FC - Franklin Covey: An Underdog Poised For Growth

2023-06-29 11:00:29 ET

Summary

- Franklin Covey Co. just reported its fiscal Q3 earnings.

- Franklin Covey has shown robust financial growth despite underperforming in comparison to its peers due to a successful shift to a subscription business model and strong capital allocation strategy.

- Potential risks include a slowdown in growth rate and over-reliance on subscription revenue.

- Despite those risks, Franklin Covey's impressive revenue trajectory, consistent rise in adjusted EBITDA, and capital allocation strategy make it attractive.

Thesis

In this article, I delve into an analysis of Franklin Covey Co. (FC), a global leader in training and consulting services. The company just reported bullish fiscal Q3 earnings yesterday, with a GAAP EPS of $0.32, surpassing estimates by $0.15, and revenues hitting $71.44 million, an impressive 7.9% increase year over year, beating expectations by $1.81 million. Currently, the company's stock is seeing a near 20% rise as a result, and despite underperforming within the Research & Consulting Services sector, being down by -10% YTD, Franklin Covey is beginning to claw its way back with an encouraging post-earnings pre-market gain.

While there are certain concerns tied to the company's high P/E ratios and price-to-book ratio, its robust subscription model, strong capital allocation strategy, and consistent rise in adjusted EBITDA indicate significant growth potential. The narrative is also punctuated by potential risks and headwinds, including the possibility of a slower growth rate and over-reliance on one source of revenue. Nonetheless, my analysis leans toward a "buy" rating for Franklin Covey, fortified by its solid financial performance, bullish Q3 earnings , and healthy capital structure.

Company Profile

Franklin Covey Co. is a global player in the training and consulting services domain, with its strategic fingerprints imprinted across key areas like execution, sales performance, productivity, customer loyalty, and educational enhancement.

Franklin Covey's operations are structured in a tri-segment configuration. First, we have the "Direct Offices," a pillar that provides a direct line of communication and services to clients. Second, their "International Licensees" segment leverages global partners to extend their reach and diversify their portfolio. Finally, the "Education Practice" segment bridges the gap between academic theory and professional practice.

Expectations

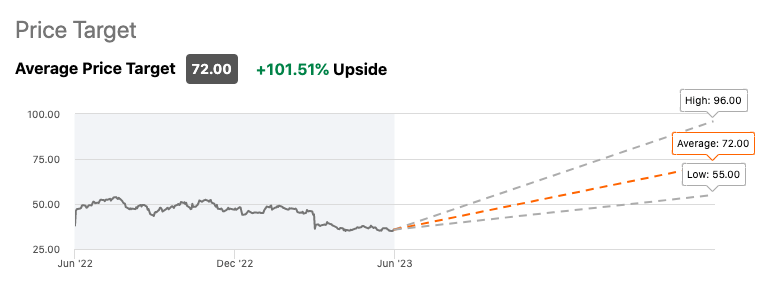

Franklin Covey is only covered by three Wall Street analysts who have an average "buy" rating on the stock, with an optimistic upside average price target of around 100%.

{kind=link}

Performance

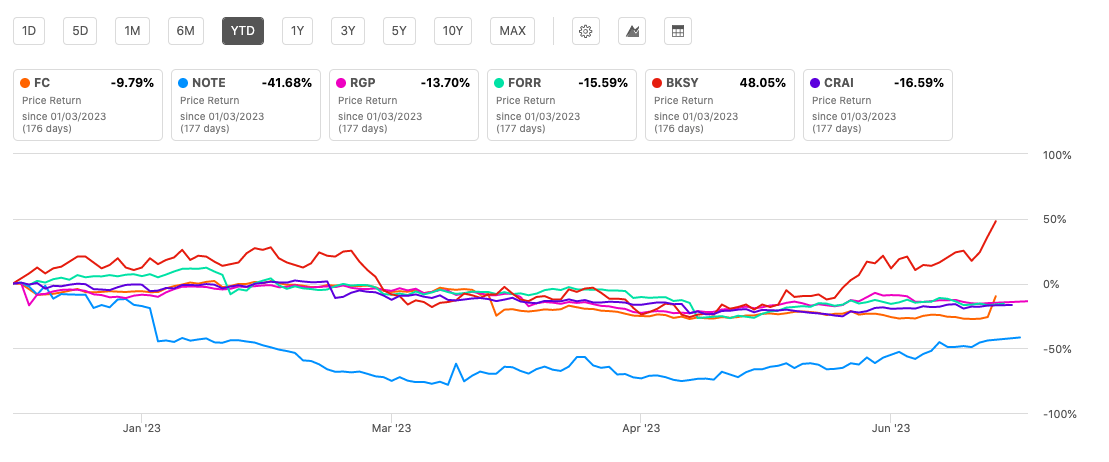

Relative to its peers within the Research & Consulting Services sector, Franklin Covey looks ready to shed its underachiever status and launch a great comeback story related to a massive boost from yesterday's earnings, now down just under 10% YTD (it was down -25% as of yesterday's close, btw).

{kind=link}

Valuation

Franklin Covey's valuation (see table below) is hanging in limbo, with a middling C+ grade, barely holding its own in comparison to the Industrials sector. The Price-to-Earnings (P/E) ratios, whether Non-GAAP or GAAP, are painting a tricky picture. For starters, both trailing and forward Non-GAAP P/Es are sitting considerably higher than the sector median. With an 84.69% difference to the sector median in TTM P/E Non-GAAP, and 58.05% for forward P/E, I'd be lying if I said it's not worrisome.

Seeking Alpha

The GAAP P/E ratios aren't looking any prettier, with both TTM and forward P/E ratios higher than the sector average. It seems that the market has high expectations for FC, and that's a lot of pressure.

Moving onto the PEG Non-GAAP ((FWD)), however, and there's a silver lining. FC's score of 1.35 implies that the market might be underestimating FC's growth potential, with its rating of B- showing a lesser degree of overvaluation relative to its expected earnings growth.

The EV/Sales (TTM and FWD) show a slightly less concerning scenario. FC's enterprise value is only slightly lower than the sales, both trailing and forward, in comparison to the sector median. The company is performing better when it comes to EV/EBITDA as well. Especially the forward EV/EBITDA which is 6.62% below the sector median - this is slightly comforting as it indicates the company's earning potential isn't as gloomy as the P/E ratios might suggest.

A sore point that's hard to overlook is FC's price-to-book ratio (P/B). At 5.41, it's more than double the sector median.

And the cash flow? The Price to Cash Flow ((TTM)) does offer some respite with a grade of B- as it sits below the sector median, meaning FC is generating satisfactory cash flow relative to its market price.

{kind=link}

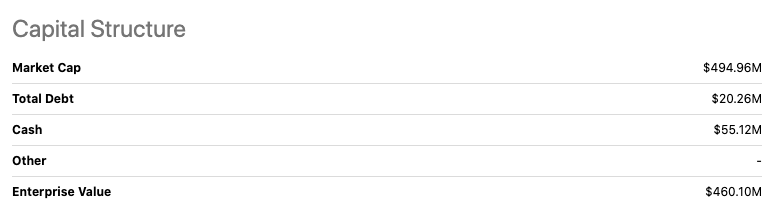

Lastly, regarding its capital structure with a Market Cap of $494.96M, total debt of a manageable $20.26M, and cash holdings of $55.12M, FC's Enterprise Value comes in at $460.10M. This suggests the company is in decent financial health.

Franklin Covey's Bullish Q3 2023 Earnings Takeaways

The narrative of Franklin Covey's financial performance is one punctuated by power, consistency, and potential. I'm particularly impressed by their remarkable revenue trajectory, underpinned by a successful transition to a subscription business model back in 2017. Since this pivot, the company's subscription and subscription services segment has blossomed spectacularly, delivering an upswing north of $150 million. The last fiscal year stands out, with a robust growth rate of 17% in this business line. With 52% of all contracts being multi-year contracts and high client retention contributing to 57% of the total subscription revenue, the model proves its mettle. Overall, the company's shift to a subscription-based model has had far-reaching effects, empowering client partners to consistently overshoot their annual revenue target of $1.3 million. The change has sparked a growth rate of about 10% for fully ramped client partners - a stark contrast to the paltry 2%-3% prior to the model's adoption.

Digging deeper, we uncover more signs of a promising future buried in the company's deferred sales balance. There's been a phenomenal increase in this metric, from $17.8 million in fiscal 2016 to a staggering $140.9 million in the recent quarter.

Investigating the company's profitability metrics, we encounter a scene that's just as reassuring. Gross margin has risen to a healthy 75.8%, and operating SG&A has trimmed down to 59.3%, heralding increased adjusted EBITDA. In fact, over the past fiscal year, adjusted EBITDA has ascended by 14% to settle at a solid $44.9 million.

The company's adjusted EBITDA forecasts are another reason for optimism. The figures for fiscal 2023 stand between $47 million and $49 million. Looking further out to FY 2024 and FY 2025, projections suggest figures of $57 million and $67 million, respectively. This consistent rise points to strong future profitability.

And lastly, looking at Franklin Covey's capital allocation strategy, the picture is equally impressive. Share buybacks to the tune of $50 million over the past five quarters, making up 8.8% of the company's total shares. So even after investing in share buybacks, the company still boasts considerable liquidity of over $100 million.

Risks & Headwinds

While Franklin Covey has shown impressive revenue growth, its rate of growth seems to be slowing down. The YoY revenue growth for the latest 12-month period is notably lower than that of the previous year. This slowdown in growth rate, combined with Franklin Covey's own admission that part of its significant growth in fiscal years 2020 and 2021 can be attributed to a rebound from pandemic lows, raises some, but not extreme, doubts about the company's ability to sustain its impressive growth rates in the long run.

As part of its growth strategy, subscription and subscription services revenue has experienced exponential expansion since it transitioned to this model. Unfortunately, however, its over-reliance on one source of revenue could leave it vulnerable to changes in market dynamics or customer preferences. Franklin Covey also mentioned a strong growth in its balance of deferred subscription sales. Although this points towards future revenues, it could also imply that the company is experiencing delays in recognizing revenue from its subscriptions, which might be a red flag.

And finally, while the company reaffirms its EBITDA guidance, the future growth rates in EBITDA predicted for fiscal 2024 and 2025 seem aggressive and may not be achievable, especially in light of the slowing growth rate. And despite expanding their client base, revenue growth from new logos has been slow, only growing marginally in each of the first three quarters this fiscal year. This slow growth rate might be a concern, especially given the aggressive expansion of their sales force.

Final Takeaway

In my final assessment, despite Franklin Covey's seemingly lofty valuation with high P/E ratios, I believe the strength of its subscription business model, remarkable revenue trajectory, consistent rise in adjusted EBITDA, and impressive capital allocation strategy underscores a compelling growth narrative. While certain risks and headwinds exist, Franklin Covey Co.'s solid financial performance, robust growth projections, and healthy capital structure underpin my analytical call to "buy" the stock.

For further details see:

Franklin Covey: An Underdog Poised For Growth