoppe brand, which could eventually be an option if it needs cash.

What you are then left with are some consumer-facing businesses that could struggle in a weakening economy, especially its furniture brands. Given the current state of the economy and its leverage, I’d prefer to put new money into other high-yielding names at the moment.

For further details see:

Franchise Group: The Dividend Is Possibly Safe, But Company Faces Headwinds