FRG - Franchise Group: The Preferred Shares Still Offer Better Value In Take-Private Deal

2023-05-11 10:00:20 ET

Summary

- Franchise Group announced on May 10 that they would be pursuing a take-private transaction at $30 per share.

- As a holder of the preferred shares I took some time to review the deal's impact on FRGAP. Details of that follow.

- I also discuss where things are with the common shares and whether or not another bid is likely.

- From my analysis the risk-reward continues to favor the preferred shares over the common in the current deal scenario.

- Read on to see why I think this, and let me know what you think below.

Franchise Group ( FRG ) announced on May 10, along with earnings, that they would be pursuing a take-private transaction at the previously announced $30 per share. Management including Brian Kahn are part of the consortium offering to purchase the remaining 64% of the common stock they do not already own. Moving forward the deal is expected to close in the second half of 2023 and includes a 30-day go-shop provision where a superior deal may be solicited.

As an investor in the preferred shares, FRGAP , I was eager to review details of the announcement to gauge how these might be handled. Last month I wrote up why I thought the preferred shares were a better way to play the deal given they retained conversion rights in the event of a change of control. So the key question for me was whether the structure of this take-private deal triggered these conversion rights or not.

It turns out that my analysis still suggests the same thing: the preferreds are the best way to play.

Does the Offer Trigger FRGAP Conversion Rights?

Let’s start by reviewing the conversion rights which we can find in the preferred’s original prospectus . Here’s the exact language:

“A “Change of Control” is when, after the original issuance of the Series A Preferred Stock, the following have occurred and are continuing:

- the acquisition by any person, including any syndicate or group deemed to be a “person” under Section 13(d)(3) of the Exchange Act of beneficial ownership, directly or indirectly, through a purchase, merger or other acquisition transaction or series of purchases, mergers or other acquisition transactions of shares of our company entitling that person to exercise more than 50% of the total voting power of all shares of our company entitled to vote generally in elections of directors (except that such person will be deemed to have beneficial ownership of all securities that such person has the right to acquire, whether such right is currently exercisable or is exercisable only upon the occurrence of a subsequent condition); and

- following the closing of any transaction referred to in the bullet point above, neither we nor any acquiring or surviving entity (or if, in connection with such transaction shares of our common stock are converted into or exchanged for (in whole or in part) common equity securities of another entity, such other entity) has a class of common securities (or ADRs representing such securities) listed on Nasdaq, the NYSE or the NYSE AMER, or listed or quoted on an exchange or quotation system that is a successor to Nasdaq, the NYSE or the NYSE AMER. ”

I added the bolded emphasis here for the key details. So really we are looking at two triggers: more than 50% of stock changing hands and that the commons are delisted. Filing information reveals that the acquiring group is purchasing 64% of the issued and outstanding common stock which gets us over that 50% hurdle. And they state directly that “Upon completion of the proposed merger, Franchise Group will become a private company and will no longer be publicly listed or traded on NASDAQ.”

So according to the language provided, we can see that this transaction will trigger the conversion rights due to a Change of Control. Language in the prospectus for these conversion rights enable conversion at par value plus any accrued dividends. Specifically, conversion is calculated at the lesser of these two options:

-

The quotient obtained by dividing (1) the sum of the $25.00 per share liquidation preference plus the amount of any accumulated and unpaid dividends to, but not including, the Delisting Event Conversion Date or Change of Control Conversion Date, as applicable (unless the Delisting Event Conversion Date or Change of Control Conversion Date, as applicable is after a record date for a Series A Preferred Stock dividend payment and prior to the corresponding Series A Preferred Stock dividend payment date, in which case no additional amount for such accumulated and unpaid dividend will be included in this sum) by (2) the Common Stock Price (as defined herein); and

-

1.9608 (i.e., the Share Cap), subject to certain adjustments.

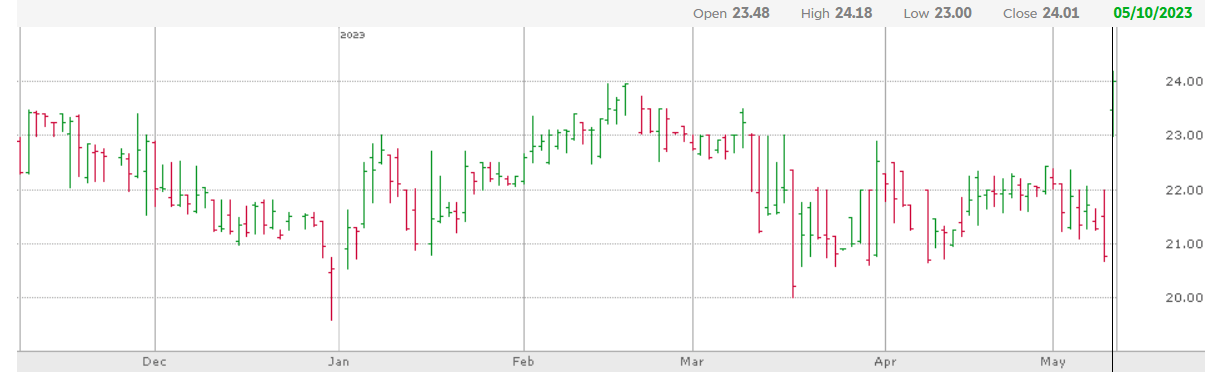

Really we are looking at option 1 here. Another quarterly dividend of $0.46875 per share will be distributed this quarter so I believe it’s safe to assume a takeout value on FRGAP at $25.47. The closing price on May 10 was $24.01 implying 6% upside to this takeout value – and this is after shares saw a +15% increase on the announcement.

{kind=link}

Clear Signal for the Preferreds from the Earnings Call

You don’t merely have to take my word for things here about the preferreds as management spoke on these directly in their earnings call. They included one sentence which highlighted what preferred owners needed to know.

“The Company anticipates redeeming its outstanding preferred stock in connection with the closing of the transaction -- continuing to pay the preferred stock dividend through the redemption date.”

So management is saying they intend to redeem the preferreds directly rather than waiting for the conversion rights to be triggered. While no timeline was given on this, my guess is that they will attempt to do this before another quarter forces a further dividend payment – meaning within the next three months.

With this estimate and the above derived 6% upside that would imply a 24% annualized return assuming it takes all three months. There is the 30-day go-shop period which could result in a higher offer being made. But I don’t feel that it’s likely. News that Franchise Group was considering an offer hasn’t really been news since the story broke in January . It was reported by Lauren Thomas at the Wall Street Journal and reads like a prescription:

“Franchise Group Inc, the investment firm that owns retailers including Vitamin Shoppe, is considering going private in a so-called management buyout, people familiar with the matter said.

The company’s management, led by Chief Executive Officer Brian Kahn, could pay a price of between $30 and $35 a share, the people said.”

And here we are five months later to the day of the article with the $30 take-private announcement. A committee of folks independent of Kahn’s interests unanimously approved the deal – basically they are giving their stamp of approval that this is a good outcome for common shareholders. If they are right in this then it would be unlikely the offer would increase. Additionally, given the deal is partially management led it seems unlikely that they will charge themselves more.

Consider also the earnings report itself. This quarter they generated a loss per share of $3.16 which wiped out all retained earnings in the company's history ($109.9 million). Retained deficit now sits at -$32.9 million -- that's not a good outcome.

{kind=link}

Where Does that Leave the Common Stock: FRG?

I can observe that it has left a lot of common stock owners here on Seeking Alpha with frustration. As of writing there are 93 comments on the SA news article announcing the buyout. The last four articles written on FRG averaged only 32 comments. So people were clamoring. And here’s the comment that kicked it off: “ This is absurd. Brian is doing us dirty. ”

Take a look at the sentiment from these sampled comments:

-

“Way to really fight for a premium there Brian”

-

“Well at least Brian Kahn's name is simple so I can remember to avoid it in the future. Good riddance to another huckster.”

-

“"How to Bilk Shareholders for $400 million and Other Bedtime Classics." - By Brian Kahn. Soon to be a bestseller on Amazon.”

-

“Where in the C-Suite, or on the BOD, is anyone working on “maximizing shareholder value”? I guess our only hope is for a white knight suitor to emerge? This feels so unethical.”

-

“What an unethical decision by management. They never took shareholder interests seriously and have just used this period of business weakness to enrich themselves at a cheap price. The investment thesis on the company centered mostly on Kahn's dealmaking ability. Kahn is certainly a wheeler dealer -- he's just not our wheeler dealer.’

-

“They are attempting to buy 65% of the company. Can we please all vote against this. It's incredibly unethical. I am not an American lawyer, but surely this should constitute a breach of fiduciary duty of some sort??? In any case, let's please vote against this.”

It goes on. But this last comment picks on something actionable. Shareholders outside of Kahn’s interest still need to approve this deal. Let’s say that another offer doesn’t come through during the go-shop period and shareholders are left to vote on this $30 option, are they likely to vote it through?

Only last June the stock was trading above $40 per share.

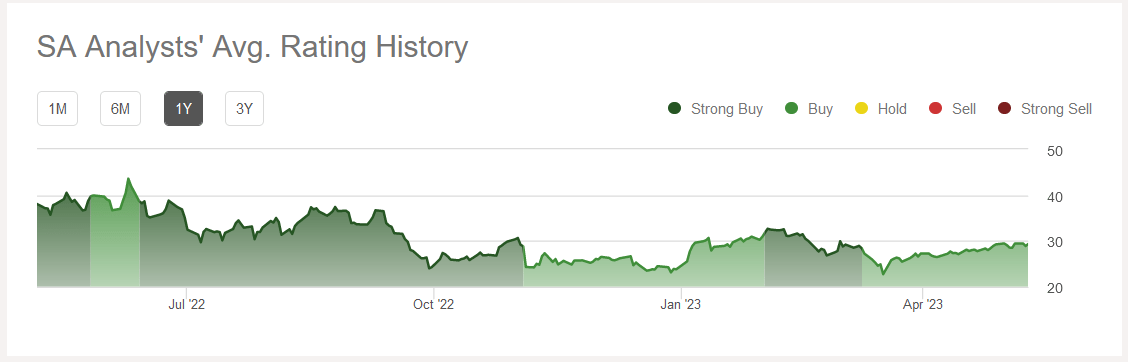

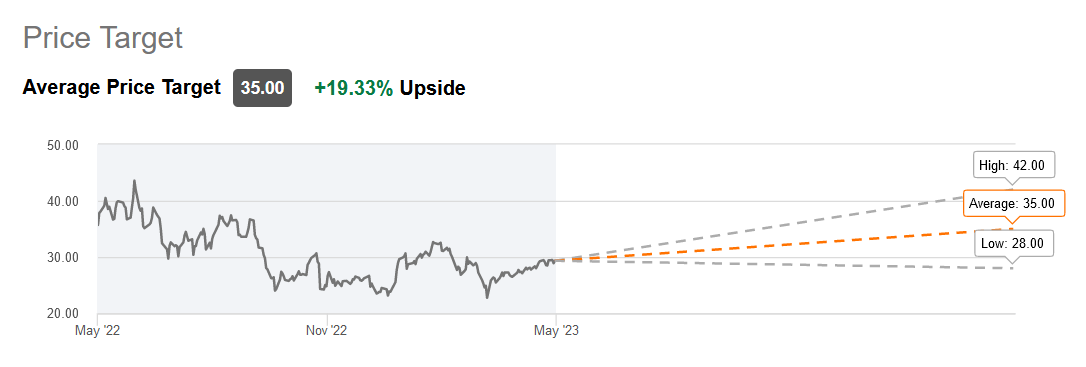

Seeking Alpha analysts' overall were strongly bullish as the stock trended downward. Wall Street analysts were bullish as well with an average price target of $35 for FRG.

{kind=link}

Seeking Alpha: FRG Analyst Ratings Chart.

{kind=link}

Seeking Alpha: Wall Street Analyst FRG Price Targets.

Why does this matter? From my read of things there were a number of investors here who had high hopes for this company even when it was trading in the $40 range. To see the stock lose 25% of its value through a take-private transaction certainly has to sting for bulls. Is that enough to cause bulls to vote-down a proposal? My guess is likely no, especially if a superior deal does not materialize.

Taking a look at the 2023 proxy we can find only two other >5% owners involved here outside of management’s interests: FMR LLC (5.5%) and BlackRock (5.4%). FMR LLC is Fidelity meaning both of these holdings are likely passive institutional holdings; these are not activist investors. So I don’t think it’s likely you’ll see these majority owners making noise about this transaction.

Which brings us back to the question of where things are for the common? My guess is that common owners are looking at a $30 takeout price. I don’t think another deal will come through nor do I think the deal is likely to be rejected.

I could always be wrong.

The stock closed at $29.33 on the day of the announcement. That means the spread on the $30 deal is just 2.3% if I'm right. And we can ignore any possible dividends because they’ve already been suspended for FRG. Today common shareholders stand to gain more from this deal by swapping to the preferred shares. A strategy to simply sell FRG and buy FRGAP as long as the deal spread remains higher on the preferreds seems reasonable.

That said, there is a risk that a superior deal is sourced during the go-shop period. Even a $32 offer, only a 6% increase to the current one, would bring the expected return for common shareholders to 9.1%. At that point holding the common shares would be the better course of action.

But as I said above, I don’t believe a higher offer is likely. Choose how you want to play this though on your own terms. One thing of note is the amount of lawsuit announcements that followed the deal news. While not altogether atypical, it does further reflect the negative sentiment folks seem to have regarding the deal.

{kind=link}

The $30 Franchise Group Offer in Summary

At this juncture the preferred shares still seem to offer a better risk-reward than the common. Management has said directly that they intend to redeem the preferred prior to the take-private transaction so there is little question as to what will be happening with these. Further, even if they do not redeem these shares the preferreds are entitled to conversion rights which will essentially have them convert at par value any way if they pursue the deal.

I do not believe a higher offer is likely given it’s been in the news for a while that FRG may be looking to go private. But I could be wrong on this, and certainly an army of lawyers will be looking for ways to advocate for shareholders. If there ends up being a higher offer made even at just $32 that would shift the risk-reward setup to the common in that scenario.

With my assumption that a higher offer is unlikely, it seems that selling FRG and buying FRGAP is a logical course of action. With FRGAP offering a 6% upside on this deal and FRG only 2.3%, I trust you can do the math.

Another option here is just take the chips off the table and recycle your capital into US Treasuries.

For further details see:

Franchise Group: The Preferred Shares Still Offer Better Value In Take-Private Deal