FNV - Franco-Nevada: Valuation Starting To Improve

2023-11-20 07:56:04 ET

Summary

- Franco-Nevada had a softer Q3 with higher production at Cobre Panama, Tasiast and Antapaccay offset by a much weaker quarter for its diversified segment.

- Unfortunately, the Q4 outlook isn't much better with oil and natural gas trending lower and added uncertainty at its largest contributor, Cobre Panama.

- In this update, we'll dig into FNV's Q3 results, whether the Cobre Panama uncertainty is priced in, and where the stock's updated low-risk buy zone lies.

We're over two-thirds of the way through the Q3 Earnings Season for the Gold Miners Index (GDX) and one of the most recent companies to report its results was Franco-Nevada (FNV). The company had a mediocre Q3 overall with higher gold-equivalent ounce [GEO] sales in its precious metals segment offset by lower GEOs in its diversified segment, resulting in a ~9% decline in GEO sales year-over-year. This has left Franco-Nevada tracking towards the low end of its FY2023 guidance and adding insult to injury, Cobre Panama is back in the news for the wrong reasons. Worse, natural gas prices have fallen off a cliff again in an encore of last year's Q4 performance, and oil prices haven't held up much better, which shouldn't be surprising given that oil entered Q4 with frothy sentiment near-term. In this update, we'll dig into FNV's Q3 results, whether the Cobre Panama uncertainty is priced in, and where the stock's updated low-risk buy zone lies.

Cobre Panama Mine - First Quantum Minerals Website

{kind=link}

Q3 Production & Sales

Franco-Nevada released its Q3 results last week, reporting quarterly sales of ~160,800 GEOs, a 9% decline from the year-ago period. This sharp decline in output has left Franco-Nevada sitting at just ~70.8% of its annual guidance midpoint (670,000 ounces) with year-to-date GEO sales over 13% below the same period of last year. In Franco-Nevada's defense, the company was lapping very difficult comparisons after a parabolic rise in natural gas prices last year and a persistent uptrend in oil. Still, Salares Norte being slightly behind scheduled (expected to produce less than 5,000 GEOs this year), lower grades at Antamina and the impact from Cyclone Yaku on deliveries, and lower PGM prices haven't helped, offsetting what have been strong years otherwise for Cobre Panama, Marigold, Tasiast (record production in Q3 following Tasiast 24k Expansion), and bonus revenue in relation to its Haynesville interests (energy segment).

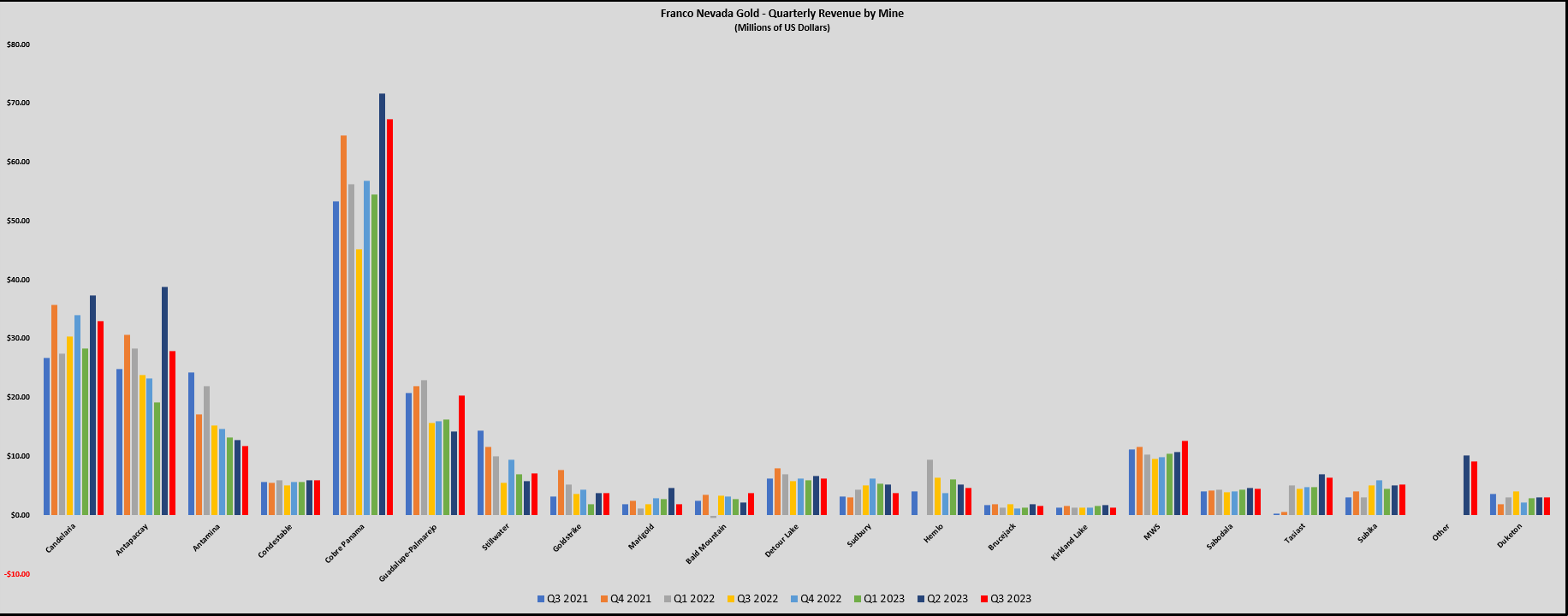

Franco-Nevada - Quarterly Revenue by Mine - Company Filings, Author's Chart

{kind=link}

Digging into the operations a little closer, Cobre Panama was the stand-out which wasn't surprising as it has been commissioning its CP-100 Expansion (Q3 2023: ~35,000 GEOs sold vs. ~26,400 in Q3 2022), and Guadalupe-Palmarejo benefited from higher grades in Q3. Meanwhile, Tasiast had a monster quarter and contributed $6.4 million in revenue, while Detour Lake had a solid quarter with revenue of $6.3 million attributable to Franco-Nevada despite unplanned downtime. Lower revenue from Antamina offset this in Q3 and year-to-date (planned lower grades), while revenue was up at Antapaccay because of higher copper grades and recoveries. However, as noted previously, the higher revenue for its precious metals segment ($240.8 million vs. $206.7 million) on higher sales and metals prices was more than offset by a steep drop in revenue from its energy segment.

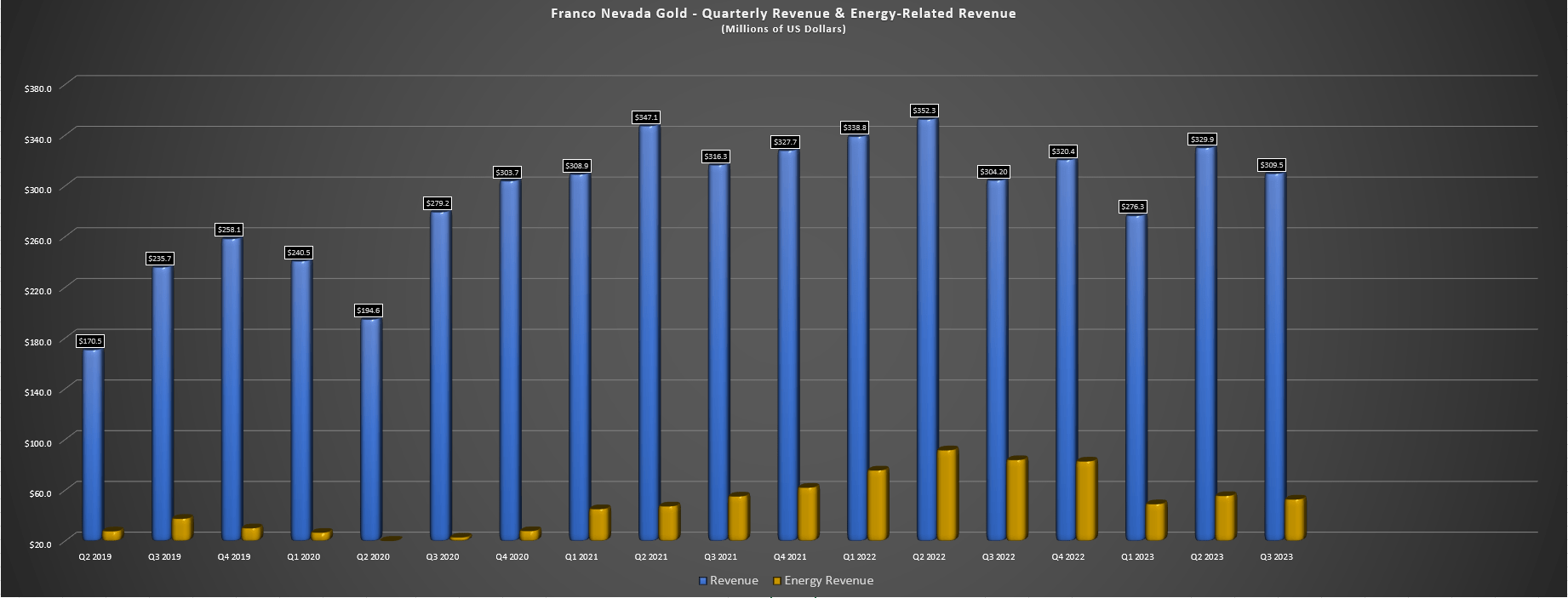

Franco-Nevada - Quarterly Revenue & Energy-Related Revenue - Company Filings, Author's Chart

{kind=link}

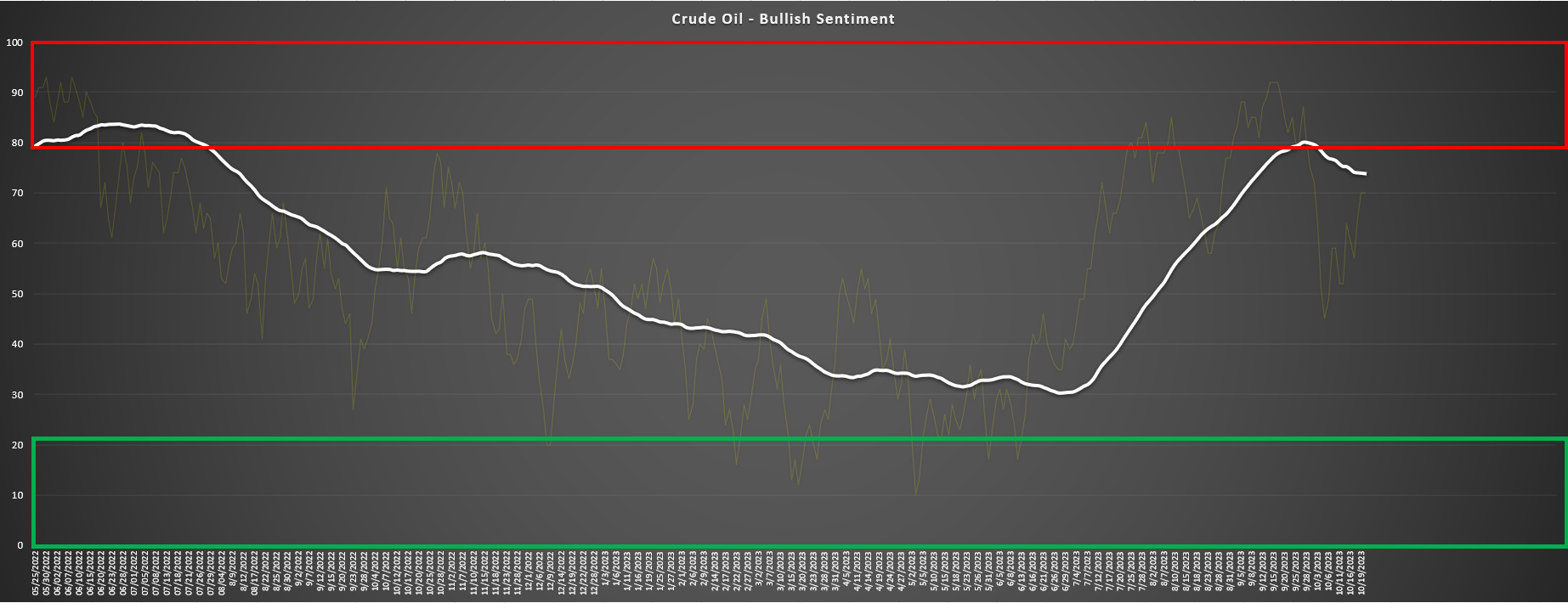

In fact, as the chart above shows, energy segment revenue fell from $83.8 million to $52.7 million, and this impact has been on a year-to-date basis as well with revenue down 8% year-over-year across the portfolio ($915.7 million year-to-date. The same is true of operating cash flow despite easier comparisons for its precious metals segment (depressed prices in Q3 2022), with an operating cash flow of $707.7 million vs. $720.2 million in the same period last year. As noted in my previous update, while Franco would see a sequential benefit (Q3 vs. Q2) from higher energy prices after the recovery we saw off the June lows for oil, it was difficult to be optimistic about Q4 given that sentiment headed into Q4 in nosebleed territory for oil (shown below). The result is that Franco-Nevada is now guiding to deliver towards the lower end of guidance (640,000 to 700,000 GEOs) and set up for meaningful year-to-date declines in revenue/cash flow unless we somehow see major breakouts in precious metals prices in the last 40 days of the year.

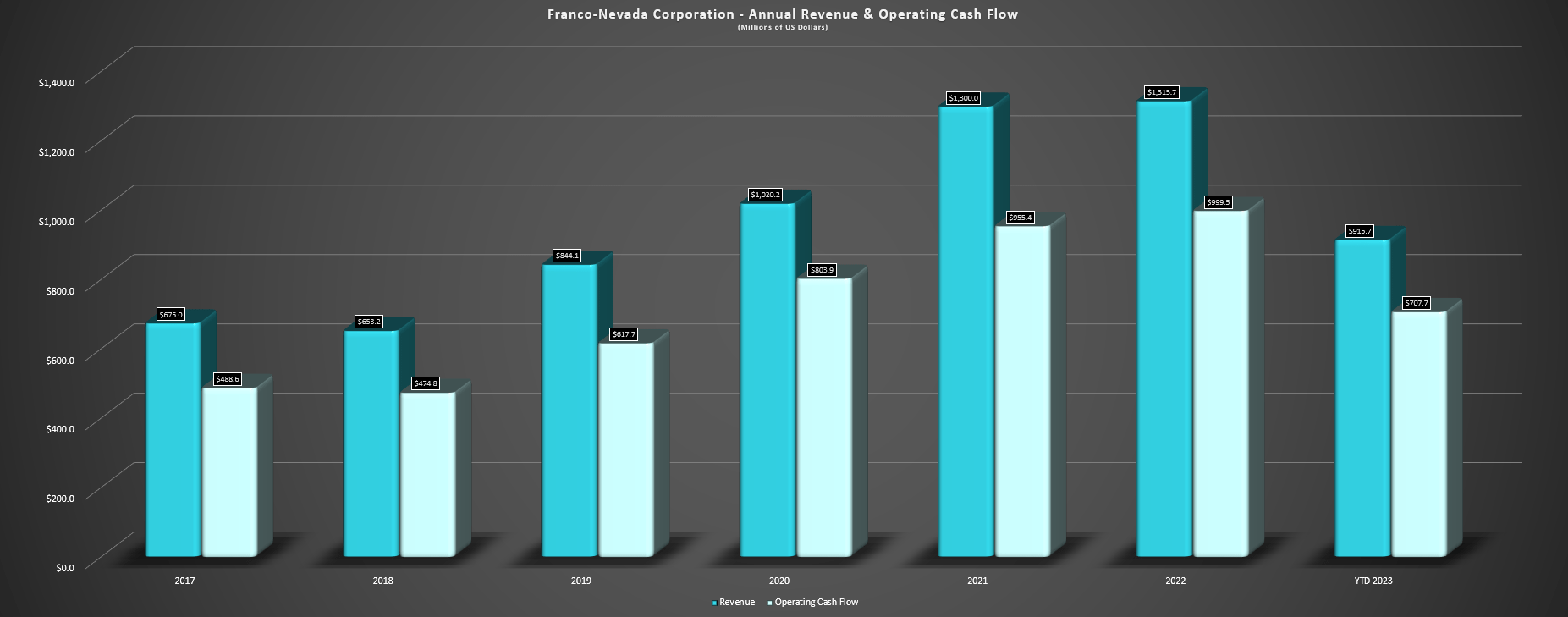

Crude Oil Sentiment - Daily Sentiment Index Data, Author's Chart Franco-Nevada - Annual Revenue & Operating Cash Flow vs. YTD 2023 - Company Filings, Author's Chart

{kind=link}

{kind=link}

In a normal scenario, the market might overlook this weaker quarter and year (which is largely because of tough comparisons), especially with multiple massive assets and a few smaller assets coming online or ramping up that will benefit FNV's 2024 results like Salares Norte, Greenstone, Posse, and Tocantinzinho (a chunky gold stream) plus a full year of commercial production/expansions at Seguela, Magino Tasiast, and Cobre Panama. However, the second dose of uncertainty related to Cobre Panama in a calendar year hasn't helped, with First Quantum Minerals (FQVLF) noting that it has reduced ore processing operations at the mine (one ramping down while two remain operational) because of an illegal blockade at the mine's port that are affecting the delivery of supplies for its power plant. In addition, these blockades have affected the loading of copper concentrate and it doesn't help that there are "a number of lawsuits" challenging the constitutionality of Bill 406 (signed into law in late October to approve the revised Cobre Panama contract between Minera Panama and the Panamanian Government). Let's take a look below:

Recent Developments

Unfortunately, Franco-Nevada's top contributor (the Cobre Panama Mine) is once again back in the news, with the Panamanian Government intending to hold a popular consultation concerning the revised contract for the Cobre Panama Mine following protests just after the mining concession contract was signed into law last month. As noted, this has increased uncertainty around this asset for the second time in less than a year. In fact, 2023 started with Franco-Nevada and the operator of the mine First Quantum selling off sharply following a brief suspension of processing operations (AMP refusing to permit copper concentrate loading operations at the mine's port) while First Quantum and the Panamanian Government worked on a draft concession agreement. That draft agreement was completed on March 8th, 2023, which included the following terms:

- Payment by Minera Panama (First Quantum's Panamanian subsidiary) of $375 million plus an additional $20 million to cover taxes and royalties up to year-end 2022

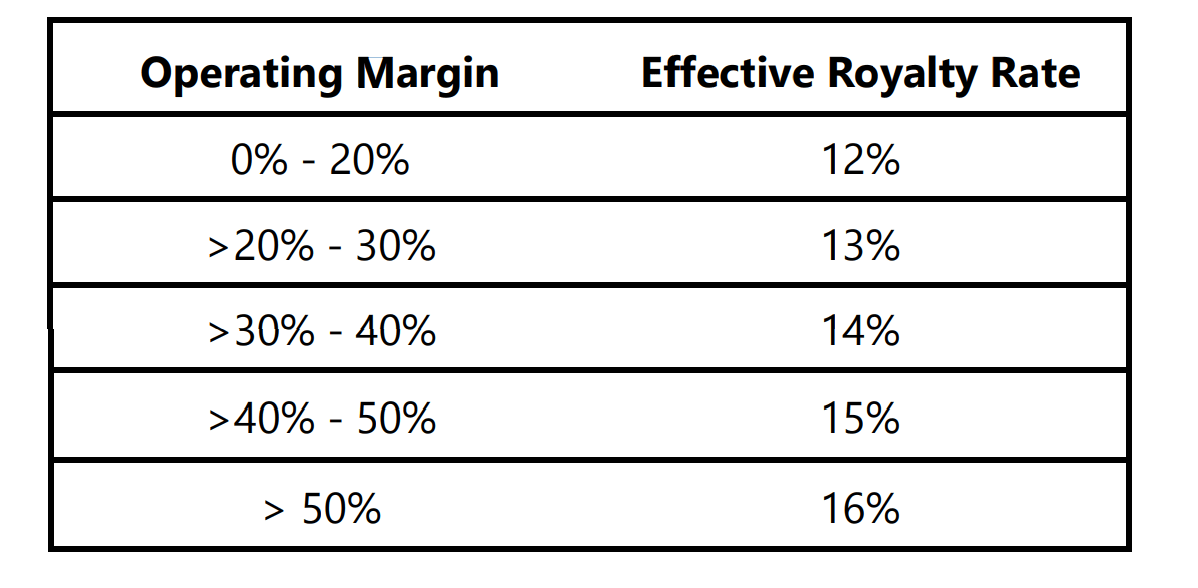

- Payment by Minera Panama of an annual minimum contribution of $375 million in government income made up of corporate taxes, withholding taxes, and a profit-based mineral royalty of 12-16% with downside protections

- Sliding scale applicable royalty rates of 12% on a 0-20% operating margin, and up to 16% on an operating margin of 50% or higher.

- Application of the general regime of income tax, including deductions for depletion, and withholding taxes in Panama.

Sliding Scale Royalty Rate Draft Concession Agreement Cobre Panama - First Quantum Website

{kind=link}

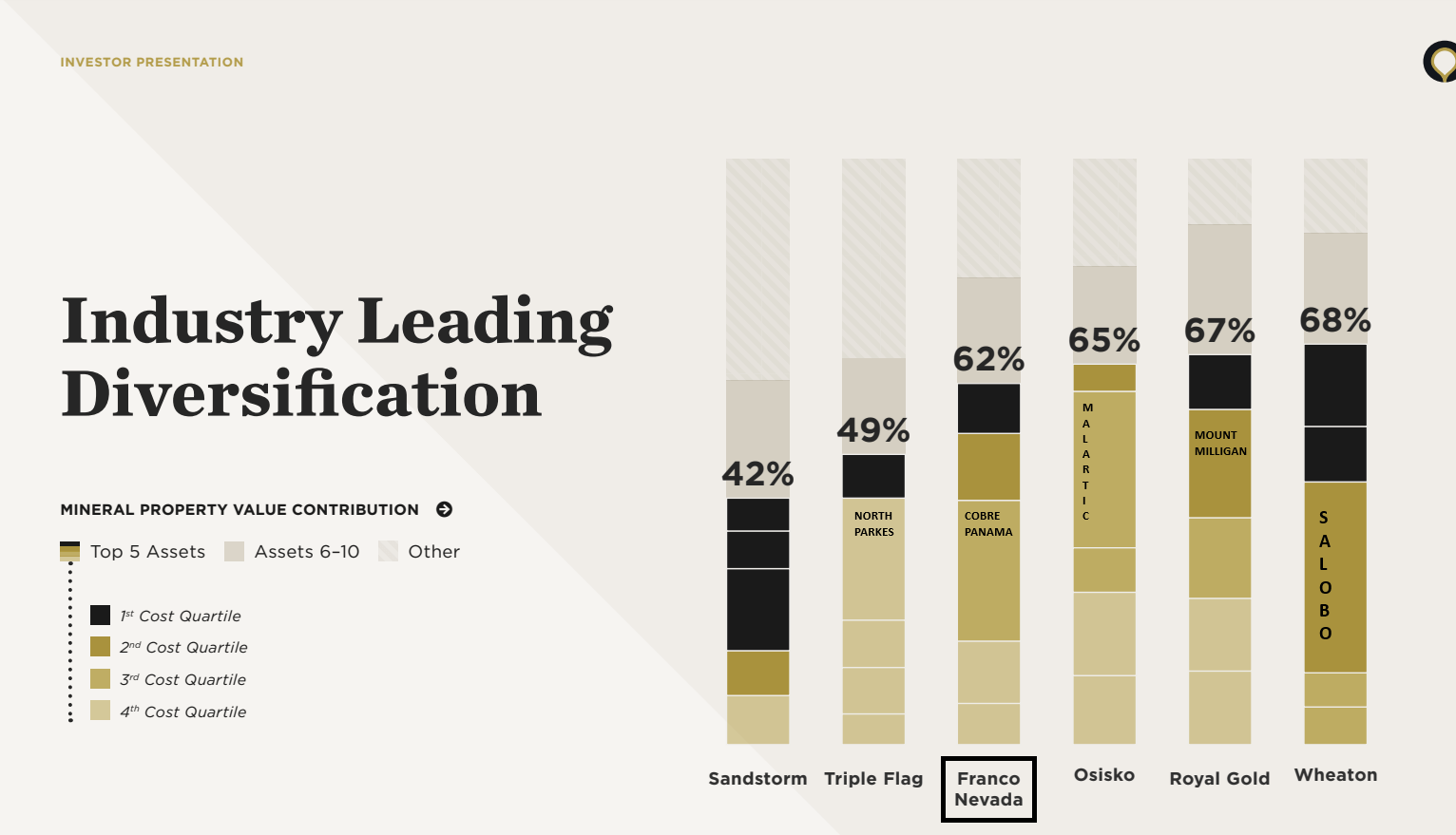

Obviously, the recent uncertainty when this previous scare was finally being discounted has unnerved investors, and some investors might believe the ~10% correction in Franco-Nevada's stock seems extreme when it's attributed to uncertainty at just one of its soon-to-be 120 producing assets (431 total assets). However, Cobre Panama is its best asset by a wide margin, making up ~21% of year-to-date revenue which is before the full ramp-up to CP100 Expansion levels (100 million tonnes per annum) at the asset by year-end. In addition, Cobre Panama makes up ~$2.5 billion of net asset value to FNV with its gold/silver stream, translating to $13.00 per share in value or ~20% of its estimated net asset value. And with Franco-Nevada regularly trading at 2.0x P/NAV or higher and a massive premium to the sector, this means its value in the stock is equivalent to $26.00, and arguably even higher given that oil/gas royalties don't trade at the same premium in the market precious metals royalties/streams.

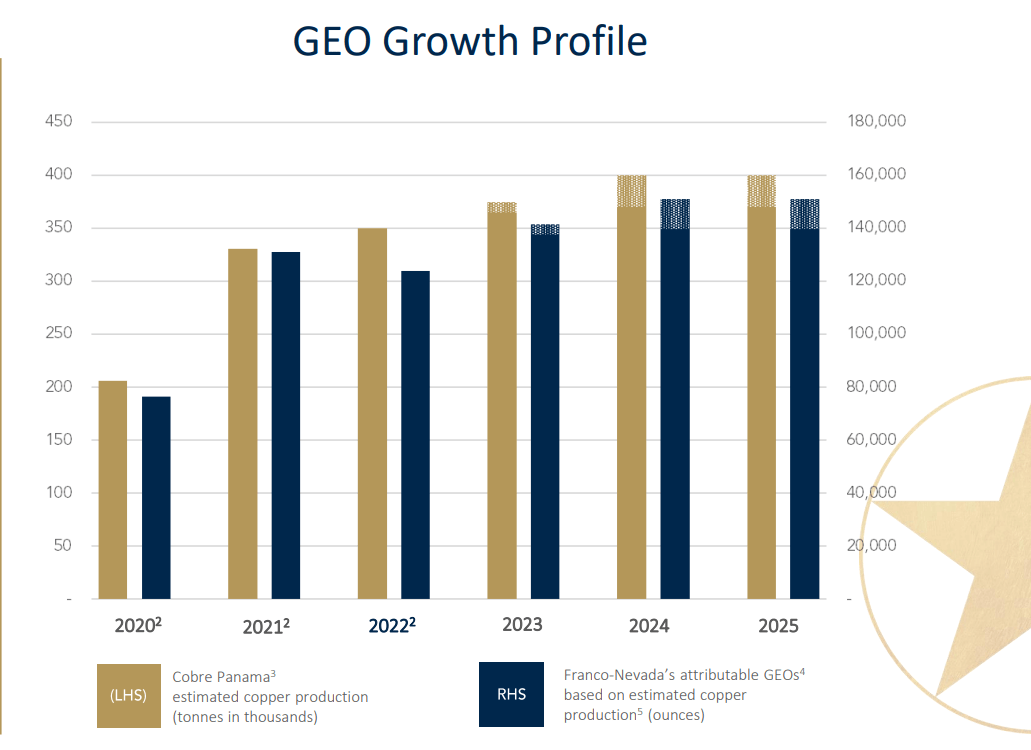

NAV Diversification Royalty/Streaming Companies - Sandstorm Gold Presentation, BMO Equity Research Cobre Panama Estimated Copper Production (000's) & Franco-Nevada Attributable GEOs - Franco-Nevada Presentation

{kind=link}

{kind=link}

Given that I see the fair value of Cobre Panama to Franco-Nevada at $25.00 - $30.00 per share at its historical NAV multiple, I would argue that the market hasn't fully discounted this asset judging by the ~$15.00 decline in the stock. And while an argument can be made that the market should not discount this full amount unless it believes Cobre Panama will head offline indefinitely and there will be no settlement from international arbitration, Franco-Nevada isn't particularly cheap ex-Cobre Panama if it headed offline. This is because we would see precious metals GEOs drop to closer to 410,000 GEOs in 2025 (even with the benefit of growth from new assets ramping up and recently coming online) of a total of ~600,000 GEOs, translating to less than 70% of GEOs from precious metals, down from closer to ~80% previously expected in 2024. This would justify some multiple compression (in my view), meaning that the impact wouldn't solely be from reduced cash flow and lower NAV, but also a lower cash flow and NAV multiple.

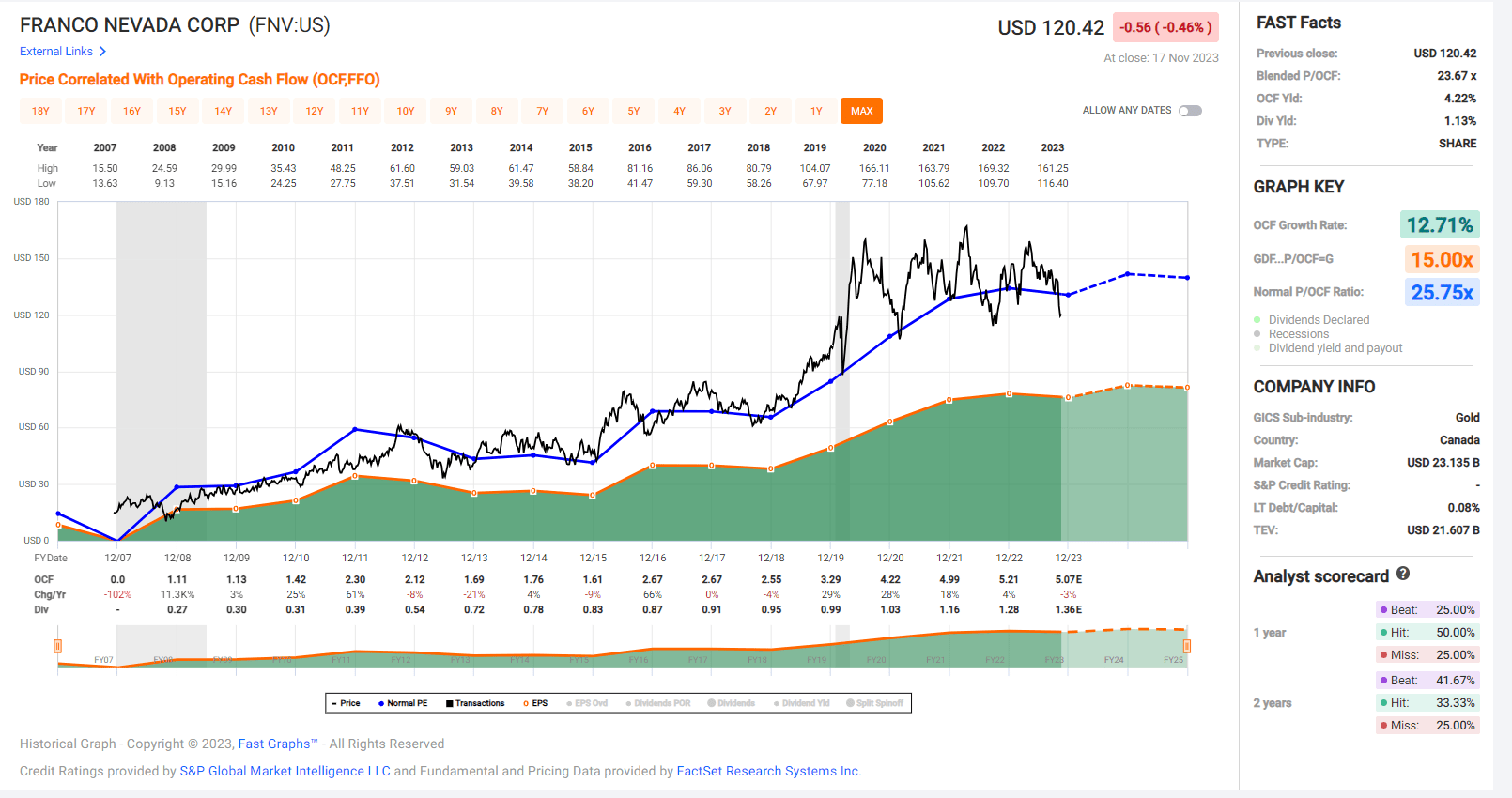

FNV Historical Cash Flow Multiple - FASTGraphs.com

{kind=link}

Obviously, all we can do is speculate currently on how this shakes out, and Franco-Nevada and First Quantum have one thing working in their favor, which is that Cobre Panama employs 4,000 people and makes up ~5% of the national GDP. Still, we have seen major mines taken offline temporarily in the past despite significant economic benefits, and I think it's difficult to argue that there's a meaningful margin of safety just yet, with FNV trading at over 20x FY2024 cash flow estimates which assume no further interruption at Cobre Panama and ~1.70x P/NAV (including Cobre Panama), with the former figure representing only a ~20% discount vs. its historical multiple of ~25.8x cash flow despite a much lower growth profile because of its scale (more difficult to grow GEOs from current size). That said, if the stock were to trade below US$110.00 where FNV would trade at just ~1.8x NAV even excluding Cobre Panama, I would view this as a low-risk buying opportunity given the company's industry-leading diversification with royalties/streams on many of the best assets globally.

Summary

Franco-Nevada has had a tough year due to lapping difficult tough comps and the Q4 outlook isn't much better with a port blockade at Cobre Panama (largest contributor) and continued softness in oil and natural gas prices. And while some of this is certainly priced into the stock here and not investing at current levels could be an opportunity cost if we see a favorable resolution, I prefer not to put capital at risk unless the reward/risk is stacked heavily in my favor and a stock is trading at a deep discount to fair value. Today, FNV certainly trades at a discount relative to its historical multiples, but these multiples are a little rich relative to peers (especially given the relatively higher non-precious metals exposure), and there are smaller-cap names available with less uncertainty with much less downside risk. Hence, while I think FNV is undoubtedly a top-5 way to get precious metals exposure, I would need a dip below US$110.00 to get more interested in the stock given the recent developments.

For further details see:

Franco-Nevada: Valuation Starting To Improve