PDM - Franklin Street Properties: Dirt Cheap Valuation Offers Significant Upside

2023-07-27 08:46:36 ET

Summary

- Franklin Street Properties is a beaten-down office REIT that owns 20 quality properties totaling 6.05 million square feet.

- FSP’s office properties - located primarily in growing and attractive Sunbelt and Denver markets - are worth significantly more than the current market valuation of $91 / SF.

- Trading at multi-decade lows and at a significant discount to Book Value and peer valuations, FSP offers an asymmetric risk-reward opportunity.

- Insiders own 6.0% of the company’s shares and have purchased $1.15m of stock in the open market in recent months.

Editor's note: Seeking Alpha is proud to welcome Deep Value Analytics as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

The multiyear selloff in Franklin Street Properties ( FSP ) - exacerbated more recently by its removal from the Russell 600 - has created a buying opportunity for contrarian, deep value investors. With 50% less debt than peers, a valuation of ~$91 / RSF, trading at 1/5 of replacement cost, and trading at just 0.22x P/B, FSP offers a compelling asymmetric risk-reward opportunity. Insiders also believe this is the case and have purchased more than $1.15m of shares in the open market in recent months.

Author Background and Initial Reasons for Interest

Based in Dallas, I’m a full-time real estate development professional and part-time investor. For the past seven years, I’ve been solely focused on single-tenant net lease ((STNL)) developments. Throughout my career, I’ve been involved in the development and acquisition of $3B+ of real estate across most product types (STNL, office, industrial, multifamily). Coincidentally, early in my career, I was involved in the development and lease-up of a North Dallas office property which was ultimately purchased by FSP. I’ve never personally communicated with anyone from FSP, although my increasingly large position as a shareholder of FSP suggests that it would be prudent for me to have discussions with management.

I think the best indicator that a stock is undervalued is when insiders begin purchasing their own stock in the open market. Personally, the most profitable investments that I’ve made over the years have been following insiders. Insider buys coupled with a stock trading at multi-year lows is even better. A grand slam is when an entire industry is getting hammered from negative macroeconomic conditions and investors (and funds) are indiscriminately selling shares because a company operates within a hated industry.

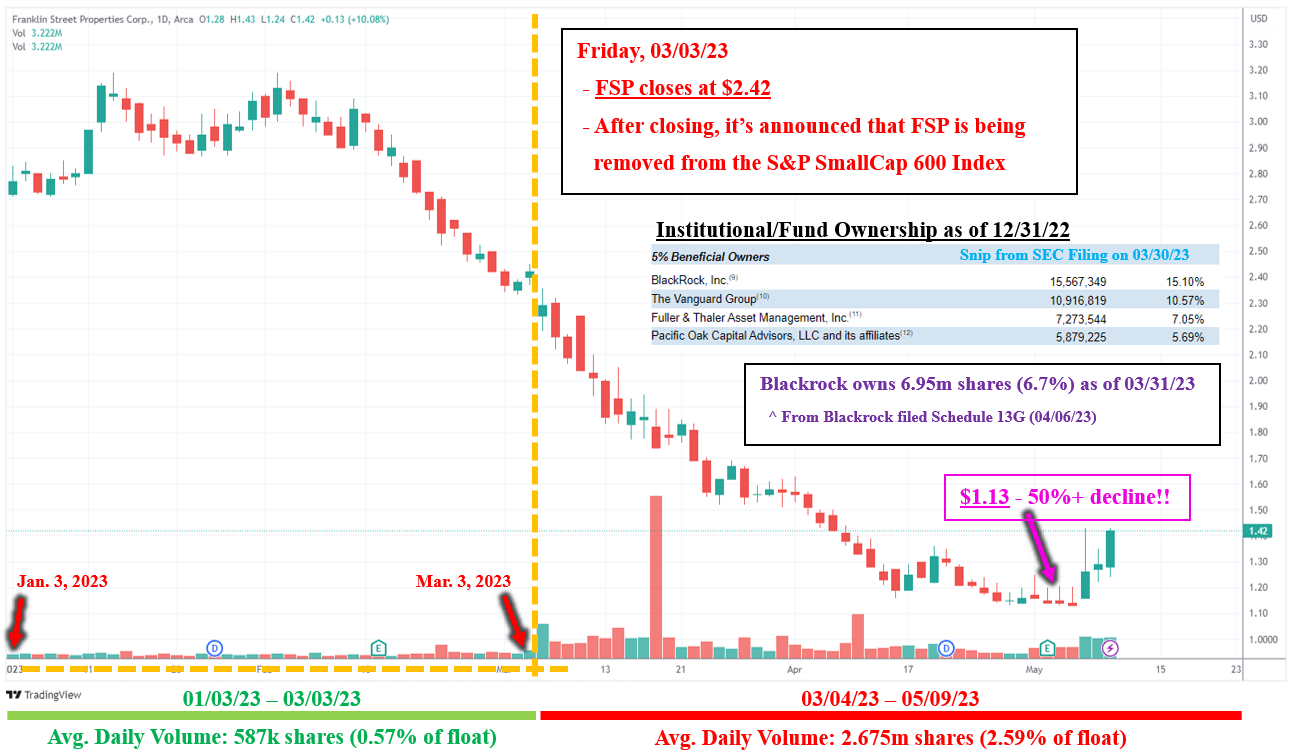

This situation and setup has occurred with the equity value of Franklin Street Properties (“FSP”), a REIT that owns 20 office buildings and was recently removed from the Russell 600 due to the reduction in its market cap over the last year. Since the delisting announcement on March 3, institutional and mutual fund filings have reflected that institutions have sold at least 12M shares (~12% of FSP float); the actual number is likely much higher.

This selloff has created an opportunity for contrarian, patient investors to acquire shares of FSP at current levels and realize gains of 150-300% over the next 1-2 years, perhaps even sooner, taking into account some near-term catalysts which will be discussed.

Because of (i) my personal real estate experience and knowledge of asset values, (ii) the fact that 5 of FSP’s 20 office properties are located in my backyard in North Dallas, (iii) FSP owns four properties in the Denver MSA, a market that I’m very familiar with, and (iv) FSP does not own any properties along the coastal markets (I don’t want office exposure to expensive markets in LA, SF, tri-state area), I decided to dig deeper into FSP. I hope you find this analysis worthwhile.

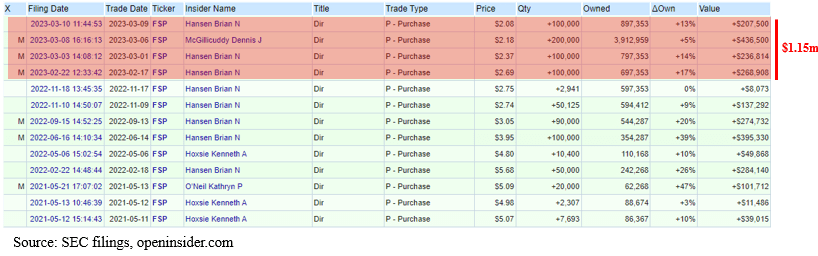

Insider Purchases

FSP first popped on my radar when a screener revealed that FSP insiders had purchased 400k shares ($1.15m) in late February and early March.

{kind=link}

Insiders now own ~6.0% of outstanding shares of FSP. The CEO, George Carter, personally owns over 1.0m shares.

I encourage readers to look at insider acquisitions of the other two dozen office REITs. There have been VERY FEW buys; those that did occur have been small bites ($20k - $50k).

Company Overview

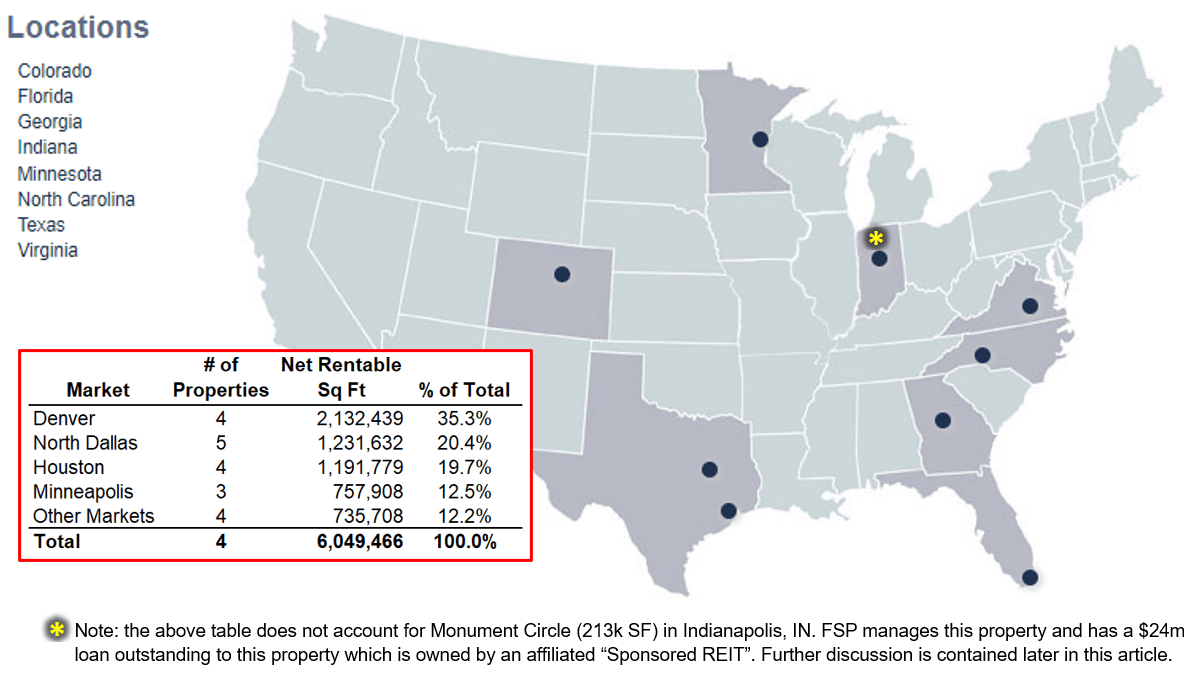

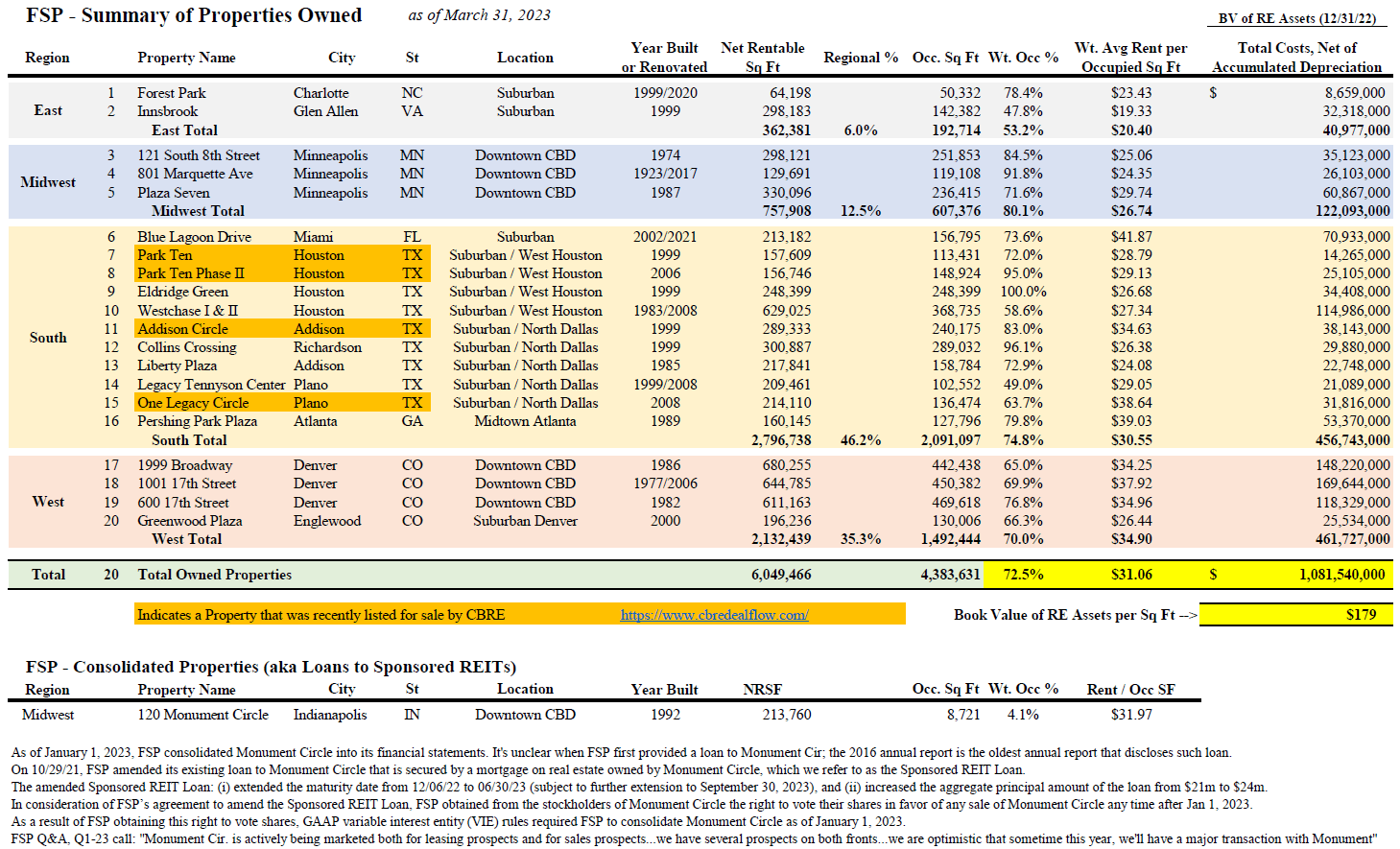

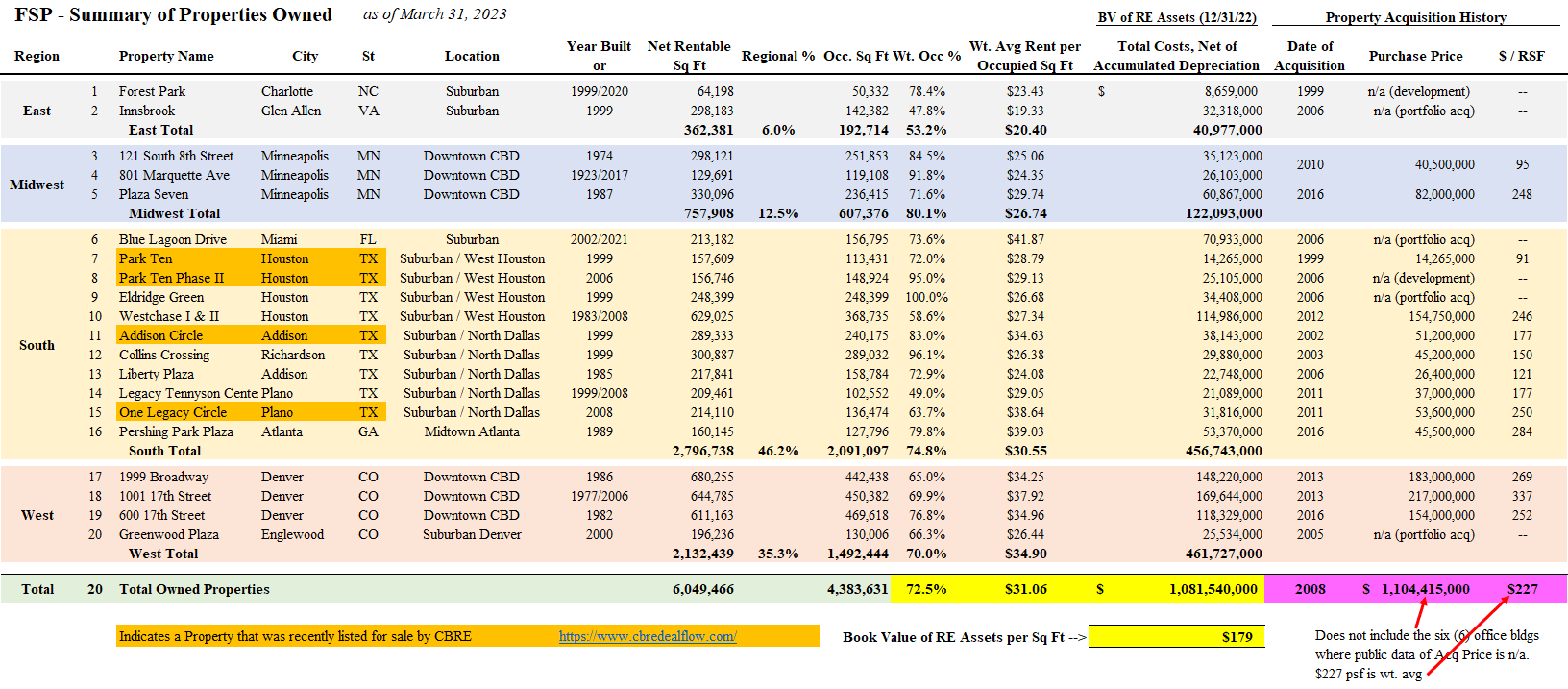

Based in Wakefield, MA, Franklin Street Properties is a publicly traded REIT that owns a portfolio of twenty (20) office buildings totaling ~6.05 million square feet (“MSF”), primarily in the U.S. Sunbelt and Mountain West regions. Its portfolio consists of (i) suburban low-rise (1-3 stories, concrete tilt-up construction), (ii) suburban mid-rise (4 to ~15 stories), and (iii) infill/downtown high-rise office buildings. As of March 31, 2023, approximately 5.3 MSF, or 87.8% of FSP’s total owned portfolio, was located in Dallas, Houston, Denver, and Minneapolis.

Company Images in Presentations Company Presentations

{kind=link}

{kind=link}

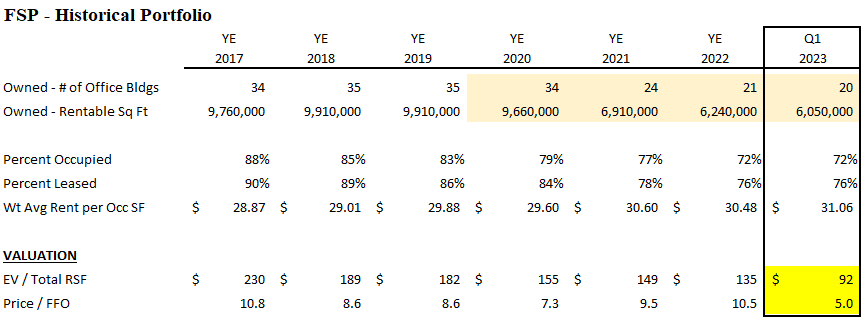

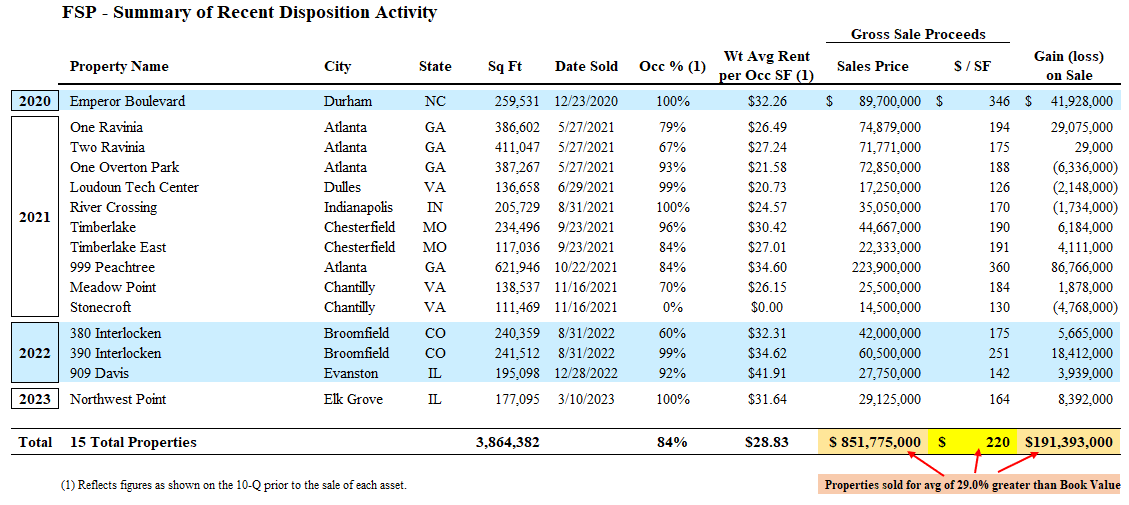

Unlike most office REITs which continued to acquire properties over the last few years and absorb additional debt, FSP management viewed the low interest rate environment as an opportunity to sell assets at attractive valuations and pay down debt. Specifically, since Q4-20, FSP has sold 15 office properties totaling $851m in gross proceeds and paid reduced its debt by 60% (from $1.0B to $398m outstanding, as of 03/31/23). Furthermore, FSP has not acquired a single property since 2016.

Management’s commentary from the Q1-23 conference call :

As the second quarter of 2023 begins, we continue to believe that the current price of our common stock does not accurately reflect the value of our underlying real estate assets. We will seek to increase shareholder value by (1) pursuing the sale of select properties where we believe that short to intermediate term valuation potential has been reached and (2) striving to lease vacant space. We intend to use proceeds from property dispositions primarily for debt reduction.

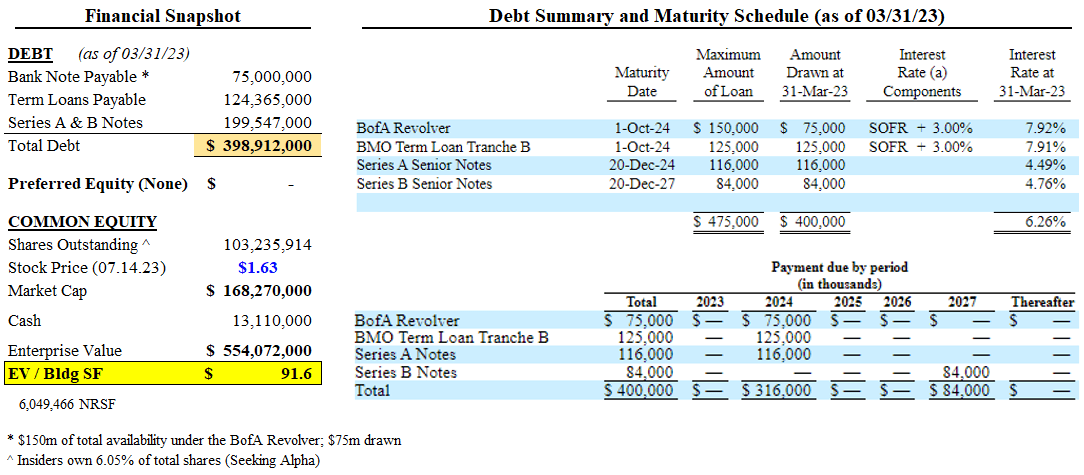

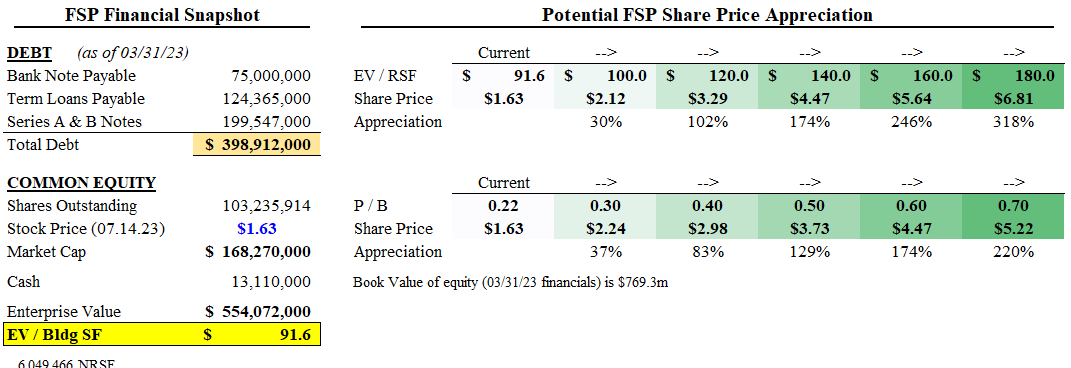

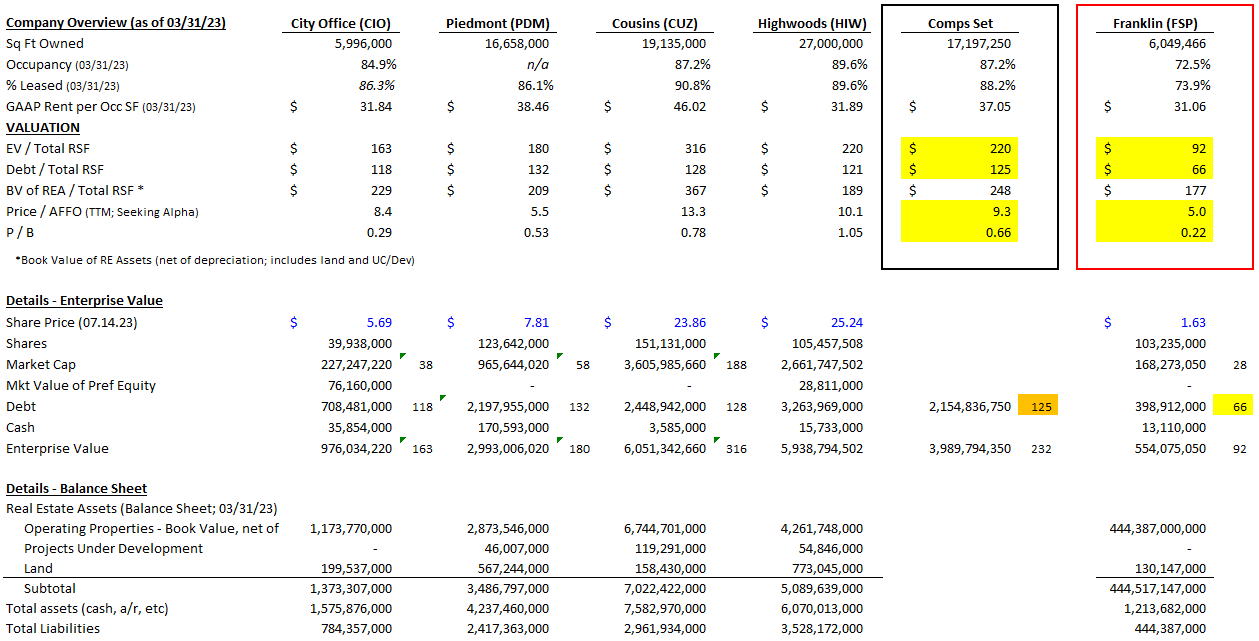

Financial Snapshot and Capitalization

{kind=link}

FSP is currently valued at only ~$91 per Net Rentable Square Foot; meanwhile, its Sunbelt peer set is valued at $220 per NRSF.

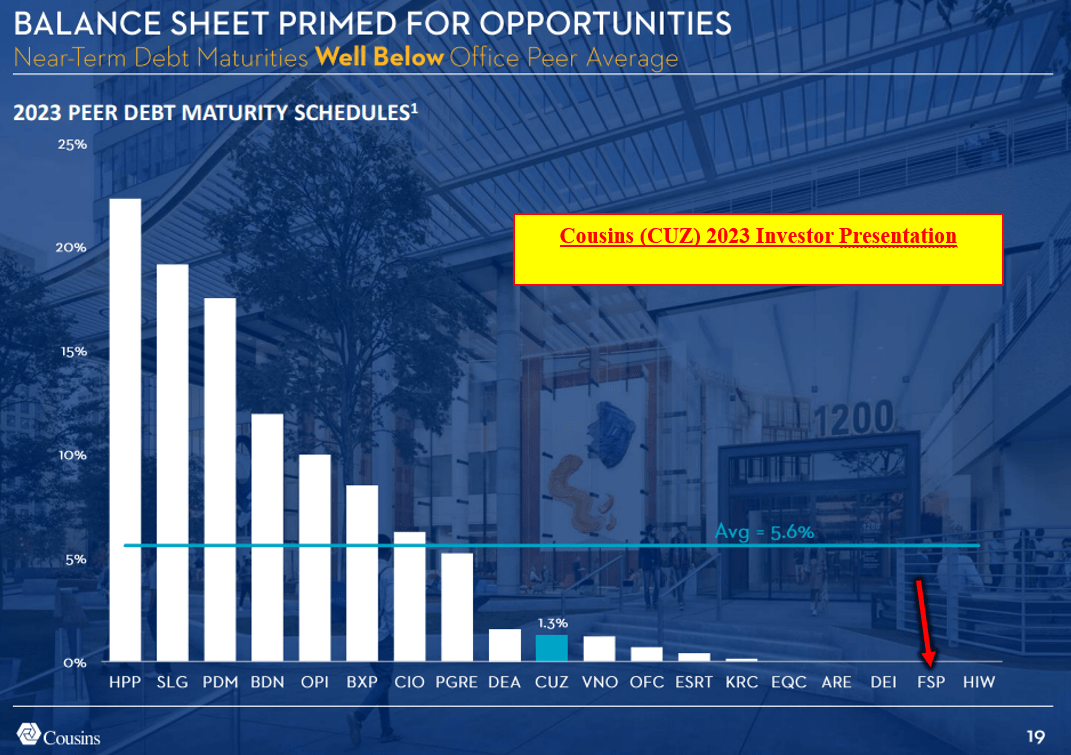

As depicted in the above table and the following slide from a recent Cousins Properties (CUZ) investor presentation , FSP does not have any debt expiring until Q4 2024. FSP management has stated that they’ll continue to use proceeds from property sales to paydown debt. Even if management is unable to dispose of properties over the next 12-15 months (at least 4 of FSP's 20 properties are being marketed for sale; one is currently under contract), FSP shouldn’t have any issues refinancing its debt next year given the relatively low leverage of this debt (~$66 of debt / NRSF).

Cousins Feb-23 Investor Presentation

{kind=link}

Real Estate Portfolio Overview

As of March 31, 2023, FSP’s portfolio of 20 company-owned office buildings was 72.5% occupied and 73.9% leased. The occupancy percentage is nothing to boast about, is less than most of its office REIT peers, and is a primary reason why management reduced the quarterly dividend to a dismal $0.01 beginning in Q3-22 (2.45% dividend yield based on recent closing price of $1.63).

{kind=link}

The weighted average GAAP base rent per square foot achieved on leasing activity during the three months ended March 31, 2023 was $32.87, or 5.7% higher than average rents in the respective properties as applicable compared to the year ended December 31, 2022. Overall, the portfolio weighted average rent per occupied square foot was $31.06 as of March 31, 2023 compared to $30.48 as of December 31, 2022.

{kind=link}

Recent Leasing Update

FSP has realized meaningful leasing activity since 03/31/23. As stated during the company’s Q1 earnings call on May 3: “Subsequent to quarter end, FSP executed approximately 112,000 square feet of leases with new tenants and expansions of existing tenants. The lease occupancy of FSP's directly owned portfolio at the end of April was approximately 75.6%.”

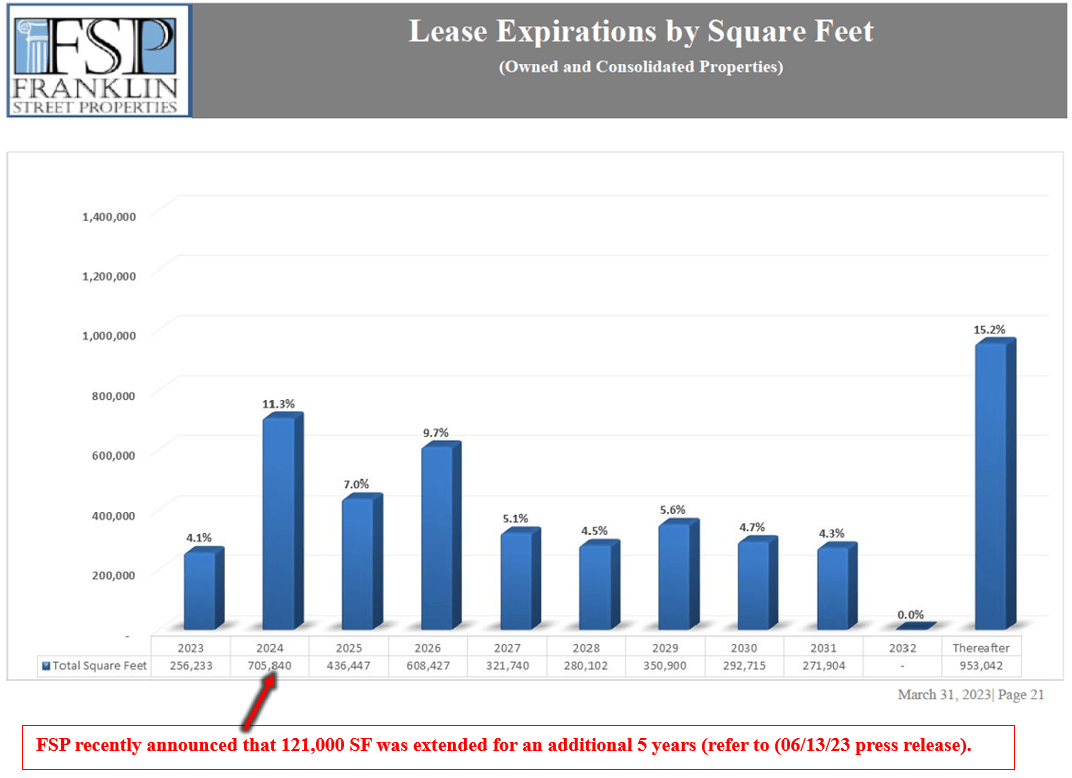

The leased and occupancy numbers should improve further over the coming quarters. In a press release on June 13, FSP announced it has entered into a new lease with a tenant at its Innsbrook property in Glen Allen, VA. The lease is for approximately 100,000 square feet, has a term of 10.5 years and is anticipated to commence during December 2023. In the press release, FSP also announced it has entered into a lease amendment with Kaiser Foundation for its Greenwood Plaza property in Englewood, CO. Kaiser’s 121,000 SF lease was scheduled to expire in 2024; the amendment extends the lease term by 5 years to 2029.

Scheduled contractual lease expirations for the remainder of calendar 2023 total approximately 256,000 square feet, representing 4.2% of FSP's directly owned portfolio.

{kind=link}

FSP's management has stated that leasing of vacant space is a top priority, as this will produce an outsized impact on distributable cash flow and increased dividends in the future. CEO George Carter discusses this topic at the recent annual shareholder meeting :

We are about 75% leased. In other words, we have 25% of our square footage, or about 1.0 MSF vacant and available for lease. For most of our properties, successful leasing of this last mile, 25% of space, can be disproportionately profitable as many fixed costs of a building's operation get effectively borne by the existing 75% lower occupancy in place rental streams. Like any business with substantial fixed costs, higher profits come at the margin. And in FSP’s case, higher lease percentages. And those additional rents will disproportionately flow to the bottom line and improve our FFO metric. Increased occupancies also can meaningfully increase values of individual properties, and maybe most important in these tough office capital markets increase their liquidity to a broader group of potential buyers. We have a significant amount of vacant space to lease and much of that vacancy is in markets that are currently beginning to gain increased traction and momentum, both because of local underlying business demand forces and improving employee post-COVID back-to-the-office trends.

Diversified Tenant Mix

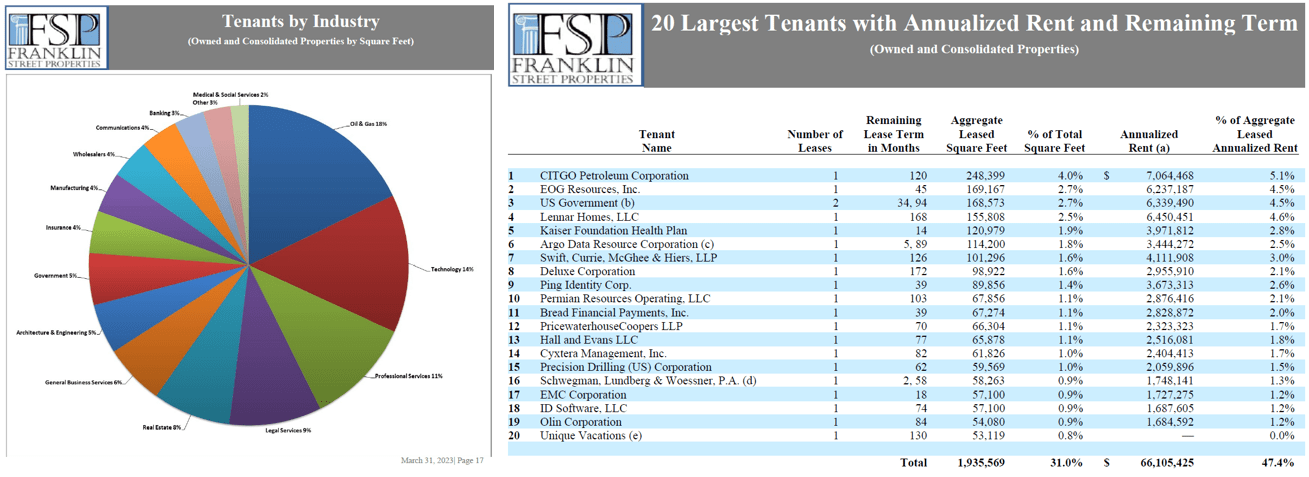

FSP has a well-diversified tenant mix across its portfolio, with no single sector accounting for more than 20% of its tenant base. Furthermore, FSP's top 20 tenants make up less than 30% of the company’s total leased square footage (and 22.1% of total 6.05 MSF). As a comparison point, the top 20 tenants in CUZ’s portfolio comprise 32.9% of total leased square footage.

{kind=link}

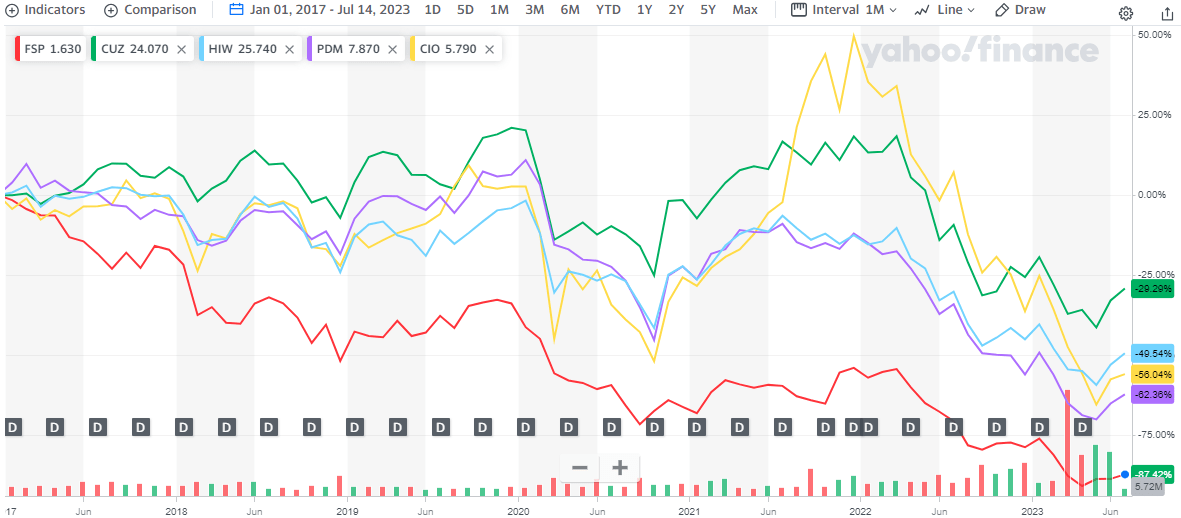

Recent Share Price Selloff

After the closing bell on March 3, it was announced that FSP and a handful of other stocks were being removed from the Russell 600, effective at the end of March. This immediately resulted in institutions and mutual funds disposing of shares. To illustrate this point, avg daily volume over the following two months increased nearly 5x the ADV of the prior two months.

{kind=link}

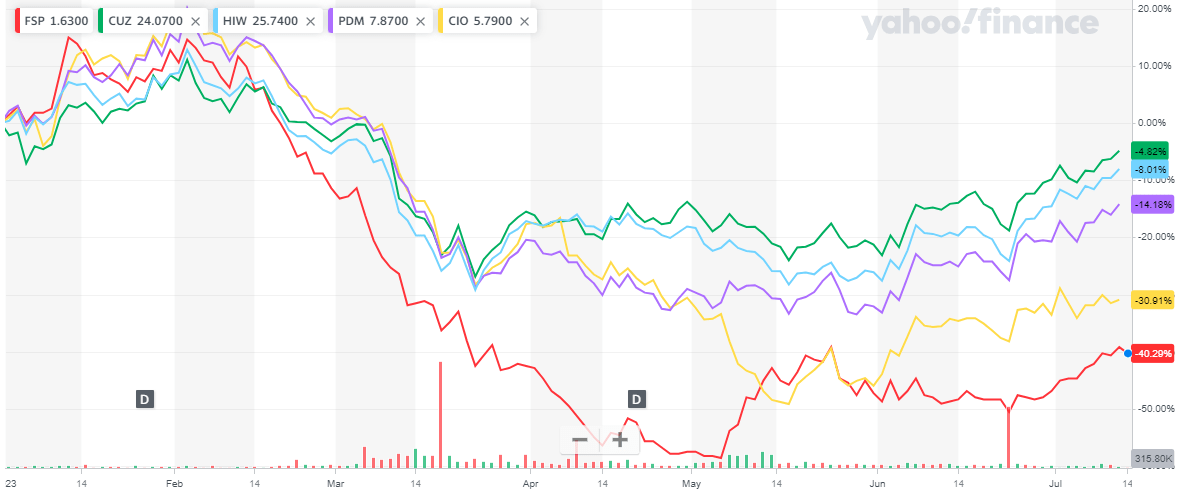

At its recent closing price of $1.63, FSP is now down 40% YTD. This is much greater than its Sunbelt office peers, which have seen their share prices fall 5 – 31%.

{kind=link}

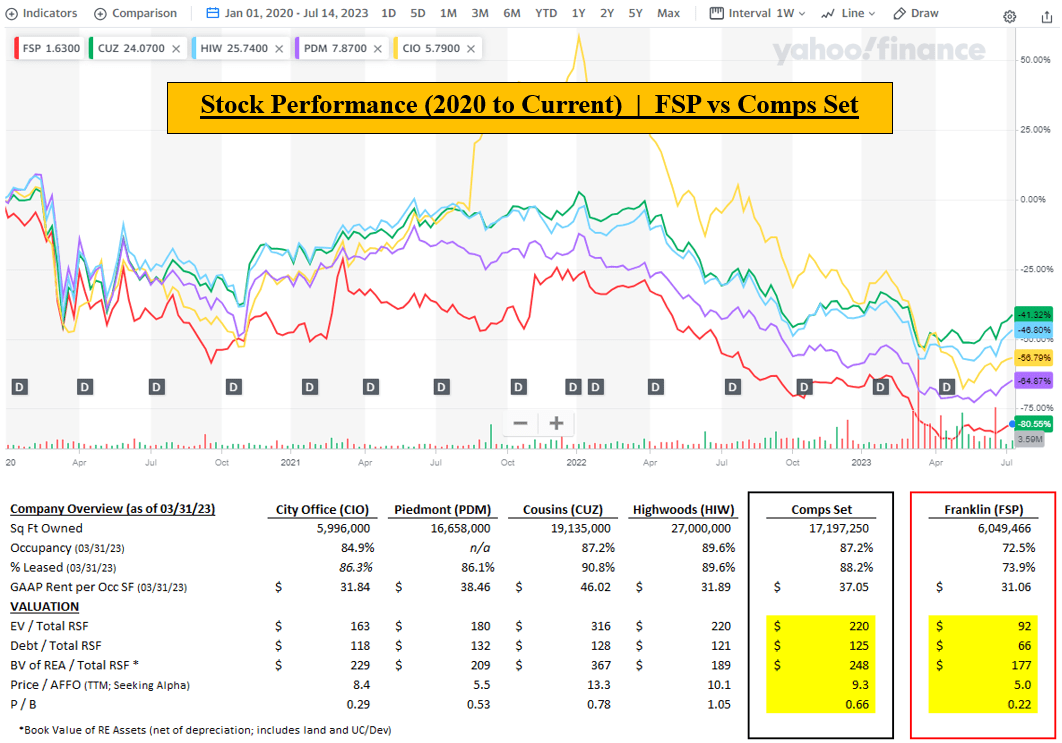

Taking a step further back, the market has punished FSP over the past few years, despite the company cleaning up its balance sheet. FSP only has debt totaling $66/RSF while its peers average debt of $125/RSF.

{kind=link}

Based on every metric, FSP trades at a significant discount to its peers. Perhaps most importantly to value investors, FSP trades at 0.22x the book value of its assets (real estate comprises 88% of FSP’s assets on its 03/31 balance sheet; this is consistent amongst nearly all REITs).

Prudent Management, Strategic Sales, and Balance Sheet Deleveraging

Unlike many of its office peers, FSP did not use the low-interest rate environment of the past 5+ years to continue to grow its portfolio and AUM. FSP has not acquired a single property since 2016.

Instead – prudently, in retrospect – FSP took advantage of the ‘free money’ environment of the past few years to strategically sell a number of its stabilized properties. More specifically, since December of 2020, FSP has completed approximately $851 million in office dispositions and reduced its debt by approximately 60% over this time period.

{kind=link}

FSP sold these properties for an average 29% premium over the book value.

Despite this significant deleveraging, Mr. Market has not rewarded FSP. In addition to the Russell 600 delisting and investors’ recent hatred of office REITs, I believe the company’s poor stock performance is a result of the market placing too much emphasis on FSP’s lackluster occupancy and correspondingly weak Funds From Operations (FFO).

{kind=link}

Valuation - Discount to True Asset Value

{kind=link}

FSP owns 20 office buildings that have a book value of $1.08 billion, or $179 / RSF. This book value reflects depreciation. As depicted in the previous section, FSP sold 15 properties in recent years at a 29% average premium over carrying book value. Now, today is a different market than the low interest rate environment of 2021-22, but I believe FSP’s assets are worth at least the book value of $179 / RSF. Stabilized, well-located office buildings are still selling at healthy “per pound” figures. For example, Highwoods (HIW) recently sold two 100% leased buildings in Raleigh and Tampa for $345 psf and $168 psf, respectively. These buildings were three and two stories (NOT expensive high-rise construction).

Also, it’s worth noting that FSP paid an average of $227 / RSF for its properties, with an average acquisition date of nearly 15 years ago. I know office buildings aren’t in favor and the sector faces its share of headwinds, but what happened to real estate appreciation?!? (slight sarcasm)

If and when the market appropriately realizes the intrinsic value of FSP’s assets, shareholders will be rewarded.

{kind=link}

Valuation - Discount to Peers

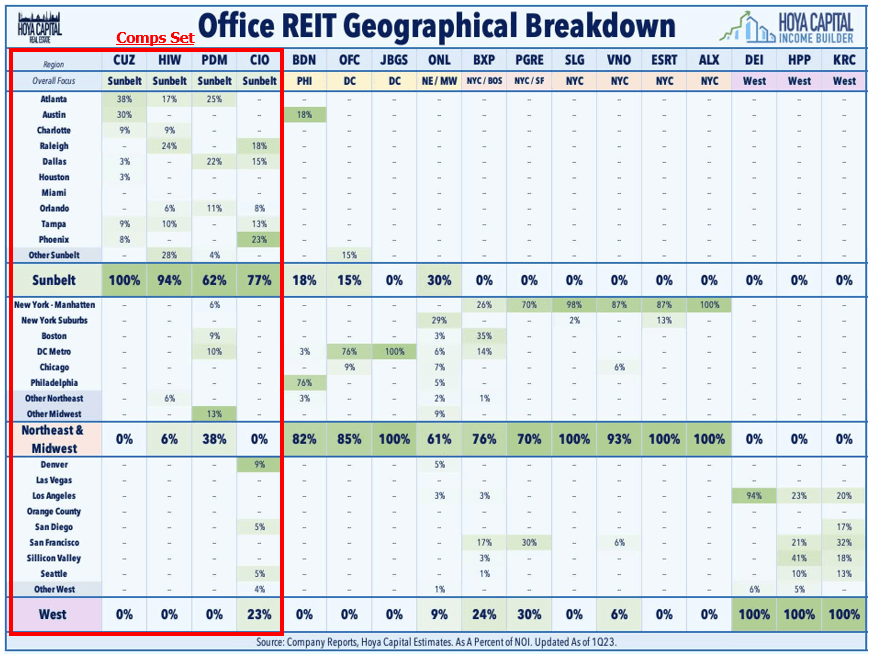

When evaluating FSP vs other office REITs, I wanted to focus on REITs that didn’t have coastal exposure. Office buildings in coastal ‘Gateway’ markets are much more expensive, more susceptible to massive swings in valuation and price, and the return-to-office outlook is not as “sunny” as that of the Sunbelt states.

I added FSP’s portfolio diversification on a graphic that Hoya Capital recently featured in one of its outstanding REIT reports .

{kind=link}

The below graph assesses FSP’s share performance since 2017 vs its peers. Despite prudently disposing of 15 assets and paying down $600m of debt since 2020, FSP has underperformed its peers.

{kind=link}

FSP trades at a significant discount to its peers on nearly every metric.

{kind=link}

Takeaways from table:

- FSP is currently valued at $92 / RSF while its peers have an average EV/RSF valuation of $220 / RSF (2.4x greater than FSP).

- FSP only has $66 of Debt / RSF while its peers all have significantly greater leverage (range of $118 - $132 of Debt / RSF).

- FSP is currently only valued at 0.22x P/B.

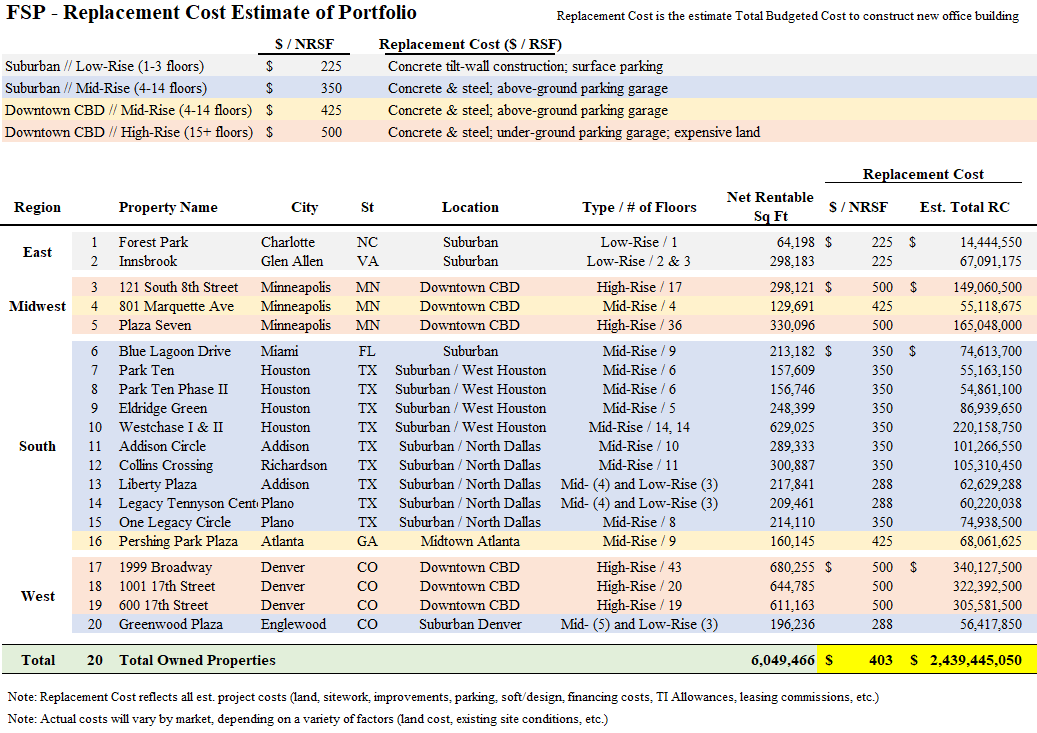

Valuation - Discount to Replacement Cost

Although distinctly different than market value, one common metric used in the commercial real estate industry is Replacement Cost, which is the estimated cost to build a similar building today based on prevailing construction costs. CPI inflation is unlikely to dip below 3% for the next couple years, and construction costs have increased 30%+ over the last five years. I prepared the below table based on my knowledge of current construction costs in the Texas market.

{kind=link}

As an example of current construction costs, it now costs $35k - $45k per parking space to construct an underground parking garage (depending on soils, depth of garage, other factors). Office buildings typically park at 4.0 spaces / 1,000 RSF. Using one of the downtown Denver office buildings as an example, it would cost $84m to construct 2,400 underground parking spaces (600k SF / 4 spaces) at $35k / space. In my opinion, the construction cost estimates depicted in the above table are conservative; actual costs are likely much greater.

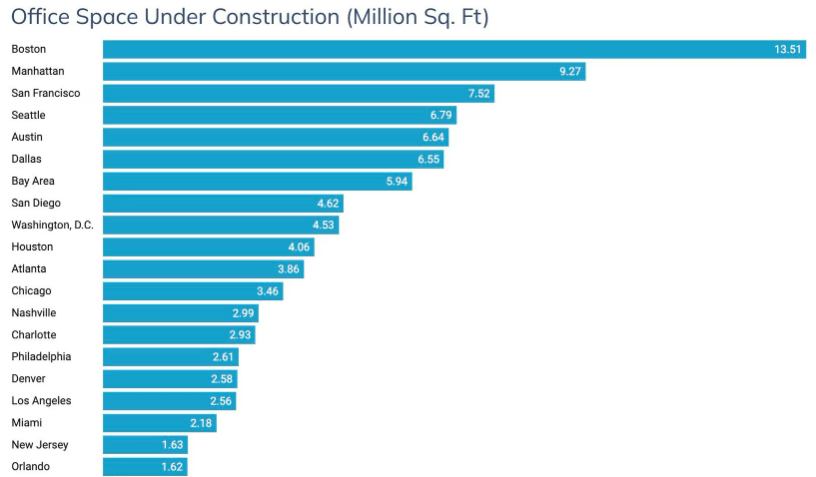

Unless a developer secures significant pre-leasing, new office development is not occurring in today’s market environment. This is a function of (i) economics not penciling due to expensive construction costs and uncertain market rents & demand, (ii) lenders are unwilling to take speculative lease-up & rent risk in this post-COVID environment, (iii) increased cost of capital, and (iv) the general ‘freezing’ of the real estate lending market.

{kind=link}

The above graphic is data as of 03/31/23, provided by Yardi Systems. Nearly all of these projects kicked off in 2021-22. Within DFW, over 30% of the SF under construction is already pre-leased.

Near-Term Asset Sales?

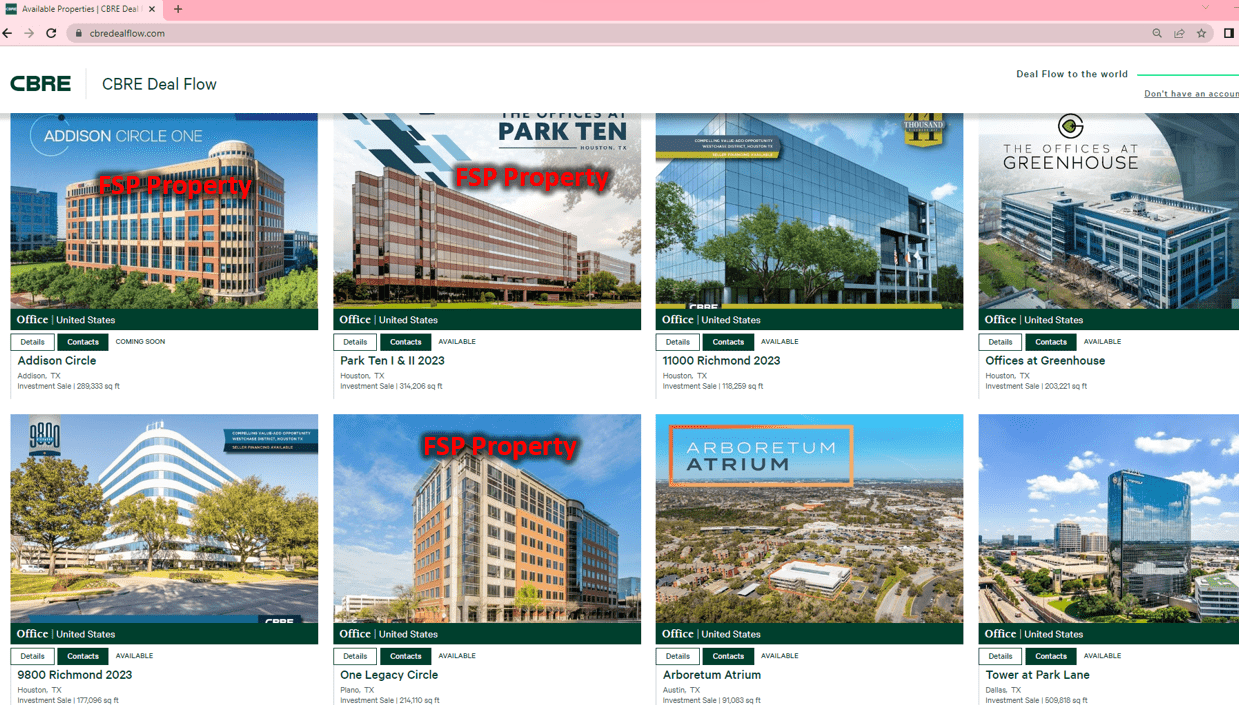

At some point over the last year, FSP management decided not to share details regarding planned asset dispositions. Some office REITs continue to be transparent with their dispositions, while others have taken a 'silent' approach like FSP management.

Despite FSP’s lack of transparent communication regarding disposition of specific properties, I discovered that FSP has engaged CBRE to market & sell at least four (4) of FSP’s 20 assets for sale. I discovered this simply by going to CBRE’s website and searching for office properties for sale in Texas. Below is a screenshot.

{kind=link}

It’s possible that FSP is attempting to sell additional stabilized assets in other markets (Blue Lagoon in Miami is a likely candidate), but I haven’t come across such info.

Risk Assessment

Like all office REITs, FSP faces the following risks, among others:

- Lease Expirations – as referenced earlier, FSP has fewer leases expiring (total RSF and as % of total leased SF) in 2023 and 2024.

- Ability to Lease-up Vacant Space

- Inability to Sell Office Buildings and Paydown Debt

- Increased Financing Costs 12+ months from today, when debt needs to be refinanced

With regard to all of the above risks, I believe FSP is in better position than its office REIT peers - particularly the office REITs that do not have Sunbelt exposure. Perhaps most importantly, FSP only has debt totaling $66/RSF (while its comp set has debt of ~$125/RSF). FSP's debt doesn’t mature until Q4-24, and it can be easily refinanced in 2024 after the lending market normalizes.

Conclusion

The multiyear selloff in FSP - exacerbated more recently by its removal from the Russell 600 - has created a buying opportunity for contrarian investors who understand the value of FSP's assets. With properties located in Sunbelt markets with strong fundamentals, trading at just 0.22x P/B and with a current EV / RSF valuation of $91 / RSF, FSP offers a compelling asymmetric risk-reward opportunity. Insiders also believe this is the case and have purchased more than $1.15m of shares in the open market in recent months.

For further details see:

Franklin Street Properties: Dirt Cheap Valuation Offers Significant Upside