FNV:CC - Franco-Nevada Corporation: A Solid Q4 But Tough Comps Ahead

2023-03-19 05:08:07 ET

Summary

- Franco-Nevada was one of the better-performing gold miners last year, losing just 1% of its value vs. an 11% decline in the Gold Miners Index.

- I attribute the outperformance to the company's inflation-resistant business model and strength in energy prices, which helped it post record revenue and operating cash flow last year.

- However, the company is now lapping tough comps from H1-2022 with several commodities trading at lower prices, suggesting the potential for weaker Q1-23/Q2-23 results on a year-over-year basis.

- So, while I see Franco-Nevada as the premier way to get exposure to the gold price, I don't see enough margin of safety, and I continue to see patience as the best course of action.

Just over three months ago, I wrote on Franco-Nevada Corporation ( FNV ), noting that while the company continued to report record results, it would be up against difficult comps in H1-23 that could weigh on share price performance. This was because it was benefiting from multi-year highs for oil ( USO ) and palladium ( PALL ) in H1-2022, and these trends had since reversed. Not only that, there was likely to be further downside likely ahead for both commodities, given that there was still no sign of capitulation in oil or palladium as of Q4. Since then, natural gas prices ( UNG ) have also declined violently, leading to weaker pricing in additional segments of Franco-Nevada's business. So, while the recent strength in the gold price is a positive, softness in other segments will partially offset this benefit.

The good news is that Franco-Nevada's portfolio continues to be rock-solid. And uncertainty related to Cobre Panama has subsided after a brief scare. Finally, we've seen multiple positive developments across its portfolio and several assets are inching closer to first production (Tocantinzinho, Seguela, Magino, Salares Norte, Greenstone, Posse) while other assets are positioned to deliver meaningful organic growth (Macassa, Detour Lake, Tasiast, Cobre Panama). Although these developments improve the investment thesis, I expect weaker Q1/Q2 results as Franco-Nevada laps strong pricing for all commodities in the year-ago period, suggesting investors should see an opportunity to enter the stock at lower prices if they're patient.

Detour Lake Mine - (Franco Nevada 2% NSR) (Agnico Eagle Website)

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Q4 & FY2022 Results

Franco-Nevada released its Q4 and FY2022 results last week, reporting quarterly attributable sales of ~183,900 gold-equivalent ounces [GEOs], a 1% increase from the year-ago period. Strong quarters from Marigold, Sudbury, Hemlo, and Tasiast (albeit very easy year-over-year comps) aided with the solid finish to 2022, but the most significant contribution was from its energy portfolio which benefited from higher average realized prices on a year-over-year basis. On a full-year basis, Franco-Nevada delivered into the high end of its FY2022 GEO guidance, reporting sales of ~730,000 GEOs, a marginal increase year-over-year and above its guidance mid-point of 710,000 GEOs. However, its precious metals portfolio wasn't to thank, with lower contribution from several assets.

Franco-Nevada Corporation - Quarterly GEO Sales (Company Filings, Author's Chart)

{kind=link}

Digging into the precious metals portfolio a little closer, revenue from precious metals dipped to 70.7% in Q4 2022 (Q4 2021: 76.1%), and we saw lower contributions from Antapaccay (lower grades), Cobre Panama (shipment timing), Guadalupe-Palmarejo (less production attributable to royalty ground), Karma (security issues that resulted in suspension since Q2 2022), Brucejack (suspension related to work related fatality), and Goldstrike. The impact to revenue and cash flow was exacerbated by lower average realized gold and silver prices in the period, which slid to $1,729/oz (Q4 2021: $1,795/oz) and $21.20/oz (Q4 2021: $23.32/oz), respectively. While we won't see a material improvement in attributable GEO sales this year from its precious metals segment, several assets are in the wings and slated for commercial production by year-end 2024, and are as follows:

- Seguela (Cote d'Ivoire)

- Greenstone (Ontario, Canada)

- Magino (Ontario, Canada)

- Salares Norte (Chile)

- Posse (Brazil)

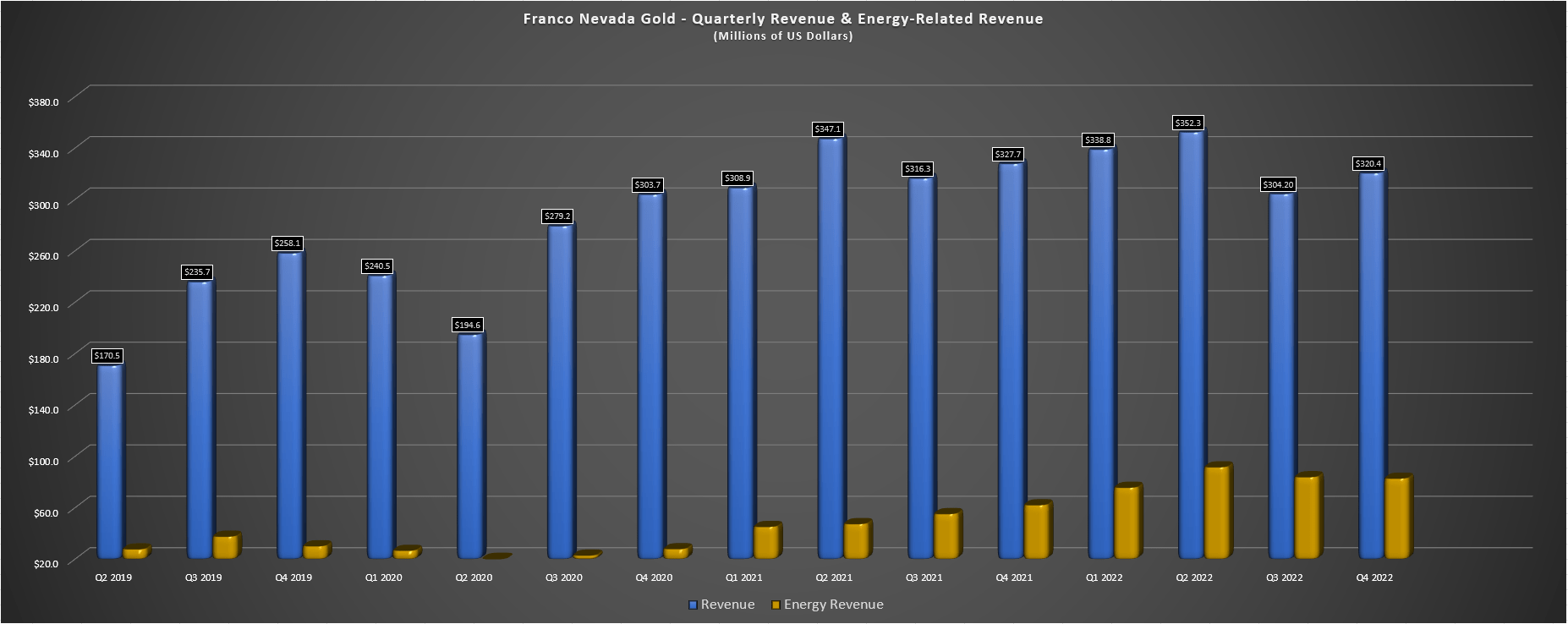

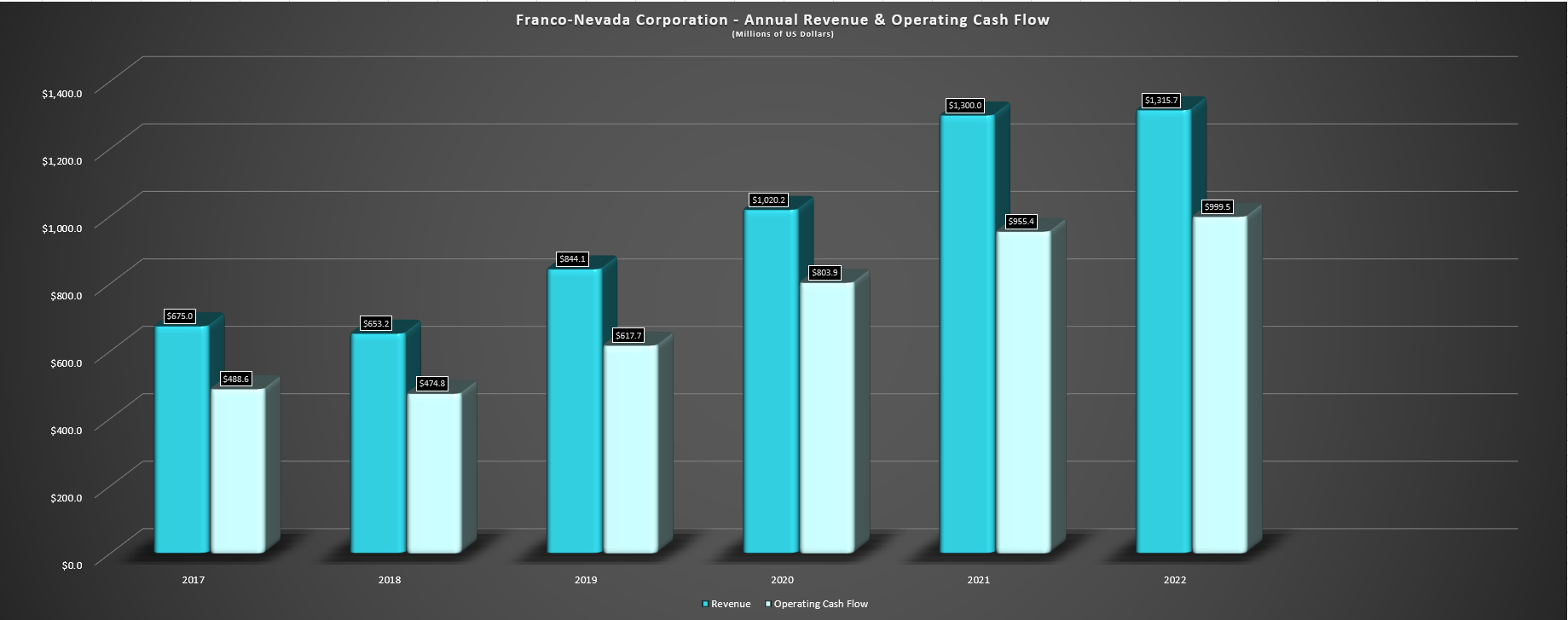

Fortunately, although its precious metals and iron ore segments saw lower revenue on a year-over-year basis in FY2022 (impacted by lower contributions and or lower prices), its energy segment picked up the slack in a big way. This was evidenced by revenue from its oil segment of $156.0 million (44% growth year-over-year), and its natural gas/natural gas liquids segment of $177.6 million (75% growth year-over-year). This was driven by significantly higher prices for WTI ($94.23/barrel vs. $67.91/barrel) and Henry Hub ($6.51/mcf vs. $3.72/mcf) and increased production from its SCOOP/STACK, Permian, and Weyburn royalty assets. The result was that annual revenue hit a record high of ~$1.32 billion despite a mediocre year from its precious metals segment, while operating cash flow hit a new record of ~$1.0 billion.

Franco-Nevada - Quarterly Revenue & Energy Related Revenue (Company Filings, Author's Chart) Franco-Nevada Corporation - Annual Revenue & Operating Cash Flow (Company Filings, Author's Chart)

{kind=link}

{kind=link}

Perhaps the most impressive statistic when viewing the above chart of annual revenue and operating cash flow is that Franco-Nevada has accomplished this 104% growth in operating cash flow despite less than a 4% increase in its share count in the same period. This highlights the beauty of the royalty/business model when it gets to this scale, with Franco-Nevada able to do all of its transactions with a mix of cash flow and debt while many smaller names like Metalla ( MTA ) and Gold Royalty Corporation ( GROY ) that continue to dilute shareholders to add new royalties. In fact, Franco-Nevada put significant capital to work last year and added the following among significant assets:

- 2.0% NSR on the Magino Project ($52.5 million)

- 0.50% NSR on Eskay Creek ($21.0 million) - total NSR now 1.5%

- 0.46% NSR on Caserones ($37.4 million)

- 2.0% NSR on Pacific Clay claims at Castle Mountain ($6.0 million) - total NSR now 4.65%

- 2.0% NSR on Spences Bridge Gold Belt claims ($6.0 million)

- 12.5% gold stream, which declines to 7.5% after 300,000 ounces of gold delivered ($250 million)

To summarize, Franco-Nevada had a solid year overall with record revenue and operating cash flow despite a weaker year for its precious metals segment due to lower production at key assets and lower silver prices. From a big picture standpoint, Franco-Nevada has augmented its long-term growth profile with new royalty/streaming additions, and some of these new additions could begin contributing meaningfully by as early as Q3 of this year (Magino, Seguela). Assuming its bets on Eskay Creek pay off, this could also be a very solid contributor long-term with this having the potential to be a ~400,000 GEO per annum asset in its first few years and potentially maintaining a 320,000 ounce per annum production profile past the first 10 years given recent exploration success.

Finally, while there was uncertainty around Cobre Panama which contributed 17% of Franco-Nevada's annual revenue in FY2022 (with increased contribution as it heads towards a 100 million tonne per annum throughput rate), this has since been resolved. As reported by First Quantum ( FQVLF ), a new Proposed Concession Contract is in place (20-year term) as of March 8th, and processing operations have resumed following a brief suspension of operations on February 23rd. This is certainly a very positive development for Franco-Nevada given that while it would still maintain a strong cash flow profile with Cobre Panama suspended, this is the company's largest single contributor and losing it in a lengthy dispute would put a severe dent in annual cash flow and earnings per share. Let's look at the 2023 outlook:

2023 Outlook

Looking ahead to FY2023, Franco-Nevada has guided for annual GEO sales of 670,000 at the mid-point (FY2022: ~730,000 GEOs), with the high end of guidance implying a 4% decline in annual GEO sales. There are three reasons for this sharp decline that are unfortunate. For starters, the delayed first gold pour at Salares Norte (the asset could produce as little as 20,000 ounces this year) will impact 2023 attributable GEO sales. Second, Franco-Nevada has chosen to be conservative on Cobre-Panama in 2023 due to the temporary restriction of concentrate shipments which could result in lower attributable GEO sales vs. GEO production for Franco-Nevada this year. On the positive side, the ramp up to 100 million tonnes per annum is on track for year-end (exit rate), pushing copper production at the asset to north of 400,000 tonnes per annum.

Cobre Panama Operations (First Quantum Presentation)

{kind=link}

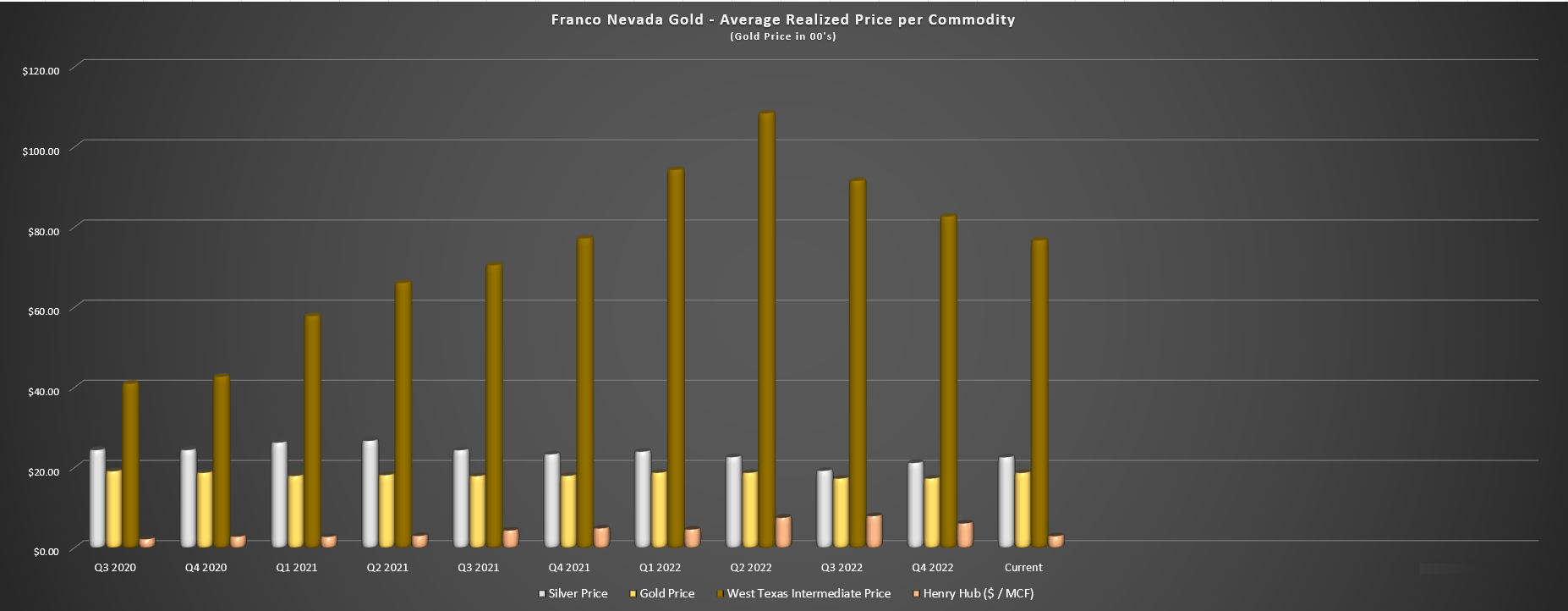

Finally, and perhaps the hardest to predict, Franco-Nevada has assumed lower energy prices this year and much lower palladium prices, impacting its GEO production from its non-gold/silver segment. The guidance assumes an average price of $80.00/barrel for WTI oil, $3.00/mcf for Henry Hub natural gas, and $1,500/oz for palladium, all well below FY2022 prices of $94.23/barrel, $6.51/mcf, and $2,107/oz, respectively. Depending on if prices are able to recover, these estimates might actually end up not being conservative enough, with palladium futures currently sitting more than 30% below guidance levels at $1,415/oz.

Franco-Nevada - Average Realized Price Per Commodity (Company Filings, Author's Chart)

{kind=link}

Given the lower contributions this year from assets like Antamina (lower grades), Hemlo (less production from royalty covered ground), and Candelaria plus what's likely to be lower energy prices year-over-year, Franco-Nevada is up against tough comps and is likely to see lower cash flow per share and annual EPS in FY2023. Based on current estimates, FY2023 annual EPS is expected to decline over 5% to $3.40 per share (FY2022: $3.64 per share) and while the recent strength in the gold price could help to buffer this decline, I don't see it making up for the shortfall in energy prices. This is especially true when it comes to Q1 and Q2 2023 when the company was already enjoying strong metals prices.

As shown above, average quarter-to-date metals prices of $22.60/oz, $1,869/oz, $76.70/barrel, and $2.90/mcf compare (silver, gold, oil, natural gas) compare unfavorably to Q1 2022 prices of $24.00/oz, $1,874/oz, $94.29/barrel, and $4.57/mcf, respectively. These comps don't get much easier in Q2 2022, with realized prices of $22.64/oz, $1,872/oz, $108.41/barrel, and $7.49/mcf, respectively, and that ignores lower commodity prices in smaller segments like palladium/iron ore. So, while Franco-Nevada had a solid Q4/FY2022 report, it's now up against tough comps and could have two weak reports on deck, potentially leading to some softness in the stock.

Condestable Operations (Company Website)

{kind=link}

It's important to note that this is a 2023 issue and we should see an increase in precious metals production in 2024 with multiple new mines coming online (Tocantinzinho, Greenstone, Seguela, Salares Norte, Posse). That said, the increases in production from these assets will be partially offset by the cap being hit at Harmony's ( HMY ) Mine Waste Solutions (312,500 ounce cap on production per the 2022 amendment agreement, with ~265,000 ounces delivered to date). This will be a pretty heavy blow for Franco-Nevada given that it's enjoying its 25% gold stream which represents nearly ~25,000 ounces per annum with a very attractive cost of just ~$460/oz.

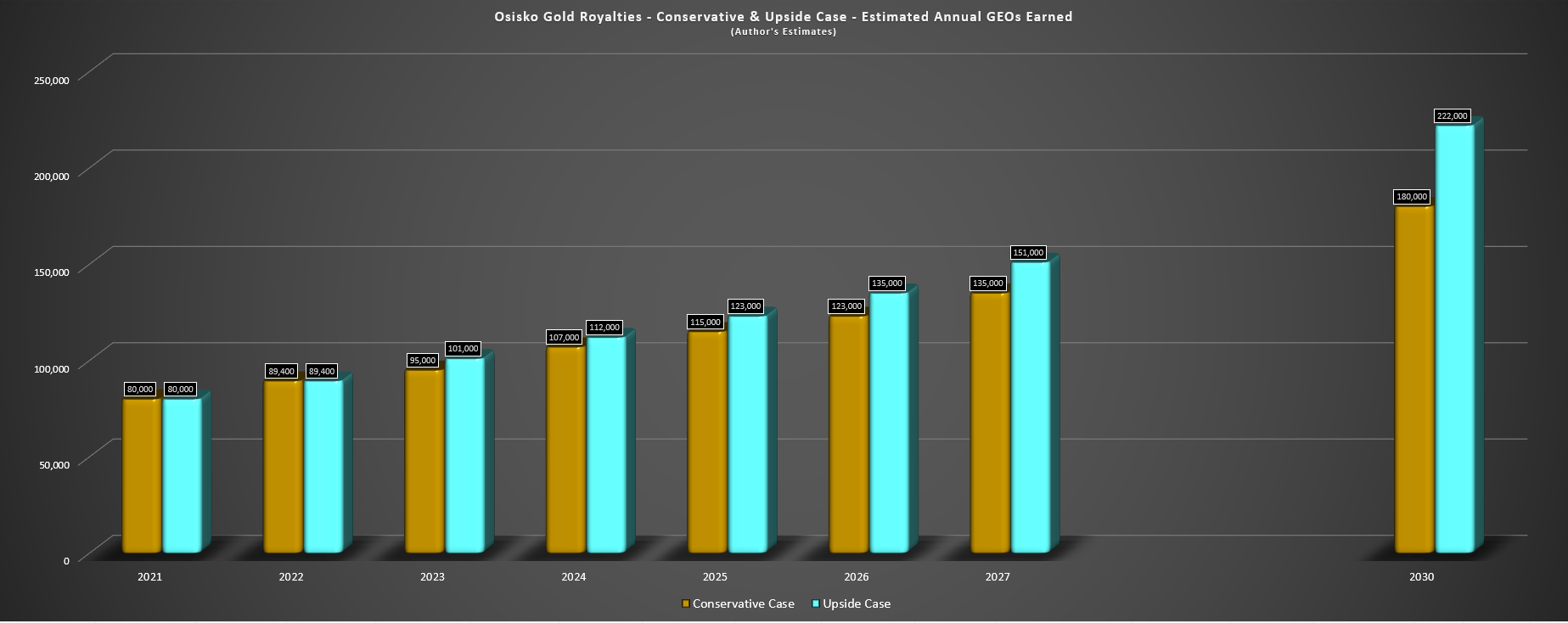

Longer-term, and despite the impact of the MWS cap and Candelaria (40% vs. 68% after 720,000 ounces of gold and 12.0 million ounces of silver delivered), Franco-Nevada expects to see annual GEO sales increase to 760,000 to 820,000 GEOs, pointing to ~12% growth vs. FY2022 levels at the top end of guidance. I would argue that this figure is conservative given that I would expect Franco-Nevada to continue to deploy at least $500 million each year into producing and development stage royalties. Still, this growth profile leaves a lot to be desired in the base when compared to names like Osisko Gold Royalties ( OR ) that could double attributable production from FY2022 levels by 2030. Hence, from a growth and value standpoint, I see Osisko Gold Royalties as the more attractive buy-the-dip candidate of the two companies.

Osisko Gold Royalties - Conservative Case & Upside Case - Estimated Annual GEOs Earned (Company Filings, Author's Chart & Estimates)

{kind=link}

Let's look at Franco-Nevada's valuation and see whether the tough comps ahead and weaker year are priced into the stock:

Valuation & Technical Picture

Based on ~192 million shares and a share price of $145.00, Franco-Nevada trades at a market cap of ~$27.8 billion, giving it one of the richest valuations sector-wide, with some premium being justified given its high-margin business with considerable diversification (113 producing assets). However, as I've noted in past articles, although this diversification and inflation-resistant business model is highly attractive and the premier way to get exposure to precious metals prices, valuation matters. In fact, Joel Greenblatt goes as far as saying that "there is no investing without valuation" and I couldn't agree more with this statement, especially when it pertains to names in a cyclical sector where downside volatility in commodity prices can make pinning down fair value more difficult.

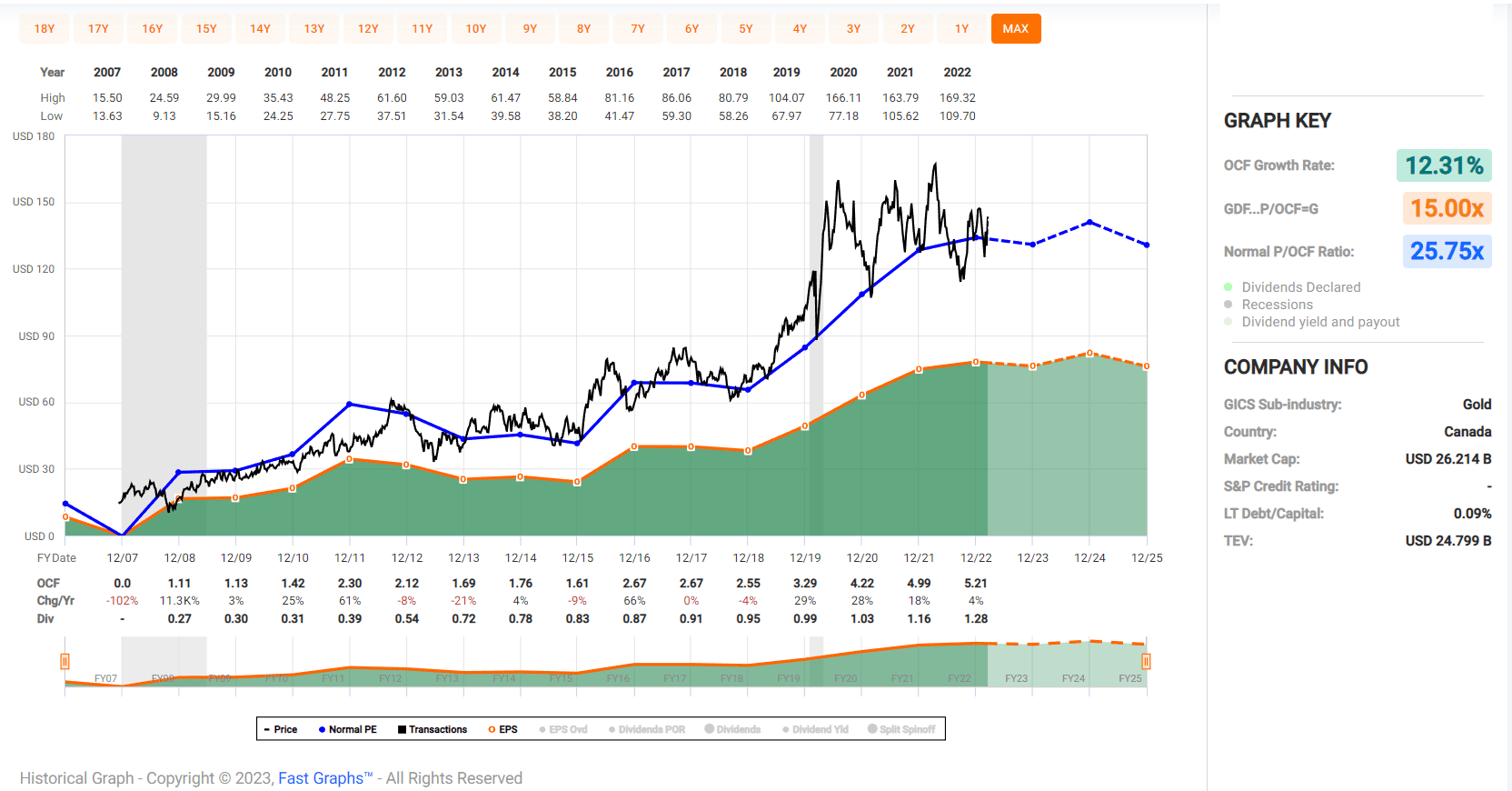

Franco-Nevada - Historical Cash Flow Multiple (FASTGraphs.com)

{kind=link}

In Franco-Nevada's case, we can see that the stock has historically traded at ~25.8x cash flow (~28.4x for its 10-year average), a very rich multiple when we consider that the best gold miners have historically traded at multiples below 12.0x cash flow. And even if we can agree that a ~150% premium from a cash flow multiple standpoint relative to the top-3 gold producers is justified, Franco-Nevada remains expensive relative to where it's traded historically. The evidence lies in the stock trading at ~28.8x forward earnings estimates ($5.04), a slight premium to its 10-year average multiple on a trailing-twelve-month basis. Perhaps a cash flow multiple of 30.0 is a more fair multiple given the increased diversity and optionality (113 producing/419 total assets vs. 107/339 in 2017). However, even at this multiple, fair value for the stock would come in $151.20 per share.

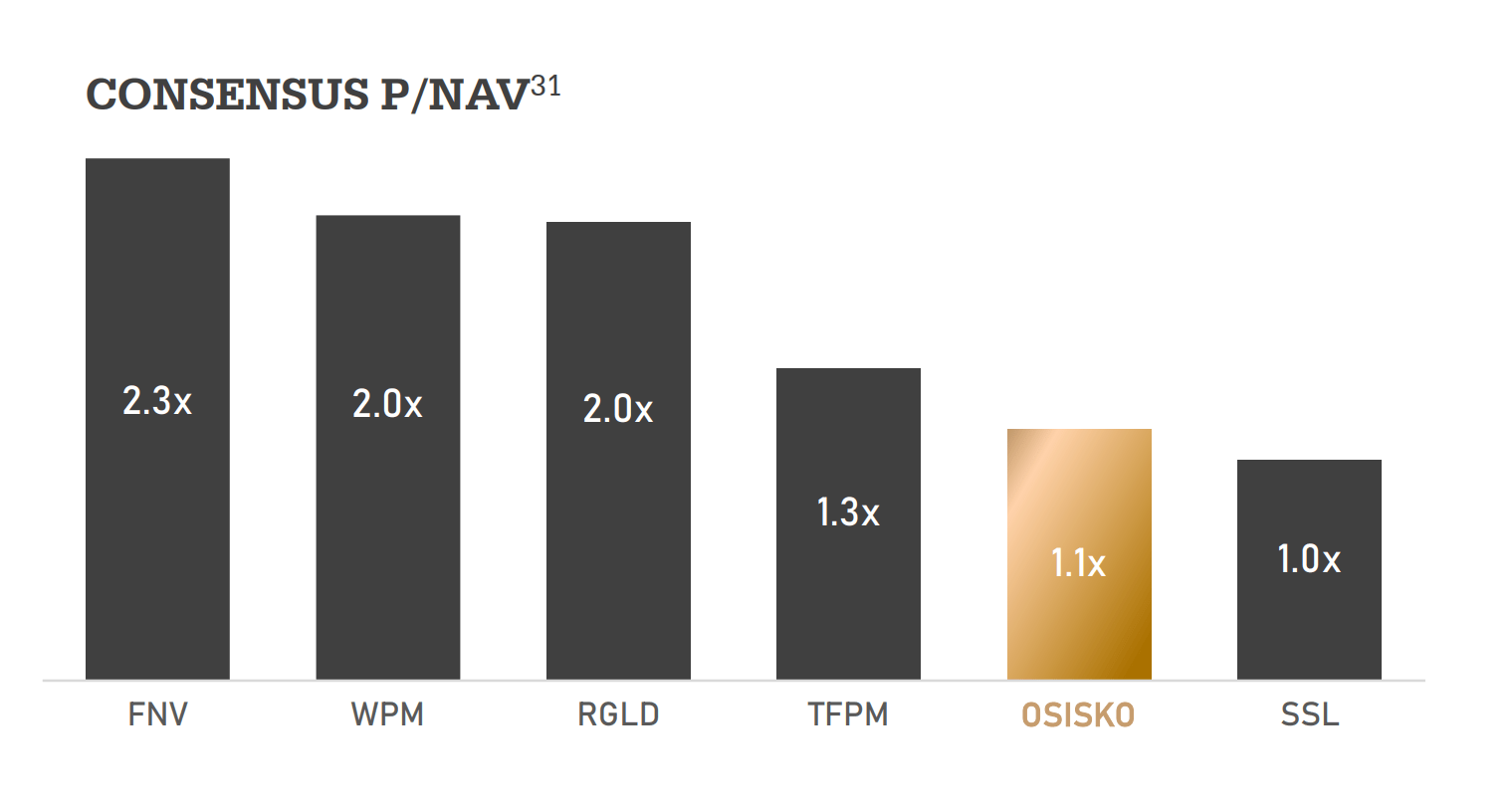

I have compared to its portfolio to 2017 given that this is the midpoint of the 10-year average period when assessing where it has historically traded (2012-2022) from a cash flow multiple standpoint. Franco Nevada's relative valuation isn't any more attractive from a P/NAV standpoint either, with it trading at a massive premium to its peer group at ~2.40x P/NAV and in the upper portion of its historical range (1.20x P/NAV to 3.20x P/NAV).

Royalty/Streaming Sector - P/NAV Multiples (Osisko GR Presentation)

{kind=link}

Although this fair value estimate points to 5% upside from current levels or a 6% total return when including its dividend for arguably the safest name sector-wide, I require a minimum 25% discount to fair value to justify starting new positions in large-cap cyclical stocks, and ideally closer to 30%. Even applying the low end of this required margin of safety to Franco-Nevada's fair value estimate, Franco-Nevada's ideal buy zone would come in at $113.40 or lower, meaning it would need to decline much further to become attractive from a valuation standpoint. Obviously, there's no guarantee that the stock pulls back by this magnitude, but with over 100 stocks in the sector and over 7,000 stocks trading on the US Market, I've never found value in chasing any stock since there are always other opportunities out there if one is patient.

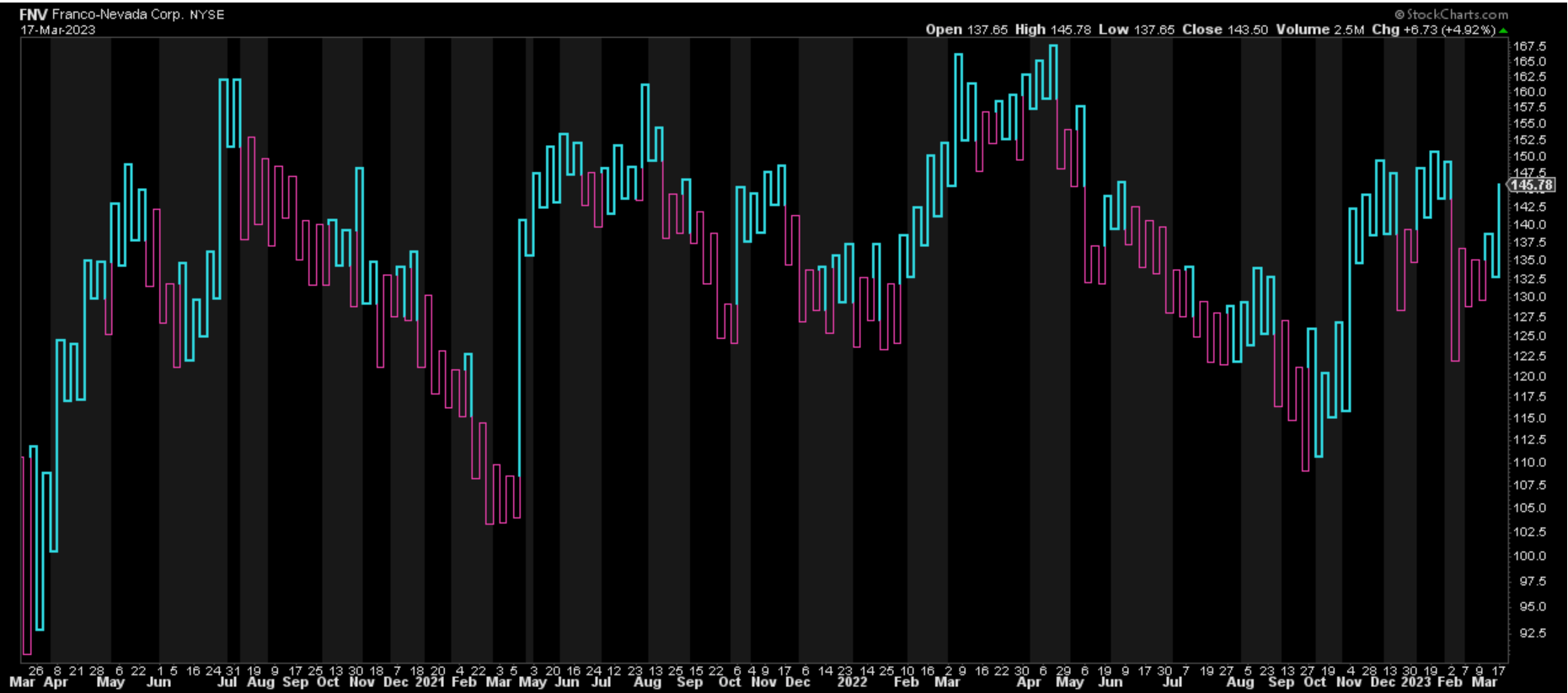

FNV - 3-Year Chart (StockCharts.com)

{kind=link}

Finally, if we look at the technical picture, Franco-Nevada is sitting in the upper portion of its 3-year range and just shy of resistance at $147.30, with no major support until $113.00. This translates to a reward/risk ratio from a technical standpoint of 0.07 to 1.0, with $2.30 in potential upside to resistance and $35.00 in potential downside to support. Given that neither the technical nor fundamental setup highlights Franco-Nevada being in a low-risk buy zone, I don't see any way to justify chasing the stock here above US$145.00.

Summary

One would be hard-pressed to find a safer way to get exposure to the precious metals space than Franco-Nevada and while several up and comers like Osisko Gold Royalties have very impressive portfolios concentrated in lower-risk jurisdictions, they lack the diversification and considerable free cash flow generation to deploy towards new royalty/streaming assets that Franco-Nevada offers to investors. That said, I prefer to buy when a sector is hated which typically means that constituents within the sector are trading at dirt-cheap valuations, and the most recent great example of that was when gold was hanging out below $1,700/oz, and the Gold Miners Index ( GDX ) was making new lows with even seasoned and loyal gold investors puking up positions.

Today, we don't have a remotely similar setup, so I see patience as the best course of action. That said, if FNV were to decline below US$114.00, I would strongly consider adding the stock back to my portfolio, given that it's arguably the best risk-adjusted way to get exposure to the sector, assuming one pays the right price.

For further details see:

Franco-Nevada Corporation: A Solid Q4, But Tough Comps Ahead