FC - Franklin Covey: Recurring Revenue And Better Margins

2023-09-26 02:57:37 ET

Summary

- Franklin Covey’s revenue has grown at a modest 4% CAGR, as industry tailwinds and the development of its services offering have driven growth.

- FC has a strong brand and reputation for delivering tangible results. Unlike many of its peers, the business is internationally recognized.

- FC’s margins have improved, owing to increased subscription revenue. Management is continuing to focus on expanding this, creating the scope for further gains.

- The business performs modestly relative to its peers, with an attractive upside based on improving financial metrics.

- Although we do see factors slowing growth, FC’s attractive FC yield and discount to its historical average imply value.

Investment thesis

Our current investment thesis is:

- FC is an attractive business, owing to its global brand recognition, suite of services, and future-proof model that continues to develop. We believe subscription-related services will perform well in the market, although the competition faced should not be underestimated. The differentiating factor is FC’s credibility in the corporate environment.

- FC’s financial development and business model adjustment have the potential to smooth its upward trajectory, contributing to greater shareholder returns. We believe there remains scope for greater value.

Company description

Franklin Covey Co. ( FC ) is a global company specializing in performance improvement solutions. Headquartered in Salt Lake City, Utah, the company offers training, consulting, and tools to organizations and individuals to improve their effectiveness in areas such as leadership, productivity, time management, and strategy execution.

Share price

FC’s share price has experienced periods of volatility, although generally in an upward trajectory, contributing to strong returns relative to the wider market. This has been driven by positive financial development during this period, although again with some YoY volatility.

Financial analysis

Franklin Covey financials (Capital IQ)

{kind=link}

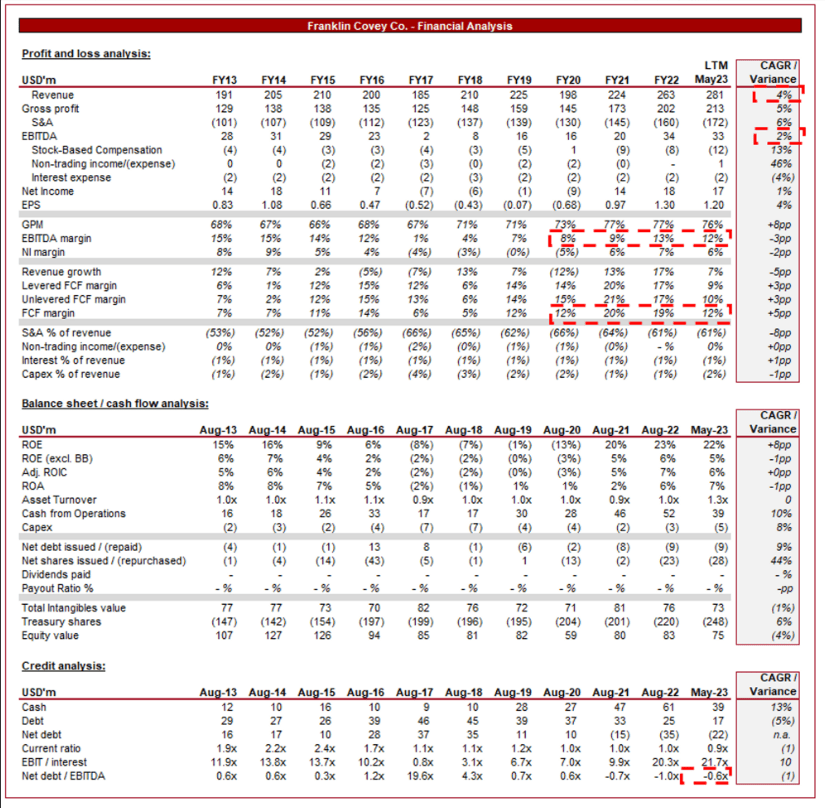

Presented above are FC's financial results.

Revenue & Commercial Factors

FC’s revenue has grown at a CAGR of 4% during the last decade, with solid consistency YoY. There have been some periods of negative growth, owing to one-off disruptions such as the pandemic, as well as lower demand.

Business Model

FC is a global company specializing in leadership and performance improvement solutions. It offers a wide range of training, consulting, and coaching services aimed at helping individuals and organizations achieve their goals and maximize their potential. FC works closely with clients to tailor solutions to their specific needs. This customization ensures that its programs align with the unique challenges and objectives of each organization.

FC works with a range of businesses, differing by sector or size. The company places a strong emphasis on leadership development at all levels, from individual contributors to top executives. It offers leadership academies, workshops, and coaching to cultivate effective leadership skills. In addition to this, FC developed its digital services, providing online courses, online productivity platforms, and training on time management and prioritization. These services are bundled into various subscription services, allowing FC to generate strong, recurring revenues, and contributing to margin appreciation.

Additionally, FC offers consulting services related to strategy execution, culture transformation, and organizational effectiveness. Its consultants work closely with clients to drive sustainable improvements against existing results.

Central to FC’s business model is its proprietary content and intellectual property. This includes well-known frameworks like "The 7 Habits of Highly Effective People" and "The 4 Disciplines of Execution." (both authored by members of the Covey family). These frameworks serve as the foundation for their training programs and materials.

FC’s solutions are designed to produce tangible results and measurable improvements in leadership effectiveness, productivity, and organizational performance. This is one of the reasons the business continues to be highly successful, as it stresses the benchmarking of the improvements it provides.

The company's global presence allows it to serve clients in various regions, industries, and sectors, contributing to an expanding client base that has a greater growth trajectory. We consider this a key advantage of the business, as many of its peers are equally as small but lack the market presence that comes with the success of Covey’s books.

Consulting and Training Industry

FC faces competition from a variety of sources, including other consulting firms, training organizations, and self-help content providers. Competitors may include Dale Carnegie, Gallup, and online education platforms.

We believe the following are key industry trends impacting the company’s growth trajectory:

- Digital Transformation - The digitalization of society has contributed to greater options for information transfer to consumers, threatening FC’s position as a gatekeeper to high-value ideas. There has been a significant rise in the number of online courses, both paid and free, as well as dissemination of data. FC's move toward digital learning and online resources has allowed it to reach a broader audience and respond to this, but overarchingly, we believe it has contributed to greater competition. Conversely, technology has contributed to greater complexity associated with running a business, suggesting an offset benefit as leadership teams require greater training.

- Data democratization - Empowered by technology and economic development, the transfer of data and information is as easy as it has ever been. Not only through digital platforms but also through books, education such as universities, etc. Similar to the above, this provides the business with increased competition given a widening array of alternatives.

- Demand for Continuous Learning - In the knowledge/data economy, the demand for continuous learning and skill development is high. For this reason, we believe there will continue to be a healthy demand for such services in the long term, with scope for improvement as the complexity of day-to-day operations continues to increase.

- Leadership Focus - In an increasingly competitive and rapidly changing business environment, driven by globalization, and technological and economic development, leadership is a critical factor for success. FC’s solutions continue to resonate well with leadership teams as a low-risk option to generate incremental gains.

- Proven Methodologies - Within this industry, having a strong track record, reputation, and visible results is key. The company's signature frameworks, such as "The 7 Habits," are widely recognized as effective tools for personal and organizational transformation, allowing FC to still benefit from these ideas decades later. This underpins the broader reputation of the company, which is highly positive, with its success stories well documented.

- Strategic Partnerships - Collaborations with other organizations and institutions have expanded their reach and brought their content to new audiences, underpinning the credibility of its services and further marketing the company.

Margins

{kind=link}

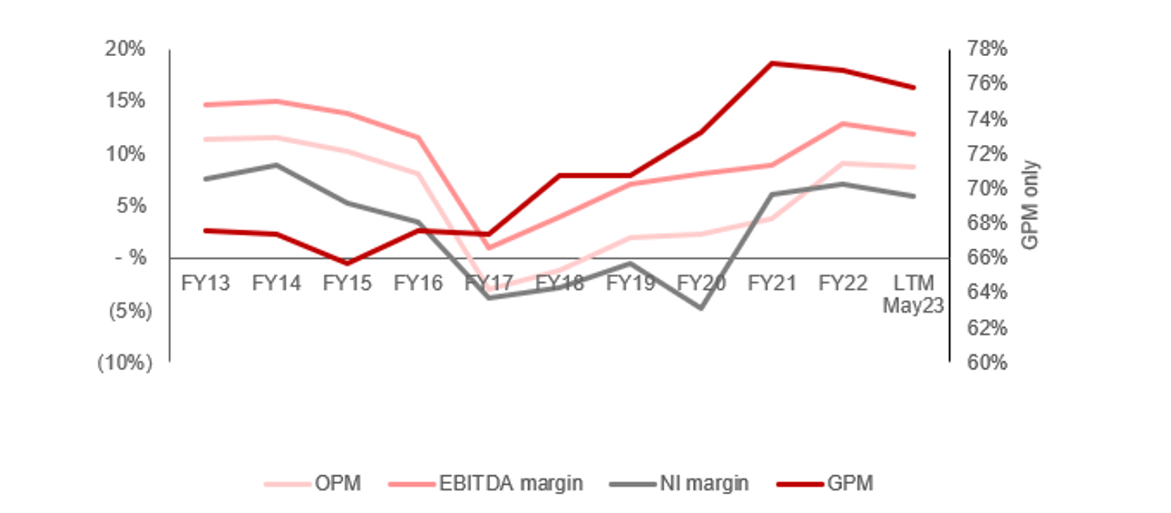

FC’s margins have been unusually volatile, owing to fluctuations in both economic and industry conditions. The improvement in recent years is a reflection of its transition toward high-margin services, namely subscription revenue, allowing for investment in high-quality solutions to generate ongoing revenue at low incremental costs.

Quarterly results

FC’s quarterly revenue growth has been exceptionally consistent, with the top-line growth in the last 4 quarters being +6.2%, +7.9%, +9.2%, and +9.7%. This has been slightly propped up by a dip in margins, with LTM EBITDA-M declining 1ppt. Broadly, we consider this a strong performance given the current economic conditions, which would understandably contribute to reduced spending in response to softening demand.

The key takeaways from Q2 are:

- All Access Pass subscription and subscription services grew by 6%, underpinning the positive trajectory of its subscription services.

- Education revenues grew 18% on the strength of increased consulting, coaching, and training days delivered. Consulting services will continue to be the cornerstone of FC and the key revenue driver, with subscriptions positioned to improve revenue.

- Billed subscription and unbilled deferred subscription revenue grew 21%, compared with May22. This should ensure a continuation of growth in the near term.

Overall, this has been a strong quarter for the company and a reflection of its business model optimization through the increase in subscription services.

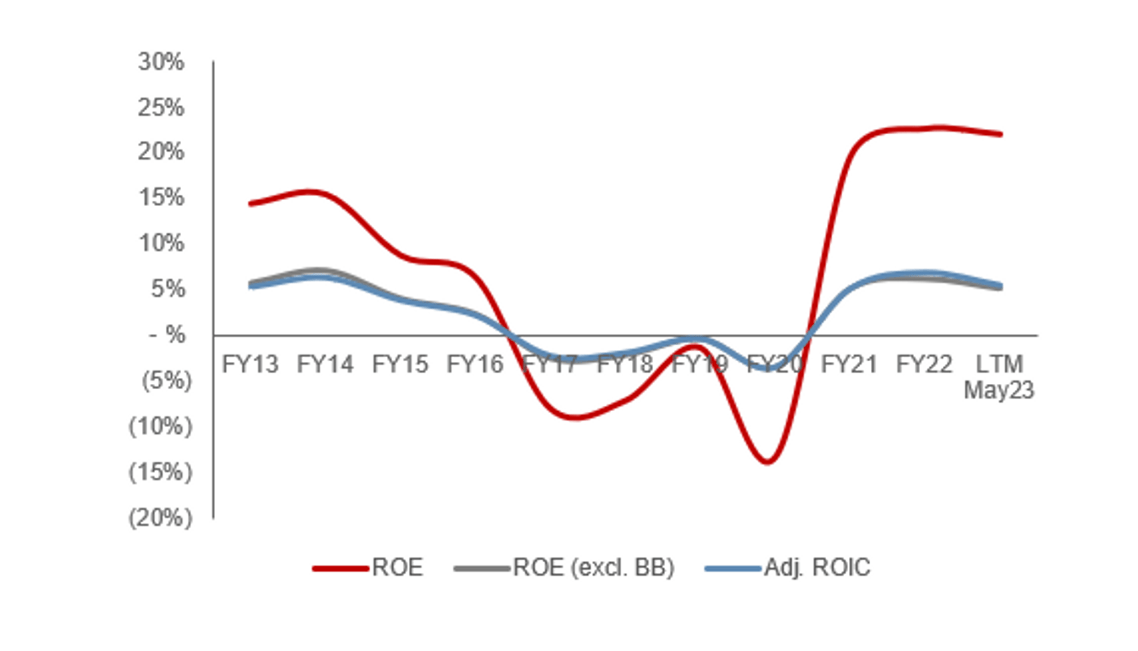

Balance sheet & Cash Flows

FC’s balance sheet is extremely clean. This company’s strong margins in recent years have translated to FCF, allowing the business to comfortably fund operations and allocate excess capital to shareholder returns. As the following illustrates, diluted shares have declined c.14%, supporting share price returns.

Our only concern would be the inability to achieve a consistent return. Volatility makes it extremely difficult to assess normalized performance levels and the achievability of its current trajectory going forward. We would expect that greater recurring revenue will mean this softens.

{kind=link}

Outlook

{kind=link}

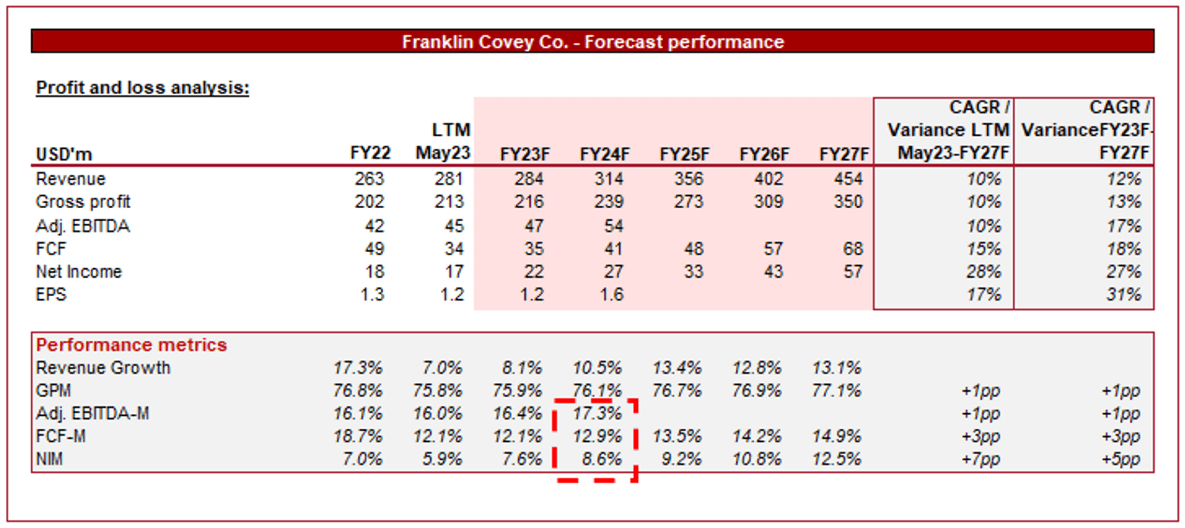

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting an improvement in FC’s growth, with an average growth rate of 10% into FY27F. In conjunction with this, margins are expected to broadly remain flat with some sequential improvement, which inherently assumes the current higher margins are sustainable.

We consider the revenue assumptions to be at the top-end of reasonable, as although subscription growth will support improved growth, moving into the double-digits appears difficult with this mature industry. Further, we consider the margin expectation to be reasonable given the growing subscription revenue.

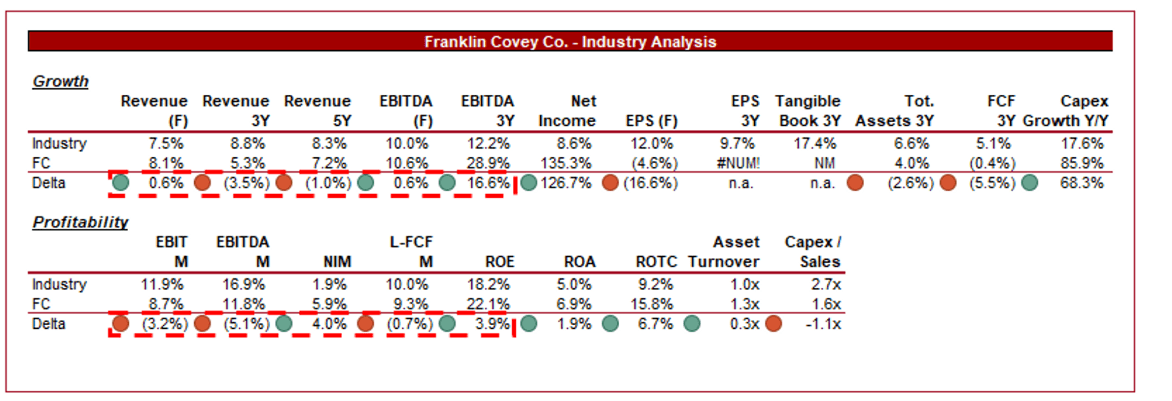

Industry analysis

Research and Consulting Services Stocks (Seeking Alpha)

{kind=link}

Presented above is a comparison of FC's growth and profitability to the average of its industry, as defined by Seeking Alpha (29 companies).

FC performs modestly relative to its peers, although is far from a standout. The company’s revenue growth has underwhelmed across a 3Y and 5Y period, although the recent improvement is expected to continue in the forward period. Further, this weakness is offset by the growth in profitability metrics. This revenue weakness is a reflection of the competitive environment FC operates within, as the rate achieved is not necessarily disappointing.

Additionally, FC’s margins are equally “middle of the road”. Its NIM, ROE, and FCF are respectable, with evidence of outperformance. However, its EBITDA-M is noticeably below the average, even after the improvement in recent years. This margin weakness is slightly exaggerated by the number of Research businesses that operate a purely recurring revenue profile and are essentially data companies.

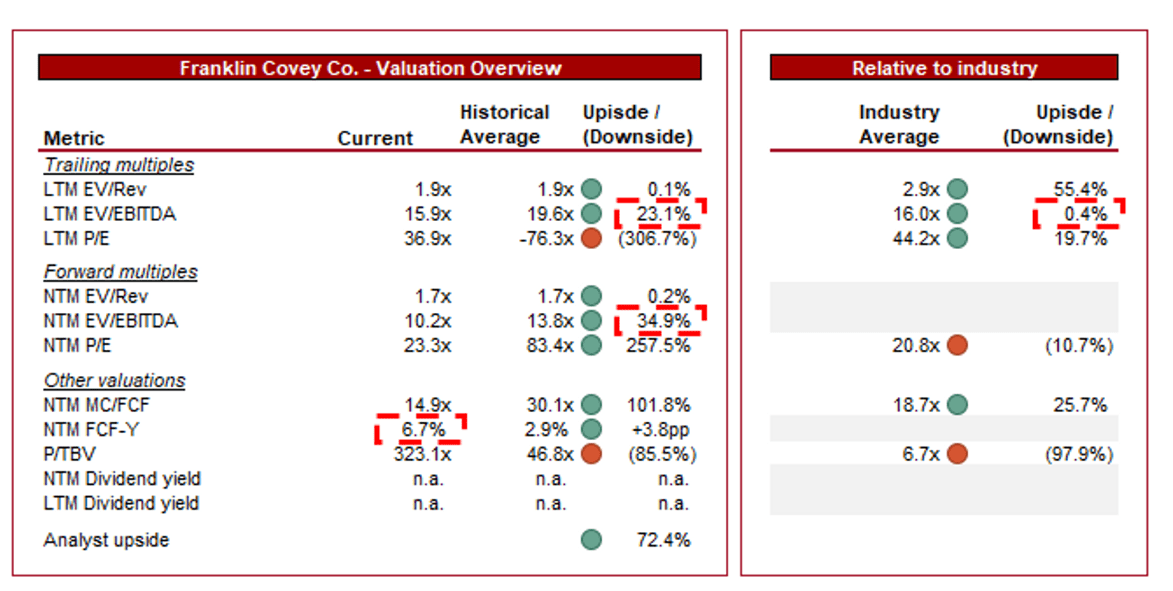

Valuation

{kind=link}

FC is currently trading at 16x LTM EBITDA and 10x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average is not warranted in our view, primarily due to the transitioning of its business model toward greater subscription revenue. We do believe these gains are offset by the scope for greater competition but on a net basis, a discount appears harsh.

Further, FC is trading at a similar valuation to its peers, with a small LTM discount and a small NTM premium. Our view is that a direct comparison is difficult to assess given the fundamental differences in business models and how revenue/margins interact. We consider the LTM metric to be more reasonable, which at a discount appears reasonable without screaming value.

The key for investors is to assess whether the expansion of subscription revenue or increased competition will be more impactful. We believe they will be broadly offsetting, although a medium-term outperformance appears reasonable based on trajectory. At an FCF yield of 7%, significantly above its historical average, we consider the stock undervalued.

Key risks with our thesis

The risks to our current thesis are:

- Scope for expanding subscription revenue - The key for FC to successfully transition toward greater recurring revenue is to develop related services that can be bundled into subscriptions. This will involve expanding its IP and potentially acquiring capabilities. Offsetting this will be competition within the market.

- Consulting volatility - The company has experienced past volatility associated with the demand for its consulting services. This risk continues to be the case.

Final thoughts

FC is a solid business. The company’s foundations are strong, built on a universally appreciated book and expert (Mr. Covey), alongside over a decade of successful projects with a number of clients. The company is uniquely positioned within the market due to its strong brand, reducing the impact of competition. We do believe there is scope for greater headwinds, although offsetting this is its focus on developing subscription-based revenue.

The key in our view is that margins have increased and are remaining resilient despite economic pressures. Further, the trajectory remains positive with healthy quarterly revenue growth. With an FCF yield of over 6%, we consider the stock a buy.

For further details see:

Franklin Covey: Recurring Revenue And Better Margins