FC - Franklin Covey Q1 Results: Long-Term Thesis Remains Strong

2024-01-16 01:26:23 ET

Summary

- Franklin Covey is a small cap that has transformed its business from a transaction based to a SaaS model, enabling for predictable cash flow.

- The company recently reported quarterly results that I will describe as encouraging.

- AAP sales experienced a 13% growth, improved free cash flow generation, and purchased $16.3 million of shares.

- My valuation implied a price target of ~$48 by end of fiscal year 2025.

Reaffirming The Investment Thesis

In my previous and first article about Franklin Covey ( FC ), I discussed why I was bullish on the company. Since then the stock has underperformed the S&P 500 by roughly 8% and the company reported earnings twice. Before we dive into the quarterly results, let me first reaffirm my buy thesis.

FC's new service AAP, has transformed the business from a transactions base to SaaS. This has significantly improved margins and enabled predictable cash flow. The firm has also significantly deleveraged its balance sheet and started returning cash to shareholders. Additionally, I'm encouraged by the improved cash flow generation and AAP's subscription growth in the recent quarter.

Recent Quarterly earnings

Since my last article, FC has reported earnings twice, on November 1, 2023, and January 4, 2024. Today, I will be discussing the most recent quarterly results. The first quarter of fiscal year 2024. Let's dive in.

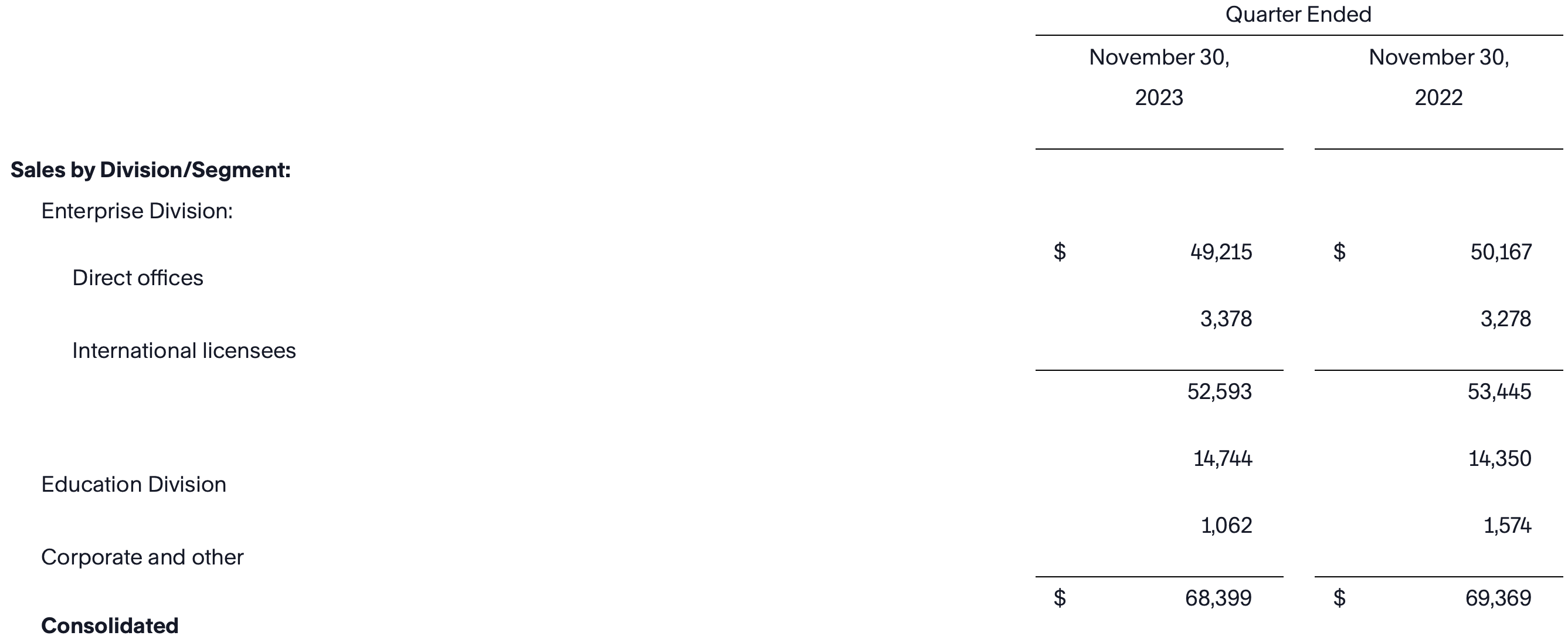

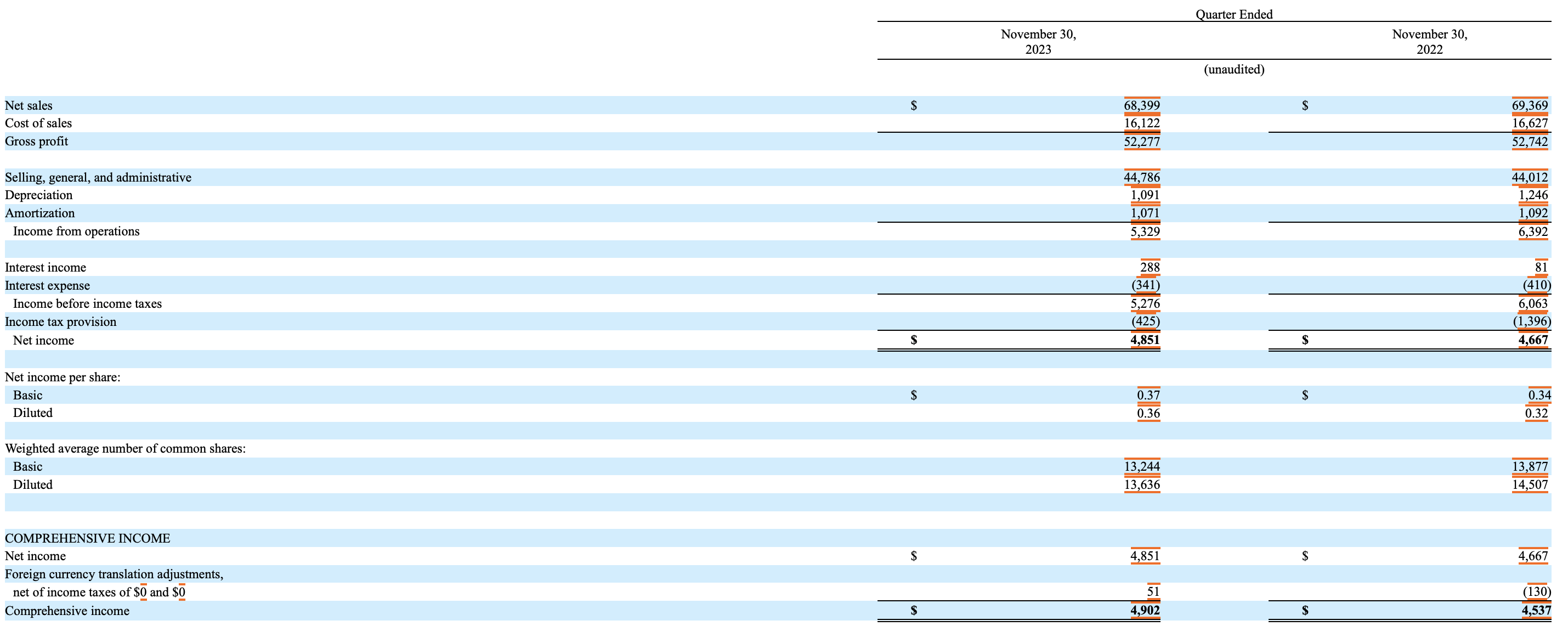

FC reported a relatively modest decrease in net sales, with a 1.40% change from the prior year, which might frustrate some investors, but not necessarily because the company's flagship service sales ("AAP") increased by 13% year-over-year; the only reason there was a decline in the direct office segment despite growth in AAP sales is due to the decrease in add-on services revenue.

{kind=link}

Q1-FY24 Press release

When it comes to SaaS companies, one has to look at deferred revenue to get an idea of future growth. At the end of November 30th, FC's deferred revenue totaled $103.3 million, up by $12.9 million from the previous year. The company also noted in its conference call that invoice subscription revenue is increasing. A large portion of the company's revenue is derived from subscriptions. This is what the CEO (Paul Walker) had to say:

Second is that our invoice subscription revenue is increasing. After flattish All Access Pass invoiced subscription growth in the second and third quarters last year

Gross margin improved by 40 bps due to lower sales and the cost of goods sold. Despite this operating margin diminishing year-over-year due to an increase in SG&A, the increase was due to $0.6 million of severance costs related to restructuring activity and $0.2 million of increased non-cash stock-based compensation expense.

{kind=link}

10Q

Cash flow from operating experienced a huge boost of $14.4 million from the previous year due to favorable changes in working capital, such as a decrease in accounts receivables (cash collected) and accounts payables. The company purchased 408,596 shares for $16.3 million and repaid $2.1 million of debt. The customer retention rate also remained high, above 90%. FC guided for an adjusted EBITDA of $54.5 million and $58.0 million, compared with the $48.1 million of adjusted EBITDA achieved in fiscal 2023.

All in all, I believe the firm started its fiscal year strong with a solid first quarter performance, beating top and bottom line estimates, and allocating capital in a way from which shareholders can benefit, such as through buybacks, debt reduction, and tuck-in M&A. Mr. Walker talked about current projects with customers that sounded promising; this is what he had to say:

The first is we're working with the CEO of a large and rapidly growing manufacturing company to develop their top 500 global leaders...The second example is where we're partnering with the Chief Human Resource Officer of a large 100,000-person firm to deploy multiple Franklin Covey solutions across the entire organization...

To me, this, combined with an increase in deferred revenue, emphasizes that there is still demand for FC's products in the corporate world despite the intense competition and harsh economic conditions.

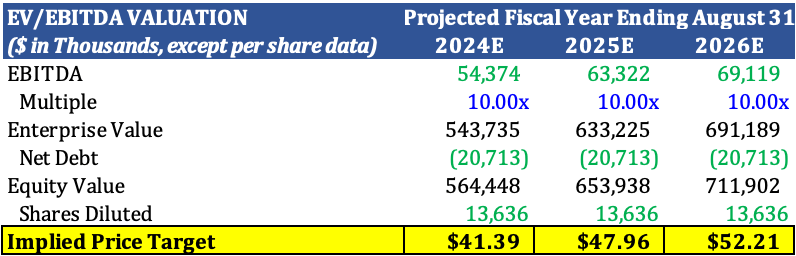

Valuation

For this analysis, I decided to value FC using a different approach, the EV/EBITDA method. I applied at a 10x multiple, which is in line with the FWD multiple, but at a discount to TTM. For 2025, I estimate an ADJ EBITDA of $63 million, which is below management's guidance of $66 million.

{kind=link}

created by the author

I arrived at an implied price target of $47.96, which translates into a 17% return from the price of this writing ($40.35). I model a 22.2% margin for COGS and 62.8% for SG&A. I expect the company to continue benefiting from economies of scale, which means that as revenue increases, costs as a percentage of revenue will decrease.

As you can see below, I expect free cash flow to almost double in 2024 due to the favorable change in working capital the company experienced in the recent quarter. FC spent roughly $9 million on curriculum development costs in 2023 and is guiding for $6–$8 million in 2024. These investments, combined with market growth and penetration, are my biggest top-line contributors.

{kind=link}

Created by the author

Investment Risks

As I mentioned in my last article, I believe the biggest risk facing FC is competition. The industry in which FC operates is highly fragmented; this can serve as a double-edged source. On one hand, it leaves FC (a large player) with a lot of room for expansion, but on the other hand, it could make it hard for FC to attract future clients. The other downside is that businesses are cutting spending and not enrolling as many employees in training programs. This can be due to high interest rates or recessionary environments.

Conclusion

To sum it all up, Despite the stock underperforming the market since my initial coverage, the fundamentals and financials of the company remain strong, underpinned by solid subscription growth, cash flow generation, and debt reduction. In the most recent quarterly results, the firm beat bottom-line estimates by double digits despite slow revenue growth, which led to a small rally in the stock.

Till next time.

For further details see:

Franklin Covey Q1 Results: Long-Term Thesis Remains Strong