FNV - Franco-Nevada: Crisis Begets Opportunity

2024-01-02 02:44:15 ET

Summary

- Franco-Nevada has lost about one-quarter of its M&I royalty ounces following the closure of its Cobre Panama mine.

- The current share price is pricing in a total loss of the asset.

- The expected recovery value is non-zero.

- Investors are getting the rare opportunity of buying arguably the best gold company in the world at a good price, plus a free option on the resolution of Cobre Panama's situation, just as gold appears ready to rally.

Franco-Nevada ( FNV ) is the oldest and arguably the best royalty and streaming company in the world. The company has a portfolio of over 400 royalty and streaming agreements heavily focused on gold, but also exposed to silver, platinum group metals, crude oil, and natural gas. Its historical stock performance speaks for itself regarding the quality of the name. Since inception, its total return compounded annual growth rate has been an astounding 17.4%, outperforming all relevant benchmarks over the same period, including the NASDAQ (11.8%), the S&P 500 (9.2%), gold bullion ETFs (5.7%), and the GDX gold miners index (-1%).

Such outperformance has been a direct consequence of its superior business model. Royalty and streaming companies have historically outperformed both gold and gold miners. Compared with physical gold, streamers, and royalties offer leverage. Under streaming and royalty contracts, miners sell a fraction of their future production or revenues in return for an upfront cash payment. The company's revenues are directly linked to the gold price, but since there are costs to sustain, the exposure is leveraged, just as for gold miners. However, gold streamers and royalties have a far better track record than gold miners.

Streamers have outperformed both miners and physical gold (visualcapitalist.com)

{kind=link}

To start with, they have much higher profit margins. Franco-Nevada has achieved a year-to-date 83% Adjusted EBITDA margin and a 56% Adjusted Net Income margin. This is far better than gold major Barrick Gold, with a 45% Adjusted EBITDA margin and an Adjusted Net Income margin close to 0%. The fundamental reason for their better margins is that streaming and royalty companies have lower and less volatile costs. Since they don’t operate the mines directly, they do not incur the cost overruns that are so frequent in the mining sector, particularly in the post-COVID era. Since 2020, inflationary pressures and labor shortages have eroded the miners' profit margins: AISC has increased by about 30%, while the gold price has traded in a range. As a result, gold streamers and royalties have hugely outperformed gold miners.

Franco-Nevada has managed to control costs far better than gold miners (Company's Presentation)

{kind=link}

Moreover, royalties and streamers receive the benefits of exploration and expansion activities by the miners at no additional cost to themselves. Thus, a portfolio as vast as Franco-Nevada's embeds free optionality, which is often difficult to properly value. The company has a significant growth pipeline via numerous exploration and development stage assets without having to directly fund them.

Franco-Nevada benefits from exploration and expansion activities by miners, at no cost to itself (Company's Presentation)

{kind=link}

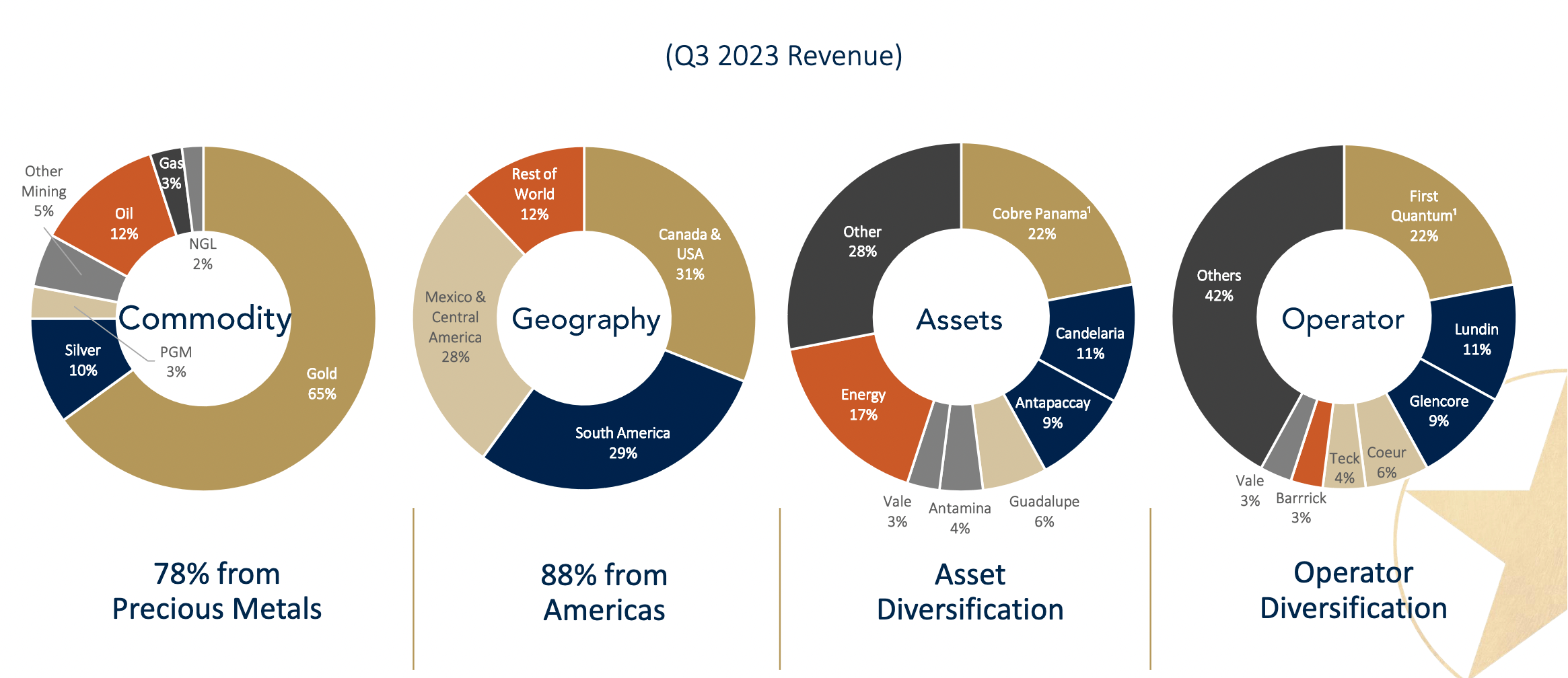

Finally, large streaming and royalty companies are diversified across different assets, geographies, and metals. About 29% of Franco-Nevada's revenues come from South America, 28% from Central America, 31% from North America, and 12% from the rest of the world. The majority of revenues are linked to gold (65%), followed by silver (10%). About one-fourth of the revenues come from oil, natural gas, and natural gas liquids exposures. Compared with miners, streamers, and royalties are less exposed to jurisdictional risks (since they operate in a large number of them) and less exposed to single-asset idiosyncratic risks (since they have interests in hundreds of mines).

Franco-Nevada's revenue diversification (Company's Presentation)

{kind=link}

In the case of Franco-Nevada, however, the assumption of diversification has recently been shaken by the closure of its Cobre Panama mine . As can be seen from the previous visualization, more than one-fifth of Franco-Nevada's revenues in Q3 came from this mine. Cobre Panama is operated by First Quantum and is one of the largest copper mines in the world. Franco-Nevada negotiated a streaming agreement for its gold and silver by-products in exchange for an initial investment of $1.36 billion. However, following unprecedented popular turmoil against the deal inked in October between the government and First Quantum, which gave it a license to operate the mine for another 20 years, Panama's top court has ruled the contract unconstitutional. The mine is currently on preservation and safe maintenance.

This is undoubtedly a terrible blow for Franco-Nevada. In terms of M&I gold-equivalent royalty ounces, Cobre Panama accounted for about 25.3% of its total metal portfolio (4,758 million ounces out of a total of 18,786 million). In addition, Cobre Panama was also expected to be one of the main near-term growth drivers. Although Franco-Nevada still has several other projects in its growth pipeline, and there is no reason why it won't be able to generate new deals going forward, the magnitude of the loss is evident.

For readers unfamiliar with the concept, gold-equivalent royalty ounces provide a way to quantify and compare Franco-Nevada’s economic interests across its disparate portfolio. A traditional net-smelter-return (NSR) royalty on a gold mining project entitles Franco-Nevada to a fixed percentage of the revenues from that mine. For example, the royalty ounces corresponding to a 2% NSR royalty are simply 2% of the Mineral Reserves and Resources of that project. In the case of a stream agreement, the situation is a little more complicated. If, for example, Franco-Nevada is entitled to buy a certain amount of gold ounces at a fixed price, it is necessary to factor in both the spot gold price and the fixed price to obtain the economic equivalent of an NSR ounce. If the deal does not concern gold ounces but silver, PGMs, or other base metals, it is also necessary to make assumptions about their spot prices. The main point is that Franco-Nevada provides in its Asset Handbook a computation of the royalty ounces of each asset in its portfolio. In this way, it makes it easy to make comparisons between different economic interests. It is as if Franco-Nevada only dealt with simple NSR royalty contracts.

There are, however, some important caveats to make regarding the computation of royalty ounces. First of all, royalty ounces do not take into account, by definition, the energy portfolio, which provides about one-quarter of Franco-Nevada’s revenues. Second, royalty ounces are computed on rather conservative spot price assumptions: the gold price is taken to be $1800 per ounce (currently above $2000 per ounce) and the silver price is $21 per ounce (currently about $24 per ounce). Even with all these caveats, royalty ounces remain, in my opinion, an extremely useful tool.

As mentioned before, Franco-Nevada has likely lost about a quarter of its M&I royalty ounces. The share price has suffered as a result, with its stock down about 20% since October, despite the gold price being up by about $150 per ounce over the same period. The question is whether the stock price has already fully discounted the implications of Cobre Panama's closure.

First of all, despite the loss, it is clear that Franco-Nevada's business model is not in peril. The company will continue to generate new deals and grow its royalty ounces going forward to cover the gap. In fact, because of the difficulties that junior developers find in raising capital via traditional means (such as debt- or equity-based deals), interest in alternative financing, via streaming or royalty deals, is expected to remain robust over the coming decade.

In addition, the financial stability of the company is not threatened. Franco-Nevada has $1.3 billion in cash and cash equivalents, plus about $1 billion in a credit facility. It also has no debt.

Therefore, it only remains to establish whether the stock price has fallen enough to account for the loss of Cobre Panama's royalty ounces. I would argue that the answer is yes. At the end of March, the company was trading around a market capitalization of $28 billion. Each M&I royalty ounce was valued at $28 billion / 18,786 million ounces = $1500 per ounce, approximately. Assuming the total loss of Cobre Panama, equivalent to 4,758 million ounces, and applying the same multiple, would give a market capitalization of around $21 billion. This value is very close to its current market capitalization. This means that the stock price is currently pricing in the total loss of Cobre Panama's ounces.

Let's have a look at the overall valuation after the drop. Franco-Nevada may still seem expensive when valued on traditional metrics. At a gold price of $2000 per ounce, the total undiscounted value of its metal portfolio is around $28 billion (obtained by multiplying its total royalty ounces, assuming the total loss of Cobre Panama, by $2000). Its current market capitalization is around $21 billion. Taking into account that its metal portfolio accounts for roughly three-quarters of NPV, this means that each of Franco-Nevada's M&I ounces is valued at approximately $1100. This is far more than for conventional gold miners. Of course, Franco-Nevada's earnings have lower volatility and higher expected growth. In fact, Franco-Nevada should really be valued as a growth company (in the last 15 years, it has been able to grow its portfolio by over 500%). From this perspective, the company is currently trading in line with its historical multiples.

Why do I believe, however, that the company is actually undervalued? Because up to now, I have assumed the complete write-off of Cobre Panama. There are reasons to believe that the political decision may be reversed. First of all, elections will be held in May 2024. Second, the Cobre Panama mine is such an important part of the national economy that its closure will also affect the government’s coffers. The mine makes up about 5% of the country’s GDP, supporting at least 40,000 jobs, directly or indirectly. Third, the concession has been declared unconstitutional before, in 2017, and the decision was later reversed. Finally, First Quantum Minerals has already expressed its intention to resort to international arbitration against Panama. Even if the mine stays closed, it is likely that Franco-Nevada will receive some form of compensation for the loss. In any case, the net present value is greater than zero.

Another reason to go long on Franco-Nevada at this price is that I am quite bullish on gold, as I have been for a while. Monetary headwinds are abating, with the Fed signaling the possibility of interest rate cuts again.

We therefore have a convergence of different factors. The stock price has suffered because of the closure of Cobre Panama. The market has overreacted by pricing in its total loss. By buying Franco-Nevada today, we are acquiring an interest in one of the best-managed companies available in the gold sector. We are also getting an option with a non-zero expected payoff on its Cobre Panama asset. We are doing so while gold appears ready to rally. For all these reasons, I am bullish.

For further details see:

Franco-Nevada: Crisis Begets Opportunity