FSNUY - Fresenius Medical Care: Attractive Post Crash Maintaining A 'Buy' Rating

2023-03-21 11:54:39 ET

Summary

- What to "BUY" in this time of absolute turmoil is something to be carefully considered. I try to focus on undervalued, qualitative opportunities. These exist in every sector.

- Fresenius has long been a position of mine. In this article, I seek to update what's happened to the Medical Care wing, with the FMS symbol.

- I've long been bullish on FMS, but favoring investing in the native FRE or ADR FSNUY, for the "full" company, as opposed to only part of it.

Dear readers/followers,

Fresenius ( FMS ) (FSNUY) will be a sort of turnaround play - as many of my more successful investments throughout my history have actually been. Fresenius Medical Care is part of Fresenius in a way, but it's also its own company, namely the focus on dialysis and overall kidney care.

Kidney care is a massive treatment area - and FMS is at the forefront of it in one of the more attractive geographical areas in the world. While this should theoretically mean attractive potential returns, a combination of COVID morbidity, management issues, and deteriorating margins as a result of some of these factors has resulted in the company seeing the worst earnings in many, many years.

In this article, I will showcase to you why despite BBB-, despite a 2.5% yield and despite some headwinds yet to conquer, Fresenius Medical Care is on my "BUY" list (although FSNUY/FRE should be higher on yours).

Fresenius Medical Care - The upside is becoming clearer

Now, as I said - I own FSNUY/FRE now, FMS. The key difference here is that the former has access to all of Fresenius's attractive business areas, while FMS is focused on one, namely Kidney care.

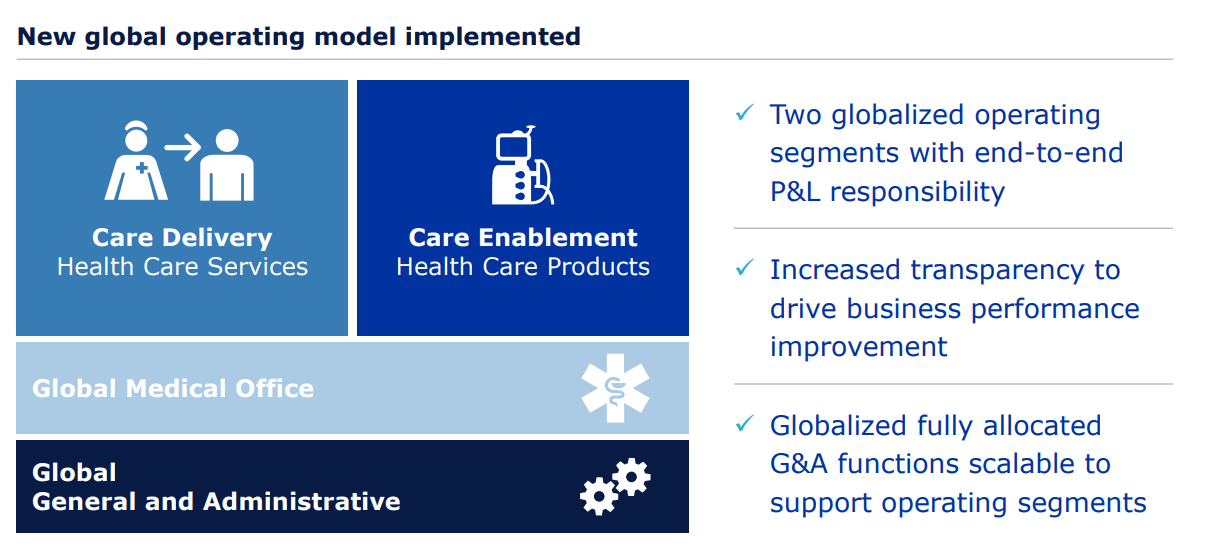

This is not a bad thing to focus on. With its two global operating segments, Fresenius Medical care provides both healthcare services through its delivery segment, and care enablement through its healthcare products.

{kind=link}

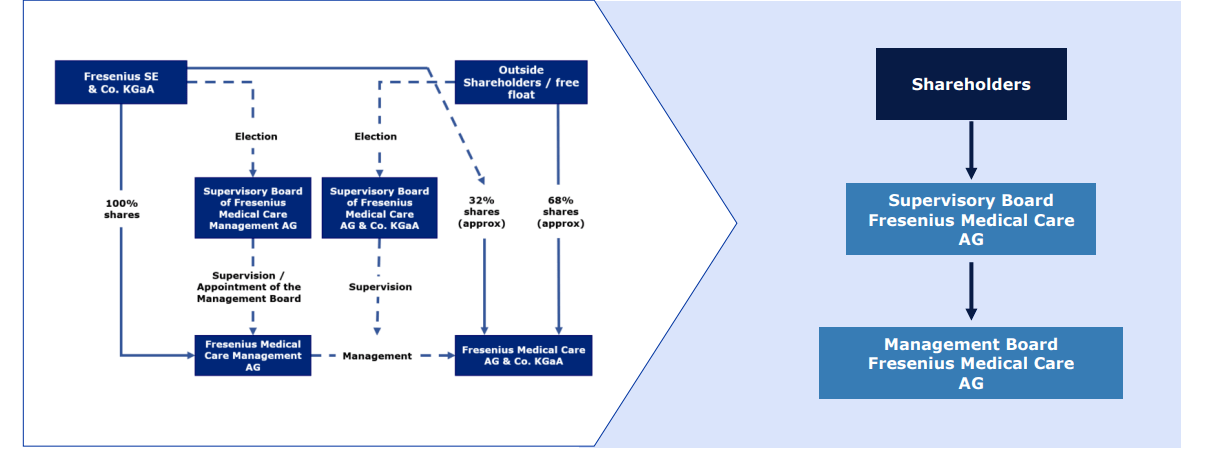

The company's simplified operating structure is on display in the latest quarter and for the full year, as part of what will be driving further company profitability and advantages. While usually, such changes are mostly on the surface, due to FMS's complex ownership structure, there are a few changes worth noting.

First off, the company's simplified governance structure will finally enable the rights of free-float shareholders somewhat more, and the simplified leadership structure will enable faster decision-making while preventing potential conflicts of interest. The company will also convert to a so-called German Stock Corp by the end of 2023, which will bring about many of these changes. A simple illustration by the company provides us with a very good explanation for why things are going to be simpler.

{kind=link}

It's hard to imagine any one company holding on to this complex sort of operating structure - but if any one company is going to do it, that company is going to be European, and more specifically German.

Company targets are as follows going forward in the next few years.

- Delevering the company's balance sheet in expectation of further interest rate hikes. This should have been done long ago, but FME is hardly alone in having been playing a bit "fast and loose".

- Restoring the dividend and earnings after its recent 17% DPS cut due to massively impacted company performance in 2022.

- Digesting what M&A's it has done, while focusing on not doing further ones, and focusing on organic growth above inorganic ones. A sound point, as I see it.

The timeframe for the realization of all of these advantages, which should see results in the next few years, comes to a close in 2025E, currently. This is a combination of operational efficiencies and portfolio optimization, including rationalizing the clinic footprint, exiting non-core markets which are unsustainable for the company, but also focusing on R&D, removing product lines that aren't conducive to the company's growth, and overall efficiencies.

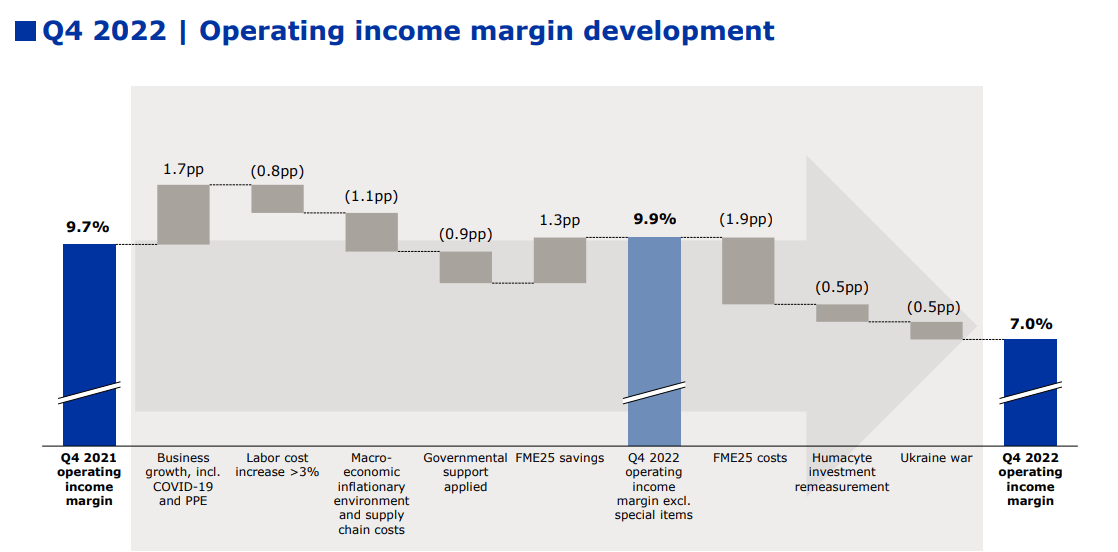

4Q22 and FY22 wasn't the best year for the company. While revenue actually grew 8% YoY, and 2% at constant currency levels, company's operating income took an absolute nosedive with a 22% decline, and 28% at constant, and nearly 40% drop in net income even without constant currency.

Why was this so bad?

A few factors:

- Labor Costs

- Staff shortages

- Inflationary cost increases of supply

- Overall supply chain issues

- Continued COVID-19 impacts.

What's more, it was largely the international segments that drove organic growth, with EMEA and APAC being major contributors, as well as seeing higher sales of in-center disposable supplies, with most everything else in sales down. The margin bridge looks something like this.

{kind=link}

The company's negative income situation has contributed to a vastly negative leverage situation, where the company's debt is close to the high level of the target corridor of 3-3.5x, at 3.4x.

2023 isn't expected to see any massive amounts of improvement here - we're expecting significant headwinds from inflation as it continues to ravage the market. Also, labor costs are expected to remain high. The government isn't going to be stepping in and making things easier for FMS either, and the dialysis, due to a combination of morbidity levels and market trends overall, is expected to more or less be completely flat.

This comes to the company expecting an up-to high single-digit revenue decline.

{kind=link}

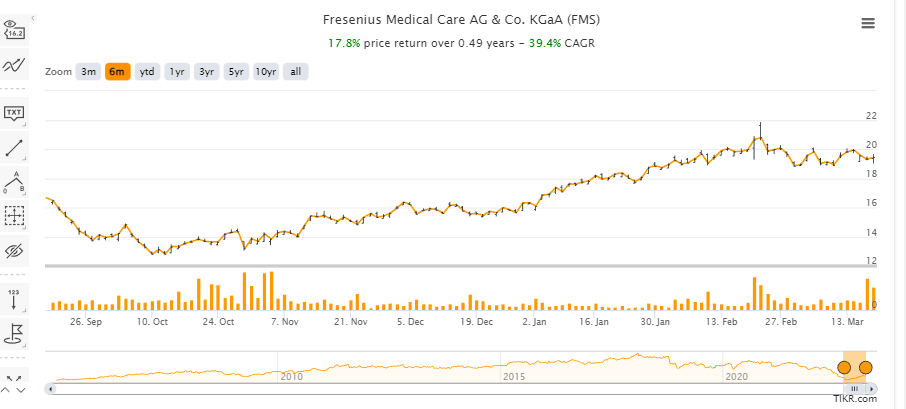

The company's share price is down 42.9% in a single year - but it hasn't seen a massive decline in the latest 6 months as other companies have. In fact, over the past 6 months, the company has outperformed index by quite a bit. This works with my overall assumption that we might have found the trough in the company's valuation.

{kind=link}

In terms of what we should be keeping an eye on, there aren't any surprises as to that. Because so much seems to hinge on the payoff of the company's initiatives, those initiatives and the more gradual payoffs expected here are what we need to look closely at.

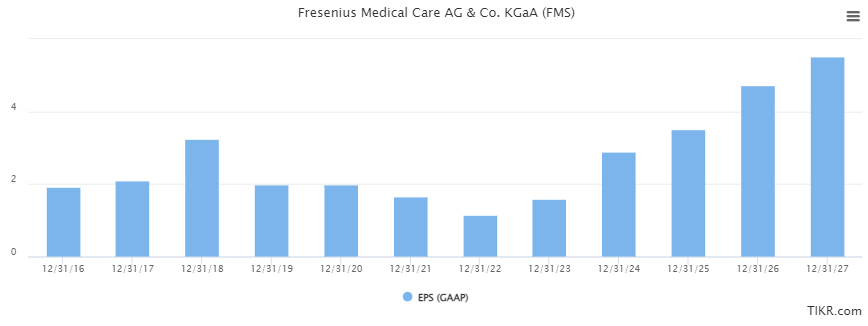

There are some reimbursements coming in this year that should slightly improve the numbers for the year and the coming 3 fiscal, as well as the patient growth recovery. But overall, it will be some years before we see a full recovery toward growth, and 2023E seems very likely to be another "downer" year as things seem to be looking now. In terms of GAAP, I expect either flat or only slight growth for FMS, followed by slow growth in earnings as we move forward - about 5-8% per year. The analysts following FMS are more positive than I am about this.

{kind=link}

If they are right about this, FMS could be nothing less than the investment opportunity of a lifetime in this sector. Overall realization of the valuation if this EPS becomes realized in 2027E would entail a massive growth rate and return.

Let's look at exactly how good things might be if this actually comes to pass.

Fresenius Medical Care - The potential upside is massive

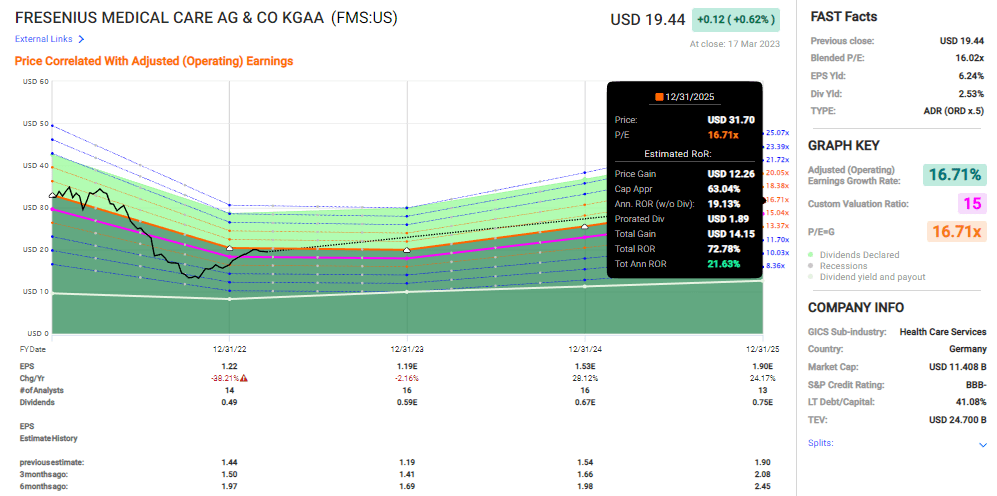

That is because the company is expected to realize significant amounts of growth in 2024-2025 and beyond, the valuation implications here are significant. If FMS manages to push these sort of earnings in the next coming years, and the valuation multiples remain at the 15-17x P/E range, then your returns could be as high as over 20%+ per year, or over 72% in less than 3 years.

{kind=link}

Of course, this requires that we keep a very close eye on the KPI's that FMS ends up reporting on a quarterly basis. Any of these growth or efficiency initiatives not reporting as expected would dim this return picture somewhat, and result in less-than-expected RoR.

Because the company is significantly worse fundamentally than Fresenius itself, I continue to view FMS as an inferior investment pick to the main company. That is even with the governance and structure in place. Fresenius also comes with the safety of diversification, which is not to be underestimated in this case, especially since some of those arms actually are doing very well (read my Fresenius articles for more details on those, and why you should consider this instead of investing in FMS).

However, for those wanting a more clear-cut investment avenue into dialysis and kidney care, FMS is the way to go. The company is set to be a market leader in an area with attractive growth potential and plenty of patients. While its leverage is not great, it's also not massively high, and I don't view it as something that you really need to worry about. The yield isn't superb, but the capital appreciation potentially in the investment makes up for that, as I see it.

What's more, analysts are still seeing Fresenius as undervalued. Out of 4 analysts, 2 are at "BUY" or equivalent for the stock, and they work from a PT range from $10.45, which is far too low, to $32, which would be fair overall, if the company realizes some of this upside. The average if $20.7, which means that at just south of $20/share, the company is still somewhat undervalued here.

Fresenius Medical Care has no direct peers - not for its specific segment that I would consider relevant to view as publicly traded comps. We could put it next to healthcare equipment suppliers, and find it in storied company like Philips, Baxter ( BAX ), Becton Dickinson ( BDX ), and Stryker ( SYK ) as well as Medtronic ( MDT ) - but doing so would incorrectly value the segment of its care arm. Valuing it as a pharma company definitely does not work, and valuing it as an industrial conglomerate or general healthcare also seems to skew the multiples, compared to where other companies in the same segments are trading.

Fresenius Medical Care is hard to compare to other companies. We can use DCF, provided we account for the high growth rate and normalize it properly after, which I would do at 4-6% with a discount rate of at least 11%. This brings us to a Fair value range of $18-$24/share, with an average of around $22/share, which also implies undervaluation.

I believe between conservative forecasts, conservative DCF, and the company's own historical and where it might go given just a "base" case performance, there is enough upside in Fresenius Medical Care to warrant a bullish view and a "BUY" rating on the company.

But I wouldn't do my job if I didn't point out that Fresenius itself has a higher upside, and comes at a similar yield, but with better fundamentals.

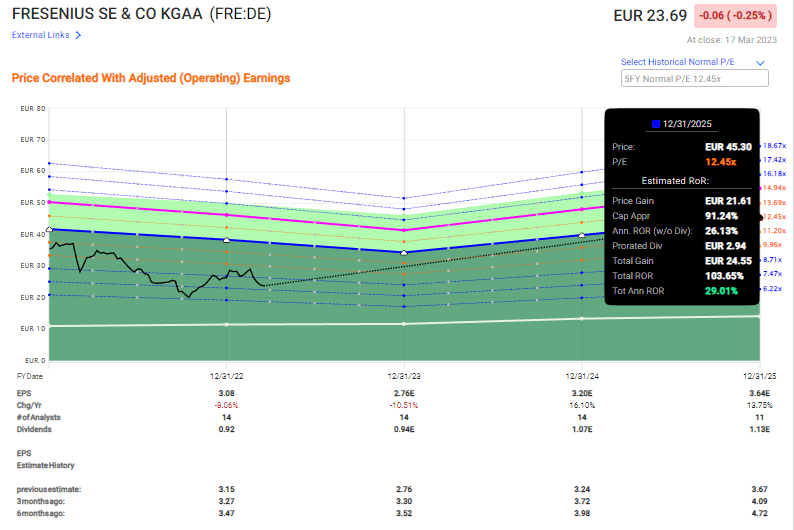

FRE, the native Fresenius tricker, trades at a €23.7/share price, yields over 3.5%, and trades at a multiple of around 7.8x. It will see similar levels of prospective growth but isn't as volatile as FMS. The upside even just based on a 12.5x forward P/E, while also being rated BBB and not BBB-, is significantly higher than for FME, going into the triple digits.

{kind=link}

Obviously, you'll have to choose which avenue is right for you here, but I want to make a clear case for Fresenius, which seems to my eyes be the far superior investment to go for here.

FMS is a "BUY" - and so is FRE. Here is my thesis for FMS.

Thesis

- I view FMS as a solid company to buy. It's a leader in the kidney care sector and owns large parts of the dialysis operations in the US market as well as on an international basis. It's BBB-rated, has a decent yield, and has a near-85% upside going forward to the next few years.

- However, due to the corporate structure, governance, and the appeal of its "parent", I consider Fresenius to be the superior investment if comparing the two. FMS is a "BUY", and it has upside - but FSNUY/FRE has a better thesis.

- I give FMS a PT of $34/share for the long term and rate it a "BUY".

Remember, I'm all about : 1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Because the company fulfills every single one of my criteria, it is a "BUY" to me here.

For further details see:

Fresenius Medical Care: Attractive Post Crash, Maintaining A 'Buy' Rating