FNV:CC - Franco-Nevada: A Better Q3 Outlook With Rebound In Energy Prices

2023-09-25 01:16:12 ET

Summary

- The GDX has had a tough start to the year, but Franco-Nevada has once again been a relative sanctuary.

- FNV's upcoming Q3 results should benefit from higher oil prices and easier comps vs. H1 2023 where revenue was negative down year-over-year.

- In this update, we'll look at the H2 outlook, how oil sentiment is trending to see if this oil rally has legs and whether FNV offers a margin of safety.

It's been a tough four-month stretch for the Gold Miners Index ( GDX ), with the sector reverting from a brief period of outperformance vs. the S&P 500 ( SPY ) with a double-digit year-to-date gain to a negative year-to-date return, with several developers down over 30% year-to-date. Fortunately, the royalty/streaming names have provided somewhat of a sanctuary from the selling pressure, with Franco-Nevada ( FNV ) up 4% for the year while Royal Gold ( RGLD ) has been relatively flat. The outperformance can be attributed to these companies being shielded from the sticky inflationary pressures because of their superior business model and also being immune to the recent rise in oil prices which could once again pinch margins in Q3 (albeit not to the same effect as Q2 through Q4 2022). In this update, we'll look at Franco-Nevada's upcoming Q3 results and any recent developments, and whether the ~20% correction has offered a low-risk entry point in the stock.

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Upcoming Q3 Results

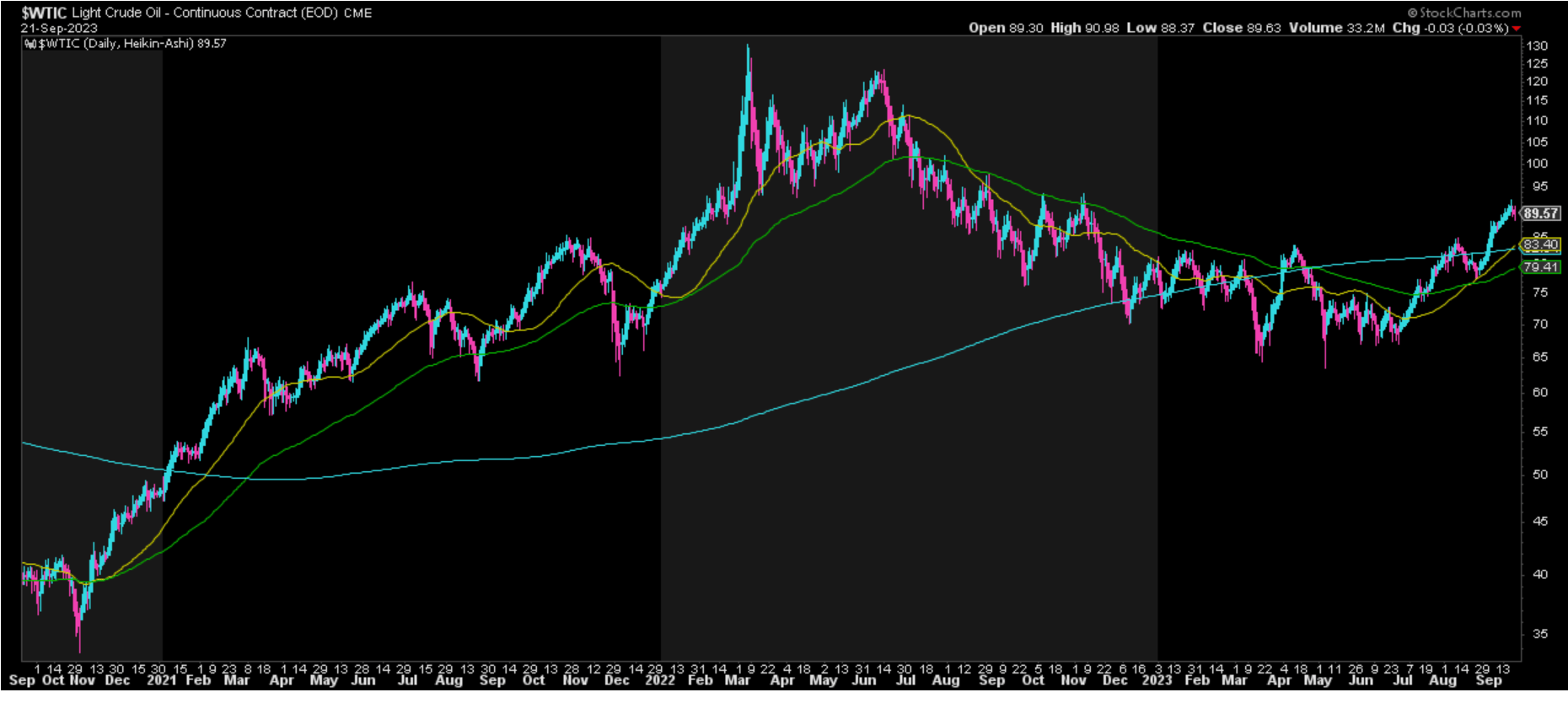

Franco-Nevada will its Q3 results by the first week of November, and while the setup still wasn't great heading into the quarter with weaker palladium ( PALL ), natural gas ( UNG ), and oil prices ( USO ) offsetting the strength in precious metals, the company has got some help from oil prices, which have soared ~35% off their Q2 lows and traded up to new yearly highs. This has left Franco-Nevada in a unique position, given that while some miners will have to work against higher energy prices in the quarter, Franco-Nevada is insulated from these costs and simultaneously a beneficiary of higher oil prices (oil made up ~12% of revenue in 2022) because of its energy segment. Notably, these prices are now back above its $80/barrel WTI assumption for 2023 and its five-year outlook, reverting to a slight tailwind from a headwind in the first half of the year amid the downside volatility in oil prices.

{kind=link}

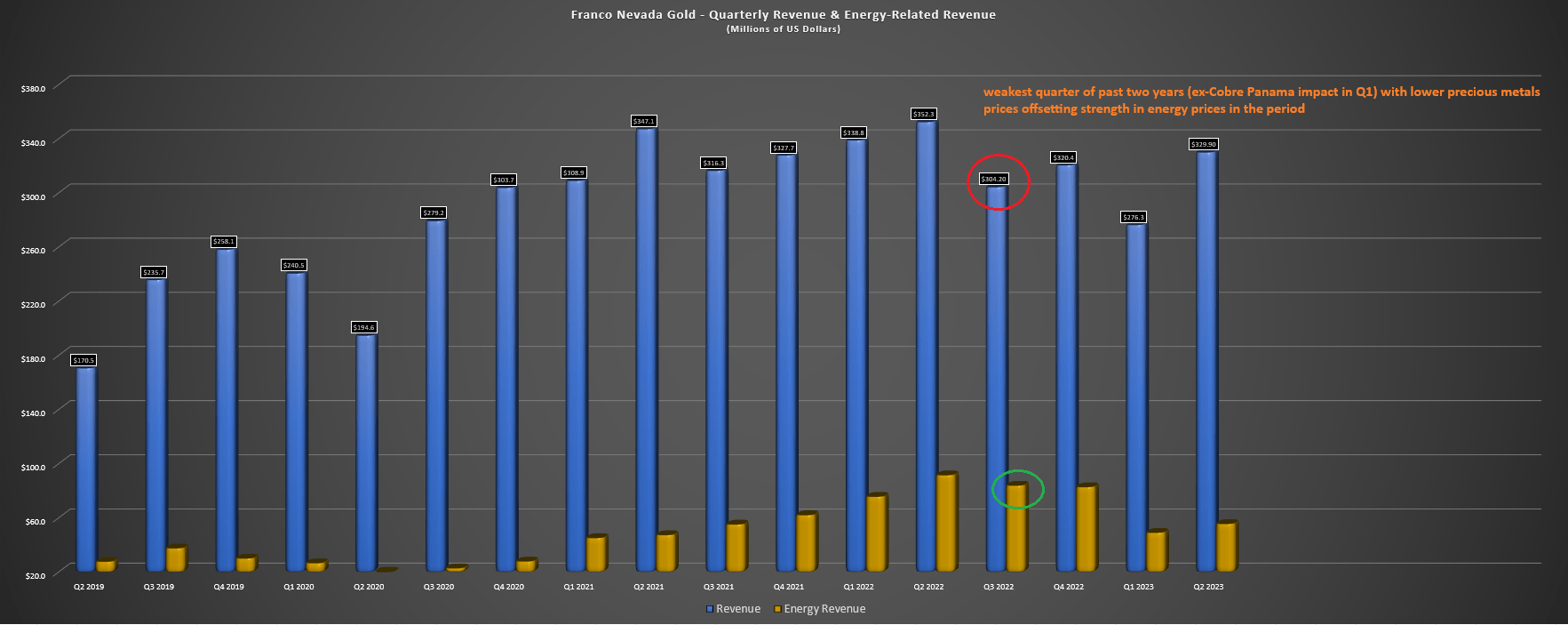

As for the precious metals front which makes up ~75% of its total revenue, the company has the opposite setup, lapping very easy year-over-year comps on gold and silver. This is because gold and silver prices correctly sharply in Q3 2022 and averaged $1,728/oz and $19.22/oz, respectively, but prices should average closer to $1,930/oz and $23.40/oz in Q3, assuming they don't collapse to finish quarter-end. The result would be a 12% higher gold price and a 22% higher silver price, translating to a meaningful improvement in the company's revenue from the $304.2 million reported in Q3 2022. And based on consensus estimates of ~$332 million for Q3 2023, we should see revenue up 9% year-over-year, a significant improvement sequentially from [-] 15% in Q1 and [-] 7% in Q2.

Franco-Nevada - Quarterly Revenue & Energy Related Revenue - Company Filings, Author's Chart

{kind=link}

So, is there any bad news?

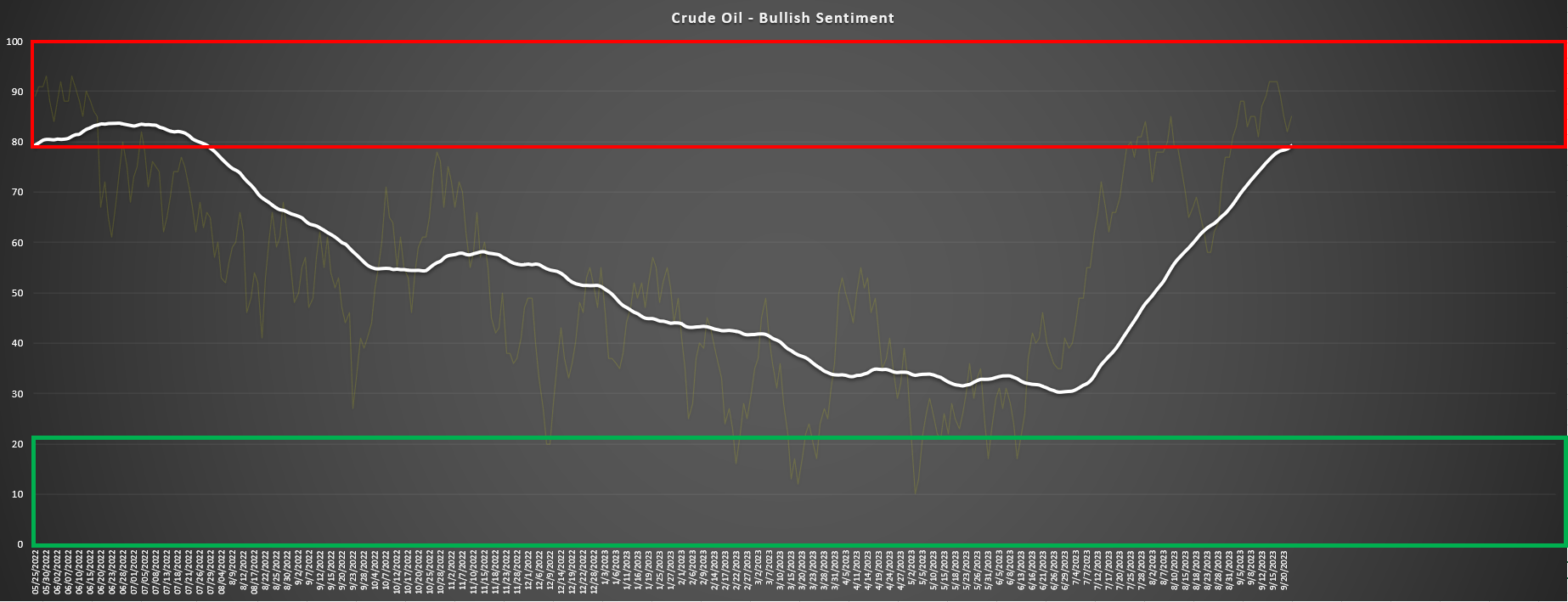

While the recovery in oil prices is a positive for this portion of Franco-Nevada's business, sentiment for oil is heading back towards nosebleed territory, with four bulls for every one bear over the past two months. As shown in the below chart, this has typically led to a correction in oil prices, with the most recent sell signal occurring on May 26th, 2022 at ~$114.00/barrel, just one week before oil would peak at ~$122.00/barrel, with a two-month and four-month forward return following the signal of [-] 17% and [-] 32%, respectively. Obviously, this time could be different, but this suggests that while Franco-Nevada will benefit from higher oil prices in Q3, we could see some giveback in Q4 2023 and Q1 2022 given that sentiment sell signals typically result in at least four months of selling pressure to adequately reset sentiment levels. To summarize, while the tailwind in Q3 is certainly a positive, I'm less optimistic about oil staying above $90.00/barrel sustaining the $90.00/barrel level short-term.

Oil Long Term Sentiment - Daily Sentiment Index Data, Author's Chart

{kind=link}

Recent Developments

Moving over to recent developments, it's been a relatively quiet quarter for Franco-Nevada in terms of deal-making, but the company continues to see progress at construction-stage or recently completed royalty assets. These include a scope change and solid progress at the Valentine Project in Newfoundland that could pull ounces forward in the mine plan (3.0% NSR), the imminent declaration of commercial production at Magino (2.0% NSR) in Ontario, the declaration of commercial production at Seguela (2.0% NSR) in Cote d'Ivoire, and solid progress at Greenstone (2.0% NSR) and Posse (1.0% NSR), which are set to reach commercial production within 12-18 months. While none of these projects are massive in scale from an attributable ounce standpoint to Franco-Nevada, they combine for a meaningful contribution, and are expected to lift Franco-Nevada's attributable production to ~800,000 gold-equivalent ounces [GEOs] in FY2027.

{kind=link}

Among larger projects, Gold Fields noted that it is confident in its ability to pour first gold in Q4 of this year at Salares Norte, with the 1.0% NSR (assumes buyback is exercised) representing an incremental ~$8.5 million per annum in contribution based on the asset's ~450,000 GEO production profile in its first seven years. Meanwhile, construction at Tocantinzinho is also progressing on schedule (51% complete), with the project expected to reach commercial production in H2 2024. And while this asset may not rival Salares Norte in scale with ~196,000 ounces in the first five years, the deliveries are expected to be much more significant due to the large streaming deal on this asset, with ~12.5% of gold produced or ~24,500 GEOs per annum at 20% of spot until 300,000 ounces have been delivered.

Elsewhere among organic growth projects, Island Gold is inching closer towards doubling its production in 2026 (0.62% NSR), and Agnico Eagle ( AEM ) continues to work on increasing production from its Kirkland Lake Camp (#4 Shaft integration and Amalgamated Kirkland) where Franco-Nevada holds a 1.5% NSR, with an additional 2.0% NSR at Amalgamated Kirkland and other areas west of the Macassa Mine. As noted in Agnico's most recent update, the Macassa mill is expected to reach full capacity of 1,650 tonnes per day by mid-2024, with the asset no longer mine-constrained given the graduation to a more productive shaft (6.5 meter in diameter with two skips). Notably, this shaft in addition to de-risking the operation and increasing hoisting capacity also allows for better underground working conditions (improved ventilation), but lower unit costs and more effective exploration east of the South Mine Complex, benefiting Agnico Eagle and also those holding royalties on the mine, like Franco-Nevada.

{kind=link}

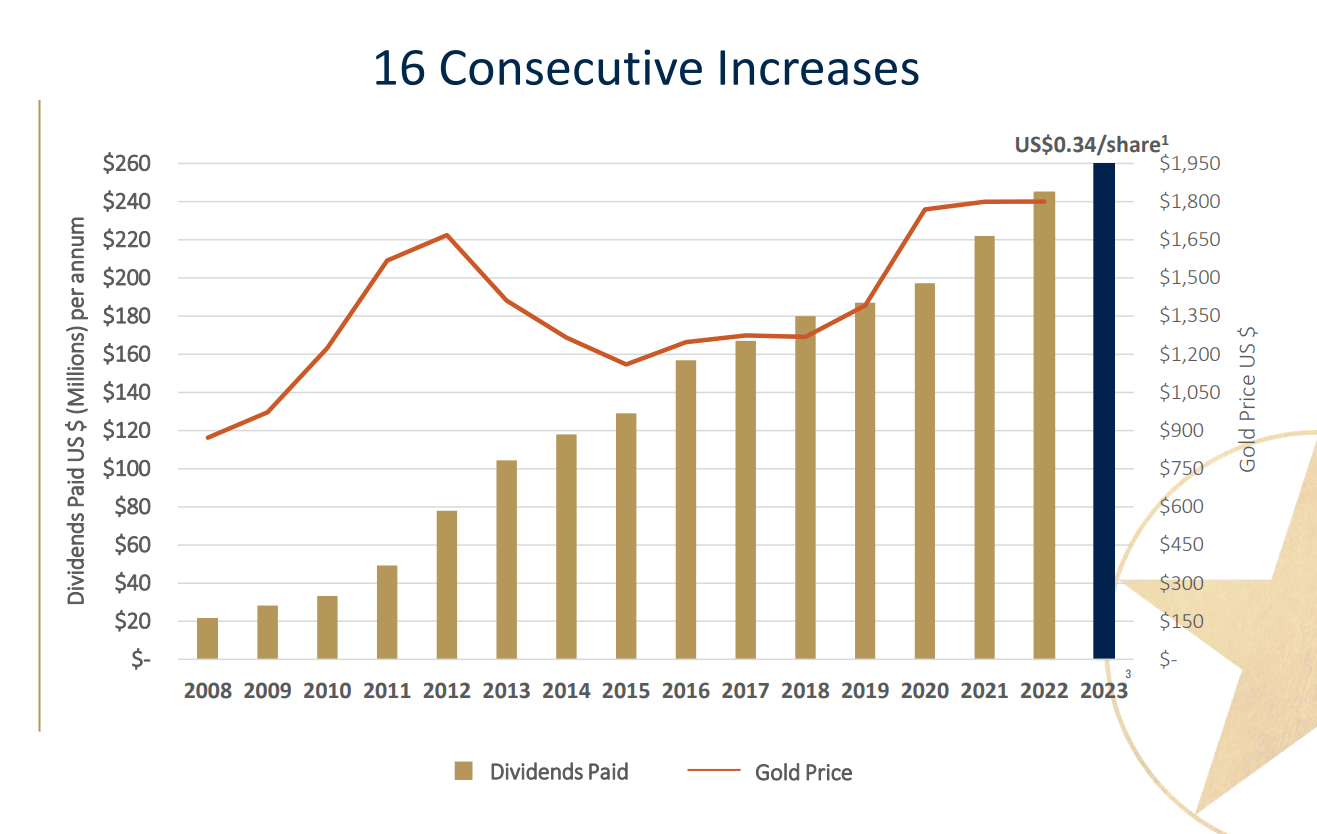

To summarize, while it's been a volatile year for commodity prices which has created some noise in Franco-Nevada's attributable ounce production and financial results, there is a path to much higher production from key assets, with other opportunities including a potential expansion to 950,000+ ounces per annum at Detour Lake (higher throughput + underground), and meaningful production from other assets in the development pipeline yet to begin construction like Eskay Creek, Stibnite, and Copper World. So, while Franco-Nevada may have had a tough H1 which was impacted further by a temporary rift between the Panamanian Government and First Quantum at Cobre Panama, organic growth in stages over the next several years should allow Franco-Nevada to continue reporting record financial results on an annual basis going forward and increasing its dividends to shareholders.

Franco-Nevada - Dividend Track Record - Company Presentation

{kind=link}

Let's dig into the valuation below and see whether investors are getting a margin of safety for this growth:

Valuation

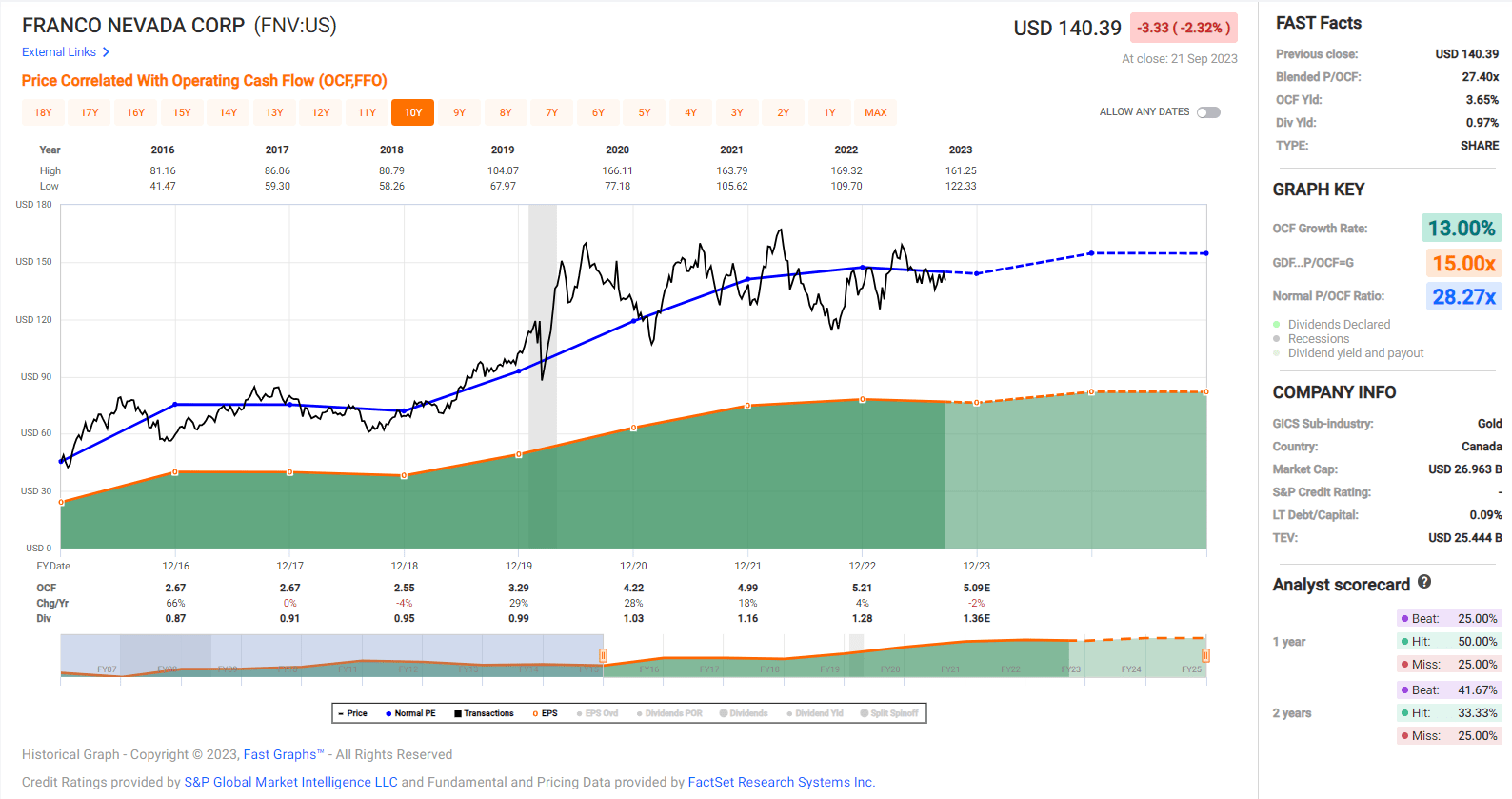

Based on ~193 million fully diluted shares and a share price of US$142.00, Franco-Nevada trades at a market cap of ~$27.4 billion. This is one of the highest market capitalizations sector-wide and it's certainly justified with the company having ~116 producing assets (47 precious metals), making it the most diversified precious metals royalty/streaming company globally. That said, the company continues to trade at a premium multiple, trading at over 28x FY2023 cash flow per share estimates, a slight premium to its historical multiple. And even if we use a premium multiple of 30.0x cash flow given the company's unrivaled position (greater scale and superior diversification across assets and jurisdictions) and FY2024 estimates of US$5.45, this translates to a fair value of US$163.50.

Franco-Nevada Historical Cash Flow Multiple - FASTGraphs.com

{kind=link}

This upside case may interest some investors given that Franco-Nevada is arguably the lowest-risk name in the sector with industry-leading margins, diversification, and a rock-solid balance sheet. However, I am looking for a minimum 25% discount to fair value to justify buying large-cap names in commodity sectors, pointing to an ideal buy zone of US$122.65 or lower. This suggests that there still isn't a margin of safety in place for the stock. And from a relative value standpoint, Sandstorm Gold Royalties ( SAND ) may not match Franco-Nevada's quality, but it has significantly improved its portfolio with better diversification, an increased weighted-average mine life, and larger scale, yet trades at one-third of Franco-Nevada's valuation at less than 10x FY2024 cash flow per share estimates. So, given that I prefer to buy hated companies trading at deep discounts to fair value, I continue to see SAND as the better reward/risk setup, even if it carries a higher risk (weaker balance sheet).

Summary

Franco-Nevada was on track to lap much easier comps in Q3 given the softness in gold and silver prices in Q3 2022, but it was still going to come up against an elevated oil price for its energy segment with prices sitting below $70.00/barrel heading into the quarter. However, the rebound in energy prices has improved this outlook, with oil averaging ~$79.00/barrel in Q3 vs. $73.78/barrel in Q2, and gold and silver prices are also much higher year-over-year. That said, while the outlook is better, sentiment on oil is now overheated short-term, and while FNV may positioned for a better Q3 than expected at the onset, I don't see nearly enough margin of safety at current levels to justify owning the stock. In summary, while I see FNV as a top-5 name from a quality standpoint sector-wide, I continue to see better bets elsewhere in the sector.

For further details see:

Franco-Nevada: A Better Q3 Outlook With Rebound In Energy Prices