FMCQF - Fresenius Medical Care: Heads Don't Roll - They Run

2023-07-27 08:30:00 ET

Summary

- Fresenius Medical Care is the world's leading full-service provider of dialysis care and benefits from the entire value chain thanks to its vertical integration.

- Despite its market-leading position, Fresenius has been a poor performer, with disappointing returns on invested capital and high turnover rates pointing to internal problems.

- The article takes a look at Fresenius' operational challenges and provides an update on the company's balance sheet against the backdrop of the current interest rate environment.

- I explain why GLP-1 receptor agonists could represent a (distant) black swan for Fresenius, potentially severely impacting the company's long-term growth prospects.

Introduction

I first covered dialysis specialist and market leader Fresenius Medical Care AG & Co. KgaA ( FMS , FMCQF ) in early 2022. I was intrigued by the company's enormous footprint with more than 4,000 dialysis clinics around the world, its brand power, and its vertically integrated business that enables it to benefit from the entire value chain. However, I felt that the high leverage and weak profitability did not fit the picture of a company that clearly has an economic moat. Fresenius is struggling with operational issues and is currently in the midst of a turnaround. Management expects it to return to comparatively solid profitability by the end of 2025.

In this article, I take an updated look at the company's balance sheet and ongoing operational problems, and explain why I continue to avoid the stock - despite the improved valuation (FMS stock has lost more than 30% since my last article). And while I acknowledge that we are still at an early stage in terms of type 2 diabetes ((T2D)) "prophylaxis" (not to mention curing patients suffering from T2D), it is also worth noting the rapidly growing adoption of glucagon-like peptide-1 ((GLP-1)) receptor agonists and their potential impact on Fresenius' business.

Capital Allocation And Operational Issues

At year-end 2022, Fresenius Medical Care's net debt amounted to €7.3 billion. The high level of debt is largely due to acquisitions. For example, Fresenius Medical Care acquired NxStage in 2019 to strengthen its position in home dialysis. I won't go into detail about the advantages of home dialysis, but the potential for disruption in this segment is enormous. Considering that Fresenius' moat largely hinges on its large clinics network and their convenient locations, it is nevertheless important to diversify accordingly - even if the growing adoption of home dialysis and increasing technological progress represent a long-term risk. As I will show in the next section, Fresenius' balance sheet opportunities to make further acquisitions in this area are very limited. In addition, NxStage was acquired at a very high price - about €1.8 billion, which translates to a price-to-sales multiple of 6. FMS stock is currently trading at a sales multiple of less than 1.

Fresenius' enormous goodwill of €15.8 billion at the end of 2022 (about 43% of total assets or more than 100% of equity) suggests that the company is an aggressive serial acquirer. Although growth through acquisitions is definitely an important part of the FMS playbook (e.g. Renal Care 2006, Liberty Dialysis 2012, Cogent Healthcare 2014), goodwill should not be over-interpreted as it is primarily attributable to Fresenius' foundation in 1996 (p. 65, 2014 annual report ).

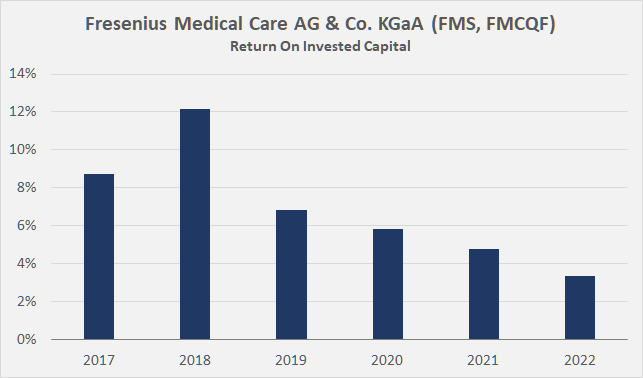

However, despite several acquisitions and its market-leading position, Fresenius is struggling. I don't think it's necessary to detail Fresenius' weighted-average cost of capital. Even under conservative assumptions, the company rarely managed to generate adequate returns on its invested capital and the performance since 2019 is really poor for what is definitely a "moaty" business:

Figure 1: Fresenius Medical Care AG & Co. KgaA (FMS, FMCQF): Return on invested capital (own work, based on company filings and Morningstar data)

{kind=link}

The pandemic hit Fresenius' Care Enablement segment (equipment and consumables) particularly hard and exacerbated existing operational problems. There is plenty of room for margin improvement in this segment in particular, as it was barely profitable in 2022. The Care Delivery segment (dialysis services) is "the horse that pulls the whole cart" (to quote Churchill ). On a consolidated basis, Fresenius expects to return to an operating margin of 10 to 14% by 2025. This wide range of forecasts underscores the uncertainties in the company's turnaround plan. I believe the company's problems, particularly in its Care Enablement segment, are deeper cultural/managerial issues. Consider, for example, that at least some of the company's long-term supply contracts with dialysis clinics did not include cost-based step-up clauses.

Fresenius' internal problems are also highlighted by the recent change of CEO. Former CEO Rice Powell (since 2013) was to be replaced by Carla Kriwet as of January 2023 . However, Powell was CEO until the end of September 2022 (p. 283, 2022 annual report ), so Kriwet apparently took over earlier, and after only few months on the job left the company at her own request due to strategic differences. The former chief financial officer of Fresenius, Helen Giza, took over as CEO after Kriwet's departure. The effectiveness of oversight by the company's Supervisory Board can therefore, in my opinion, be critically questioned, which is also illustrated by the change in chairmanship (Stephan Sturm was succeeded by Michael Sen in October 2022). It should be added, however, that the Supervisory Board openly recognizes the current challenges:

In a fundamentally sound industry Fresenius Medical Care now needs to sharpen its focus on the operational turnaround, further drive performance improvements, and focus on its core […]

Michael Sen - Chairman of the Supervisory Board

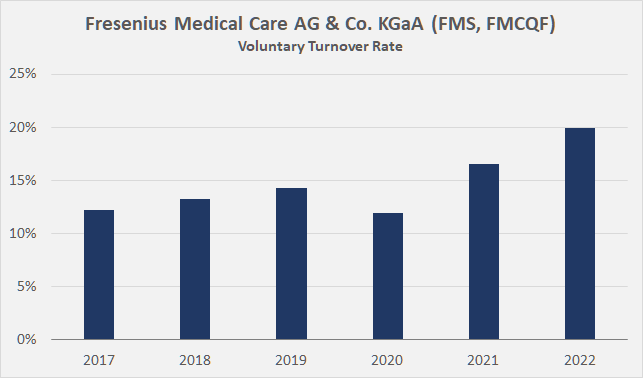

Importantly, readers should also take note of the company's steadily increasing voluntary turnover rate as a possible sign of culture and/or motivation-related problems within the company (Figure 2). The rate is calculated by dividing the number of employees who voluntarily left Fresenius over the course of a year by the number of employees at the end of the year. I attribute the decline in 2020 to the pandemic-related restrictions and the difficult labor market from the employees' perspective in that year. The long-term negative trend is intact, in my view.

Figure 2: Fresenius Medical Care AG & Co. KgaA (FMS, FMCQF): Voluntary turnover rate (own work, based on company filings)

{kind=link}

How Serious Is Fresenius' Debt Situation?

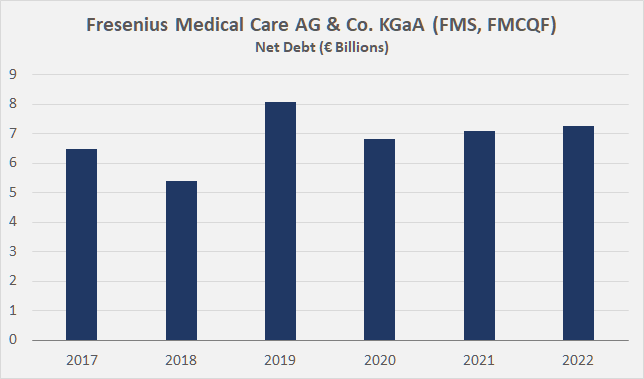

As already mentioned, Fresenius' net debt amounted to €7.3 billion at year-end 2022 (Figure 3). Despite the fact that the acquisition of NxStage was completed more than four years ago, Fresenius was not able to significantly reduce its debt. The €7.3 billion figure does not include lease obligations, which are definitely material at €4.7 billion (balance sheet value).

Figure 3: Fresenius Medical Care AG & Co. KgaA (FMS, FMCQF): Historical net debt, excluding lease liabilities (own work, based on company filings)

{kind=link}

As an aside, since the adoption of IFRS 16 (effective for reporting periods beginning January 2019), companies have to disclose lease liabilities on their balance sheets. Cash flows due to lease payments are reported as cash flows from financing activities and should therefore not be overlooked when calculating free cash flow ((FCF)).

Including lease-related cash flows, Fresenius Medical Care's baseline FCF is approximately €1.4 billion (average of 2020 to 2022, adjusted for working capital movements). The year 2020 was impacted by a significant one-time increase in payables (€1.4 billion). In 2021 and 2022, Fresenius reduces its payables and significantly increases its receivables. Based on 2020 to 2022 average revenues, FMS' free cash flow margin is 8%. This is certainly not alarming, but still a rather poor performance given the company's supposedly strong ecosystem and leading position (see above). In line with management's comments during the last conference call, the 11 analysts quoted by FAST Graphs (data source FactSet Research Systems Inc.) expect Fresenius' FCF to stagnate in 2023, but the operating turnaround should yield tangible results in 2024 and 2025.

Based on the abovementioned FCF, the company would need 5.2 years to repay all outstanding debt if it were to suspend its dividend. If lease liabilities were hypothetically included, the ratio would increase to over eight years. It will take considerable time and a lot of effort for Fresenius to get its leverage ratio back under control. The uncertainties associated with the turnaround and ongoing challenges were a key reason for rating agency Moody's to change the outlook for the long-term credit rating to negative. Fresenius' long-term debt is currently rated Baa3, the lowest investment grade rating. A downgrade to junk status does not seem unrealistic and the impact on FMS' financial stability would be significant.

Fresenius' interest coverage ratio is about six times the three-year average FCF before net interest expense, or five times 2022 FCF before net interest expense. While these are not really concerning numbers, keep in mind they are largely due to the company's low weighted-average interest rate of 2.1% (2022 year-end figure). That sounds very positive at first glance, but should be seen in the context of Fresenius' debt being 40% denominated in USD (60% in EUR, much lower risk-free rate than in the U.S.), while the company generates 70% of its operating income in the United States. I don't think it's a stretch to conclude that FMS has significant currency-related interest expense risk in the event of an appreciation of the euro. The company writes that it actively manages foreign currency and interest rate exposures (p. 72, 2022 annual report), but I submit that if the positions were fully hedged, there would be no significant savings (even ignoring the cost of hedging). I would much prefer to see the company align its debt with its segment earnings, but to be fair it should be added that management may have factored upcoming maturities into its consideration of not hedging certain positions. As always, I welcome discussion of this aspect in the comments section below.

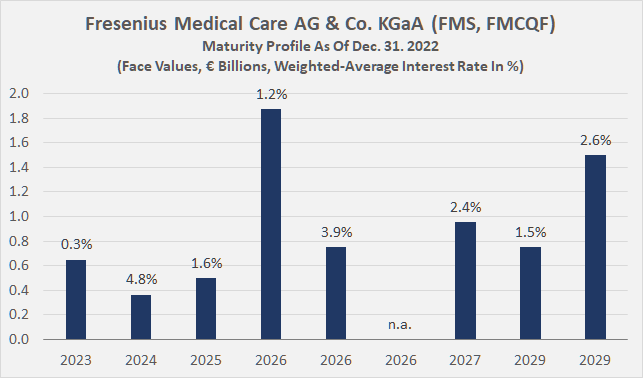

Figure 4 shows an updated debt maturity profile. Fresenius' bonds maturing between 2023 and 2026 have a weighted-average interest rate of only 1.4%. If interest rates remain "higher for longer", this would have a significant negative impact on the company's debt servicing ability. Take the example of Fresenius' recent bond placement in September 2022. 750 million euros was priced at a yield of 3.96%, about 260 basis points above the maturity-matched risk-free rate at the time. In my view, the combination of relatively high debt, upcoming maturities with low interest rates and a possible downgrade to junk level is an important risk to consider before investing in the stock.

Figure 4: Fresenius Medical Care AG & Co. KgaA (FMS, FMCQF): Debt maturity profile, as of December 31, 2022 (own work, based on company filings)

{kind=link}

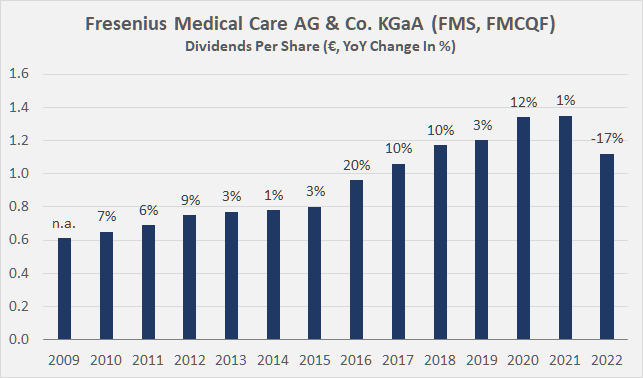

Understandably, management remains committed to maintaining its investment grade credit rating. This was expressed in the last earnings release and I believe that the dividend cut in 2023 also underlines this commitment. From a payout ratio perspective (27% of three-year average normalized FCF) and also taking into account cash outflows to non-controlling interests (€219 million, bringing the payout ratio to 44%), a dividend cut was not really necessary. Moreover, Fresenius has a very good liquidity position with cash on hand of €1.3 billion and an undrawn revolving credit facility of €2.0 billion, as well as other, smaller sources of liquidity. Nevertheless, the 17% cut clouds the otherwise solid dividend performance of the company, which has increased its dividend for 25 consecutive years (p. 7, 2021 annual report ) - despite the severe impact of the pandemic:

Figure 5: Fresenius Medical Care AG & Co. KgaA (FMS, FMCQF): Dividends per share and year-over-year growth in percent (own work, based on company filings)

{kind=link}

Concluding Remarks - And A Potential Black Swan

Over the years and decades, Fresenius Medical Care has established a market-leading position in dialysis and consequently benefits from significant scale. Thanks to its vertical integration, the company should be able to take advantage of a wide range of opportunities. There are a number of indicators that Fresenius is pulling the right levers, such as subscription-like purchase agreements and long-term contracts with hospitals, monetization of clinical observations, and strong referral incentives in its network of nephrologists via non-controlling interests. However, due to weak execution, the company's return on invested capital continues to disappoint - especially in recent years.

The pandemic had a significant impact, of course, but it would be misguided to attribute performance (or lack thereof) solely to the lockdown measures and temporary excess patient mortality. The company's problems are more deeply rooted, as evidenced by recent management changes, increasing employee turnover and, most importantly, the significant gap between actual performance and what should be expected from a vertically integrated market leader operating in a segment with steadily growing demand.

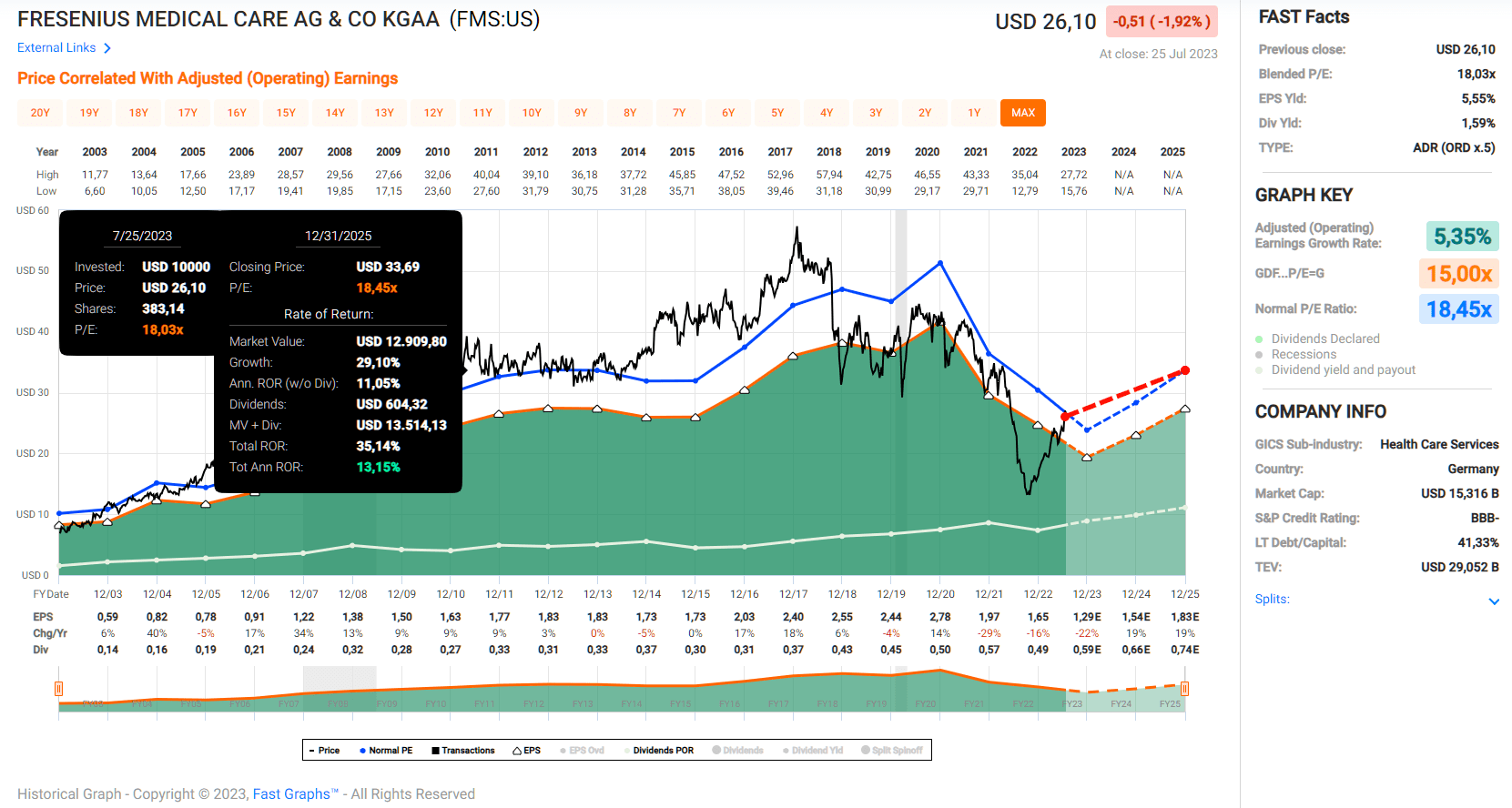

Fresenius is a turnaround investment, but at a blended price-to-earnings (P/E) ratio of 18 (Figure 6), I won't bite. The resignation of Carla Kriwet after only a few months on the job, the steadily rising turnover rate, and the poor performance despite what I consider a solid foundation suggest that the company has serious internal problems. In addition, policy-related risks should not be underestimated, especially given Fresenius' strong exposure to the United States. I would probably consider Fresenius Medical Care stock at a lower valuation, but due to the abovementioned issues, the rather poor balance sheet, refinancing risk, and likely unhedged currency risk, I prefer to stay on the sidelines. The rather high debt level also leaves Fresenius with no real optionality to make acquisitions that might be necessary in connection with the increasing adoption of home dialysis and related technological progress.

Figure 6: Fresenius Medical Care AG & Co. KgaA (FMS, FMCQF): FAST Graphs chart, based on adjusted operating earnings per share (FAST Graphs tool)

{kind=link}

Finally, I would like to point to the potential impact of GLP-1 receptor agonists on Fresenius, which could represent a distant black swan. After all, the company treats end-stage renal disease in its clinics, for which diabetes mellitus is a leading cause .

Denmark-based Novo Nordisk A/S ( NVO , NONOF ) is the current leader in the field with semaglutide, which was approved for T2D and obesity in 2017 and 2021 under the brand names Ozempic and Wegovy, respectively. Eli Lilly and Company ( LLY ) made headlines with tirzepatide (Mounjaro), which was recently approved for T2D and will likely soon be approved for obesity. The molecule, which activates both GLP-1 and glucose-dependent insulinotropic polypeptide receptors, appears superior to semaglutide. Research into GLP-1 receptor agonists for the treatment of T2D and obesity is not new, but because of their potential - now proven but still largely untapped (consider the prevalence of T2D , and the possibility of orally administered treatments and perhaps even "prophylaxis") - this area is likely to become an even greater focus in the future.

Given the significant therapeutic successes in T2D and especially also in obesity (and associated comorbidities), the potential long-term impact on Fresenius' growth prospects - not only in the U.S. but also in Asia, especially China - should not be underestimated and could represent a strong headwind, potentially exacerbated by technological advances in home dialysis and artificial kidneys. However, I think GLP-1 receptor agonists represent a risk that lies far in the future and even then will occur with a significant delay, as diabetic nephropathy typically develops only after several years of suffering from diabetes mellitus.

As always, please consider this article only as a first step in your own due diligence. Thank you for taking the time to read my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there's anything I should improve or expand on in future articles, drop me a line as well.

For further details see:

Fresenius Medical Care: Heads Don't Roll - They Run