FMS - Fresenius Medical Care: Other Stocks Still Better But Upside Exists

2023-06-01 12:41:12 ET

Summary

- Fresenius Medical Care has shown some improvement in recent trends, but still faces headwinds and pressures in its markets.

- Analysts have consistently underestimated FMS's performance, and I think the company has a potential upside of 15% annually or 44% until 2025E.

- However, the native Fresenius ticker may be a better investment due to its diversification and better fundamentals, depending on your goals.

Dear readers/followers,

Fresenius Medical Care ( FMS ) isn't my favorite Fresenius investment - I prefer the native ticker Fresenius ( FSNUY ). However, that doesn't mean that there isn't some sort of appeal in the medical care ticker. You just have to buy it cheap enough. For the past year, that's what I've been doing, albeit in small "bites". Since my last article on the company, FMS has outperformed. Over 20% since my article in January, and almost double digits since my article in April/May, which means that it has actually doubled the performance of the S&P 500 in the same time.

Seeking Alpha Fresenius (Seeking Alpha)

However, as you may see, the company is still really mostly in the negative for the longer term - and I don't see any immediate catalyst for a significant reversal. In fact, we may see a bit lower price, which could see the company's appeal in terms of valuation rise once again.

Let's digest 1Q23 and see where we are - the company reported these results back in early May.

Fresenius Medical Care - plenty of pressures and headwinds remain

This is not an easy company to invest in at this time. The company's results during and after COVID-19 have not been a pleasant read, with 2022 declining nearly 16% on an adjusted EPS basis, and 2023E is set to decline a massive 64% on an adjusted EPS basis. The company is now BBB- rated and comes in with a market cap of around $12.6B.

This company is showing strain and decline in most of its current relevant markets, relative to its business and overall macro trends.

TIKR.com FMS margins (TIKR.com)

{kind=link}

While improvements are on their way, including simplified governance, a global operating model with two segments, and excellent financial reporting structures with better transparency than before, it doesn't change the fact that it will likely take time for this company to really turn things around. The company's capital allocation policy is disciplined, and the company is targeting ROIC improvements through better use of capital, but these improvements will take time to actually land.

The best that can be said for Q1, which is also why we've seen some climb in the share price, is that trends are improving. For Care delivery, the volume trends are up, and for enablement, we're seeing a strong foundation. This top-line trend did not translate into profitability though - operating margin continues to decline, though at a slower pace than before due to improved business performance, and phasing of product sales.

The company is also likely not yet done with its legacy portfolio optimization. FMS did confirm its 2023E outlook, expecting top-line growth and profit declines/pressures to continue here.

{kind=link}

Turnaround will be some time coming here. Inflation is doing its thing, as is the US labor market, which is heavily impacting results. This is normalizing, but it's not normalized yet, nor is it going fast in any way. The company also performed some write-offs, impacting P&L trends for the company, but this is creating increased sales and demand for its home hemodialysis machines.

Inflation is the reason why the care enablement segment is down - without inflation, the entire segment would have been growing, based on slight volume growth of around 3% YoY.

There are a lot of arguments based around "the best that can be said". The best that can be said for Fresenius is that its 1Q results came in with positive FCF for the quarter - €2M, compared to negative FCF for the YoY results.

Fresenius is, as the credit rating implies, also at the upper range of its leverage target corridor. Should this rise another 0.1-0.3x, it's doubtful to me that they would be retaining their investment grade credit.

{kind=link}

The company expects 2023 results to be down - but also makes sure to give the 2025E targets, which are what we should be looking at if we want to invest in this company. By 2025E, the company expects and targets an operating margin of at least 10%, but around 14% on the higher end, marking a 200-600 bps improvement from the current levels, which also should trickle down to the net income margin.

The company has been cheaper - a lot cheaper, as it happens. That was when I bought most of the shares I own, which is why I'm slightly positive here. It's still cheap, but it's not as cheap, and the question becomes how the company will handle an EPS decline in this year which is set to eclipse what we saw during last year's results.

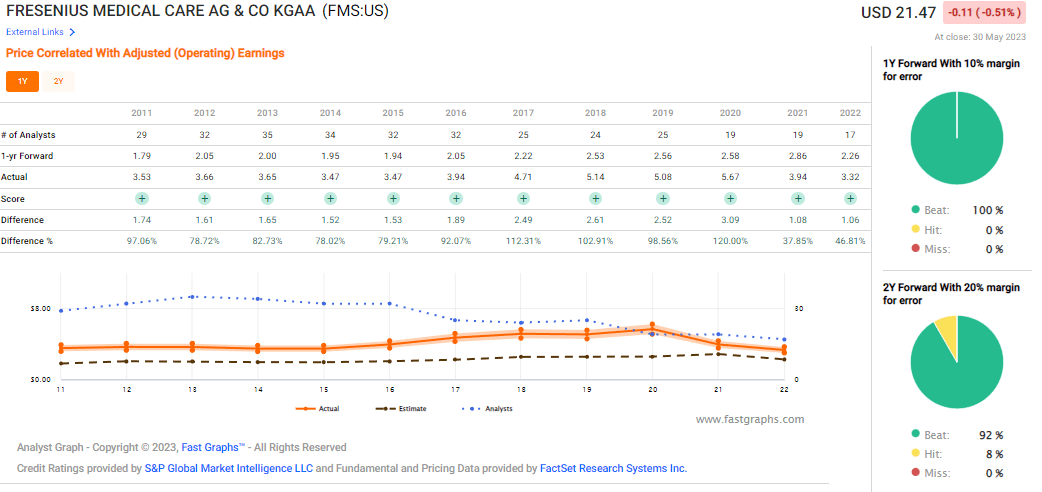

However, there are some positives that I will not let you leave this article without having seen. Analyst accuracy, for one. Analysts are forecasting the company to drop massively. Would you like to see how these analysts have usually fared, with a 10-20% margin of error?

FMS Analyst accuracy (F.A.S.T Graphs)

{kind=link}

This is the first company in the history of my analyzing and forecasting where analysts so chronically underestimate a company that the company is able to provide a perfect 10-year 10% MoE analyst-beating record. Something to consider/be reminded of, for sure. Fresenius Medical Care is likely to perform much better than expected.

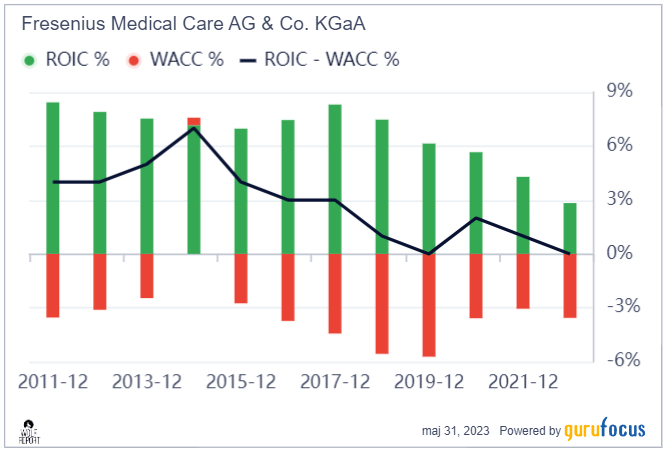

The company has experienced a massive margin decline over the past 1-2 years - but this hasn't impacted the fact that the company does remain ROIC-profitable, if barely at this particular time.

Fresenius ROIC/WACC (GuruFocus)

{kind=link}

Large institutional investors that follow the company are pretty much split down the middle. Several of them have reduced or sold out completely since December of last year, but many others have been added. The common denominator is that since that time, those that sold did not get almost 41% RoR during a very problematic market. The clearly correct stance for Fresenius at the time, which I have held myself, was therefore "BUY".

I still do see problems and risks with the company. A couple of things we do need to keep our eyes on include wage/labor growth costs as well as how the clinic closures across the US impact the company business, volumes, and earnings. Wage inflation during 1Q23 alone was 4%. The company blames unfavorable 1Q trends on the Omicron variant - I think it's somewhat more complex than that, and I do expect wage costs to increase going forward. The company also closed 51 clinics in 4Q and 1Q together.

Market treatment growth should look better in 2Q than in 1Q, but for a real reversal, we'll have to wait for longer - 2024-2025 would be more likely. The company's current revenue/net income trends do not look that favorable, with low margins - but that's set to improve going forward, which means that this could still be the time to buy the company.

Fresenius Medical Care Revene/net (GuruFocus)

{kind=link}

Let's look at company valuation.

Fresenius Medical Care Valuation - Plenty to like

The upside for this company in case of reversal remains massive. That's also why I'm pretty positive on the company, despite all of the challenges and things to look out for that I just mentioned.

Analysts do not think this company will outperform. The NYSE ticker targets from 4 analysts are actually below the company's current share price, which expresses in my opinion the short-term nature of these targets. Something to keep in mind, of course, is that I don't think FMS is bound to outperform near term - so if you buy, you'll want to stick to this company for some time and let it recover. if you don't have the time for that or want the income, then invest in something else.

At a normalized 15x P/E multiple this company has an upside of 15% annually, or almost 44% until 2025E. That's lower than the last 2 articles where I reviewed the company, but analysts have also cut their estimates significantly. They don't expect the decline in 2023 to be made up by the company for the 2 years after, which I believe to be somewhat "too negative", given that this company has outperformed estimates 100% of the time for the past 10 years.

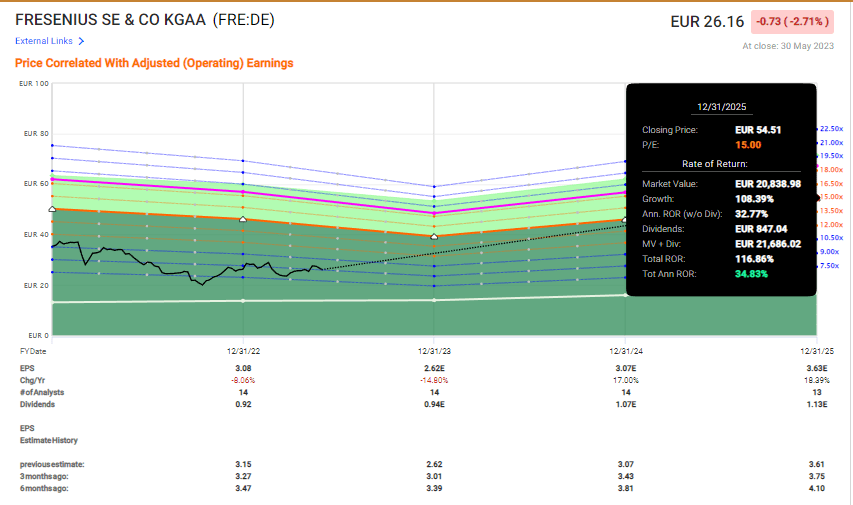

DCF isn't usable when the company is this volatile - and there is, I believe, still much to be said for the upside that FSNUY offers instead of FMS. Take a look at the native FRE ticker upside.

Fresenius upside (F.A.S.T graphs)

{kind=link}

This is the major reason that I'm investing in Fresenius instead of the Medical care wing. The native ticker is better diversified because it's not just dialysis/kidney, it has a better mix of more appealing segments that can complement one another in a downturn, and in some ways, COVID-19 has actually been a tailwind for parts of the Fresenius business. Also, FRE has BBB credit and a higher yield.

Because the company is significantly worse fundamentally than Fresenius itself, I continue to view FMS as an inferior investment pick to the main company. And that attraction is not changed due to an improved governance structure that I mentioned in the initial parts of the article.

Still, if you do want that clear investment into kidney care and dialysis with a focus on the US market, then FMS is the way to go for you. There is market leadership here, and the potential of more. Leverage isn't perfect, but it's not too high and likely to drop, and there is capital appreciation potential.

And, to be clear, you have that perfect outperformance rating, which is something the native ticker FRE doesn't have from analysts.

My investment goals dictate to me that the native FRE ticker and Fresenius is the better investment for me - for you, FMS might be the investment that's better. In either case, both companies are "good" - and the choice of which one makes the most sense for you is of course up to you.

Here is my thesis for the company - and I'm not changing the PT here.

Thesis

- I view FMS as a solid company to buy. It's a leader in the kidney care sector and owns large parts of the dialysis operations in the US market as well as on an international basis. It's BBB- rated, has a decent yield, and has a near-50% upside going forward to the next few years.

- However, due to the corporate structure, governance, and the appeal of its "parent", I consider Fresenius to be the superior investment if comparing the two. FMS is a "BUY", and it has upside - but FSNUY/FRE has a better thesis.

- I give FMS a PT of $34/share for the long term and rate it a "BUY".

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Because the company fulfills every single one of my criteria, it is a "BUY" to me here.

For further details see:

Fresenius Medical Care: Other Stocks Still Better, But Upside Exists