FSNUF - Fresenius Medical Care: Don't Let The Ozempic Kidney Failure Scare You Off

2023-10-12 13:29:16 ET

Summary

- Fresenius Medical Care (FMS) and Fresenius (FRE) stocks have experienced a decline due to the Novo Nordisk drug Ozempic ending a kidney failure study early.

- FMS remains a good player in the dialysis field and is not fundamentally impacted by the Ozempic report.

- FMS has the potential for significant improvement in the next few years, with a low-mid single-digit growth in revenues and a slight decline in EBIT forecasted for 2023.

Dear readers/followers,

I've been covering Fresenius Medical Care ( FMS ) and Fresenius ( FSNUY ) for over 2 years at this point, mostly holding a positive view on both stocks and viewing the companies as investments with good upsides. My preference, due to the lack of dialysis concentration/diversification has been the general Fresenius ticker, natively listed under the FRE ticker on the German stock market.

FMS is a fair investment potential here that can be viewed as an alternative to FRE. With the latest decline, some investors might ask themselves if my thesis on the company has changed materially, or if there are worries or information worth considering or including in the thesis here that means we should expect a decline.

In short, I would say that is not the case.

Let me show you my reasoning for continued upside in both FMS as well as Fresenius as a whole.

Fresenius - Update after the Crash

So, the reasoning for my update here is the latest crash in dialysis companies after the result of the Novo Nordisk ( NVO ) drug Ozempic ending a kidney failure study early due to results meeting efficacy data expectations/requirements from independent monitors. Ozempic is the company's GLP-1 drug, and Novo has been pinning a fair bit of hope on the drug for the future. As a result of this, dialysis companies which work on the other side of this area, are dropping double digits. Businesses like Baxter ( BAX ), FMS, and Outset Medical ( OM ), dropped double-digits, with onset dropping the most at 21% in a single day.

Fresenius Medical Care is up today after an 18% drop but has obviously lost much of the upside that has been confirming my long-term thesis for the company. It's still up compared to the earliest of my articles on FMS, but significantly less than the market. At least for now.

Fresenius and Fresenius Medical Care is, I would say, not fundamentally impacted by this report. Other players like onsets are getting the worse end of this stick, being smaller - but Fresenius remains a good player in this field, whether you choose to go via the Medical Care or the general company route.

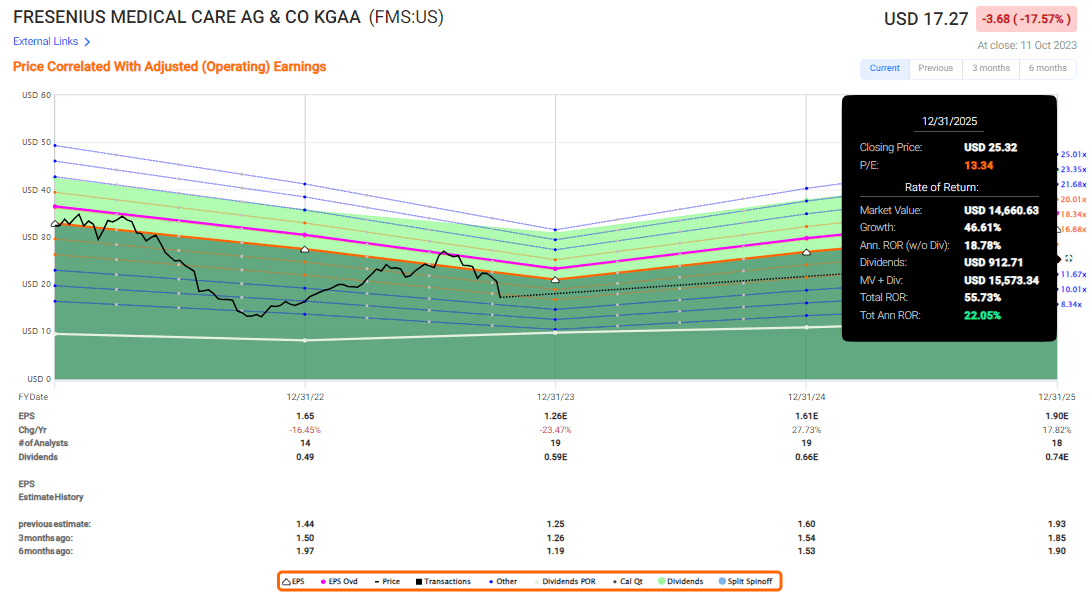

I said in my last article that FMS is not an easy company to invest in. This has been proven true at this time once again. The company's results during and after COVID-19 have not been a pleasant read, with 2022 declining nearly 16% on an adjusted EPS basis, and 2023E is set to decline a massive 64% on an adjusted EPS basis. (Source: Fresenius 2Q23 )

The market cap for FMS is now less than $12.3B with a BBB- rating from S&P Global. The dividend yield, based on the 2022A yield is around 2.4%. To say this sounds attractive would be false.

However, the kicker lies in the upside we see in the next few years after the 2023E trough actually passes.

Unlocking the value is the theme of FMS, and this change will take time - to 2025E at the very earliest. The company's priorities are ROIC improvements and disciplined capital allocations, moving and working within its new global operating model with improved governance, which is a positive. (Source: Fresenius 2Q23)

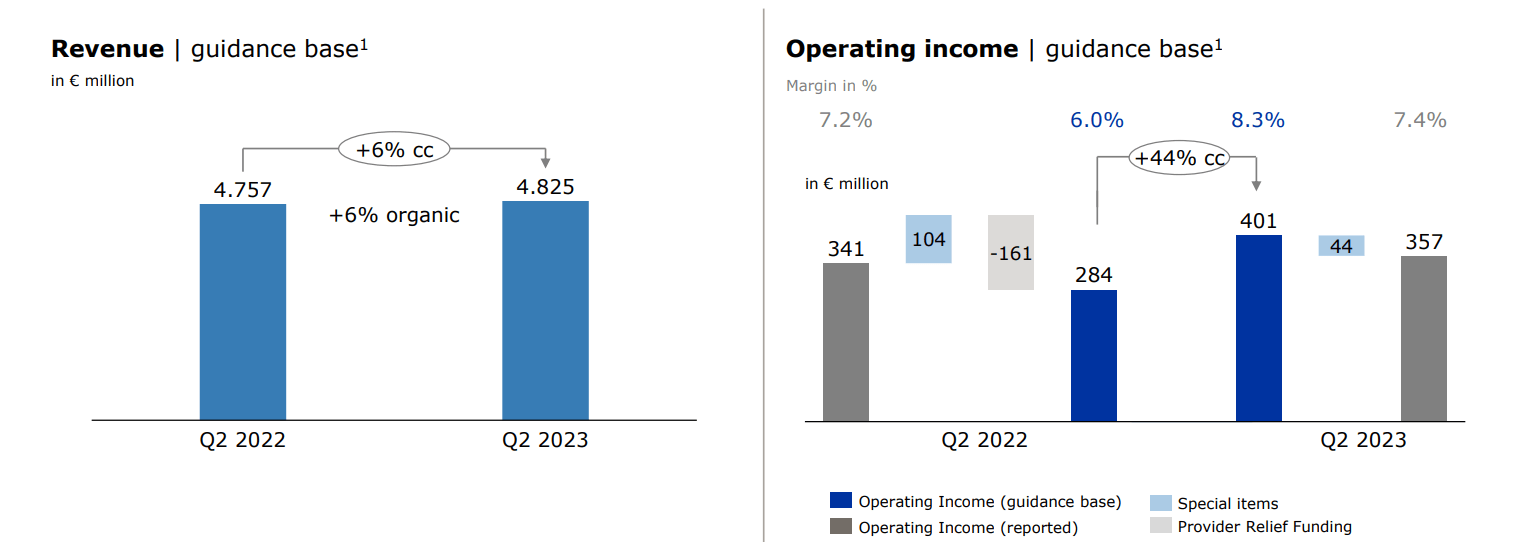

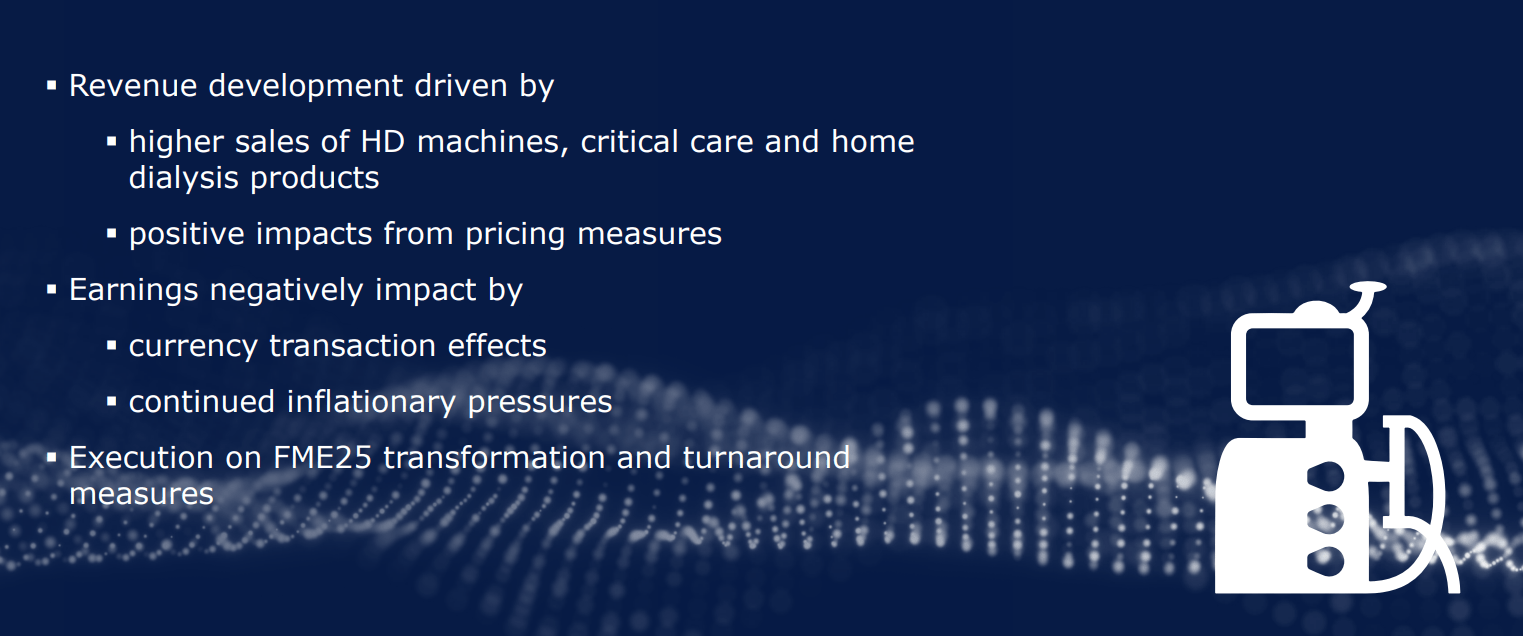

The latest results, reported in August, showcase impressive levels of organic growth driven by good treatment volumes and continued execution on its turnaround plan as well as portfolio optimization. This resulted in a narrowing of the overall guidance range.

Both revenue and EBIT were up, either slightly or significantly on a YoY basis.

{kind=link}

The reasons for this improvement were clear - the company is selling better, and at higher prices, which is an excellent combo, while also cutting labor costs, improving productivity, improving business performance, and good one-off effects from relief funding. Even with some dragging down by inflation and cost increases, these are actually good results. You're starting to see the work the company is doing paying off - even if that progress is slow, and currently still impacted by those one-offs. (Source: Fresenius 2Q23)

Care enablement saw very good trends, even if inflationary impacts were fairly heavy - but still improvements on a YoY basis.

{kind=link}

FCF conversion is increasing, and the company is seeing a flat net debt development, within the limits of its debt target corridor of 3.4x The overall outlook for the entire company, based on these 2023E trends, is a low-mid single-digit growth in terms of revenues, and a slight decline in EBIT , not the double-digit EPS drop that's being forecasted by analysts here from FactSet or similar companies. (Source: Fresenius 2Q23)

What I want to say here is that the company has the potential to actually do quite a bit better than expected, and the FY2025E targets are inclusive of an improvement in operating income margin of 10-14% as a target.

if the company does achieve even the lower end of this target range, I do not view it even close to valid for the company to trade well below 15x normalized P/E as it does today.

I want to remind you at this point that FMS results and profitability are where I would consider them unnaturally low, to where they are very likely to improve significantly on a forward basis.

{kind=link}

I do not consider these ROIC trends to be indicative of the long-term performance. There have been a significant amount of negative one-off impacts for the past few years, including but not limited to LATAM impairment in 2020, FME25 impairment in -21, Humacyte investment remeasuring in -22, and effects in 2023 from portfolio optimization.

As an investor in FMS, or FRE, you should know that both of these companies currently remain in a trough, and are likely, as I see it, to revert with time, and once these trends normalize.

Here I'm talking about cost patterns and things like inflation and the like.

And, let's move to the recent piece of news about Ozempic. Here are my comments and why I am in no way impairing my FMS or FRE targets as a result of this.

First off, let's talk about treatment costs. There's absolutely no indication as of yet, about the healthcare savings potential of using this instead of dialysis. As someone who works on processes within the healthcare field, let me assure you that this is not an area where many are eager to jump on new, expensive treatment techniques when proven techniques are available - unless you're paying for it yourself. While the successes are laudabe and positive, I would want to see a detailed analysis of actual cost savings before I go more positive on Novo as a result of this.

Second, This is not a cure for Kidney failure. It's a delay. The patients are still going to need dialysis. This does in no way take away FMS or FRE patients, it delays their introduction into the company's care environment. It's in the literal results from the study - we're talking about "signs of success in delaying the progression of kidney disease." (Source: Reuters)

Yet the markets seem to be reacting as though we're talking about a cure to kidney failure, no longer needing dialysis. That is in no way the case here.

I believe these two points "pop up" the irrational sell-off that we've been seeing in the last 24 hours with regards to these companies because not even NVO is claiming anything else.

I view the companies, Fresenius and FMS, as just as attractive as they were only a few days ago, and in fact more because of how oversold they've become as a result of this.

Let's look at the recent set of valuations and what the upside looks like at this point.

Fresenius Medical Care - The oversold status of the stock makes the upside 70%+ on a 3-year basis at below 15x P/E.

As the paragraph above says, we now have a situation where the company, now trading at 12.8x P/E, can see a 71.8% upside, or 27.5% per year, on a 14.8x P/E forecast , despite expecting almost 30% EPS growth in 2024 and another 17.8% in 2025E as its long-term strategy begins, hopefully, to pay dividends.

Fresenius medical care can easily be estimated at higher multiples based on this reversal, but estimating it at less than 15x has the sort of conservative stance or indication that I am comfortable taking here.

To be clear, we're not yet close to trough levels. Those were back in 2022, at $13-$14 for FMS. That's where I bought most of my Fresenius after the crash, and it's also why I'm still in a positive for this company at this point.

Frankly, you get over 20% annual return even if you forecast the company at a 13.3x P/E, which is even more conservative, and fairly amazing when you consider it.

{kind=link}

So this is a high-reward investment with, as I view it, very low risk despite its BBB- at this price. But I believe there is a better option for you if you're willing to go international and outside of ADR - and that's where I invest.

{kind=link}

Fresenius, the "base" company, is trading below 10x P/E, has a higher yield than FMS, and comes at an upside of almost 85% at current forecasts. It's more stable than FMS, as you can see both in terms of the earnings forecast, as well as the decline in the last few days.

This is very natural given the company's diversified state and far broader appeal given the various segments it holds.

So whenever I look at FMS and FRE, my money actually goes to FRE. It's why I hold only a small watchlist position in FMS, but why 2.66% of my commercial portfolio is in Fresenius, with more share additions today as we're back up slightly. If you follow my articles, you know I invest mostly on "up days".

So, concluding here.

I believe both FMS and FRE are incredibly oversold here. This is an article on FMS - and I believe the Ozempic impacts on the company's business will be negligible. At worst, there will be a delay when patients are moving in for dialysis, but this is not a cure. It has never been advertised as such, and I do not understand why the market in part seems to be treating it as one.

For that reason, and on that basis, this is my thesis for Fresenius Medical Care at this time.

Thesis

- I view FMS as a solid company to buy. It's a leader in the kidney care sector and owns large parts of the dialysis operations in the US market as well as on an international basis. It's BBB-rated, has a decent yield, and has a near-72% upside going forward to the next few years.

- However, due to the corporate structure, governance, and the appeal of its "parent", I consider Fresenius to be the superior investment if comparing the two. FMS is a "BUY", and it has upside - but FSNUY/FRE has a better thesis. I still view this as being the case.

- However, the company is a very solid "BUY" here - and the recent decline due to the Ozempic trial results do not faze me in the least. I show you two reasons why this company is actually unlikely to see any sort of impact as of this, at worst we'll see some delays in treatments.

- I give FMS a PT of $34/share for the long term and rate it a "BUY".

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Because the company fulfills every single one of my criteria, it is a "BUY" to me here. I'm talking about both FMS and FRE here, but this article is on FMS.

For further details see:

Fresenius Medical Care: Don't Let The Ozempic Kidney Failure Scare You Off