FNV - Franco-Nevada: Another Record Quarter

Summary

- Franco Nevada released its Q2 results last month, reporting record quarterly revenue of $352.3 million, a 1% increase from the year-ago period.

- This was despite lapping very difficult comps (35% two-year revenue growth rate in Q2 2021), and was helped by higher energy prices, setting FNV up for record earnings in 2022.

- However, with crude oil prices well off their highs and it being unclear whether precious metals will pick up the slack, we could see annual EPS peak short-term in FY2022.

- During periods of decelerating earnings growth, we often see multiple compression, and at ~1.9x P/NAV and ~34x forward earnings, I don't see enough of a margin of safety just yet.

It was a mixed Q2 Earnings Season for the Gold Miners Index ( GDX ), but Franco Nevada ( FNV ) has stood head and shoulders above the rest. This was evidenced by the company reporting record revenue and earnings per share in Q2, benefiting from a sharp increase in energy prices, which offset much lower silver/iron ore prices, and fewer gold/silver ounces sold. However, with oil prices looking like they've peaked, FNV's significant tailwind could become a headwind in H1 2023, creating difficult comps. So, with the stock trading at a massive premium to its peer group (~1.9x P/NAV), I believe it makes sense to be patient for lower prices before rushing into the stock.

{kind=link}

Detour Lake Mine (Agnico Eagle Presentation)

Q2 Results

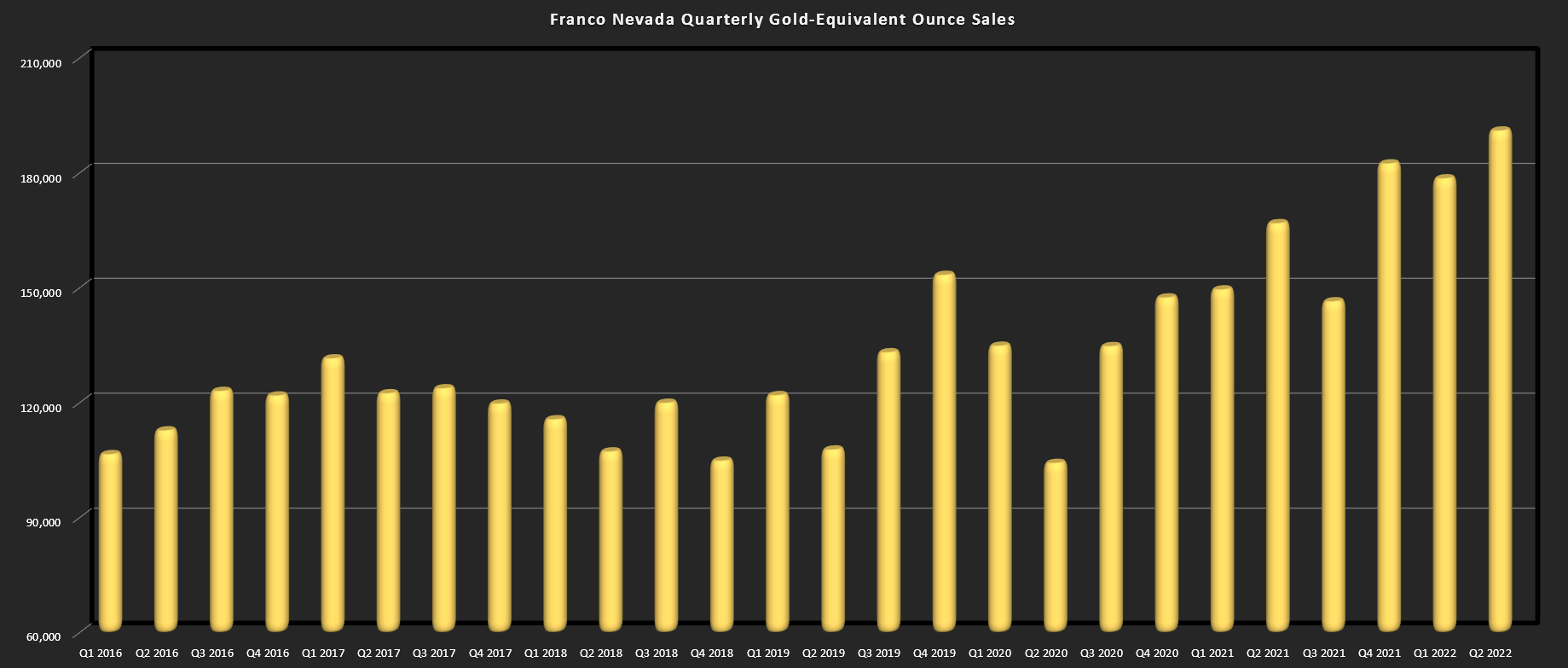

Franco Nevada released its Q2 results last month, reporting quarterly sales of ~191,100 gold-equivalent ounces [GEOs], a 1% decline from the year-ago period. This was helped by a record quarter from Cobre Panama with ~98,800 tonnes of copper produced and record mill throughput (~21.2 million tonnes), a much higher contribution from Hemlo, and a better quarter from Detour Lake, which continues to fire on all cylinders. It's also worth noting without the benefit of a double quarter from its Vale royalty, its quarterly GEO production would have been up in the period on a year-over-year basis.

{kind=link}

Franco Nevada - Quarterly Gold-Equivalent Ounce Sales (Company Filings, Author's Chart)

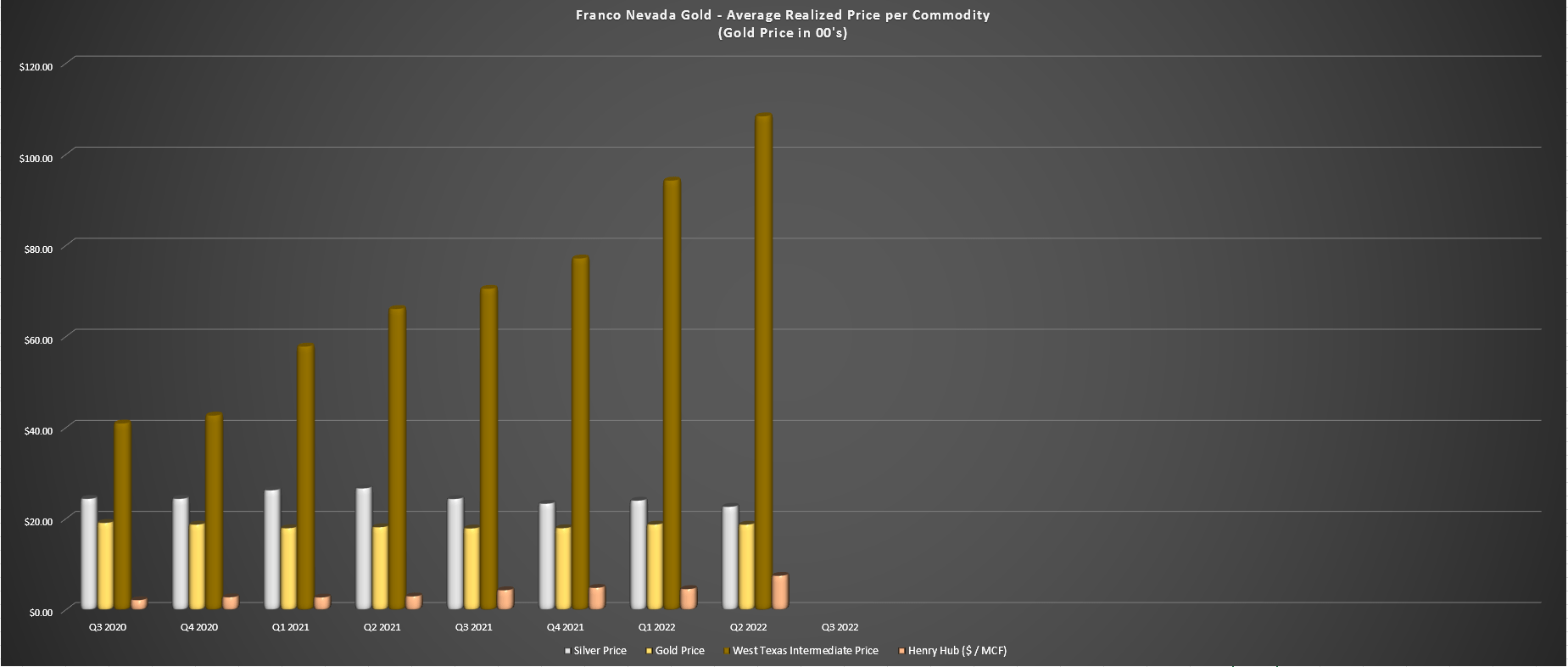

The steady contributions from its precious metals royalty assets/streams, a higher gold price, and much higher energy prices helped Franco Nevada report record revenue of $352.3 million. While this was only a 1% increase year-over-year, the company was up against very difficult comparisons, with revenue having increased 35% from Q2 2021 vs. Q2 2019, a significant growth figure for a company of Franco Nevada's scale. This was also despite a much lower average realized silver price of $22.64/oz in the period (Q2 2021: $26.69/oz), which impacted silver revenue and lower iron ore prices.

{kind=link}

Franco Nevada - Average Realized Prices (Company Filings, Author's Chart)

{kind=link}

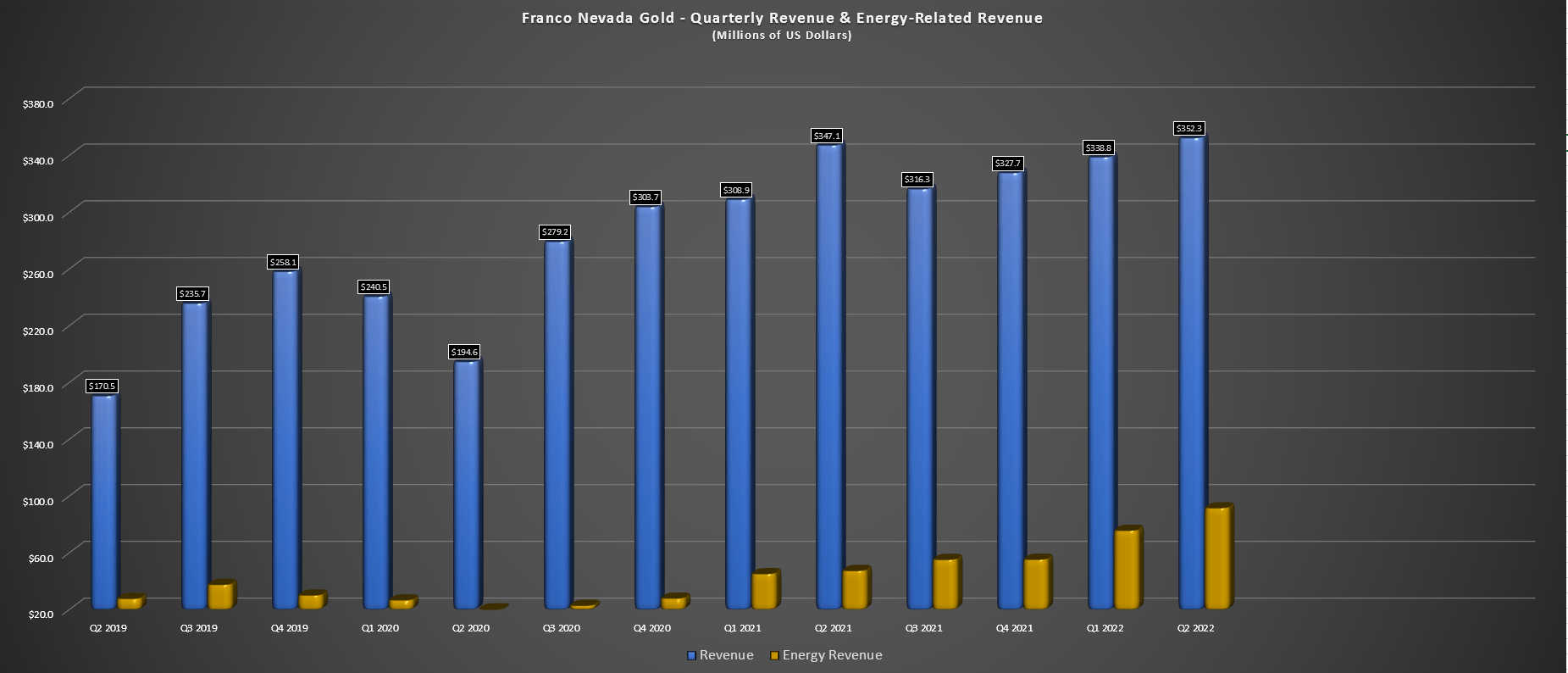

Franco Nevada - Quarterly Total Revenue & Energy Revenue (Company Filings, Author's Chart)

Looking at the charts above, we can see just how significant energy revenue was in the period, increasing from a nearly non-existent contribution in Q2 2020 to more than $91 million in Q2 2022. The growth in energy revenue came in at 93% year-over-year, and the strong contribution has helped Franco Nevada to track well against its FY2022 guidance of 710,000 GEOs at the mid-point despite lower grades at Antapaccay, higher costs at Hemlo combined with a shift in mining areas, and lower platinum and palladium prices which impacted GEOs earned from Stillwater. During Q2, Franco's average realized WTI price was $108.41/barrel, while Henry Hub prices increased to $7.49/MCF.

{kind=link}

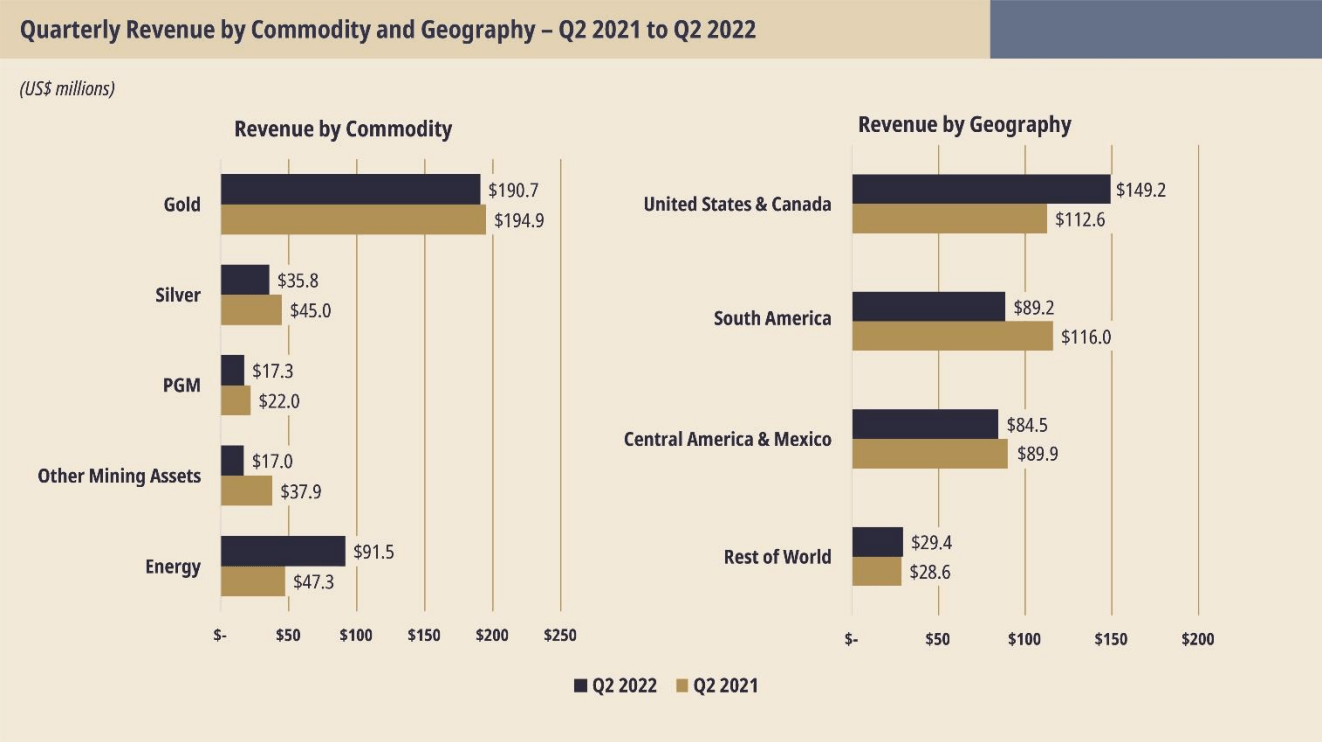

Franco Nevada - Revenue by Commodity/Geography (Company Filings)

To summarize, though Franco Nevada has seen some criticism for its focus on other commodities in the past, it's clear that its energy bets buoyed its sales and earnings in what's been another mediocre period for precious metals. Given the increase in revenue from other segments and the strength in energy prices, Franco Nevada's precious metals contribution dropped to just 70% of revenue, down from 75% in the year-ago period. That said, while energy has been a huge tailwind, as has steady GEO growth from Cobre Panama, crude oil is well off its peak, and attributable production growth will be slower next year.

Recent Developments

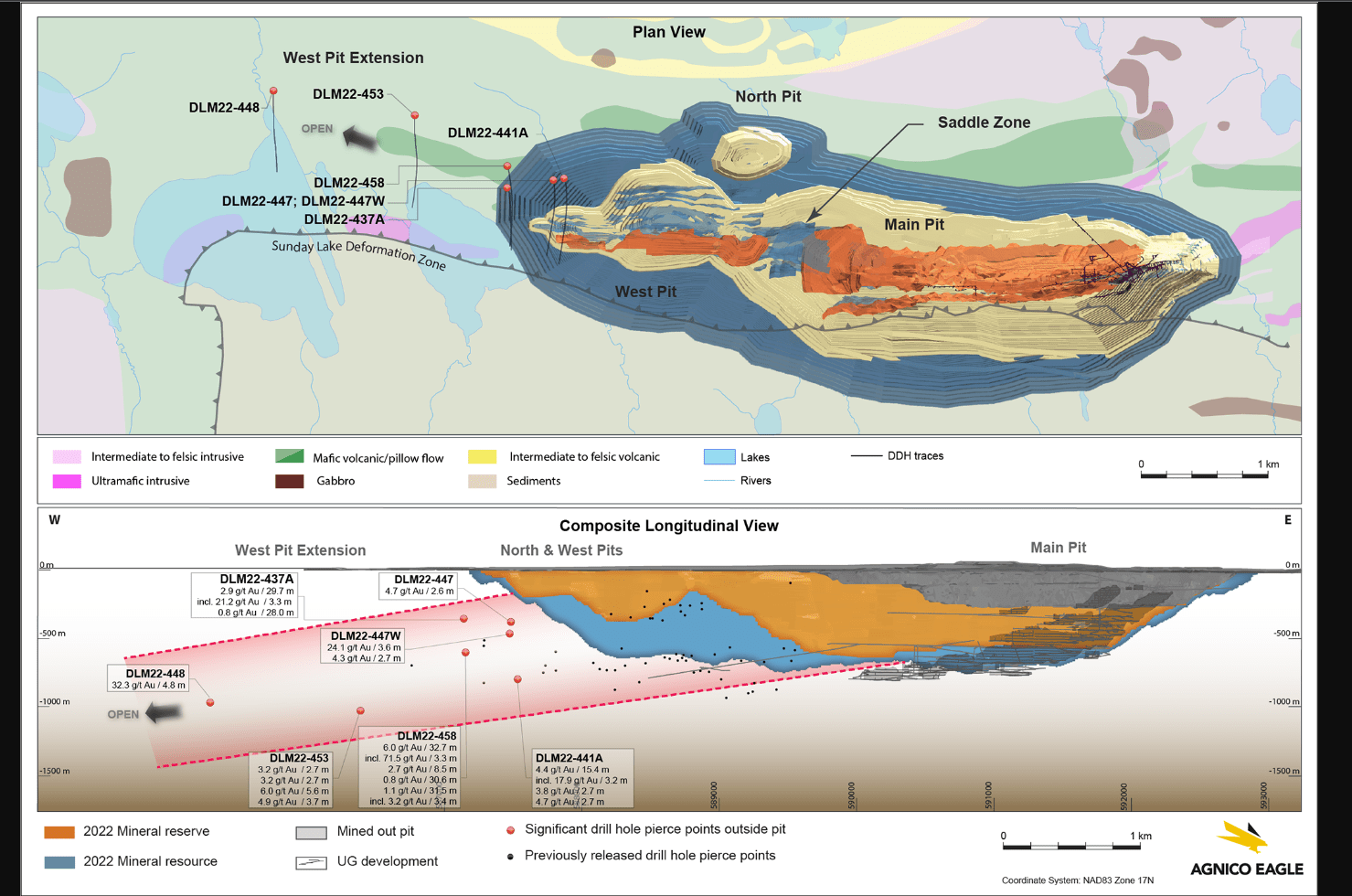

If we look at recent developments, there have been several, with the first being that Agnico Eagle ( AEM ) aims to make its Detour Lake Mine the largest in Canada. This was discussed in its recent Q2 Conference Call, with Agnico having ambitions to turn the ~750,000-ounce per annum mine into a one million-ounce producer. Based on Franco Nevada's 2.0% NSR royalty, this would add over 4,000 GEOs per annum if achieved later this decade, depending on the timing of this expansion. Just as importantly, reserves increased 38% to 20.4 million ounces, extending the mine life to 2052, but given the recent step-outs, I would not be surprised to see the asset produce well into the 2060s.

{kind=link}

Detour Lake Drilling (Agnico Eagle Mines)

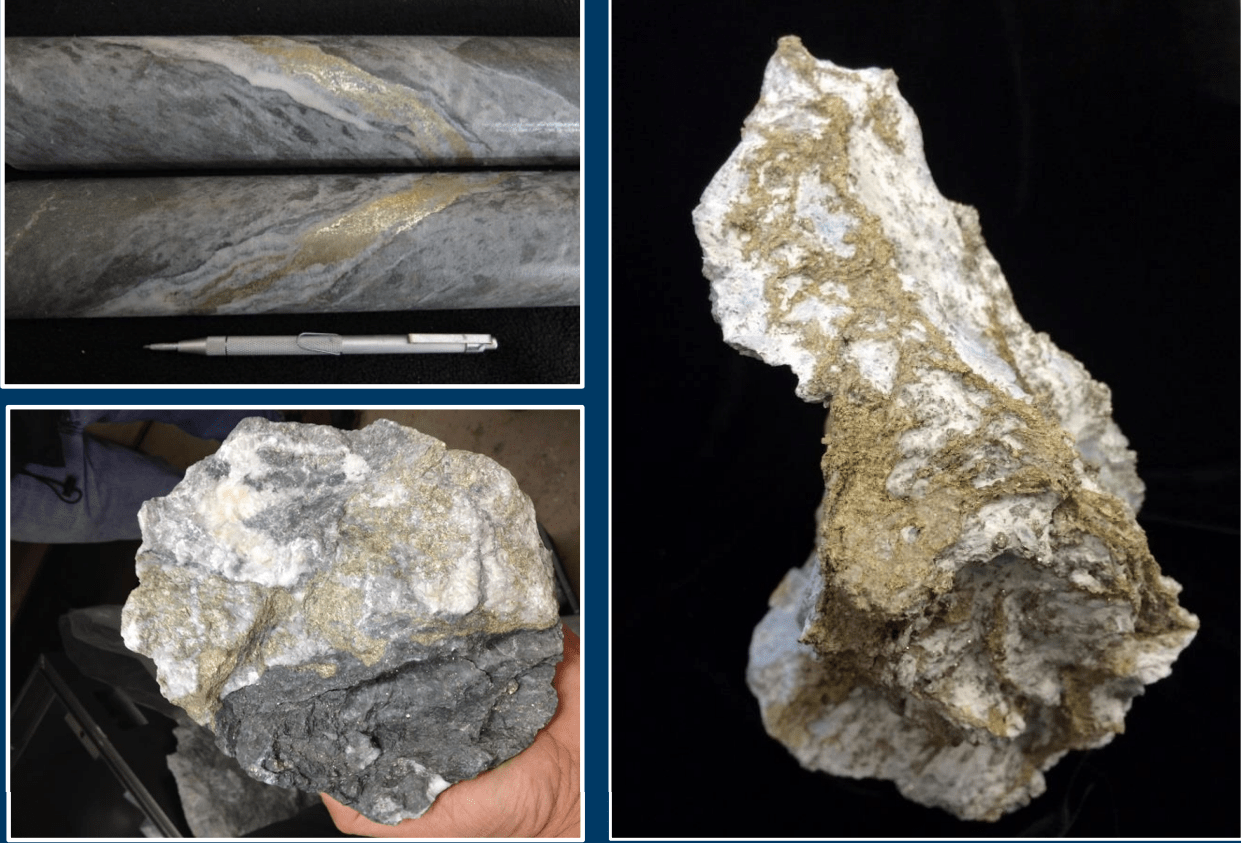

At Brucejack in British Columbia, this may be a small royalty, but under Newcrest (NCMGF), I would expect it to become a larger asset, and exploration success has continued. Newcrest shared that it has a three-phased approach to optimizing the asset, including the potential to increase throughput. Highlight holes included 25.5 meters at 52 grams per tonne gold, 28.5 meters at 35 grams per tonne gold, and 36 meters at 33 grams per tonne gold. These intercepts are in addition to the Golden Marmot regional discovery north of the Valley of the Kings Zone, where the company hit 20 meters at 187 grams per tonne gold.

This is a small royalty, so I wouldn't expect a huge increase in annual revenue given Franco Nevada's scale, even with these new zones being delineated. However, given the new discoveries, the value here is the mine life is likely to be closer to 20 years vs. the sub-10-year mine life that was expected before these new near-mine and regional discoveries, meaning that FNV can expect this asset to contribute well past 2035.

{kind=link}

Brucejack Mineralization (Newcrest Presentation)

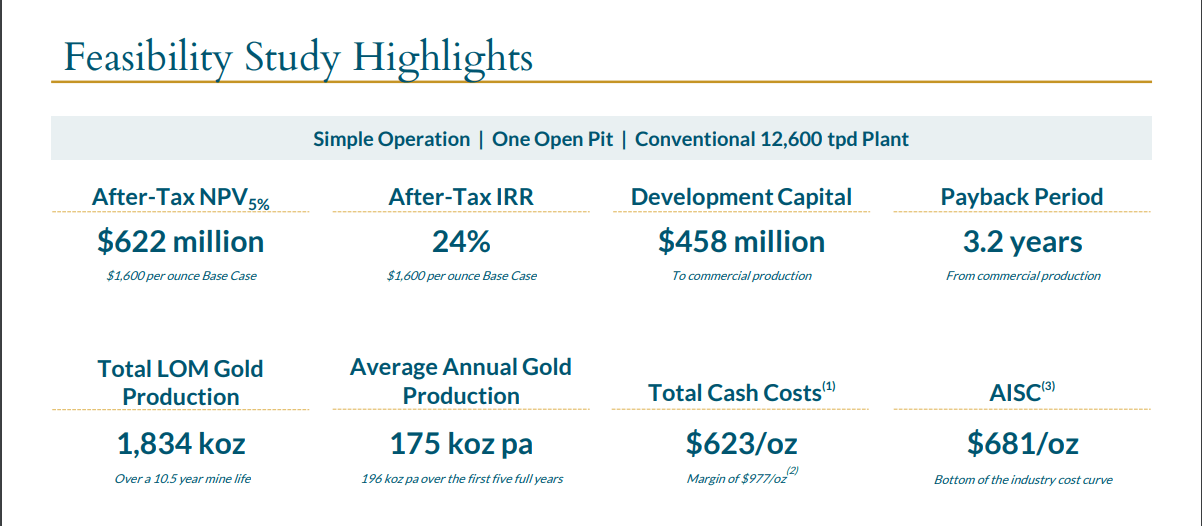

Finally, Seguela and Greenstone continue to progress towards their first gold pours in 2023 and 2024 and are on schedule and budget. Similar to Brucejack, these are not huge contributors, but they are very low-cost assets that will provide a small boost to its annual gold sales. In addition, Franco Nevada made one major deal for a 12.5% gold stream (first 300,000 ounces at 20% of spot) on the Tocantinzinho Project in Brazil, which should be a major contributor starting in 2025, contributing over 20,000 GEOs per annum for its first five years.

Notably, this project is also likely to be on schedule and under budget with the very experienced G Mining team in charge of construction, with successful builds at Merian 1 and 2 and Fruta Del Norte, also in South America.

{kind=link}

Toctantinzinho Feasibility Study Highlights (G Mining Presentation)

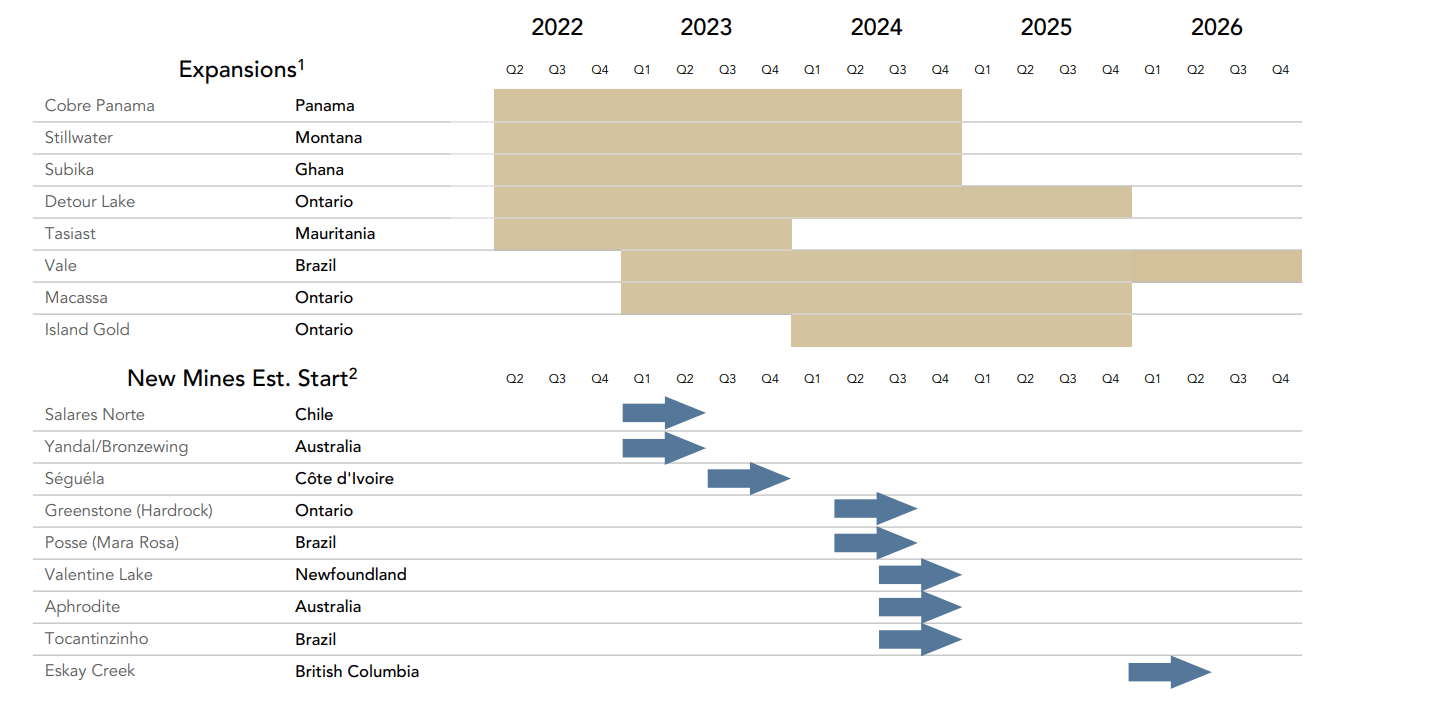

The above discussion does not do the total portfolio's organic growth profile justice, with additional contributions from Salares Norte in Chile, the possibility of contribution from Eskay Creek ( SKE ) in 2025, and growth at several already-producing assets over the next few years. Based on the current outlook, Franco Nevada expects to see total GEO sales increase to 765,000 to 825,000 ounces by FY2026, representing more than 12% growth at the mid-point vs. its FY2022 guidance. So, even if we see weaker energy and precious metals prices vs. H1 2022, Franco's growth in attributable production will pick up the slack post-2024 assuming prices remain soft.

{kind=link}

Franco Nevada Organic Growth (Company Presentation)

Earnings Trend

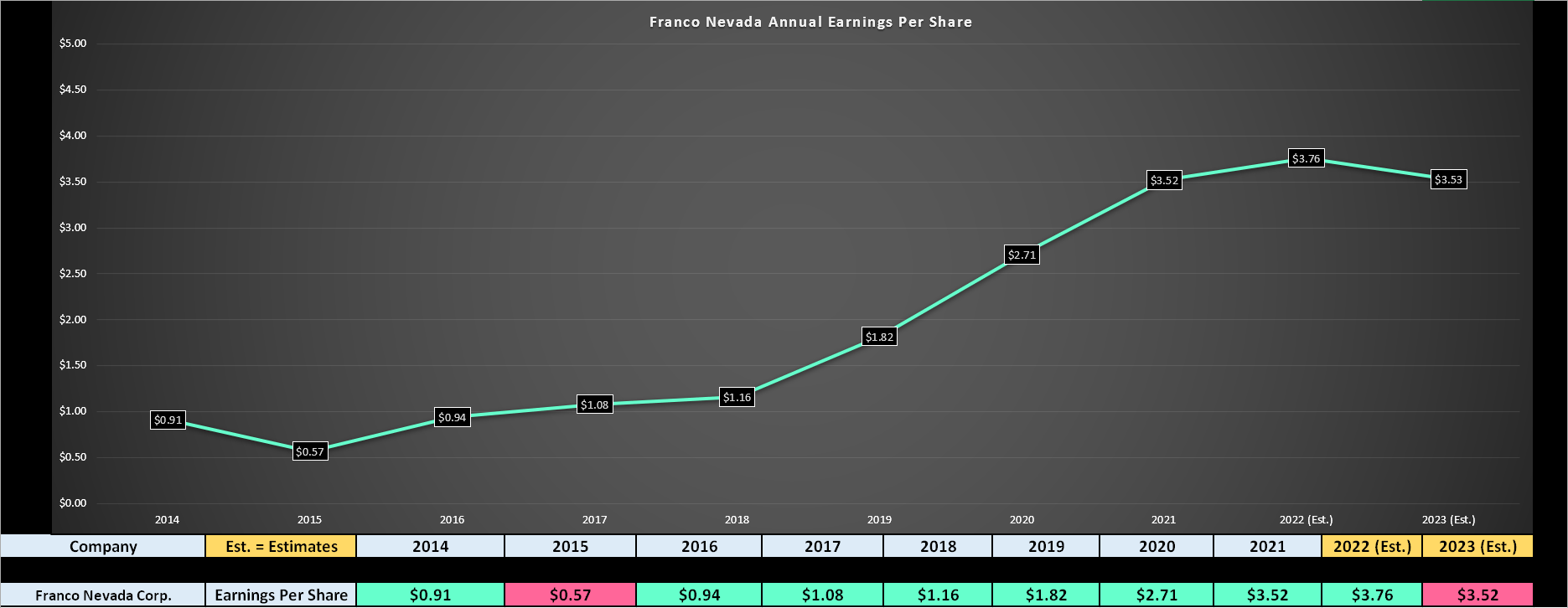

As shown in the chart below, Franco Nevada has massively outperformed its peer group from an earnings growth standpoint, growing annual earnings per share [EPS] at a CAGR of 19.4% since FY2014 (compared to FY2022 estimates). If we compare this to Newmont ( NEM ), the world's largest gold producer, this is a more than 800 basis point outperformance and with lower volatility in the same period. Based on FY2022 annual EPS estimates, Franco Nevada will see another new all-time high for annual EPS, benefiting from higher revenue in its energy business, which explains why it has outperformed its peers in the precious metals sector from a return standpoint.

{kind=link}

Franco Nevada - Annual Earnings Per Share Trend (YCharts.com, Author's Chart & Estimates)

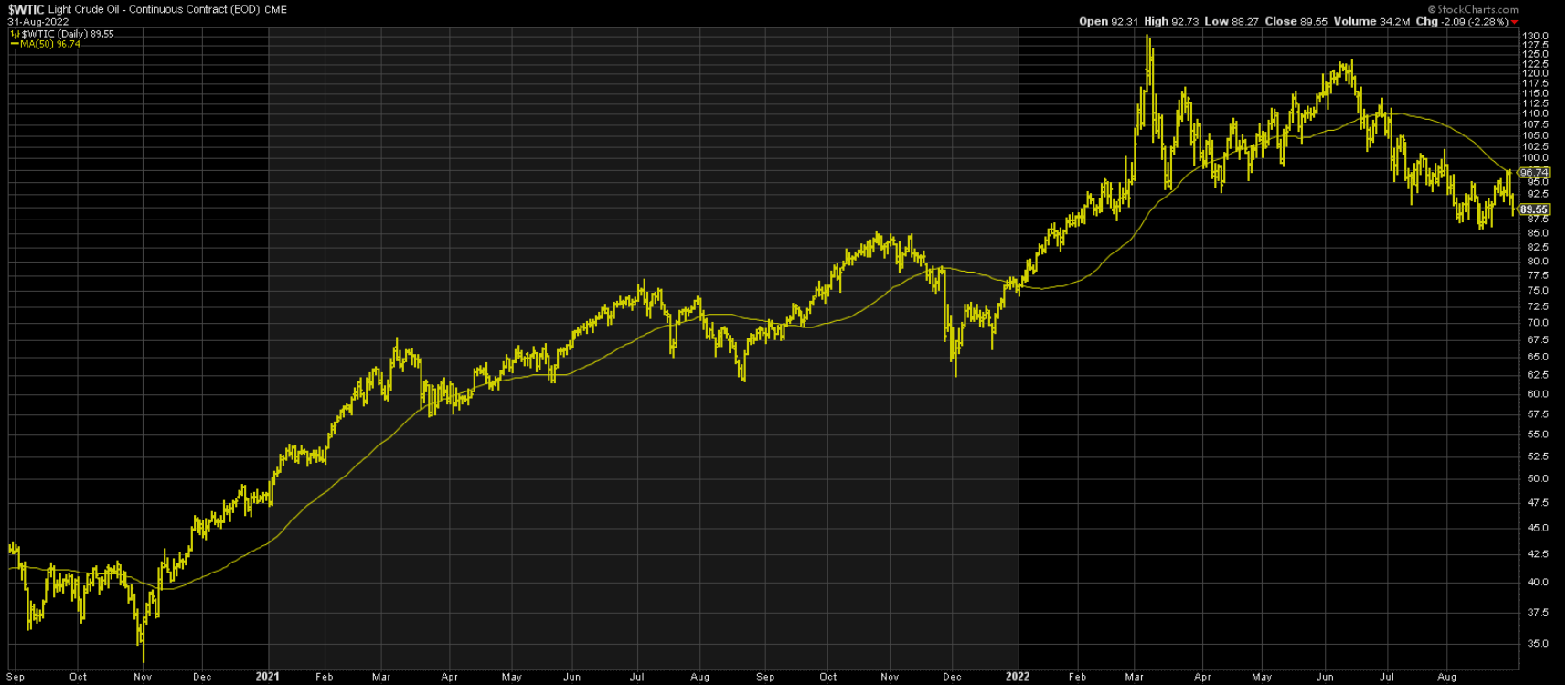

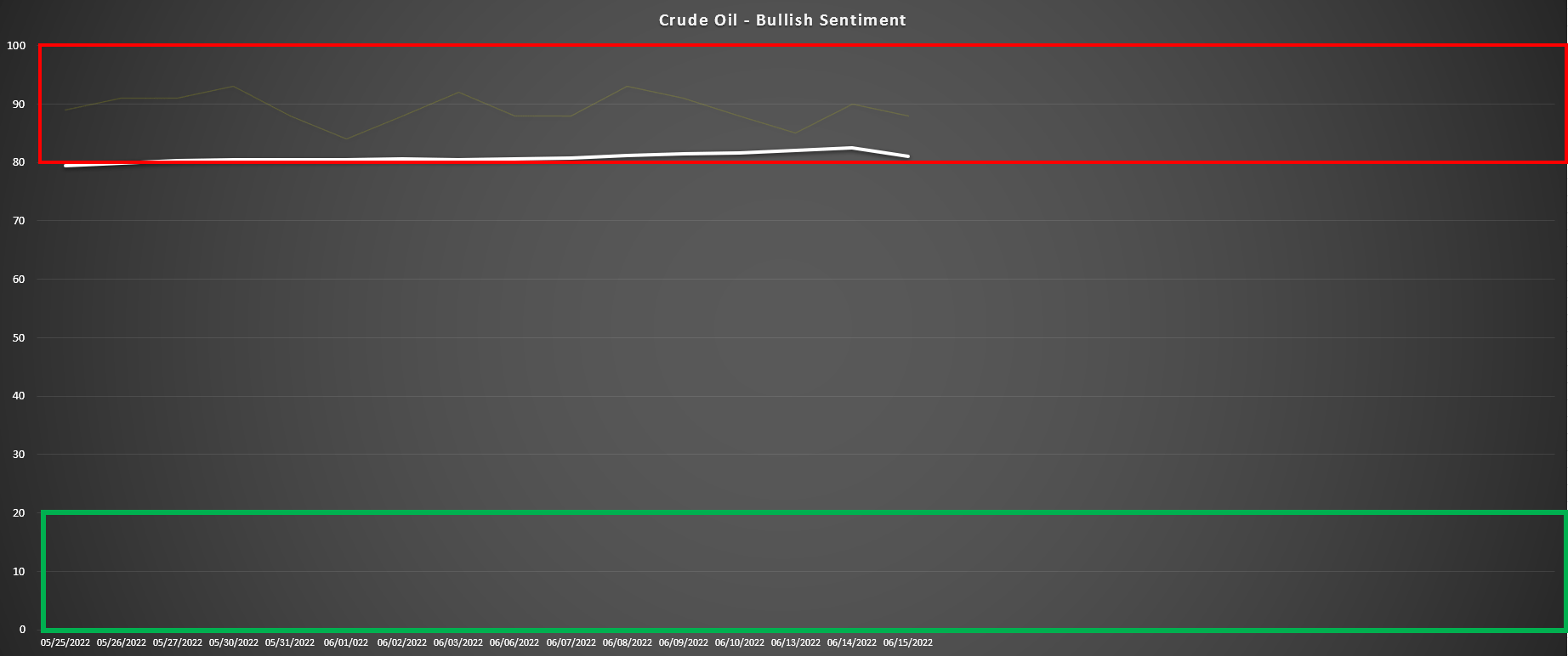

However, as I pointed out in my most recent article, the strong energy prices in H1 2022 had created difficult year-over-year comps for Franco Nevada, and I was less optimistic that it would be able to lap these comps without help from precious metals. This was reinforced by the fact that sentiment for crude oil was at its highest levels in years, and this typically has marked 1-year and sometimes multi-year tops for commodities, suggesting the $125.00/barrel mark was likely the peak. Unfortunately, instead of precious metals strengthening to pick up any slack, they continue to weaken, creating difficult comps in both areas of its business if they don't recover.

{kind=link}

Crude Oil Futures Price (StockCharts.com)

{kind=link}

Crude Oil - Bullish Sentiment - June 2022 (Daily Sentiment Index Data, Author's Chart)

Given this outlook and without the benefit of significant GEO growth like some of its small-cap peers, FY2022 may mark a short-term peak for earnings at $3.76, with the potential for a dip to $3.53 or lower in FY2023. Often, when earnings peak after an extended uptrend, we can see margin compression, and this is similar to what we've seen in many retail stocks this year after a year of tailwinds due to wardrobe refreshes (pent-up demand) and the benefit of government stimulus in 2021. Based on the potential for a mid-single-digit earnings decline next year and the possibility that we've temporarily seen peak earnings, it's harder to justify FNV's premium multiple. Let's take a closer look below.

Valuation

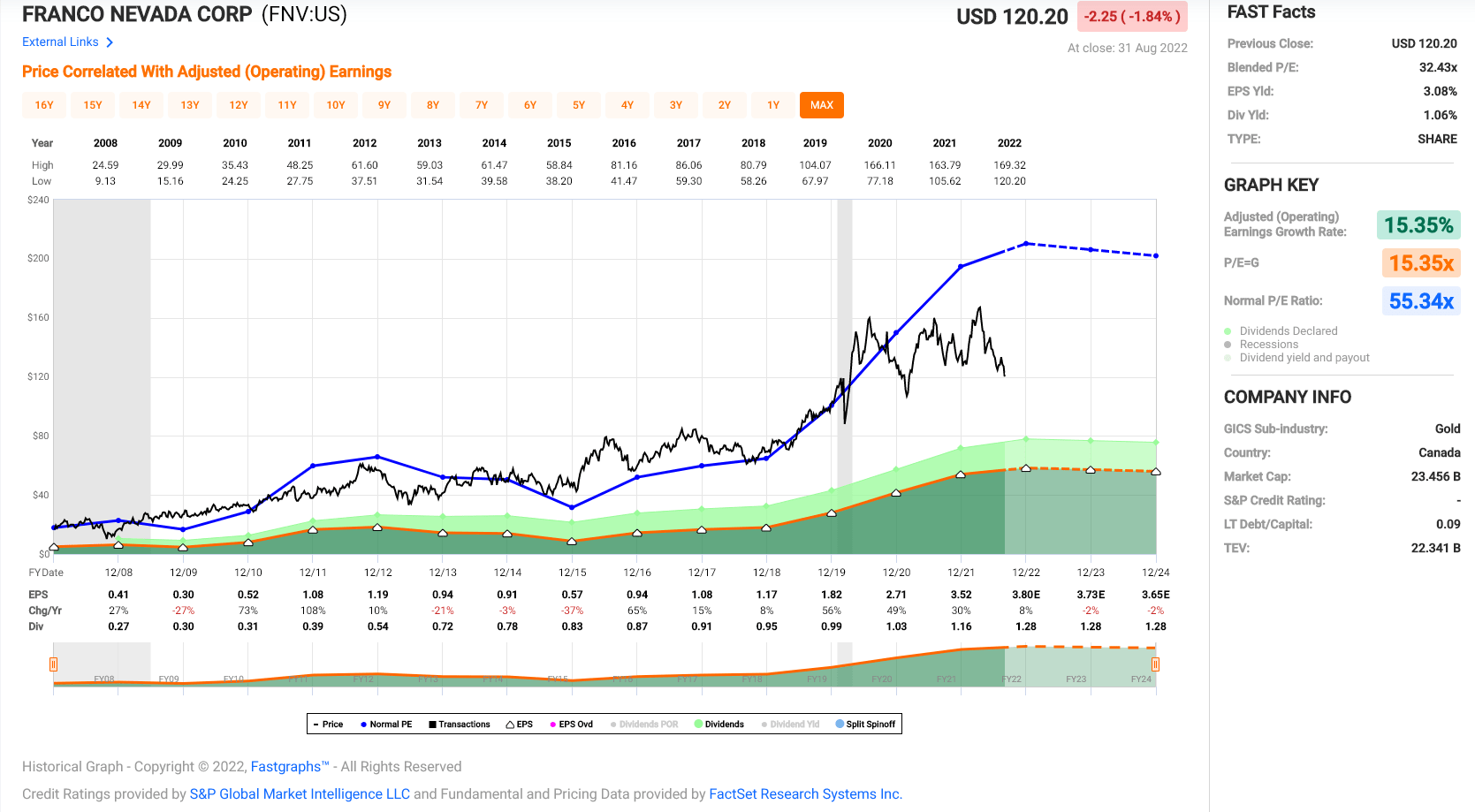

Based on ~192 million shares and a share price of $120.20, Franco-Nevada trades at a market cap of ~$23.1 billion, making it one of the largest precious metals companies by market cap. The stock has historically traded at 55x earnings and a massive premium to its peer group due to its low-risk business model. In a time of rising costs, this premium for an inflation-resistant business makes sense. However, I believe a more conservative earnings multiple for the stock is 44, given that it's harder for FNV to grow relative to other royalty/streaming peers due to its size. Based on FY2023 earnings estimates of $3.53, this translates to a fair value of $155.30.

{kind=link}

Franco Nevada - Historical Earnings Multiple (FASTGraphs.com)

While a fair value of $155.30 points to a 29% upside to FNV's fair value, I prefer to buy at a minimum 25% discount to fair value when it comes to large-caps, and a 30% discount to fair value is likely a safer margin of safety if there's a risk that earnings have peaked short-term. After applying a 30% discount to fair value ($155.30), FNV's low-risk buy zone would come in at $108.70, nearly 10% below current levels. So, while this pullback has certainly improved the valuation, I don't see FNV as anywhere near a screaming buy like some other names in the sector currently, where I would consider discounting the technical picture and buying on valuation. On that topic, let's look at the technical picture below:

{kind=link}

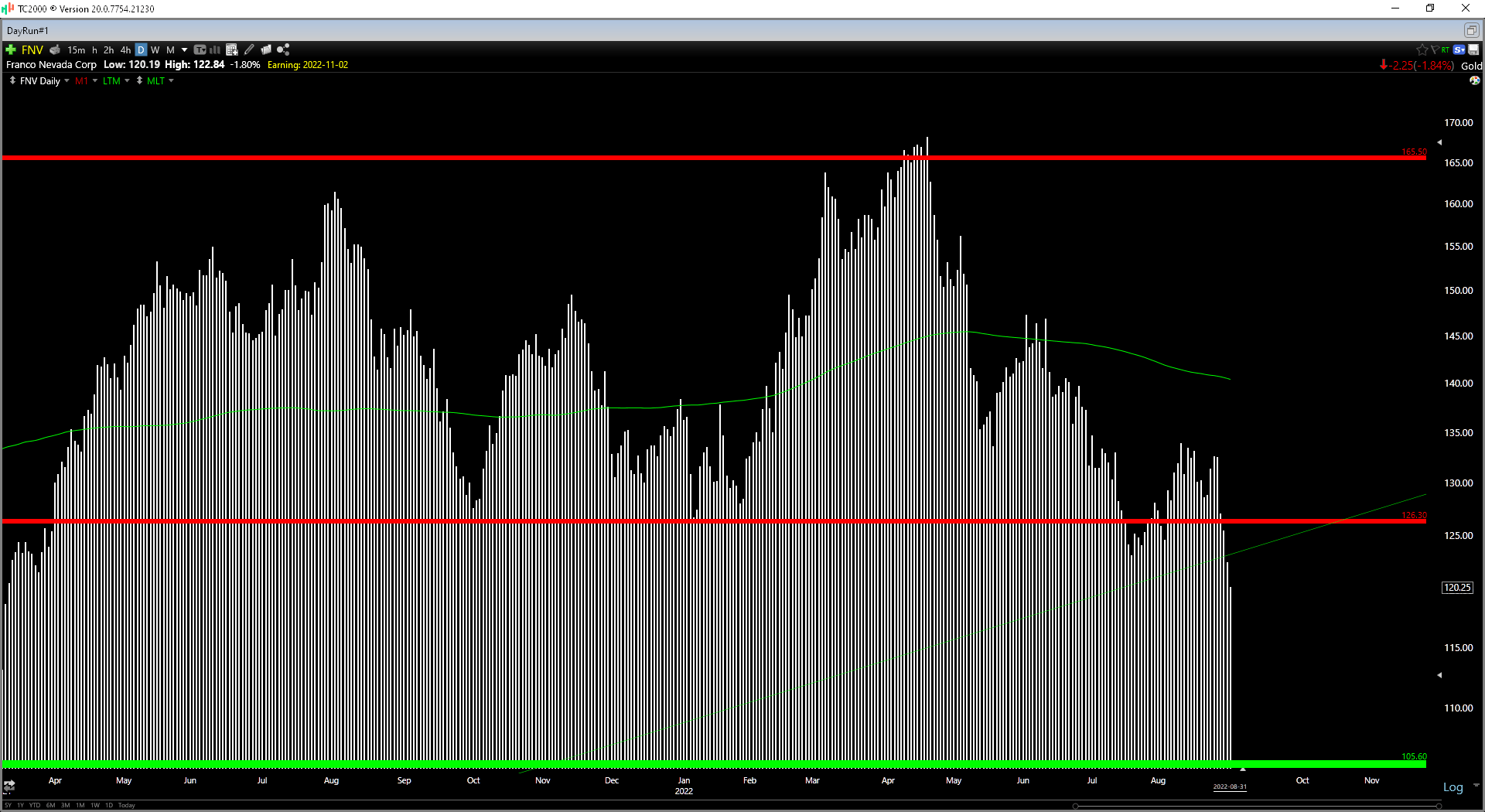

FNV Daily Chart (TC2000.com)

In my previous update, I noted that FNV would enter a low-risk buy zone at $130.00, and while the stock did rally from this level, it put together a very feeble rally and higher low, failing to reclaim its moving average. Since then, the stock has broken down below critical support at $126.00 and has continued to make lower highs and lower lows since its Q1 2021 peak. This is a negative development, and we now have a new resistance level at $126.00, given that critical support levels, when broken, often become resistance. The reason is that traders that accumulated at this support level can become anxious to exit at break-even on any bounces after suffering through a draw-down.

This negative development from a technical standpoint doesn't mean that the stock must head lower, but it does point to a less attractive reward/risk profile than was present in June. In fact, at a share price of $120.20, FNV's reward/risk from support to resistance comes in at just 0.41 to 1.0, well below the 5 to 1 reward/risk ratio that I prefer to wait for before entering new positions. So, with FNV trading at a huge premium to its peer group even after its recent decline (1.9x P/NAV) and ~34x FY2023 earnings estimates, it's tough to argue for rushing into the stock here. Instead, the low-risk buy zone has been revised to $108.70 or lower, which would place FNV within 3% of its next support level ($105.60).

Summary

Franco Nevada has been a massive beneficiary of higher energy prices. This is one reason it's been able to continue posting record annual EPS vs. other precious metals names, with this side of its business offsetting lower realized gold/silver prices. However, with oil prices looking like they plateaued in March, this has set up difficult comps in 2022, and stocks often overshoot to the downside in these periods, similar to what we've seen in silver producers in 2022 (lapping benefits from the silver squeeze).

The good news is that FNV has arguably the best portfolio in the sector and has seen multiple positive developments which will boost revenue long-term. However, while several new assets will boost production over the next several years, GEO production should only be up 4% or less vs. FY2020 levels next year. This makes it harder for FNV to lap difficult comps than peers with higher attributable growth rates, putting pressure on earnings short-term. Hence, I think it makes sense to be patient before rushing into FNV and focus on more attractively priced names elsewhere in the sector, where a larger margin of safety is present.

For further details see:

Franco-Nevada: Another Record Quarter