FPRUF - Fraport: A Growth Story That Bleeds Cash

2023-03-21 16:11:32 ET

Summary

- Fraport faces significant cash outflows as it fuels big construction projects that will pay off in several years.

- Dividend likely to remain suspended until these projects start returning cash.

- 2023 should be a lot better, but the EBITDA guidance range is too broad for a comfortable buy.

I have been looking at airport stocks as a way for investors to capitalize on growth in air travel demand. In my view, airport stocks provide some better stability than for instance airlines with the risks to the business being the economic indicators supporting air travel demand and maintaining a diverse and attractive portfolio of airports to operate. As I discuss in this report, Fraport (FPRUF) is currently going through a cash-intensive period that renders the company unable to pay a dividend but its business is recovering nicely.

How Do Airports Make Money?

So, how do airports make money? It is basically two revenue streams; the first one is aeronautics revenues that include landing and departure fees, passenger charges, terminal space rentals, security and aircraft parking. The second stream is non-aeronautical revenues which include things like car parking, car rental, ground transportation, retail, food and beverages and fast track.

So, there are two revenue streams that are well-suited to capitalize on the travel rebound. On one hand, we have airlines increasing their flight schedules again, which benefits the airport via aeronautical revenues. On the other hand, the passengers are returning to the terminal halls, and they have money to spend, which benefits the commercial revenues which form a big portion of the non-aeronautical revenues.

So, as an airport, to make money, you have to appeal to airlines providing smooth operations and offer travelers a unique experience.

Fraport Operations: Which Airports Does Fraport Operate

Fraport's cash cow is Frankfurt Airport, but the company has a portfolio of airports in Greece such as Corfu, Kos, Santorini Zakynthos and Rhodos that obviously perform strongly on leisure travel during the summer as well as the airport in Antalya, which it jointly operates with TAV Airports and the airports in Varna and Bourgas which feed the Sunny Beach tourism. Furthermore, in South America, there are the airports of Fortaleza and Porto Alegre in Brazil and Lima in Peru while via Fraport USA retail space is being marketed in some US airports.

Fraport: Pace In The Recovery

{kind=link}

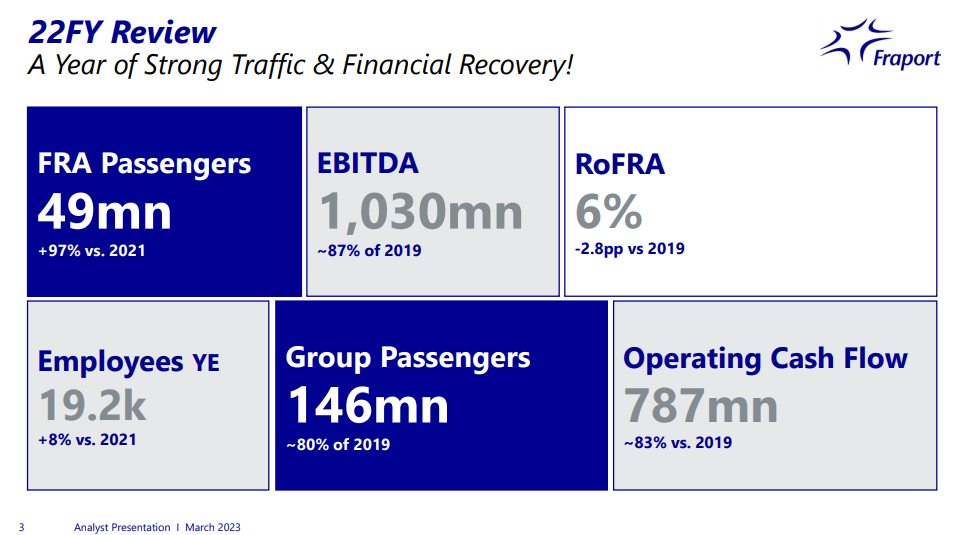

Year-over-year, we saw that Frankfurt passenger volumes nearly doubled while the group passenger volumes are 80% recovered. A positive here is that EBITDA is down "only" 13% while passenger volumes are still down 20%. However, what should be noted is that EBITDA in 2022 was positively impacted by one-off items such as a gain on sale of €54 million for the stake in Xi'An airport that has been sold, a €23.6 million settlement agreement for Fraport Greece, portfolio rebalancing activities yielding €19 million for Retail & Real Estate and €34 million in costs for ground handling provisions. If we include all effects, the actual recurring result was €948 million showing that adjusted EBITDA was actually recovered in line with the group passenger volume. So, there is pace in the recovery but part of it is driven by one-off positives.

The positives are that EBITDA for the Greece airport portfolio is exceeding 2019 levels by 60% on stable revenues, so that is something where investments are already paying off. Furthermore, Antalya airport is showing stable results. I'd say that most of the recovery has to come from Frankfurt Airport which has remained pressured for a longer time due to the Omicron variant as well as operational constraints. A positive there is that we see spend per passenger up 1.5% for the year compared to 2019 and fourth quarter spending was up 12.5%.

{kind=link}

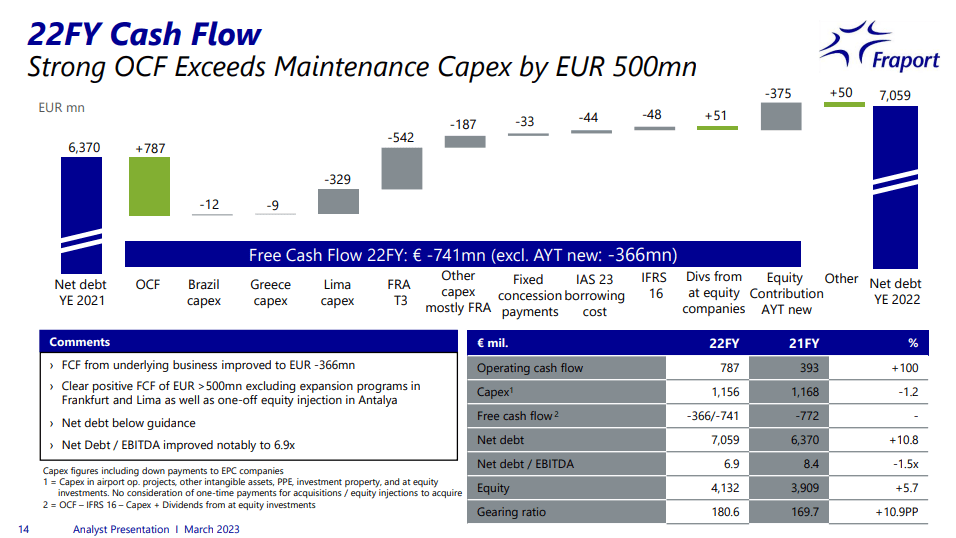

Operating cash flow grew year over year and in fact doubled. However, what we do see is that CapEx is exceeding the free cash flow. That is driven by the project in Lima, which is big project with a new ATC tower, taxiways, runways and a new terminal while a new runway will be constructed. This will allow for a capacity of 40 million passengers, and from 2025 until 2041, Fraport, which has an 80% stake in the operations, will be paying the dividends for that investment. Similarly, there was €542 million in CapEx for the construction of Terminal 3 in Frankfurt, which should start paying off by 2026. There is still €2 billion in CapEx, which will mostly be spent this year and next year. For the new Antalya Airport, there was a €375 million CapEx which was a one-off item. These three projects are significantly inflating the cash outflow but should pay dividends once completed. So, through 2025-2026, there is some increased CapEx, but those investments should start paying off around the same years as well.

As a result of the cash burn, net debt increased, but its leverage improved, and while cash burn is expected to continue this year, I do believe that the long-term trajectory for deleveraging is positive with stable leverage in 2023 and maybe even slightly better when the high end of the 2023 guidance is met with sufficient liquidity to cover financial liabilities towards 2026.

{kind=link}

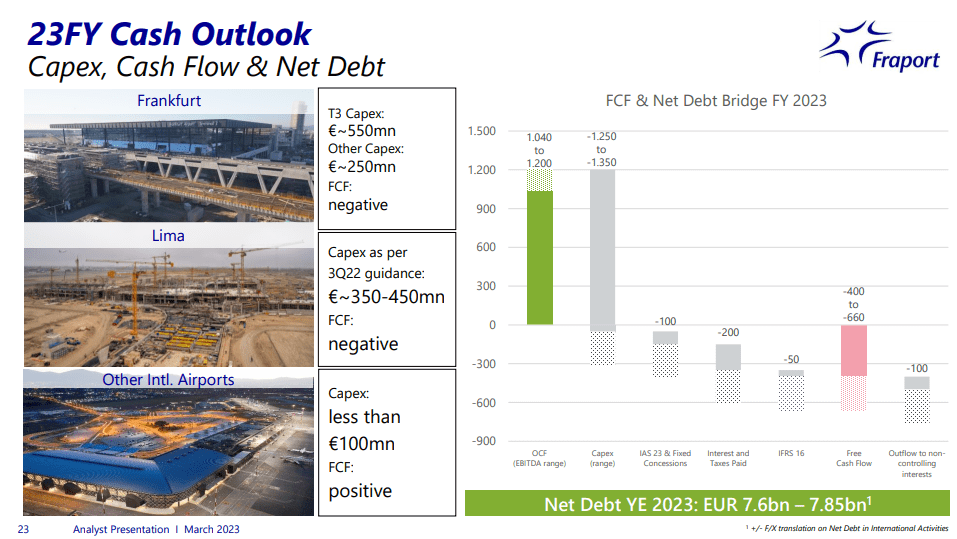

For 2023, at Frankfurt, the seat capacity will be 80% recovered on continental level where Eastern European operations remain pressured due to the absence of flight connections with Russia and Ukraine, but international seat capacity and movements will be 90% recovered. So, for Frankfurt, we should see a better year in 2023. The cash intensive projects, namely Lima and T3 at Frankfurt, will see similar cash burn as in 2022, but Frankfurt other CapEx will be up. Overall, the net debt is set to further increase. Free cash flow will be slightly better than in 2022, but it will still be negative. EBITDA is expected to be in the €1.04 billion to €1.2 billion range with net debt in the range of €7.6 billion to €7.85 billion, implying a leverage of 6.3x to 7.3x. So, while I am hoping for stable and even slightly better leverage year-over-year, the guidance implies that it could also be a bit worse this year, but these are driven by project expenditures that drive future cash flow and EBITDA generation while the leverage is projected against the current EBITDA generation expected. So, you don't see the profit accretion these projects will have in the future.

Due to the CapEx heavy years, there is no dividend payment for 2022 and also not for 2022 and I doubt we will see one in 2024 as the CapEx will be more or less the same, but beyond that I do believe that a dividend will be reinstated as projects start paying off the investment.

Conclusion: Fraport Stock Works On Future Shareholder Returns

Fraport is investing significantly in the future and I do believe that should positively impact earnings from 2025 onward with some demand-driven expansion in EBITDA in the years to come. However, cash outflows will keep a dividend on the sideline for now. As a result, I am marking shares of Fraport a Hold. Partially also because I am not too sure whether headcount reductions in Frankfurt to cut costs is the preferred path that allows for sustained growth.

For further details see:

Fraport: A Growth Story That Bleeds Cash