FELE - Franklin Electric: Growth Challenges Keep Me On The Sideline

2023-12-26 03:08:41 ET

Summary

- Franklin Electric Co. faces near-term headwinds from declining backlog and inventory destocking, impacting revenue growth.

- Projects in the Water Systems and Fueling Systems segments are being deferred due to high interest rates, further impacting revenue growth.

- There are also concerns about the long-term decline in traditional gas station sales due to EV adoption.

Investment Thesis

I last covered Franklin Electric Co., Inc. (FELE) in early October with a neutral rating. While the stock is up in sync with the broader market since then, I continue to prefer remaining on the sidelines. The company's revenue growth faces near-term headwinds from a declining backlog and inventory destocking at its customers. In addition, the company's Water Systems and Fueling Systems businesses are seeing projects deferral from clients due to high interest rates which should continue to impact revenue growth over the next few quarters. While a potential reversal in the interest rate cycle and easier Y/Y comparisons are expected to help the company's revenue growth in the back half of next year and beyond, there are concerns about the long-term decline in the company's traditional gas station sales in the Fuelling Systems segment sales due to EV adoption. The company is offering some EV-related products but there is not much clarity on the extent to which the company's new and relatively small EV-related sales can offset the decline in its traditional fueling systems product lines.

On the margin front, the benefits from the company's cost-control efforts and declining commodity costs should help the margins. However, the unfavorable mix due to lower sales in the high-margin Fueling Systems segment should continue to negatively impact margin growth.

So, despite FELE stock trading at a discount to its historical averages, the unfavorable growth prospects keep me on the sidelines and I have a neutral rating.

Revenue Analysis and Outlook

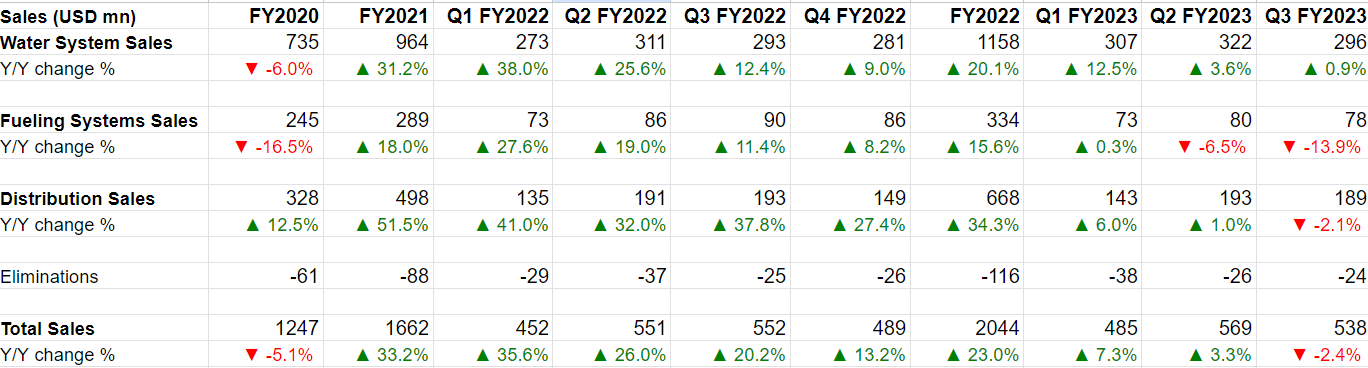

After experiencing double-digit growth in FY21 and FY22 benefitting from strong end-market demand, price increases, and strategic acquisitions, FELE witnessed a slowdown in sales growth as FY23 progressed and the company's sales turned negative in the last quarter.

In the third quarter of 2023, the company's sales declined 2.4% Y/Y to $538 million due to lower volumes and a 2% impact from unfavorable FX translation which more than offset the benefits from higher price realization. In the Water Systems segment, sales grew 0.9% Y/Y led by continued strong end-market demand for large dewatering pumps, mainly in the U.S., and increased sales in the Latin America and EMEA regions. This was partially offset by a decline in sales of groundwater equipment brought on by channel inventory destocking and wet weather conditions across the U.S.

In the Fueling Systems segment, sales declined 13.9% Y/Y due to the negative impact of continued channel inventory destocking, market delays in new station build projects, and divestiture of the above-ground storage tank business in 2022. The Distribution segment's sales declined 2.1% Y/Y caused by lower pricing on commodity-based products sold through the business and continued wetter-than-expected weather delaying contractor installations across much of the U.S.

FELE's Historical Revenue Growth (Company Data, GS Analytics Research)

{kind=link}

Looking ahead, I anticipate a challenging period for the company in the next few quarters.

While the company has benefited from elevated backlog levels in recent quarters, facilitating sales, the backlog is swiftly returning to normalized levels. Sequentially, the company's backlog was $44 million lower at the end of Q3 compared to Q2. I expect the company's backlog to further decrease by the end of Q4, and the company entering next year with a lower backlog doesn't bode well for sales.

The company's sales grew 7.3% Y/Y in Q1 FY23 on top of 35.6% Y/Y growth in Q1 FY 22. I believe high backlog levels at the end of the previous year played a role in strong Q1 FY23 growth. The Y/Y growth then sequentially decreased as the year progressed with backlog levels continuing to decline. As the company laps the benefits from higher backlog conversion in the last year, I expect growth to be negative at least in the first half of the next year.

The end market conditions are also challenging with the company continuing to see inventory destocking in the near term and its project business, both in the water as well as fueling side, seeing deferral from clients due to high interest rates. The Grid Solution business on the Fueling side is seeing a good demand as EV adoption tailwinds continue to benefit it. However, this is a relatively new and smaller portion of the company's business and most of the Fueling segment is tied to traditional gas stations where there is a long-term threat from secular decline.

There are some positives though. With a potential reversal in the interest rate cycle by mid-2024, some of the deferred projects may get started as the return on investment becomes more attractive. The comparisons are also getting easier in the back half of FY24.

So, the growth outlook of the company is mixed with the first half of FY24 expected to be challenging and some improvement expected in the back half.

Margin Analysis and Outlook

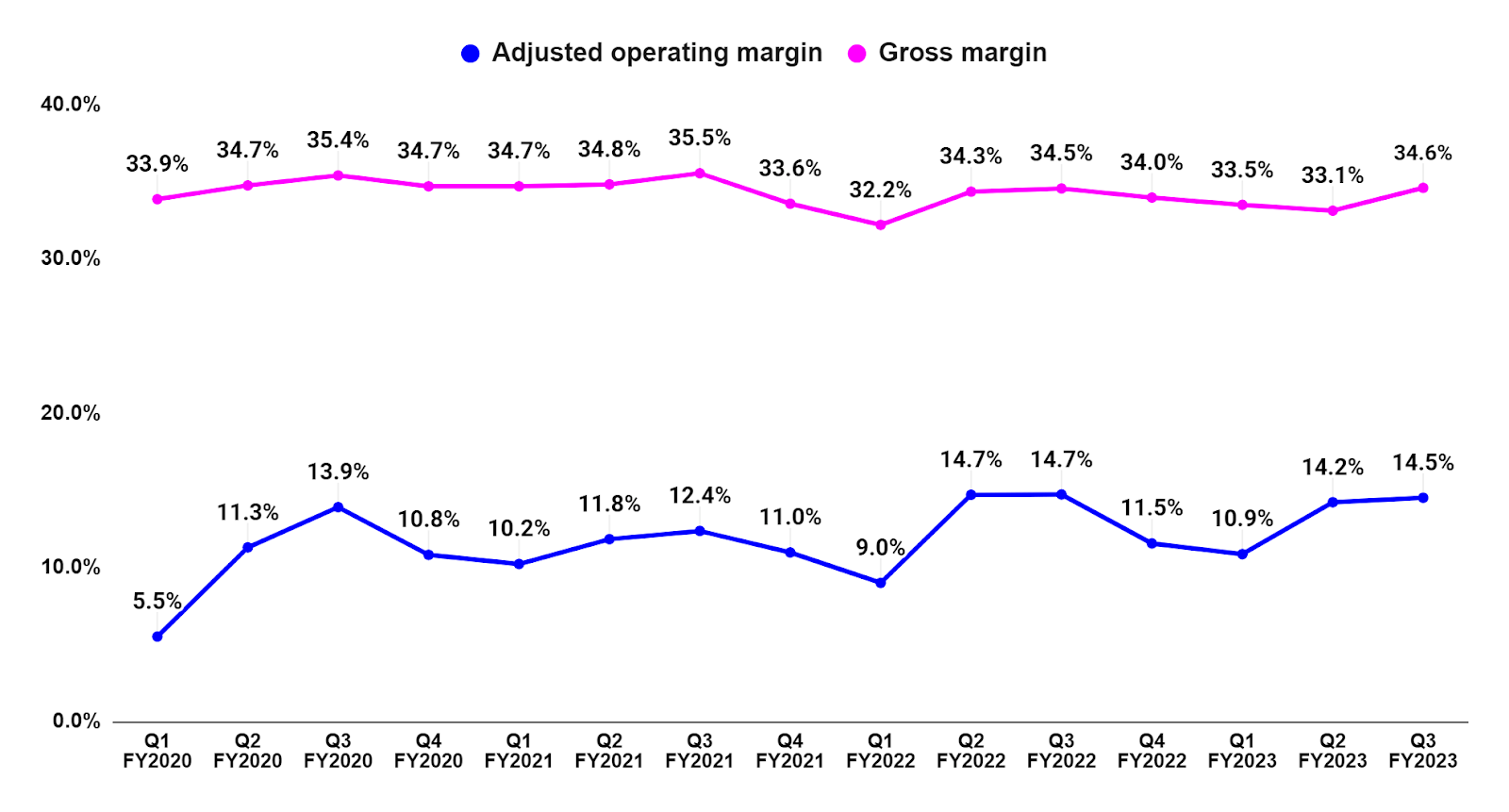

In Q3 2023, the company's gross margin benefitted from higher price realization, favorable product mix, and lower freight costs in the Water Systems and Fueling Systems segments which offset the impact of margin compression from unfavorable pricing of commodity-based products sold through the Distribution segment. This resulted in a 10 bps Y/Y increase in gross margin to 34.6%. However, the adjusted operating margin declined 20 bps Y/Y to 14.5% as the decline in the high-margin Fueling Systems segment revenues negatively impacted the mix.

On a segment basis, the Water Systems and the Fueling Systems segments adjusted operating margin improved by 210 bps Y/Y and 80 bps Y/Y, respectively. On the other hand, the Distribution segment's adjusted operating margin contracted by 420 bps Y/Y due to lower sales and unfavorable pricing of commodity-based products sold through the business.

FELE's Adjusted Operating margin and Gross margin (Company Data, GS Analytics Research) FELE's Segment Wise Adjusted Operating Margin (Company Data, GS Analytics Research)

{kind=link}

{kind=link}

Looking forward, the company's margin outlook is mixed. The company is executing well in terms of cost control and some of the commodity costs are declining, helping margins. However, the outlook for growth in Fueling Systems (which is a high-margin business) remains challenging due to near-term project deferrals and long-term headwinds to traditional gas stations (where the majority of this business is) from rising EV adoption.

The Fueling Systems segment's operating margins are almost double that of the Water Systems segment and four times that of the Distribution business. So, the challenging growth outlook for Fueling Systems will continue to negatively impact the margin mix.

Valuation and Conclusion

FELE is currently trading at a 22.09x FY24 consensus EPS estimate of $4.38, which is at a discount versus the Company's 5-year average forward P/E of 24.81x.

While the valuation is lower than historical, I believe the lower valuation is justified given the near-term challenges with headwinds from the declining backlog, inventory destocking, and project deferrals impacting the near-term revenue growth and the long-term growth challenges in the high-margin Fueling Systems segment with rising EV adoption. So, I believe it would be better to wait on the sidelines till the backlog/order trends start bottoming and there is some visibility on the extent to which the company's EV-related business can offset the secular decline in legacy fuel systems business in the longer term. For now, I have a neutral rating on the FELE stock.

For further details see:

Franklin Electric: Growth Challenges Keep Me On The Sideline