FSP - Franklin Street Properties: Still Cheap Even After Reversal

2023-10-10 09:38:54 ET

Summary

- Franklin Street Properties' common stock prices are trading much lower than the worth of its underlying assets.

- The decline in share prices is not isolated to FSP, but is industry-wide for office REITs due to the pandemic and increasing interest rates.

- FSP's estimated equity value is multiple times higher than its market share, providing investors with significant upside.

Franklin Street Properties (FSP) is a REIT focused on office properties in the U.S. that is currently trading much lower than its book value. Even though the share prices increased over 50% from its recent lows earlier this year, the share still offers significant upside. In our analysis, we will try to show that the common stock prices are still much lower than the worth of underlying assets.

Why is FSP down?

Even though the share price recently increased from its lows, the share price is still down over 75% over a 5-year span and over 90% down from 2005 when the stock first started trading publicly .

{kind=link}

When comparing the share price with other office REITs over a 5-year period, it becomes clear that the problem is not isolated to FSP, but industry-wide. Office REITs in general suffered quite a bit, especially in the last few years, when the covid-pandemic accelerated the shift to home-office and increasing interest rates are putting further pressure on real estate.

As a result of declining cash flows, FSP decided to lower its quarterly dividend from $0.09 to $0.01 in 2022, which also had a negative impact on sentiment around the share price.

As Deep Value Analytics pointed out in their recent analysis of FSP (a great analysis IMO!), the reason for a further sell-off of the shares is the delisting of FSP from the S&P SmallCap 600. This resulted in a steep decline in price and an uptick in volume over the next few trading months, indicating increased selling activity from institutional investors as a response to the delisting from the S&P SmallCap 600.

FSP valuation

When trying to define a fair value for FSP's total assets, it is obviously most important to find a fair value for FSP's real estate holdings. FSP currently holds 21 total owned and consolidated properties. The total square feet for all properties are 6,270,658, 73.3% of which are currently leased.

FSP's recent disposition activity (FSP Q2 2023 earnings release)

{kind=link}

First, we are going to look at the real estate holdings FSP has disposed of since December 2020, in order to find a fair valuation for the other real estate FSP is still holding as of now. We assume that using these recent dispositions as a benchmark, we can accurately analyze how much value FSP is adding to their properties and also only factoring in properties that are already hit with post-covid pessimism regarding office spaces.

Price per Square Feet of recent dispositions (Asset Alchemist)

{kind=link}

Since December 2020, FSP has sold 15 properties across the U.S. Through these sales, the company has achieved total gross sale proceeds of $851,775,000 and an average sale price per square feet of $221.45. After all these dispositions, FSP's real estate holdings currently have a total square footage of 6,270,658. Applying the average sale price per square feet we calculated, we can come up with a very rough value of ~$1.39b for FSP's remaining real estate holdings.

In the last quarterly results , the company announced the upcoming sale of one of its properties and also has entered into purchase and sale agreements for three other properties. For these four dispositions, if successful, the average price per square feet would be ~$250, putting them even higher than the average of the previous dispositions since December 2020. This further reinforces that our current estimate of $221.45 per square feet is not optimistic. Our fair value estimation of ~$1.39b for FSP's real estate is over 25% higher than its book value of ~$1.08b as of the company's Q2 2023 release. As we can see with FSP's recent disposition, the company was able to book a gain on the sales compared to the properties' book value in most of the cases, which justifies the assumption that fair value of the company's real estate holdings is higher than the book value.

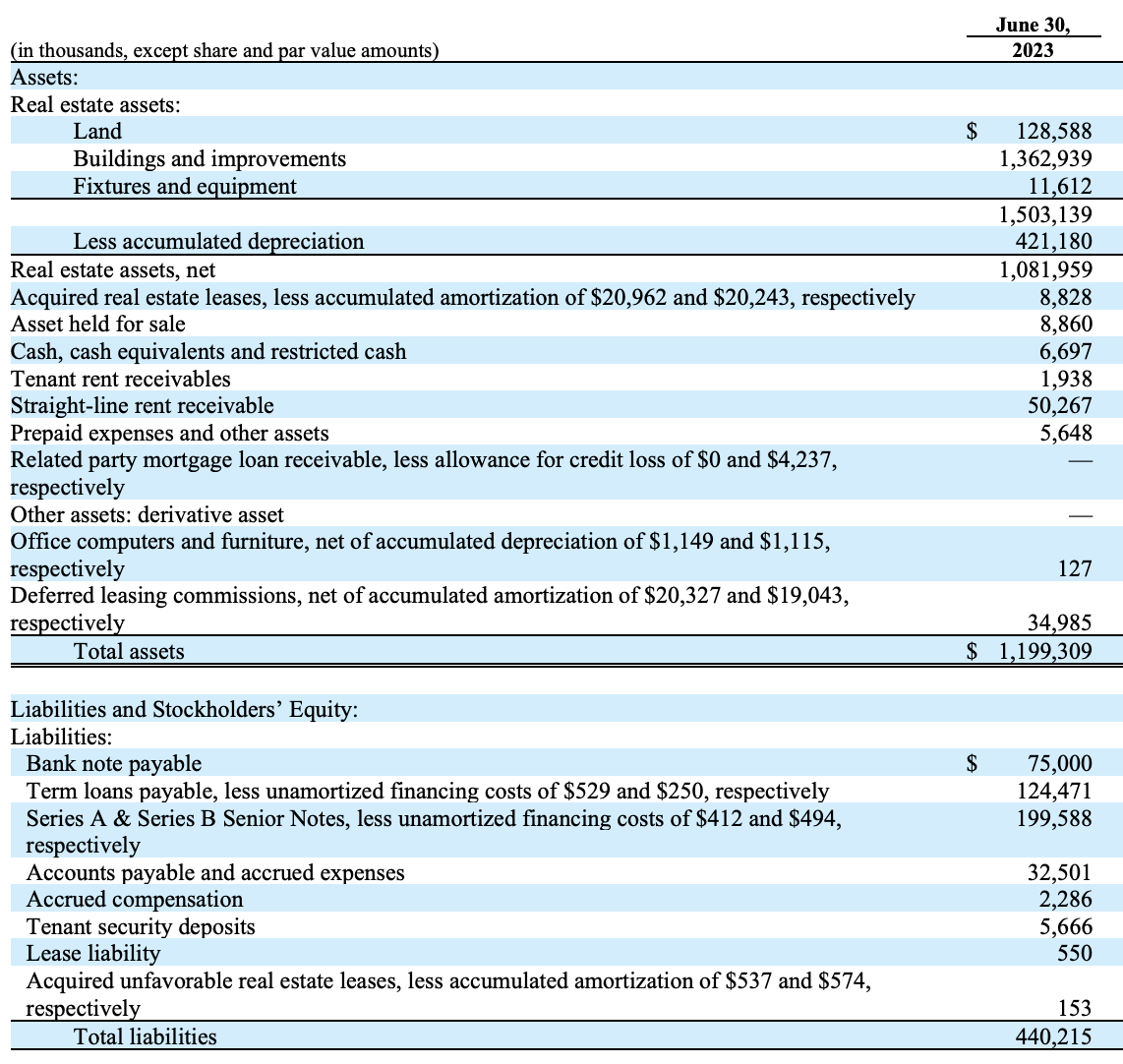

FSP Balance Sheet (FSP Q2 2023 earnings release)

{kind=link}

Assuming the book values of all other assets (like rent receivables) on the company's balance sheet is equal to their fair values, we estimate the fair value of the company's total assets to be ~$1.5b. With total liabilities of ~$440m, we estimate the net value of the company's assets to be ~$1.06b.

With Funds From Operations (FFO) of $15.5m for the six months ended June 30, 2023 the company's operating business could also add to the company's valuation. For our analysis' purposes, we will assume a pessimistic case, that the ongoing operations of FSP have a value of $0 and only focus on the company's assets, and assume that ongoing business funds will be used to pay expenses and dividends only.

Closing the gap

With our estimated fair value for the company's equity of ~$1.06b and a current market cap of ~$185m, the question remains, whether or not investors will ever see the gap between equity fair value and share price close.

In the last quarterly result FSP's CEO had the following opening comment:

(...) we continue to believe that the current price of our common stock does not accurately reflect the value of our underlying real estate assets. We will seek to increase shareholder value by (1) pursuing the sale of select properties (...) and (2) striving to lease vacant space.

In the same quarterly result , the company has also announced expecting to close on the sale of their Forest Park property for $9.2m and entering into sale and purchase agreements for three other properties for ~$152m. Adding these planned sales to the dispositions the company has already performed since December 2020, it shows the legitimacy of management's claim looking to increase shareholder value by pursuing the sale of properties.

Regarding the lease of vacant space, we will continue being pessimistic in our analysis and assume no further value creation by leasing vacant space.

Using the proceeds from property sales to pay down company debt, FSP could free up over $22m yearly in interest expense and also become more flexible in the future when it comes to returning capital to shareholders or funding growth initiatives.

Based on management being aware of the discrepancy between the common stock and the underlying assets and taking specific steps to address the issue, we expect that management will be able to further close the gap of the common stock price since the lows earlier this year and continue unlocking value. Due to the low debt, FSP should not be thrown into the same basket as other, highly leveraged, REITs.

Even if we assume a worst-case-scenario of management being able to get the common stock price to reflect a value of just half the fair value of the company's equity (so ~$503m), we can set an approximate price target of almost 5$ per share - upwards potential of almost 180%.

What to look out for

In the following quarters, we should mainly look out for the success of the planned property sales. Further successful sales and repayment of debt are strong positives. Any increase in vacant space could put the company's positive FFO at risk, which is why that is an area of concern in the next coming quarters. An increase in leased space on the other hand would be a great bonus, reinforcing the buy-rating for the stock.

Given the big gap between equity value and common stock prices, any plans to buy back shares or increase dividends could also have a great, positive, impact on share prices. For the next couple of quarters, we should closely follow any comments and plans management is making regarding the issue of common stock not accurately reflecting equity prices.

Conclusion

FSP's common stock prices are down due to a mix of circumstances. Based on our analysis, and also management's opinion, the current common stock prices do not accurately represent the fair value of the company's equity based on their real estate holding.

Based on our pessimistic assumptions, a change in the company's share price to a point where it represents a return to only half of our estimations for equity fair value, would already mean returns of almost 180% for the common share. Investors should closely monitor all measures the company is taking regarding closing the gap between equity value and share prices.

Editor's Note: This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Franklin Street Properties: Still Cheap, Even After Reversal