LIFZF - Franco-Nevada: A Commodity Weighted Portfolio Of These Smaller Royalty Companies Is 50% Cheaper

2023-06-07 08:07:26 ET

Summary

- Franco-Nevada trades at around a medium-term 2.8% earnings yield which is expensive compared to other precious metal royalty companies.

- This is especially true, given that its energy and iron ore assets accounted for around a third of its earnings in 2022.

- A portfolio of Osisko Gold Royalties, Labrador Iron Ore Royalty Corporation, and Freehold Royalties trades at around twice the earnings yield.

- The companies in this portfolio all own long-life assets of at least equivalent quality to Franco-Nevada’s assets.

- Therefore, it makes more sense to own a commodity-weighted portfolio of these companies as it sells at a 50% discount to Franco-Nevada.

Thesis

Franco-Nevada ( FNV ) trades at a premium to other royalty companies which I believe is unjustified based on a sum of parts analysis of its precious metals, energy and iron ore assets. It trades at a medium-term earnings yield of around 2.8%, which represents a 100% premium to a commodity weighted portfolio composed of royalty companies Osisko Gold Royalties (OR), Labrador Iron Ore Royalty Corporation ( LIFZF ) and Freehold Royalties (FRHLF). In addition, the assets of these three royalty companies are located in safer jurisdictions and often have more production upside. Therefore, I would recommend selling Franco-Nevada and replacing it with a portfolio of these royalty companies.

Company Overview

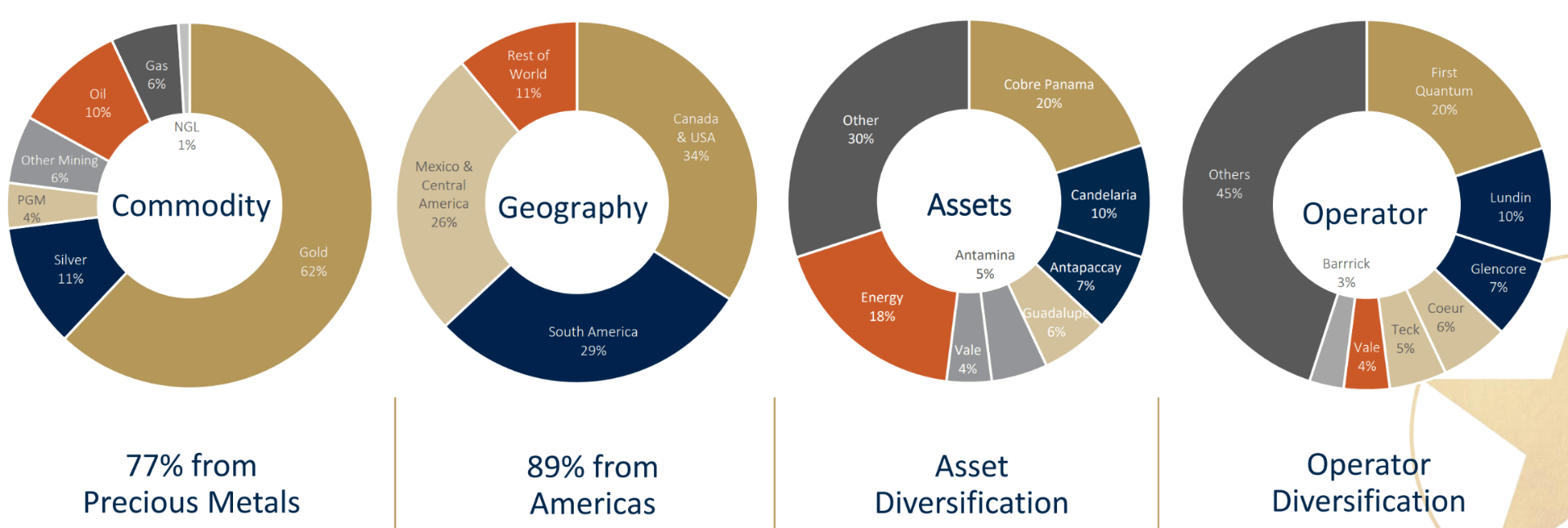

Franco-Nevada is the worlds' largest precious metal focused royalty and streaming company by market capitalization. Gold accounts for 62% of revenues, with silver and platinum group metals accounting for 11% and 4% of revenues respectively (see figure below). Uniquely among the larger mining royalty companies, it has exposure to oil and gas assets, which account for 17% of revenues. Most of its remaining revenues come from iron ore royalties on Vale's ( VALE ) mines in Brazil and its stake in Labrador Iron Ore Royalty Corporation (LIORC). It is heavily exposed to mines in Latin America which may entail some risk. Six royalties/streams account for over 50% of revenues, which could cause problems for Franco Nevada if one of those mines runs into issues, which was recently on display with First Quantum's ( FQVLF ) dispute with the Panama government.

Franco-Nevada May Investor Presentation

{kind=link}

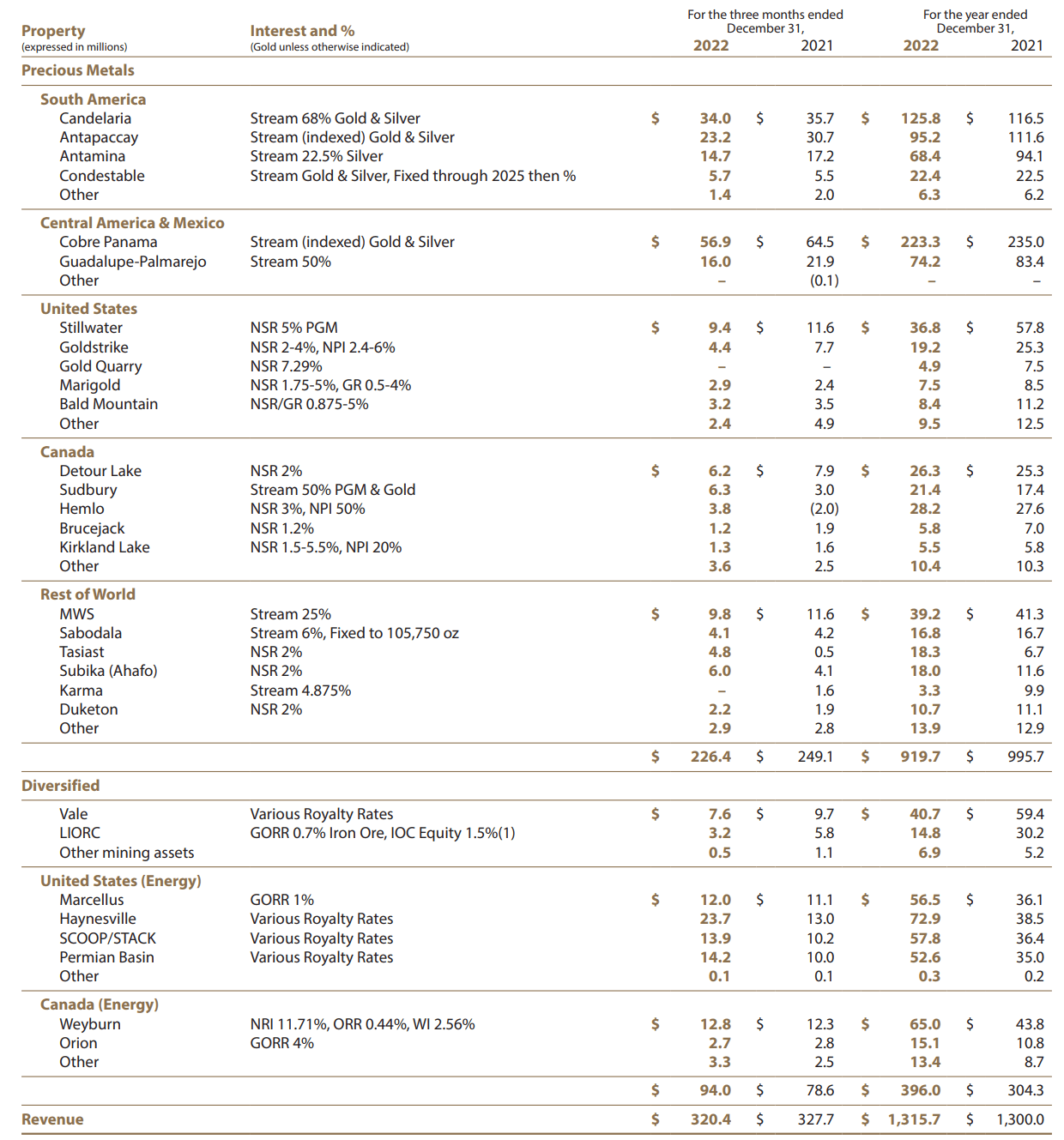

A more detailed breakdown of revenues by assets is displayed in the figure below. All of the energy assets are in Canada and the US, which account for half of its total Canada and US revenue exposure, which means its precious metal exposure is more heavily weighted towards Latin America. The precious metal assets are mainly streams, while the diversified assets are mainly royalties. Given that payments are generally associated with streams, but not for royalties, this needs to be considered when calculating the proceeds generated by the assets. The streams cost of sales was $158.2 million in 2022, while the energy cost of sales was $16.6 million . Making these adjustments to the revenue values, precious metals accounted for $761.5 million in proceeds or 67% of total, iron ore assets accounted for $62.4 million in proceeds or 5% of total, and energy assets accounted for $317.0 million in proceeds or 28% of total. This means that the diversified assets are more important to Franco-Nevada's bottom line than is reflected in the revenue breakout.

Franco-Nevada 2022 Annual Report

{kind=link}

Company Financials

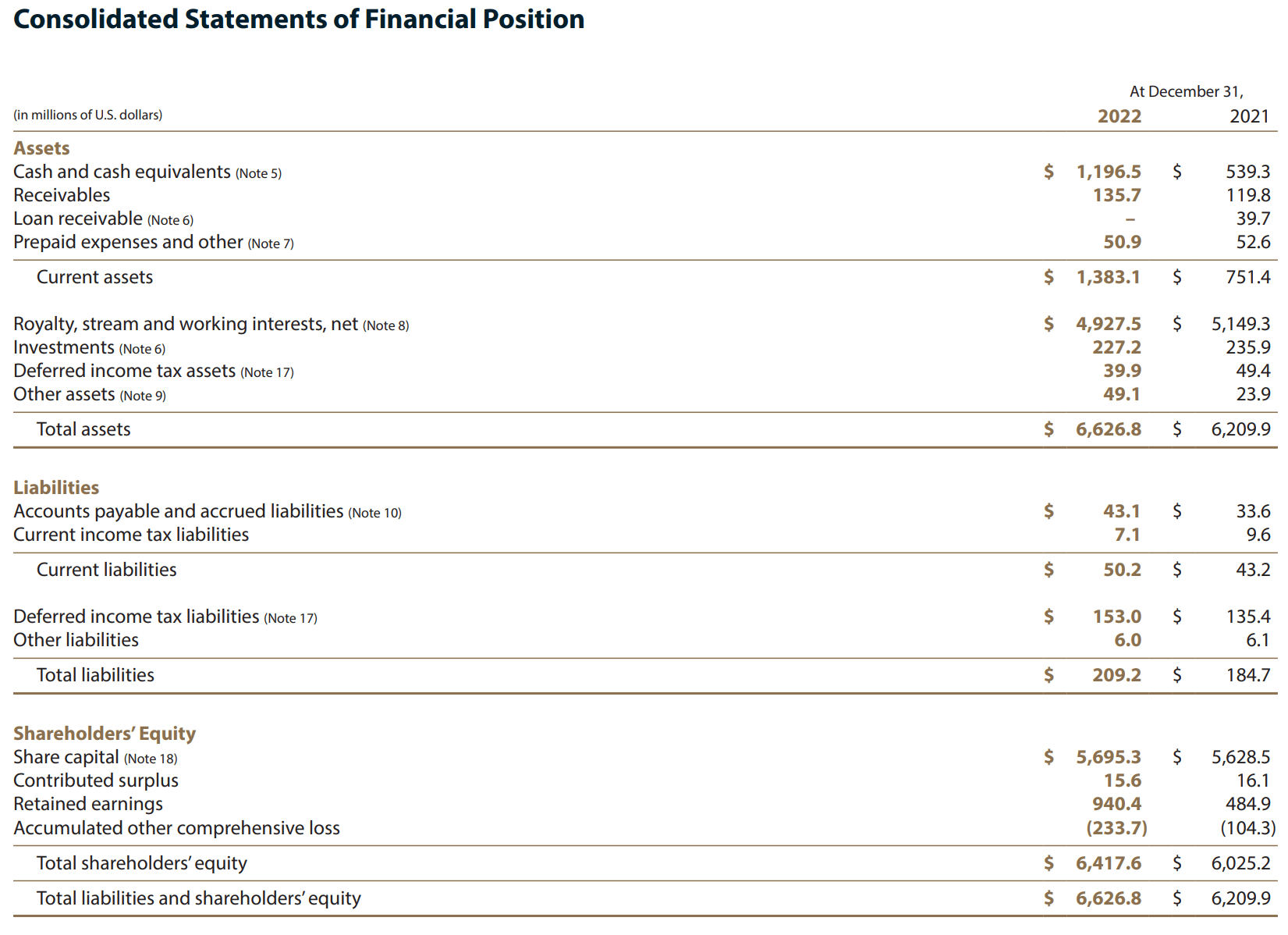

Franco-Nevada has a very strong balance sheet with over $1 billion in cash and little to no debt (see table below). This compares with a market capitalization of $27.3 billion using a share price of $142. It has net assets of around $6.4 billion resulting in a price to NAV (P/NAV) ratio of 4.3, which is likely overstated as the royalties are valued at just $4.9 billion even though they generate annual revenues in excess of $1 billion. Franco-Nevada also has some investments, the majority of which is in LIORC which owns a royalty and equity interest in the Iron Ore Company of Canada mine in Labrador. Franco-Nevada owns 10% of LIORC and treats it as a flow through royalty.

Franco-Nevada 2022 Annual Report

{kind=link}

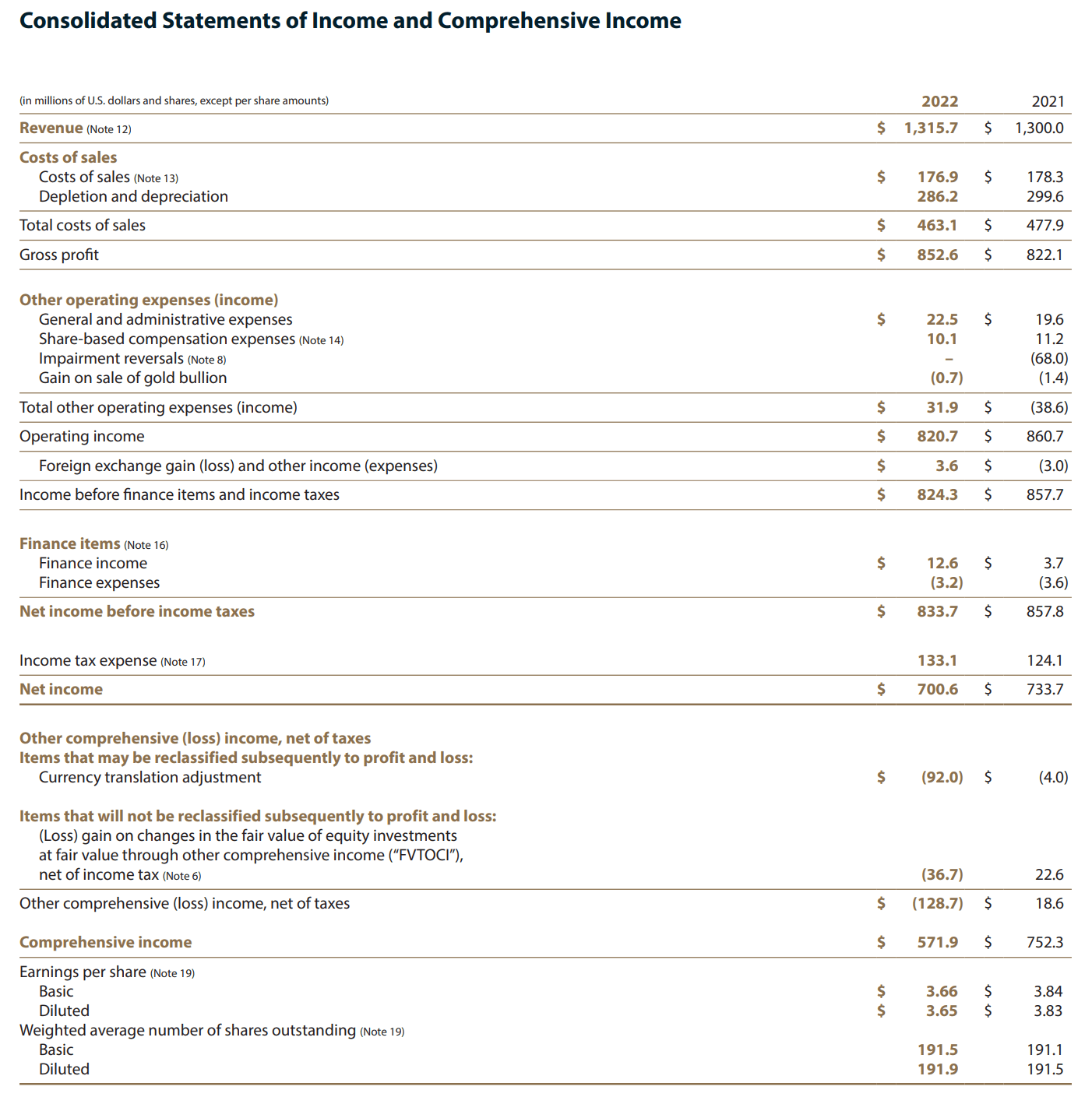

In 2022, Franco-Nevada had revenues of $1.3 billion (see table below). After netting out the costs of sales, this translates to royalty and stream proceeds of $1.1 billion. Dividing Franco-Nevada's market cap by these proceeds gives a price to sales (P/S) ratio of 25. Depreciation and taxes are the main expenses with G&A and share-based compensation payments being relatively low. Therefore, most of the net proceeds flow into net income which was $0.7 billion in 2022. This results in a price to earnings ratio (P/E) of 39.

Franco-Nevada 2022 Annual Report

{kind=link}

Company Valuation

Given that some royalty companies trade at less than 10 times P/S such as Ecora Resources ( covered here ) and LIORC ( covered here ), Franco-Nevada trades at a very steep valuation. Granted precious metals focused royalty companies tend to trade at a premium to industrial metals royalties, but Franco-Nevada trades at a premium even to its precious metal peers.

Of the six largest precious metals royalty companies, Osisko Gold Royalties had the highest percentage of revenues originating from precious metals in 2022 at 99% . It had revenues (net of cost of sales) of C$202 million , which flowed through to earnings of C$85 million . Using a share price of C$21, gives a market cap of C$3.9 billion. Therefore, it has a P/S ratio of 19, and due to higher relative overhead costs, a P/E ratio of 46.

Osisko is growing rapidly and projects that it will receive around 135,000 gold equivalent ounces ((GEO)) in 2027, compared to 89,367 GEOs received in 2022, which is an increase of 51%. By comparison Franco-Nevada expects to receive around 790,000 GEOs in 2027 compared to 729,960 GEOs received in 2022, which is an increase of 8%. Assuming conservatively a linear relationship between revenues and profits (even though profits would likely rise faster due to lower relative overhead) Osisko's P/S ratio would decrease to 13 and its P/E ratio would decrease to 30. By comparison Franco-Nevada's P/S ratio would decrease to 23 and its P/E ratio would fall to 36.

In addition, Franco-Nevada has energy and iron ore assets which tend to trade at lower multiples. Iron ore royalty company LIORC, which Franco-Nevada holds a 10% equity stake in, distributes all its free cash flow as dividends and is currently at a trailing dividend rate of 10% . The oldest major Canadian oil and gas royalty company, Freehold Royalties, generated net income of C$209 million in 2022, compared to a market cap of C$2.1 billion using a share price of C$14, which gives a P/E ratio of 10.

As discussed above Franco-Nevada has a commodity weighted asset portfolio of 67% precious metals, 28% energy and 5% iron ore which is expected to generate an earnings yield of 2.8% (1/36). By comparison a portfolio holding 67% Osisko with an expected earnings yield of 3.3% (1/30), 28% Freehold with a current earnings yield of 10% (1/10), and 5% LIORC with a current earnings yield of 10%, would provide a combined earnings yield of 5.5% (67%*3.3% + 28%*10% + 5%*10%). Given that Freehold and LIORC will likely increase their earnings over time, Franco-Nevada's portfolio can be replicated by a portfolio of these three companies at a 50% discount.

Risks to Thesis

Three factors that could narrow Franco-Nevada's premium are changes to commodity prices, the quality of existing assets and the quality of future assets purchased.

Commodity price changes are unlikely to narrow the Franco-Nevada premium as Osisko, Freehold and LIORC have very similar commodity exposures to Franco-Nevada's precious metals, energy and iron ore assets respectively. Freehold and Franco-Nevada both have exposure to more oil assets than gas assets. LIORC has more exposure to high grade iron ore than Franco-Nevada, but this is likely a positive for LIORC as only high grade iron ore can currently be used in electric arc furnaces, which are essential for decarbonizing the steel industry. Both Osisko and Franco-Nevada have exposure to more gold than silver assets. While Franco-Nevada in addition has exposure to platinum group metals (PGMs), this only accounted for around 4% of Franco-Nevada's revenue in 2022.

The quality of assets is impacted by factors such as future volume increases, country risk and operator risk. While Franco-Nevada's asset operators are mostly large and well capitalized, around half of their assets by value are located in Latin America, which has recently become a riskier region. Regarding, future volume increases Franco-Nevada stated that they have exposure to 18.8 million measured and indicated (M&I) royalty ounces, which compares to the around 790,000 GEOs Franco-Nevada expects to receive annually in the medium term. They also stated that their M&I (inclusive) royalty ounce mine life was 32 years in 2021, which is impressive and demonstrates the quality of their deposits. However, Osisko stated they have around 1.9 million proven and probable (P&P) and 4.1 million M&I (exclusive of P&P) royalty ounces in 2022, which compares to the around 135,000 GEOs they expect to receive in the medium term. Dividing the royalty ounces by the 135,000 GEOs gives a royalty ounce mine life of 44 years, which is much higher than Franco-Nevada's mine life. In addition, Osisko's asset operators are also large and well capitalized and 73% of Osisko's 2022 GEOs came from mines in Canada. Therefore, Osisko's assets may actually be of higher quality than those of Franco-Nevada. Both Franco-Nevada's and Freehold's energy assets are located in Canada and the U.S. and are held by well capitalized producers. The quality of Freehold's assets are demonstrated by the fact that asset production increased from 9.8 thousand barrels of oil equivalent per day (boe/d) in 2020 to 14.1 thousand boe/d in 2022; and proved developed producing, total proved and probable reserves increased from 29.4 million barrels of oil equivalent (MMBOE) in 2020 to 54.5 MMBOE in 2022. LIORC forms are a large part of Franco-Nevada's iron ore assets and therefore the iron ore assets are likely of similar quality.

Franco-Nevada could increase it asset value per share by buying new royalties and streams, as it has a strong balance sheet and can borrow debt cheaply. However, other competitors such as Osisko could also do this, which would keep the valuation gap wide. Also, given Franco-Nevada's high market capitalization it might be difficult for them to find assets of significant enough size to dramatically increase its per share asset value. Alternatively, Franco-Nevada could buy a smaller competitor such as Osisko which trades at a lower P/NAV ratio. However, they would likely have to do this at a premium to current stock price, which would make it even more attractive to hold stock in smaller royalty companies such as Osisko, Freehold and LIORC.

Final Thoughts

If one were to equal weight purchases of Osisko, Freehold and LIORC in a portfolio, this would result in an average earnings yield of 7.7% (33%*3.3% + 33%*10% + 33%*10%), which is higher than the commodity weighted earnings yield of 5.5% detailed above. This points to the large discount non-precious royalty companies trade at compared to precious metals royalty companies. Therefore, if one is agnostic about commodity exposure, it would make more sense to buy non-precious royalty companies, as they would provide much higher future returns at current prices.

For further details see:

Franco-Nevada: A Commodity Weighted Portfolio Of These Smaller Royalty Companies Is 50% Cheaper